Justin Sullivan

AMD’s Enlarged Product Suite Is Likely To Gain Share

Advanced Micro Devices, Inc. (NASDAQ:AMD) investors have suffered in 2022, with its total return down nearly 60% YTD, as the bears accurately pointed out its overvaluation. Despite that, AMD’s 5Y total return of 43.7% suggests that earlier bulls have benefited tremendously from its leadership against Intel’s (INTC) woes.

However, with the well-deserved pummeling in 2022 as management’s optimism was misplaced, investors need to know whether there could be a “deeper hole” for AMD to sink further. Or, could the company successfully overturn its bearish bias as it cements its leadership against Intel in high-performance computing and data center/hyperscaler workloads?

Its integration of Xilinx’s FPGA-powered AI inference engine and Pensando’s DPU has proffered the company significant advantages in accelerating specialized data center workloads. It has also boosted its capability in AI training and inferencing, given the increasing focus of its customers on leveraging AI and machine learning.

As such, AMD appears well-positioned in 2023, as it aims to continue gaining share against Intel in the data center segment. Accordingly, DIGITIMES highlighted that Microsoft (MSFT) has “fully upgraded” Azure to Milan-X EPYC processors in H1’22, powering AMD’s market share higher.

Furthermore, it added that the leading US and Chinese hyperscaler will continue driving the server market in 2023. Notably, they have “all adopted servers powered by AMD’s EPYC CPUs in 2022.” As such, DIGITIMES estimates that AMD should continue gaining share against Intel, with “the share of AMD-powered servers estimated to grow to over 17% in 2023, while that of Intel-powered ones will slump to below 75%, down from around 77% in 2022.”

But, Don’t Ignore The Threat From Arm-Based Processors

Despite that, investors shouldn’t ignore the increasing threat of Arm-based processors. Notably, DIGITIMES also cautioned that “Arm-based processors will begin to penetrate into the server market.” Furthermore, it highlighted the moves by Nvidia (NVDA) and Ampere, as the leading hyperscalers, such as Amazon (AMZN), are “working keenly on developing new cloud and HPC solutions with Arm-based processors.”

Accordingly, the leading hyperscaler, AWS, has also introduced its new Graviton3E chip, a marked improvement from its previous version. Accordingly, the company claims that:

Making its own chips will give customers more cost-effective computing power than they could get by renting time on processors built by the likes of Intel Corp., Nvidia Corp., or Advanced Micro Devices, Inc. – Bloomberg

Given the increasing threat of a global recession, which could impact enterprise IT spending further, Amazon’s move to demonstrate further cost savings to its customers is critical. In addition, leveraging its massive IaaS scale could allow the company to justify the R&D and production costs of customizing its own chips. As such, it could threaten the market share of the x86 architecture, including AMD, as it needs to justify its valuation by growing faster than the market.

Hence, we believe investors need to watch these developments closely, even as AMD is confident in its enlarged suite and serviceable available market.

Is AMD Able To Outperform Its Peers?

With the PC market likely remaining in the doldrums in 2023, AMD’s ability to continue growing in its data center segment is vital. Despite that, investors should expect the decline in desktop and notebook shipments to improve in 2023. However, they are still expected to post negative growth, indicating that AMD needs to move even faster in its data center segment.

Hence, the question is whether the market has reflected these headwinds.

AMD last traded at an NTM EBITDA of 13x, well below its 5Y average of 26.6x. However, we believe investors would be remiss in expecting AMD to be re-rated toward its 5Y mean anytime soon.

Given the macro headwinds and industry-specific challenges, AMD needs to execute better to justify its valuation. Why?

AMD remains priced at a steep premium against its semi peers’ median EBITDA multiple of 8.4x (according to S&P Cap IQ data). As such, there’s a clear growth premium embedded in AMD’s valuation.

We also gleaned that Wall Street analysts expect the company to post an adjusted EPS growth of 5.1% in 2023. However, analysts expect the semi industry to post an 11.5% decline in earnings in 2023. Hence, AMD is expected to deliver much healthier earnings growth against its peers, implied in its valuation. Therefore, investors adding AMD at the current levels need to have high conviction over its execution amid macro and industry challenges.

However, investors should also parse whether AMD’s price action has reflected these headwinds and if the reward/risk favors buyers at the current levels.

