AleksandarGeorgiev/E+ via Getty Images

Adaro Energy (OTCPK:ADOOY) is not a household name in the US. It was last in the US mainstream business news in 2016 when it bought all of BHP’s coal production in Indonesia. But the company is seeing stunning demand not only at home but from its main export markets in Asia.

Unknown to most Americans: Indonesia is the largest exporter of coal in the world; Adaro is its second largest miner. It is a low-cost, truly “under-the-radar” mining company that is enjoying unprecedented growth. It should provide strong earnings in the coming year amid rising coal prices, fresh EU demand, and aggressive hoarding by India and China. It might be worth familiarizing yourself with the ticker.

King Coal’s Interregnum: Rising Demand / Flattish Investment

We have entered a new interstitial period. Geopolitics has punctured Globalization 2.0 and the Ukrainian war now has the world frantically re-circuiting its energy sources in what will be a far less efficient, more costly way. US LNG and Indonesian coal will now cross oceans to Europe. The Russian gas that was barred from nearby Germany will eventually flow the course of the Eurasian landmass to coastal East Asia. In 2022, Indonesian coal exports to Europe reached 4 to 5 million tons –far and away its largest export year to that continent in history (which typically only averaged 500,000 tons). The world is scrambling, hand over fist, for coal as Europe’s energy security crisis upends the chessboard.

Global coal demand hit at an all-time high this year, with global use set to have risen by 1.2% in 2022, surpassing –for the first time– 8 billion tons in a single year and beating the previous record set in 2013. Despite sharp declines in certain mature markets, the demand for coal in Asia is rising, even accelerating. China, India and Indonesia are all expected to hit production records.

Despite firm prices and nice margins, however, coal producers are keeping it “tight to the vest.” They are not investing in export-driven coal projects. This reflects caution among investors and mining companies about the medium- and longer-term prospects for coal.

By actively crimping investment in the dirty fossil fuels, the now “universal assumption” that wind and solar will seize the baton and quickly shoulder a sizable use share has added a new “uncertainty.” The dilemma: if renewables don’t reach their potential within the next 2 – 3 years, the world will be left with a far bigger energy supply gap, with far more expensive coal, oil, and natural gas. Everything begins in mystique and ends in politics…

India and China still see coal as the basis of their modernity. China, by far the largest coal consumer, accounts for 53% of global demand. Its consumption increased by 4.6% in 2021. India’s consumption has doubled since 2007. As the world’s second-largest consumer, India’s use increased by 14% in 2021. It has strongly defended its intent to keep using coal as the quickest path to economic growth.

Coal is the cheapest of fossil fuels, with thermal coal (the kind burned by power plants) costing approximately $15 per million BTU, compared with $25 for crude oil and $35 (global price) for natural gas. For governments this is key. With its re-opening commencing, China is actively stockpiling, mindful of the heat waves that hit the southern coastal cities in September 2022, and bent on avoiding the full outages that plagued it in 2021.

This explains why coal demand was pushed to an all-time high this year.

Indonesia: A Port in the Storm

Indonesia recently stated that it will raise its coal production to 694 million tons to fulfill both export and domestic supply demands (mostly for electricity). According to the Indonesian Coal Mining Association, Indonesia is seeing more demand from China and India as well as European countries, which only started importing from Indonesia aggressively in April.

Despite a population of 276 million and a growth rate of about 5.2%, Indonesia still only has a GDP of about $1.2 trillion (and a per capita GDP of about US$12,000). The country is in the early innings of its capitalist rise, and suffers none of the indebtedness of the more mature markets. In fact, Indonesia posted a $3.9 bln budget surplus in the recent Jan-Sept nine month period as tax revenues soared.

Financially speaking, Indonesia is insulated from the US asset bubble and a long recession in Europe. It is helped by today’s commodity inflation and the broad efforts to find fresh supply chains. Last quarter FDI was up 63% year over year as money diverts from China to “friend-shoring” ASEAN countries like Malaysia, Indonesia, and he Philippines. Unlike the late 90s, it is not exposed to the vicissitudes of hot money western investment. In terms of stock ownership, foreign ownership accounted for only 28% of Indonesian equities in early 2022, down from 37.5% in 2013.

