da-kuk

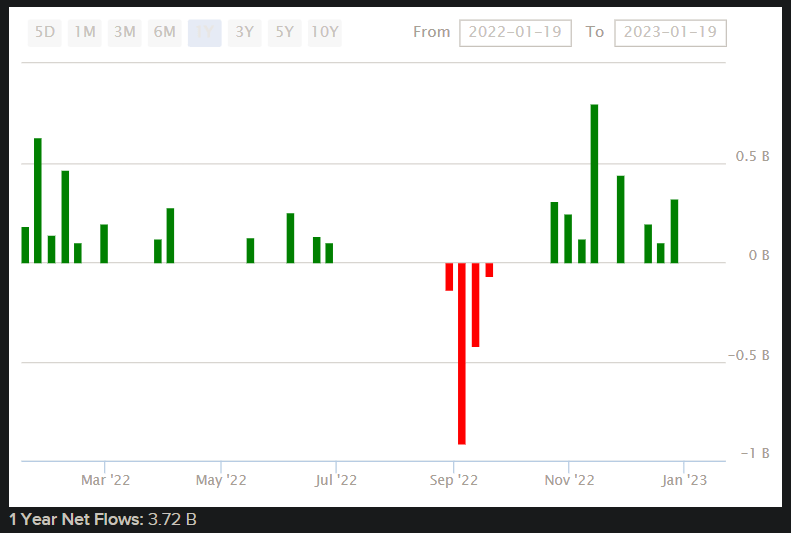

iShares MSCI ACWI ETF (NASDAQ:ACWI) is an exchange-traded fund that provides investors with exposure to a broad range of international developed and emerging market companies. The expense ratio is 0.32%, and net assets under management were $19.2 billion as of January 20, 2023, making ACWI one of the “mammoth” iShares funds (i.e., popular). Net fund flows have remained positive over the past year or so, when equities have generally been falling in the face of various risks (elevated inflationary pressures globally, rising interest rates, elevated equity risk premiums, etc.). I last reviewed ACWI in November and May 2022. I continue to retain my bullish stance on ACWI’s prospects.

ETFDB.com

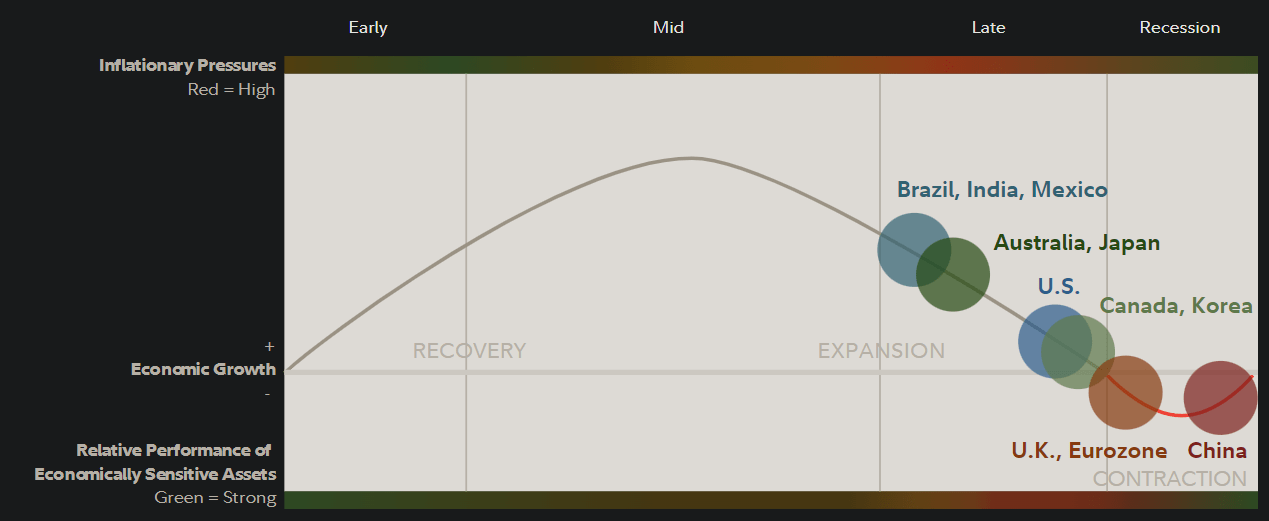

Eventually, one would think that equity risk premiums would begin to contract, likely just as inflationary pressures abate and long-term yields (i.e., risk-free rates) begin to contract too. The world is heading toward a contractionary period, although it is still not certain as to when the downturn will truly “kick in”, or how deep any contractionary period will be. The chart below from Fidelity illustrates current business cycle positioning per country.

