Orla/iStock via Getty Images

ACADIA (NASDAQ:ACAD) is an old standby that has been a serial disappointment. In this article I discuss the past, present, and future of its once promising mega-blockbuster therapy NUPLAZID (pimavanserin, selective serotonin inverse agonist). In the dreams of bulls.

That is the story; however Acadia has another round pending with the FDA. Trofinetide in treatment of Rett syndrome looks like a possible consolation prize. I will discuss it. Lastly, I take a look at Acadia’s financials and how they measure up from an investment perspective.

NUPLAZID is the once and not future king of therapies.

NUPLAZID’s past

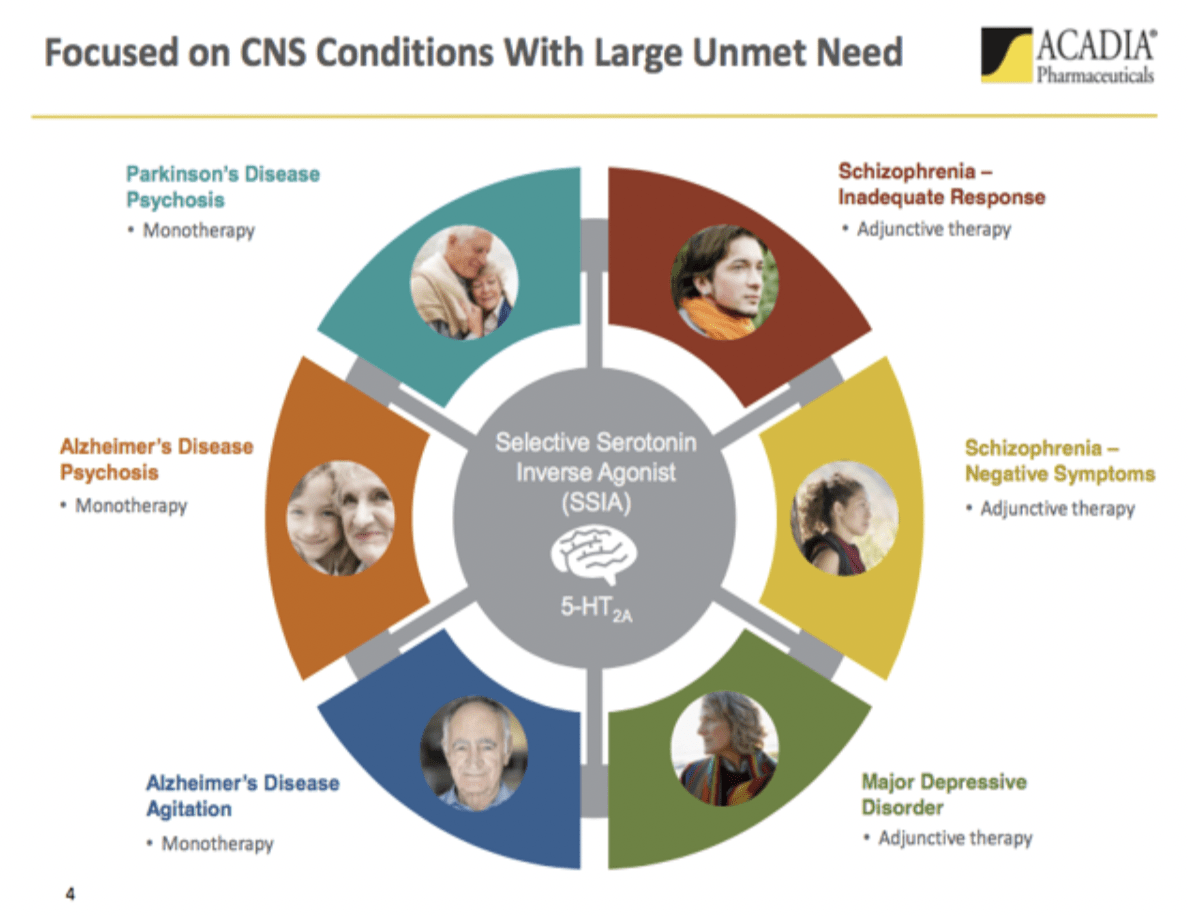

My first, 07/2017 Acadia article, “Acadia: Order For Central Nervous Systems In Need”, included the following graphic:

Seeking Alpha

Acadia trade-named pimavanserin, the selective serotonin inverse agonist to which the graphic refers, as NUPLAZID. I closed the article with the following:

To me the most compelling aspect of the Acadia saga is its laser focus on solving some of medicine’s knottiest conundrums. I wish it the very best of luck; I want to be on hand ready to get in full bore once it shows that it is a true contender for restoring order to central nervous systems in need.

