PhonlamaiPhoto

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note’s date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Apparently Warren Buffett Can Do Tech

As everyone knows, Warren Buffett is no good at technology investments. He doesn’t understand them, he says, they’re best avoided. Er, except his huge bet on Apple (AAPL), which has been and is likely to continue to be a major winner in our view. And, just in case you care to write Apple off and say, well, that’s just a consumer brand he’s buying there, nothing to see here, move on? There’s the recent big buy into a sector so technical that it scares off most technology investors, being semiconductor fabrication.

As everyone also knows, Buffett doesn’t do technical analysis, because it’s “voodoo”. Er, except he managed to buy a goodly chunk of TSMC (NYSE:TSM) stock right at the 78.6% Fibonacci retracement of a prior huge move up – a perfectly timed technical buy.

We covered all this in our recent note on TSMC, which you can read here. We rated the stock at ‘Accumulate’, meaning, build up a stake slowly, being disciplined with the size and price of each addition. This has so far proven a righteous call.

Cestrian TSMC Article (Seeking Alpha)

The company printed its earnings yesterday before the market open – and the earnings weren’t wonderful. Q4 showed solid growth (although revenue missed consensus), peak gross margins (meaning major pricing power and better than normal utilization of existing inventory), but, a hit to cashflow from increased capex. In the cyclical world of semiconductor fabrication this is a heads up that the cashflow yield is about to fall. Pricing power and inventory utilization fall (so gross margin is down and operating margins are squeezed), and capex is up (so unlevered pretax free cashflow margins fall).

But the stock has been so beaten up of late that the name rebounded anyway. The cyclical nature of semiconductor production will hardly be news to long-term TSMC investors and so if you believe the economy will hold up okay, ergo long-run end-user demand for chips will hold up – and if you believe that TSMC’s undisputed leadership of the merchant manufacturing market will hold up (we’d like to hear a reason why it won’t), then as a long-term hold we remain bullish on this name.

We Move From Accumulate To Hold

If you have a very long term view we see no harm in buying now, but for us the stock is now in our Markup Zone where we believe late money will flow into the name, particularly if this market recovery continues and folks decide that semiconductor fabrication isn’t so toxic a category after all. So we change our rating to Hold in anticipation of gains to come.

Risks and Risk Management

Again, the guidance is the risk here. The company missed Wall St consensus this quarter but arguably got away with it. That’s not a repeatable trick so, if you own the name be prepared for some volatility. As regards risk management, you will have your own preferred methods of course. A stop just below that Wave 2 low on our chart can protect you against a market dump. The approach we’ve taken in staff personal accounts is to be (1) long the stock and (2) long Jan 2025 $80 calls and (3) long Jan 2025 $80 puts. By weight of capital, substantially net long. The puts and calls were purchased before earnings as a way to hedge the outcome. As it happens the calls are in the money and the puts out of the money but net-net this was a profitable hedge. With long expiry and limited theta burn to worry about for a little while we plan on holding both the calls and the puts as the market continues its faltering recovery.

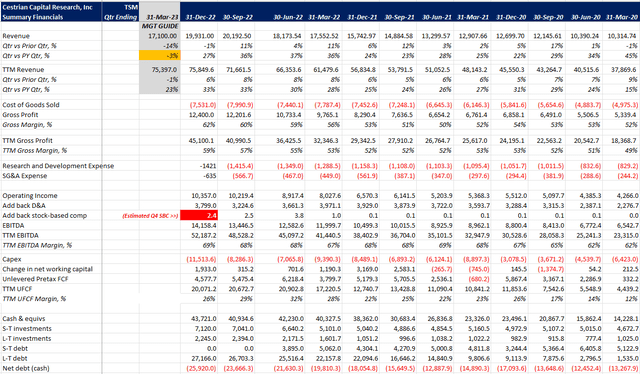

Fundamentals

TSMC Fundamentals (Company regulatory filings, YCharts.com)

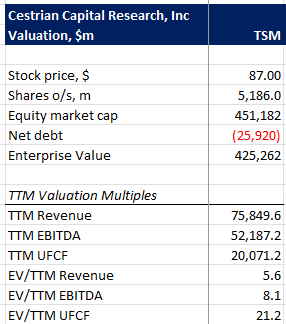

Valuation

TSMC Valuation (Company regulatory filings, YCharts.com, Cestrian Analysis)

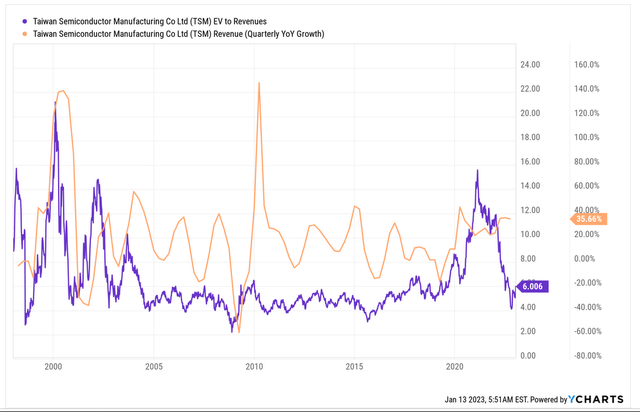

The revenue multiple you’re being asked to pay for TSMC is in the normal long-run range – it’s neither cheap nor expensive right now. Below we show that multiple vs. the prevailing rate of revenue growth.

TSMC Valuation History (YCharts.com)

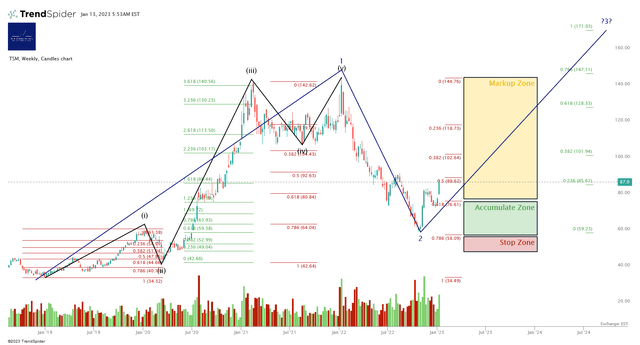

Chart outlook as we see it:

TSMC Chart (TrendSpider, Cestrian Analysis)

You can open a full page version of this chart, here.

So – we have a Hold Rating, sit back and see what happens.

Cestrian Capital Research, Inc – 13 January 2023.

Be the first to comment