Takeaway

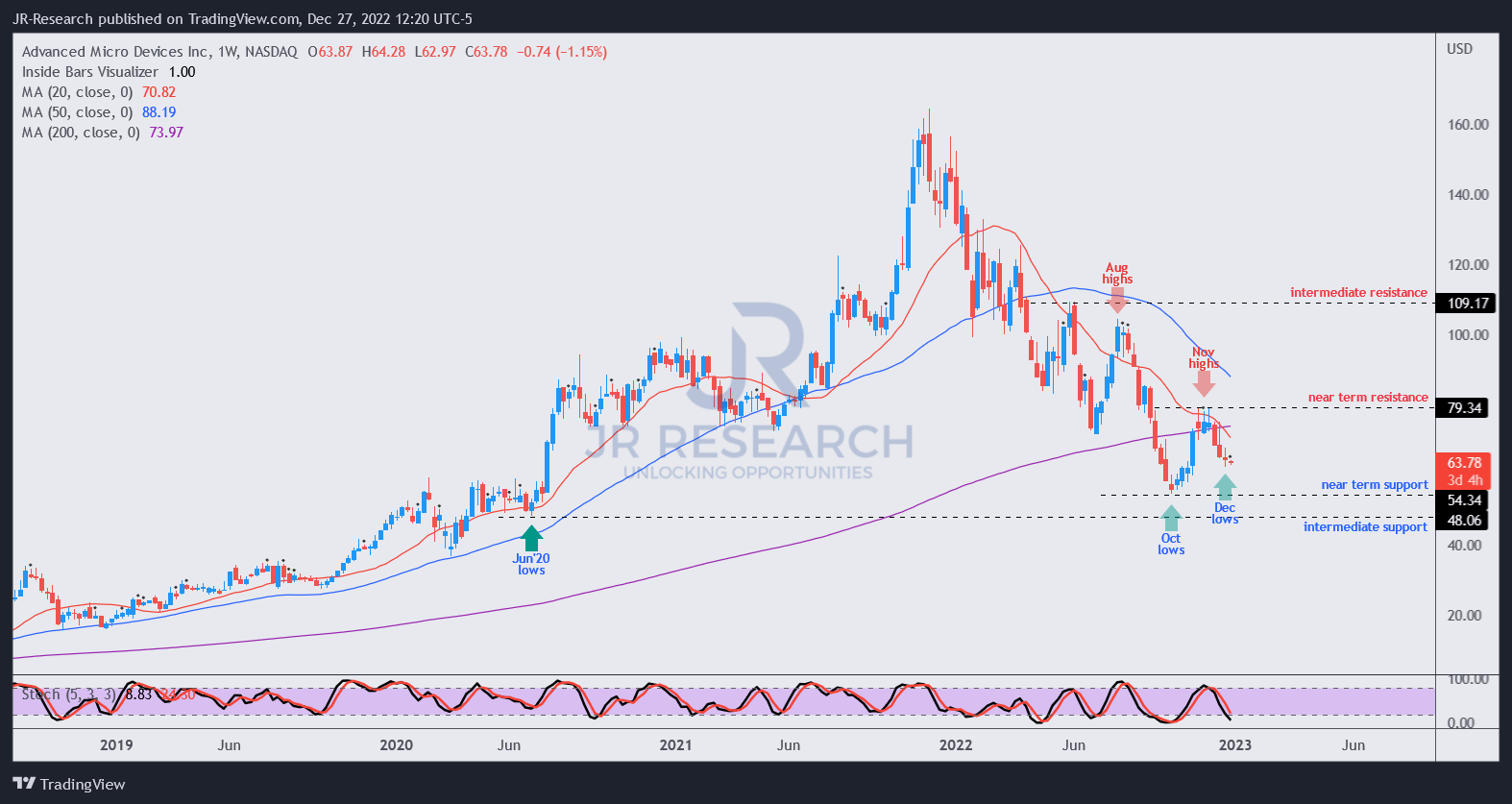

AMD price chart (weekly) (TradingView)

AMD’s medium-term price-action remains bearish. We also highlighted in our previous article that its buying momentum could fail at its 200-week moving average (purple line).

Hence, we urged investors to wait patiently for a pullback first to assess the conviction of buyers in sustaining its recovery.

We gleaned that while AMD still needs to retake the robust resistance zones at the $80 level, buyers could be ready to stanch further downside from here.

As such, we assessed that investors can consider adding at the current levels, with an eye toward a further re-test of its October lows.

Therefore, consider adding progressively to avoid getting caught up in a perilous “falling knives” scenario.

In favor of the bears: A still premium valuation, medium-term bearish bias, and worsening macroeconomic headwinds that could impact enterprise IT spending further. AMD’s earnings estimates are still expected to outperform the industry. Hence, a worse-than-expected recession could torpedo its recovery hopes.

In favor of the bulls: De-risked estimates and a much lower relative valuation than its 5Y average. In addition, AMD is expected to continue making gains against Intel with its next-gen EPYC CPUs. Moreover, the decline in the PC market should subside in 2023, mitigating the downstream consumer headwinds that have engulfed AMD in 2022.

Rating: Revise to Buy (Previous: Hold)

Be the first to comment