FatCamera/E+ via Getty Images

Afya (NASDAQ:AFYA) has been on a run since I last covered the stock (see here and here), benefiting from a strong quarter and positive news flow despite the inflationary headwinds. A recent 6-K filing seems to have flown under the radar but is worth noting – Brazil’s Ministry of Education has granted Afya authorization to add 64 medical seats for its Itabuna-based medical university FASA (Faculdade Santo Agostinho). This isn’t a game-changer but it entails an additional ~R$141m to Afya’s value using the implied per-seat valuation of the UNIT Alagoas/FITS Jaboatão deal, which isn’t insignificant.

Meanwhile, the fundamentals aren’t bad either – Afya’s core undergrad medical education business continues to outperform, while specialization courses are seeing a positive recovery as well. Together, these business segments should more than offset the competitive challenges in digital services. Afya stock trades below peers Cogna Educação (OTCPK:COGNY) and Anima (OTC:ANNMF) on FY24 earnings estimates, despite maintaining a lower risk/leverage profile; net, I remain bullish here.

FASA Gets 64 More Medical Seats

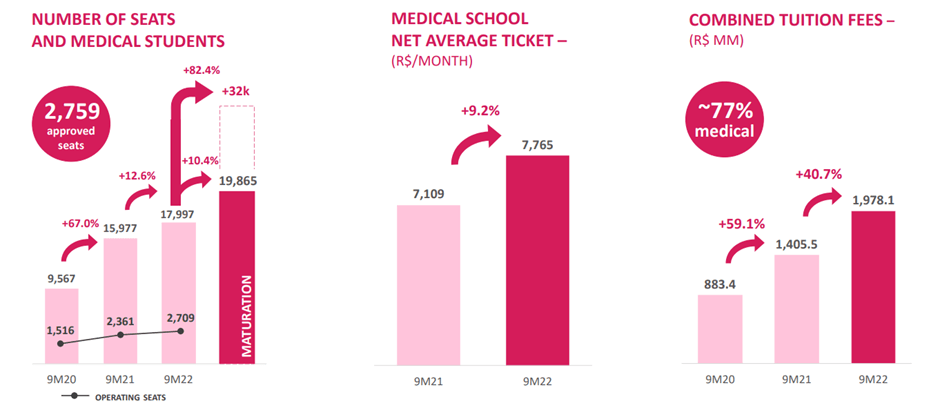

Afya closed out 2022 with more good news, filing a disclosure that the company had been authorized to add 64 medical seats to its FASA medical university in Itabuna city, Bahia. This was a long time coming – recall that the license was first awarded as part of the 2014 ‘Mais Medicos’ program to address shortages of doctors across the country’s interior and city outskirts. The initial allocation was for 85 seats, with an option to add another 100 seats. With the latest approval of 64 seats, Afya now has a total of 149 authorized seats at the facility and 36 remaining in its allocation. In aggregate, Afya will have massive scale in its medical business post-deal, with 2.8k of approved seat capacity, reinforcing its status as the largest medical player in Brazil.

The expansion likely came as a positive surprise to investors – it has been a long time since the last approval at FASA and should lead to upward earnings revisions heading into the Q4/FY22 results. The most likely scenario is for these seats to come into operation in early 2023, in my view; I am penciling in Q2 as the base case for now. Given the profitability of FASA seats, the valuation implication is likely positive as well. Using comps from Afya‘s most recent UNIT Alagoas/FITS Jaboatão transaction of R$2.2m/seat would imply ~R$141m of incremental market value.

On Track for a Top-Line Beat in FY22

Coming off a strong Q3, Afya looks poised to outperform an unchanged FY22 guidance bar. Organic growth at the core medical undergrad business remains the key highlight (overall +9.2% YoY increase in ticket ex-acquisitions), complemented by a continued education business that also outpaced inflation. Digital is the only blemish for Afya – heightened competition in key residency prep courses Medcel has weighed on revenue growth, resulting in a disappointing +1.3% YoY ex-acquisitions on a YTD basis.