Fidelity.com

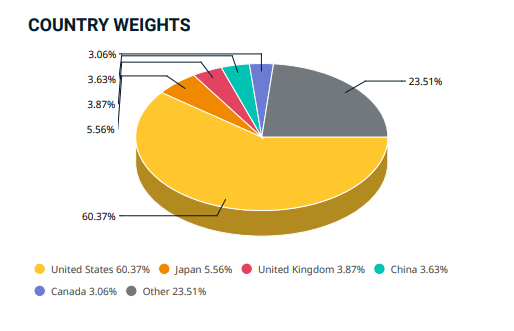

Bear in mind that while ACWI invests globally, the fund has recently found itself invested in the United States with approximately 60% of fund assets. This is owing to the naturally high weighting that U.S. equities achieve, as the markets in the United States are deep, liquid, and broad. The fund invests in accord with its benchmark index, the MSCI ACWI Index, which as of December 30, 2022 also referenced allocations to Japan (6%), the U.K. (4%), China (4%), and Canada (3%). It is a U.S.-led index, and thus ACWI is a U.S.-led fund, but there are plenty of global exposures that collectively serve as a helpful diversifier.

MSCI.com

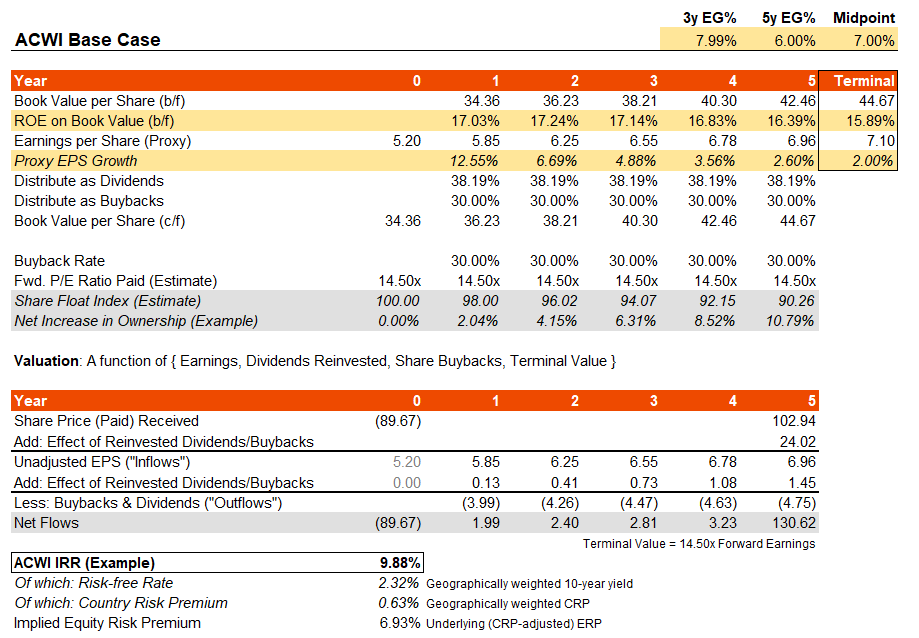

The benchmark index also reported trailing and forward price/earnings multiples of 16.32x and 14.50x, respectively, with a price/book ratio of 2.47x. That implies a forward one-year earnings growth rate of 12.55%. Morningstar meanwhile suggest a three- to five-year average earnings growth rate of 10.88%. That is probably optimistic; I will assume a five-year average of about 6%, such that my terminal year growth rate falls to 2%. My return on equity falls from 17% to 15-16%. The net IRR looks fair, with a strong underlying equity risk premium of about 6.9%.

Author’s Calculations

Bear in mind that the top 10 holdings, in reflection of the fund’s U.S.-centrism, shows that ACWI is invested heavily in companies that have engaged in strong buyback programs in the past. Yardeni Research has reported a buyback rate of well over 50% of operating earnings for the S&P 500, which is also heavily weighted toward similar names. For ACWI, I have assumed a buyback rate of circa 60% (the U.S. weighting) of 50% (a rough estimate of the forward buyback rate). Buybacks may well be higher than this; or lower. We do not know, but it makes sense to assume some flexible buybacks going forward as in the past. A higher assumption would boost the underlying IRR.

As the fund-weighted risk-free rate is quite low, and even the country risk premium (using data from Professor Damodaran) is quite low, the underlying ERP is healthy. The headline IRR per the projection is almost 10%, indicating that ACWI is not over-valued, and could even be under-valued. In fact, I would argue that the long-term earnings multiple could increase from the present forward P/E multiple to 14.50x to circa 18x. That is, on the basis that long-term risk-free rates hold roughly steady, long-term nominal earnings growth is at least 2% (that’s the inflation target of central banks, so it makes sense as a minimum growth rate to perpetuity), and an ERP of just over 5% globally.

I would not assume a higher earnings multiple in this case, but it gives me some comfort in case buybacks come in stronger than anticipated. If corporates are buying back shares that are, on average, not too expensive relative to reasonable expectations of value, these buybacks can help create value for the portfolio.

On the basis of my 6% five-year earnings growth forecast (apparently under consensus) and holding most other assumptions within the bounds of normality, ACWI looks set to continue to produce strong returns over the long run. I previously covered ACWI in early November 2022, and the fund has out-performed the S&P 500 so far (8.99% price-only return, vs. the S&P 500’s move of 5.43%, according to Seeking Alpha data at the time of writing). I am not sure if the out-performance will continue, but the global diversification component makes the fund especially attractive independent of relative value.

It is important to remember that given ACWI is so diversified (2,314 holdings as of January 20, 2023) it is essentially a “global equity beta” fund. You do not buy ACWI for out-performance as such. However, I like ACWI, I remain bullish, and this bodes well for global equities more generally.

Be the first to comment