Well, it has not had such good luck. It has been awful. The indications above have dropped off one by one. The latest failure came in 08/2022 when the FDA batted down its Alzheimer’s disease psychosis with a CRL.

NUPLAZID’s present

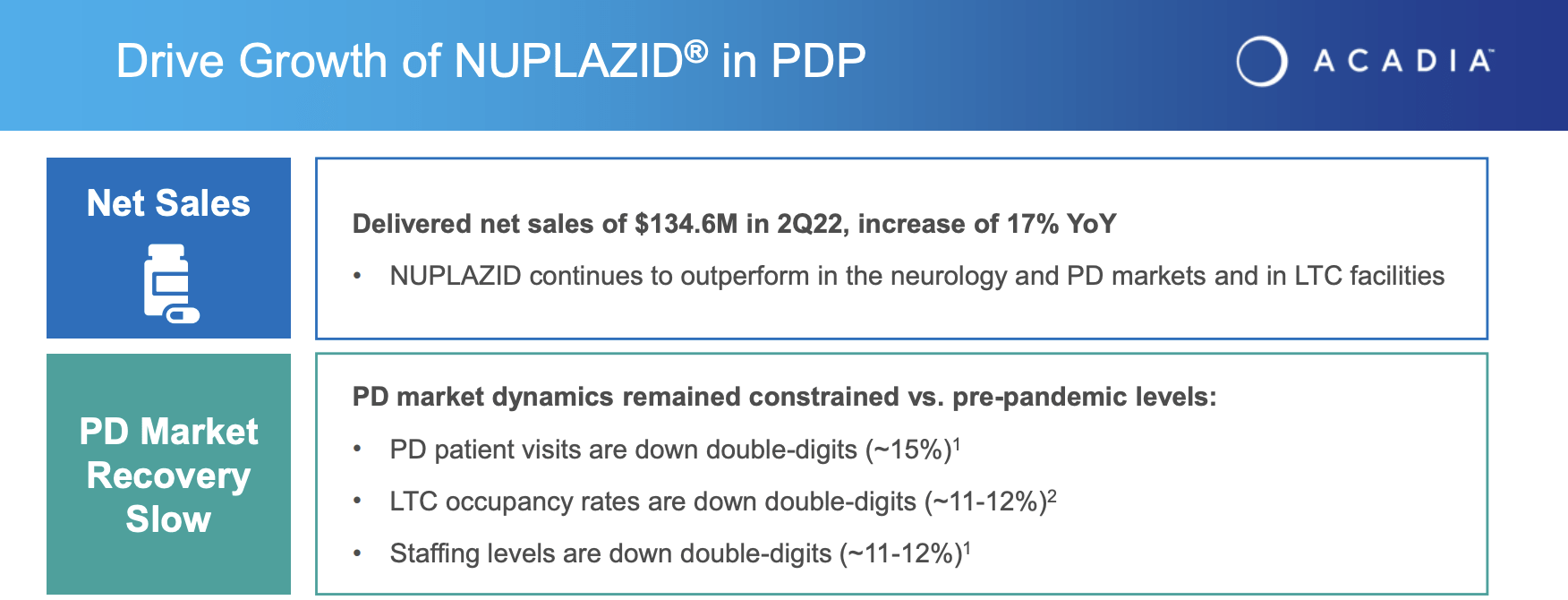

Today as I write on 10/18/2022, NUPLAZID’s sole FDA approved indication is for hallucinations and delusions associated with Parkinson’s disease psychosis [PDP]. The PDP market is a smallish subset of Parkinson’s disease patients estimated at 15%–30% with visual hallucinations and 4% with delusions.

In a 2020 JPMorgan presentation, Acadia estimated this market at ~125,000, far the smallest of the addressable markets for the various indications it was seeking. The slide excerpt below from Acadia’s Q2, 2022 earnings presentation provides the latest information on it current sales:

Acadia IR

NUPLAZID’S future

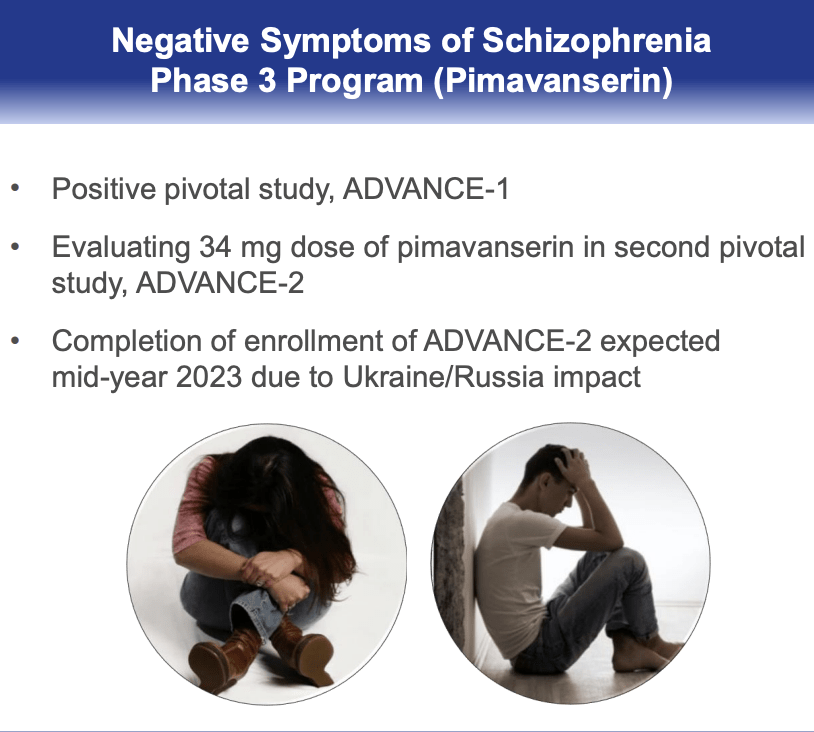

Beyond its approved Parkinson’s disease indication, Nuplazid has one more shot on goal. It is still pursuing NUPLAZID’S negative symptoms in schizophrenia indication. Its status is shown by the Q2 earnings presentation slide excerpt below:

Acadia IR

Acadia’s latest webcast includes extensive discussion of this. A September 19, 2022 appearance at the Cowen 2nd Annual Novel Mechanisms in Neuropsychiatry Virtual Summit by CEO Davis and CSO/Head of Rare Diseases, Kathy Bishop, devotes its initial 17 minutes to this program.

The two takeaways that I noted were that data readouts may be delayed into early 2024 and that the size of the market was ~5X that of PDP. That tells me that any new revenues are probably a 2025 story. I am also mindful that the FDA recently CRL’ed Minerva’s (NERV) recent application for roluperidone in treatment of negative symptoms in schizophrenia.

I discussed Minerva’s filing and its previous tussles with the FDA at length in a recent article. By the time 2025 rolls around, this indication may have more competition than it does now.

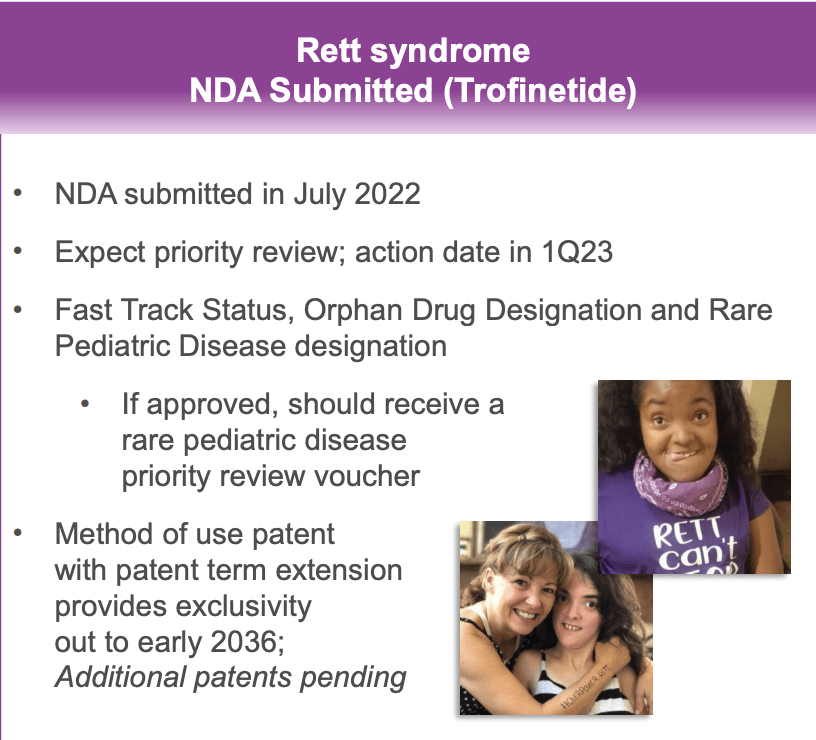

Beyond NUPLAZID, Acadia has one other late stage candidate, its recently filed NDA for Trofinetide in treatment of Rett syndrome.