Adaro: Impressive Growth at a Sound Valuation

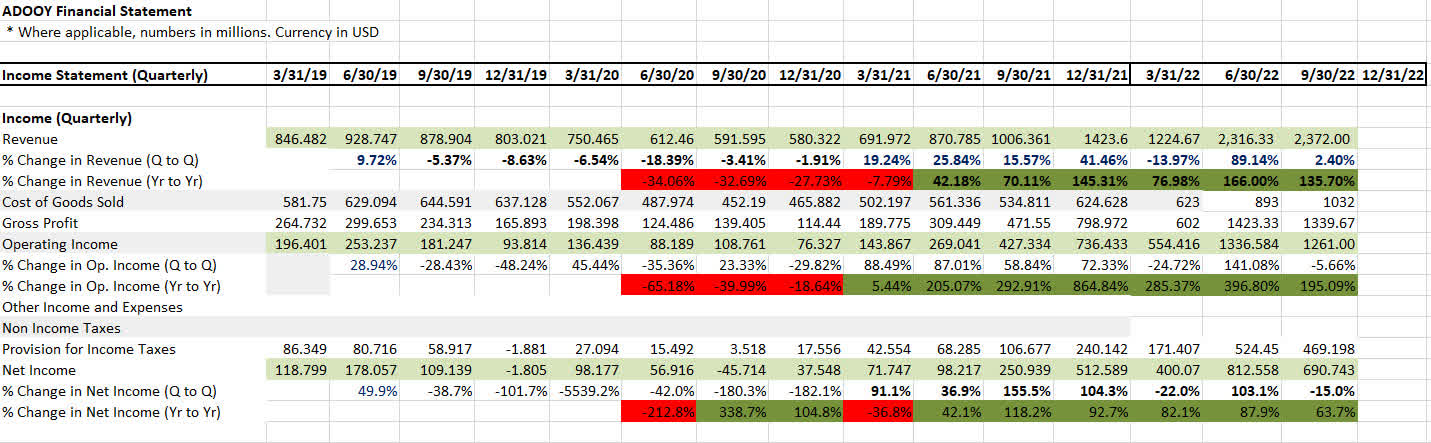

Hit hard during the pandemic, Adaro Energy has since has experienced a stunning jump in top-line revenue and net income:

- Q32022 revenue was up 135.70% year over year, from $1.01 billion to $2.37 billion.

- Year over year, Q3 Operating income was up 195% and net income 63.7% (from $250.9 million to $690.7 million).

- Its end-of-3Q cash balance weighed in at $3.3 billion, up 122% higher year over year.

Adaro Energy Revenue and Operating Income (Author)

On December 22, Adaro Energy Indonesia announced an “historically high interim dividend” of $500 million (approximately 93 cents a share), representing an increase of 67% from 2021. Slated for January 2, 2023, the dividend increase is indicative of just how successful 2022 has been for the company.

Unlike most US equities, Adaro Energy offers the American investor access at a very low valuation. It trades at a 3.16 P/E; a 1.7 P/S; a 1.68 P/B; an EV/Assets of .65; and an EV/EBITDA of 4.29.

The company sits well outside our asset bubble. ASEAN stopped being trendy with US investors 10 years ago as genuine advancements in biotech, cloud computing and phone-centric mobility kept buyers at home. Recently, however, investors have started to look again at the under-bought region. Foreign direct investment in Indonesia rose 63.6% on a yearly basis in the third quarter.

Technically speaking: in mid-November Adaro bounced off of a $10.82 support/resistance line that had been established in the Spring. November 14 saw a sharp reversal in momentum (as evidenced by the MACD and Chande Momentum Oscillator). Upper resistance stands at $14.02, hit on September 9th.

Adaro_2022 Price Action Chart (Adaro_2022 Price Action Chart)

Risks and Prospects for the Coming Year:

Coal prices swung widely in 2022. Though the benchmark Newcastle contract was recently at $400 per ton, about 145% higher than December 2021, the volatility of this market remains the biggest risk to Adaro’s profitability. (It is not a coincidence that Adaro’s September peak and November bottom both occurred when the Newcastle contract went from $457 to $320 a ton.) A ceasefire in Ukraine, very cool weather in India, or a substantial slowdown in China (due to a knock-on effects of a European AND US recession) could all adversely impact its coal prices.

However, 2023 is likely to be another good year. And unlike US producers, Adaro doesn’t suffer from intense regulatory scrutiny by Jakarta or from ESG pressures by its mainland Asia buyers. More importantly, it is an adroit player with an eye for diversification. The company’s investments in power plants and coking coal helps protect against volatility in the thermal coal market. When its net income soared more than 500% in 2021, it scaled into renewable energy, building out several 200-megawatt capacity solar-powered plants with over retired mining sites in Bintan.

Adaro is also building hydropower plants and aluminum smelters. Its subsidiary PT Adaro Minerals –itself the best performing Indonesian ticker this year– has announced plans for around US$1.1 billion in capital expenditure this year, most of which will go into an aluminum smelter project. Powered by hydroelectric dams the smelter is situated in North Kalimantan in the new “green industry district.” It expects to begin commercial operation in Q1 2025 with an ultimate capacity of 1,500,000 tons, and cater to Asian demand for car parts and EV components.

2023 will likely be a tumultuous year, with a further fall (and bottoming?) in US equities, and a roiling energy crisis in Europe which could send the continent into a two year recession. Given its low valuation, low beta, promising growth and high dividend, Adaro is – at $12.56 – an investment that allows you to step away from all the uncertainty.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment