RiverNorthPhotography

Earnings season is generally a good time for bargain hunters to go shopping, and this latest round of earnings has proved no different, producing bargain buying opportunities in stocks such as Stanley Black & Decker (SWK) and V.F. Corp. (VFC). That’s because disappointing results can lead to analyst downgrades and market over-reactions, producing long-term buying opportunities for value investors.

This brings me to Advance Auto Parts (NYSE:AAP), which appears to be one such opportunity, whose price is now trading well below its 52-week high of $244. In this article, I highlight why long-term value and dividend growth investors ought to take a look at this bargain name, so let’s get started.

Why AAP?

Advance Auto Parts is a leading parts provider for the automotive aftermarket, serving both professional installers and DIY customers alike. It operates over 4,700 stores and 312 Worldpac branches primarily in the U.S., Canada, and Puerto Rico. AAP also serves 1,329 independently owned Carquest branded stores, furthering its reach to more customers and markets. Over the trailing 12 months, AAP generated $11 billion in total revenue.

AAP benefits from its scale, reach, customer base, and brand. The company’s scale is evident in its large store footprint. This gives it a distinct advantage over smaller rivals and even the online juggernaut, Amazon (AMZN) because customers are more likely to visit an AAP store when they need a part, due to its in-store expertise, higher inventory turnover and availability of parts. These strengths are reflected by Morningstar in its recent analyst report:

Despite Amazon’s recent efforts to sign distribution agreements with manufacturers, we anticipate that incumbent retailers will be able to defend their privileged market standing because of their in-store services and ability to offer several categories of needed components on demand.

Hard parts are increasingly complex and can vary significantly depending on the model year and selected options on any vehicle. The purchase and installation of such products can be daunting, and the support provided by trained in-store sales staff is difficult to replicate through do-it-yourself videos and online assistants. Advance’s tool loan offerings add additional value, as part installations sometimes require a specialized instrument that is better borrowed from Advance than purchased for a single-use application.

Aside from the lack of personalized service, customers looking to replace a failed critical component often need the part immediately in order to regain reliable use of a car or truck in commuting or business. Few digital retailers are able to combine depth of inventory with speed of delivery.

Meanwhile, AAP’s share price has taken a beating in recent days, falling from the $210 level from the middle of this month to $181. This was driven by nearly flat sales growth of just 0.6% YoY and a 0.6% decrease in comparable store sales compared to the prior-year period. This compares unfavorably to peer O’Reilly (ORLY) which saw a 4% revenue growth over the same period. However, this could be due more to ORLY’s heavier reliance on inflation-sensitive lower income customers. As a reference, the DIY segment represents 60% of ORLY’s customer base compared to 40% for AAP.

While AAP may continue to see challenges in the near-term, especially as cost inflation pressures DIY customers, I see the long-term growth thesis as being intact. That’s because AAP continues to expand into new locations with additional stores, signaling a bullish long-term outlook by the company. It’s also investing in more efficient scale, which could introduce higher profitability over the long-run. These factors were noted by management during the recent conference call:

Rounding out our top line growth initiatives, we’re executing our new store opening plan. In the quarter, we opened 43 new locations, including the recent opening of our flagship store in downtown Los Angeles. Our California expansion is already contributing to share gains in the West. Year-to-date, we’ve opened 78 new locations and remain on track to deliver our annual guidance of 125 to 150 new stores and branches.

We’re streamlining and simplifying our supply chain to improve service and reduce cost. We continue to rollout a single warehouse management system across the Advance and Carquest DC network and are on track to complete the implementation by the end of 2023. We’ve also begun activating elements of our labor management suite of tools across our DC network and are beginning to see productivity benefits.

Meanwhile, AAP maintains an investment grade rated BBB- balance sheet and it’s significantly grown its dividend over the past couple of years. It currently yields a healthy 3.3% at the current price, and the dividend is well-protected by a 40% payout ratio.

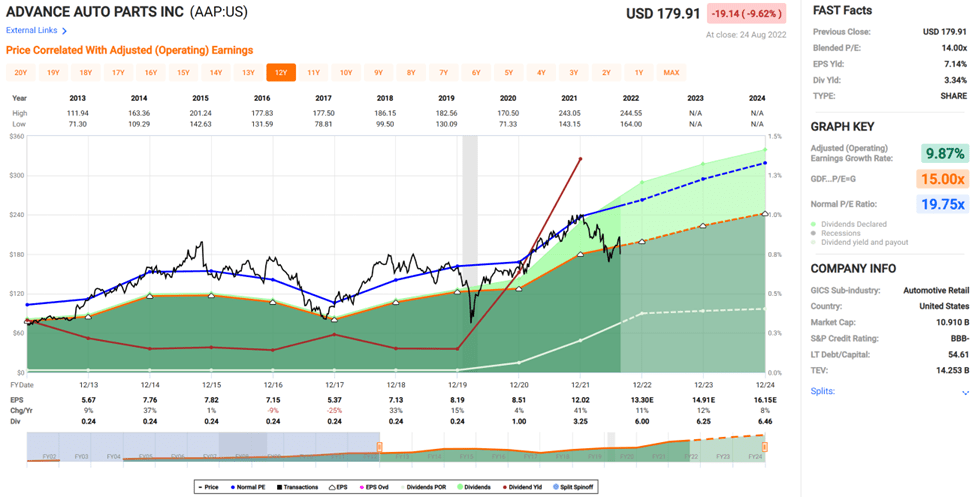

I see value in AAP after the recent drop in price. At the current price of $181, AAP trades at a forward PE of just 13.6, sitting well below its normal PE of 19.8 over the past decade. Analysts expect 8% to 13% annual EPS growth over the next 3 years, and have a consensus Buy rating with an average price target of $214, while Morningstar has a $234 fair value estimate. This translates to potentially strong double-digit total returns.

AAP Valuation (FAST Graphs)

Investor Takeaway

Advance Auto Parts is a great value play in the auto parts retail industry. The company has a strong long-term growth thesis, driven by expansion into new markets and investments in supply chain efficiency. However, it faces near-term headwinds from cost inflation pressures, which could impact DIY customers. Nonetheless, at the current price of $181, I see significant upside potential in AAP for patient investors.

Be the first to comment