On 07/18/2022 Acadia filed an NDA for Trofinetide for the treatment of Rett Syndrome. Trofinetide is a molecule for which Acadia acquired North American rights in 08/2018 bolstering its over reliance on NUPLAZID. I discussed the deal in detail in “Acadia’s Big Scores”.

Acadia’s Q2, 2022 earnings presentation slide 7 excerpt provides the following status report on Trofinetide:

Acadia IR

At the time of its acquisition Acadia was touting the Rett Syndrome market as a $500 million opportunity. An 06/22 global Rett landscape article points to the crowded field of some 15+ companies vying to pursue this market. Unfortunately, the actual report rests beyond a hefty $1,500 paywall which exceeds my research budget.

When I checked clinicaltrials.gov on 10/18/2022 for phase 3 trials treating Rett syndrome, I encountered 11 results. Four were Trofinetide trials. Two had not posted information since 2011 or earlier; three others were apparently abandoned.

Two Anavex trials, NCT04304482, a phase 2/3 trial of ANAVEX2-73 oral liquid in female children age 5-17 with an estimated completion date of 12/2022 and NCT03941444, a phase 3 trial of ANAVEX2-73 of adults with Rett had an actual study completion date of 09/2021.

The results in this second trial have been controversial. However ANAVEX2-73 has received fast track, rare orphan disease and rare pediatric disease designations (slide 20) from the FDA just like Trofinetide.

Accordingly Acadia’s NDA takes on a mantle of major importance. If the FDA issues another CRL it could allow Anavex to hopscotch Acadia. One recent Anavex article describes the situation:

Last week saw the FDA accepting Acadia Pharmaceuticals’ (ACAD) new drug application of Trofinetide for Rett syndrome. Acadia Pharmaceuticals had reported good results for this drug candidate. The FDA has granted priority review to Acadia Pharmaceuticals’ application, and is to decide on the application by March 12, 2023. If the FDA were to approve Trofinetide, then that would mean Anavex 2-73 may lose orphan drug designation for Rett syndrome, and may in any case face competition. There seems to be one advantage, highlighted by Anavex, and that is that Anavex 2-73 has a more favorable safety profile.

During its Cowen virtual summit referenced above (minute 28:30), Acadia couches its stomach upset issues as tolerability rather than safety issues that can be handled. With its NDA pending and the stakes being high, Acadia bulls are certainly optimistic that the FDA will agree that the issues are manageable.

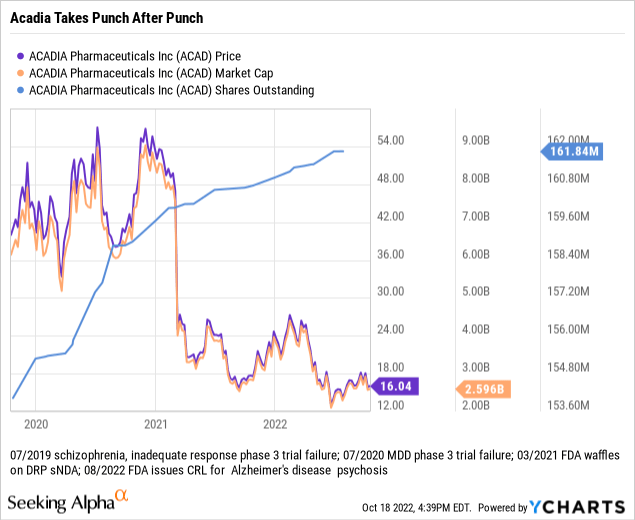

Acadia has had a rough road as its NUPLAZID indications have dwindled.

The stock price chart below summarizes the Acadia story all too eloquently. Its share price and market cap have taken leaden punch after leaden punch.

The big palooza, dropping Acadia’s market cap from high single digits billions of dollars to <$3 billion, was the FDA derailing its dementia related [DRP] indication in early 2021. The stock has not recovered from this. It will likely not do so unless it sweeps the table by scoring a Rett approval on its assigned 03/12/2022 PDUFA date and following up with positive data and FDA action on its negative symptoms of schizophrenia trial.