Afya

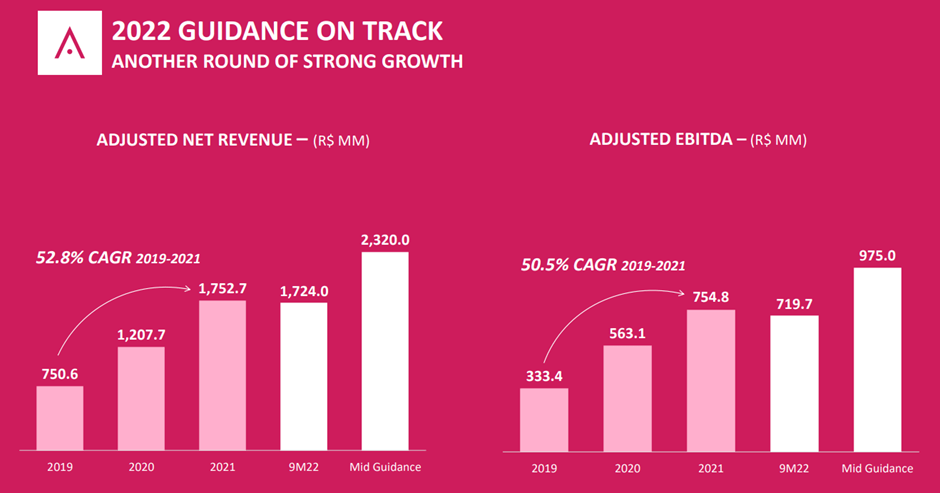

While the steep -23% YoY decline (flat QoQ) in the prep course student base is concerning, there is hope of a recovery in Q4, given the H2 intake typically starts in the fourth quarter. And with YTD revenue from specialization courses already up by ~47% YoY, recovering from a COVID-driven negative trend (due to practical class interruptions), momentum is on Afya’s side. Also helping in the near-term will be the shift towards medical grad courses (via IPEMED) and away from other underperforming acquired operations, which should boost overall pricing. All in all, the reiterated FY22 adj revenue guidance range of R$2.28bn-R$2.36bn seems well within reach, particularly having already achieved three-quarters of the guidance mid-point YTD.

Afya

Margin Performance Has Been Mixed but the Guidance Bar is Low

The profitability side is less cut and dry. On a YTD basis, adj. EBITDA margin is down ~4%pts on an organic basis and ~3%pts including acquisitions amid a wave of headwinds. These include operating deleverage from the lower prep course student base and inflationary pressures across the corporate expense base. Additionally, the integration of recent acquisitions such as Unigranrio is also temporarily weighing on margins, while digital services profitability is likely underperforming the group average as well. Relative to the adj. EBITDA (ex-acquisitions) guidance range of R$935m-R$1,015m, Afya has already made significant headway on a nine-month basis, so the bar for a profit beat isn’t high from here.

While management hasn’t focused its guide on FCF generation, I would also keep an eye out here. Capex needs have been elevated over the last year amid higher requirements for campus maintenance and the buildout of new medical and continuing education campuses. The capex cycle should wind down by 1-2%pts YoY for FY23, though, supporting higher cash flow generation going forward. With the capital allocation framework focused on inorganic growth, more cash should drive a higher earnings growth algorithm over the mid to long-term.

On Track for More Seat Expansion as the Growth Story Continues

With the latest round of seat expansion at FASA greenlighted by the Ministry of Education, Afya looks on track for more upside in the coming months. At ~ R$2.2m/seat (per the UNIT Alagoas/FITS Jaboatão deal economics), the additional 64 medical seats could add R$141m to Afya’s market value. This isn’t a game changer, but it does highlight Afya’s growth runway as it continues to drive further seat expansion over time.

Meanwhile, the main undergrad medical education and specialization courses businesses are seeing a healthy post-COVID recovery, reinforcing Afya’s existing (and growing) competitive edge. The ongoing P&L pressure at the smaller digital services business remains a blemish but the stability and growth from the core businesses should more than offset the headwinds here. The stock trades at a relative discount to Cogna and Anima at ~9x FY24 earnings and should re-rate as the Afya growth story continues to play out.

Be the first to comment