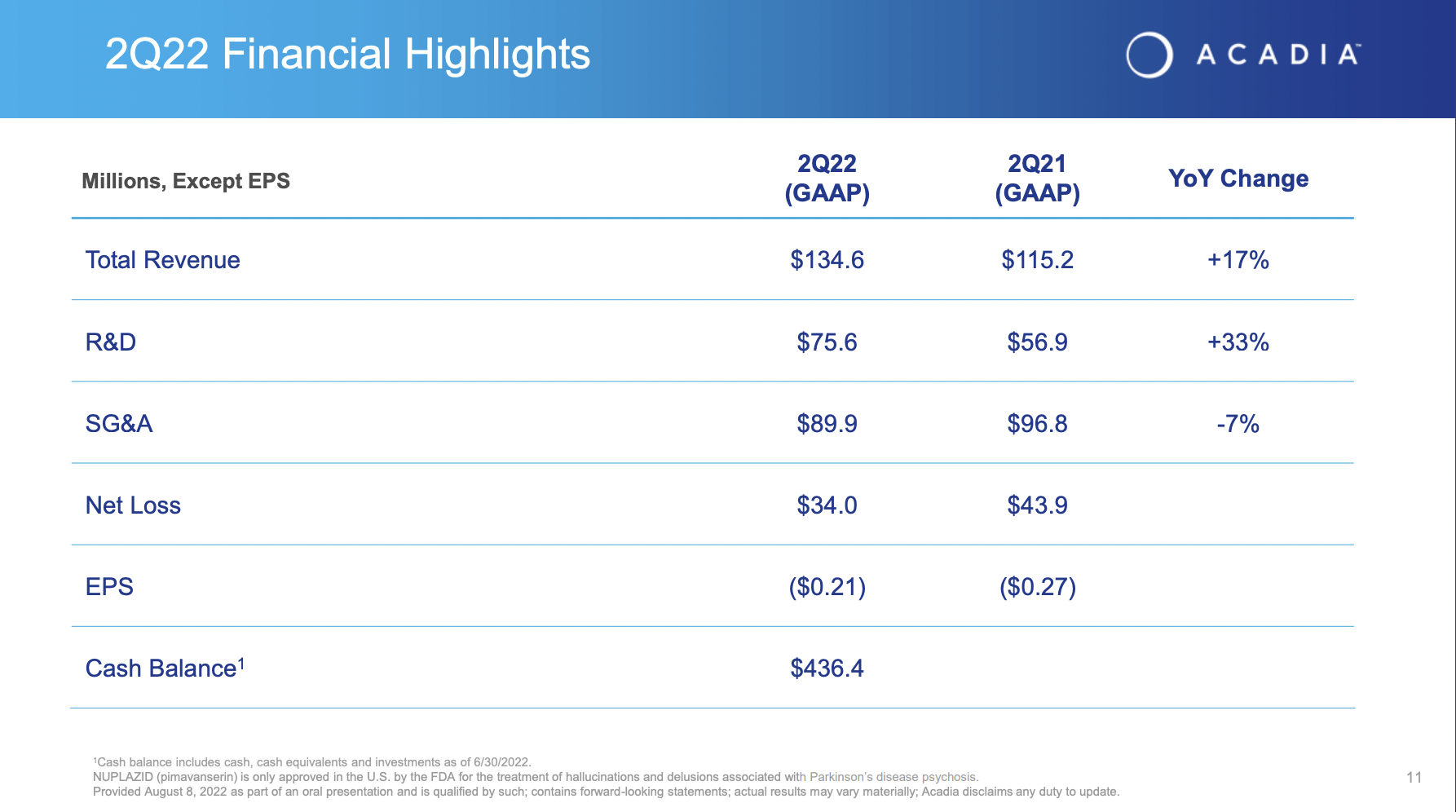

Consider its history and its future. Its operations are a disaster as shown by its Q2 financial highlights slide below:

Acadia IR

These kinds of losses were tolerable when waiting for near term FDA approvals on diverse indications. Now that Acadia’s pipeline has been whittled down to two late stage candidates, things are a bit dicier. Take a look at Acadia’s Q2, 10-Q background disclosure below:

We have incurred substantial operating losses since our inception due in large part to expenditures for our research and development activities and more recently for our sales and marketing activities related to the commercialization of NUPLAZID. As of June 30, 2022, we had an accumulated deficit of $2.3 billion. Contingent on the level of business development activities we may complete as well as pipeline programs advancing, we may continue to incur operating losses for the next few years as we incur significant development and commercialization costs.

Conclusion

Acadia’s current 10/2022 market cap of $2.5 billion is not insignificant when one considers its recent track record in developing its late stage therapies. I am cautiously optimistic that its situation will improve. On that basis I refrain from rating Acadia as a sell.

However now that it has given up entirely on its Alzheimer’s disease psychosis indication, I consider it a strong “do not buy”. Accordingly I rate it as hold.

Be the first to comment