ilkermetinkursova

Investment Thesis

AbraSilver Resources (OTCQX:ABBRF) is a quality silver exploration and development company, which derives most of its value from the Diablillos project, located in the Salta province, Argentina. The company has its primary listing in Canada (TSXV:ABRA:CA) and an OTC listing in the U.S.

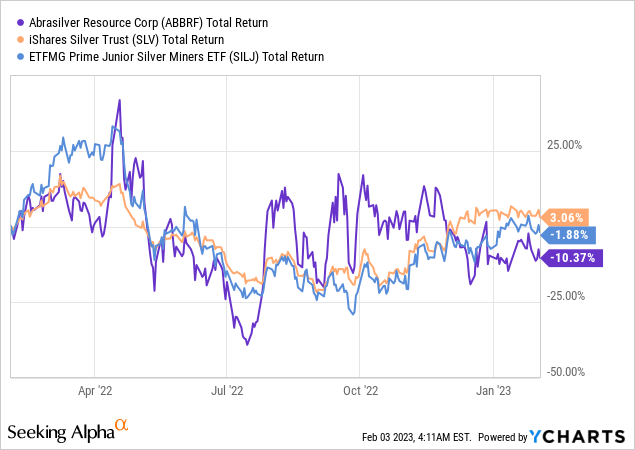

The stock price has over the last 3 years had an excellent return, outperforming most peers by a wide margin. However, the stock price performance has over the last year been less impressive, despite the fact that the company has delivered even better drill results lately and has grown its resource base. So, the valuation for AbraSilver is now very attractive given the existing resource, which is set to grow further in 2023.

Figure 1 – Source: AbraSilver

Diablillos

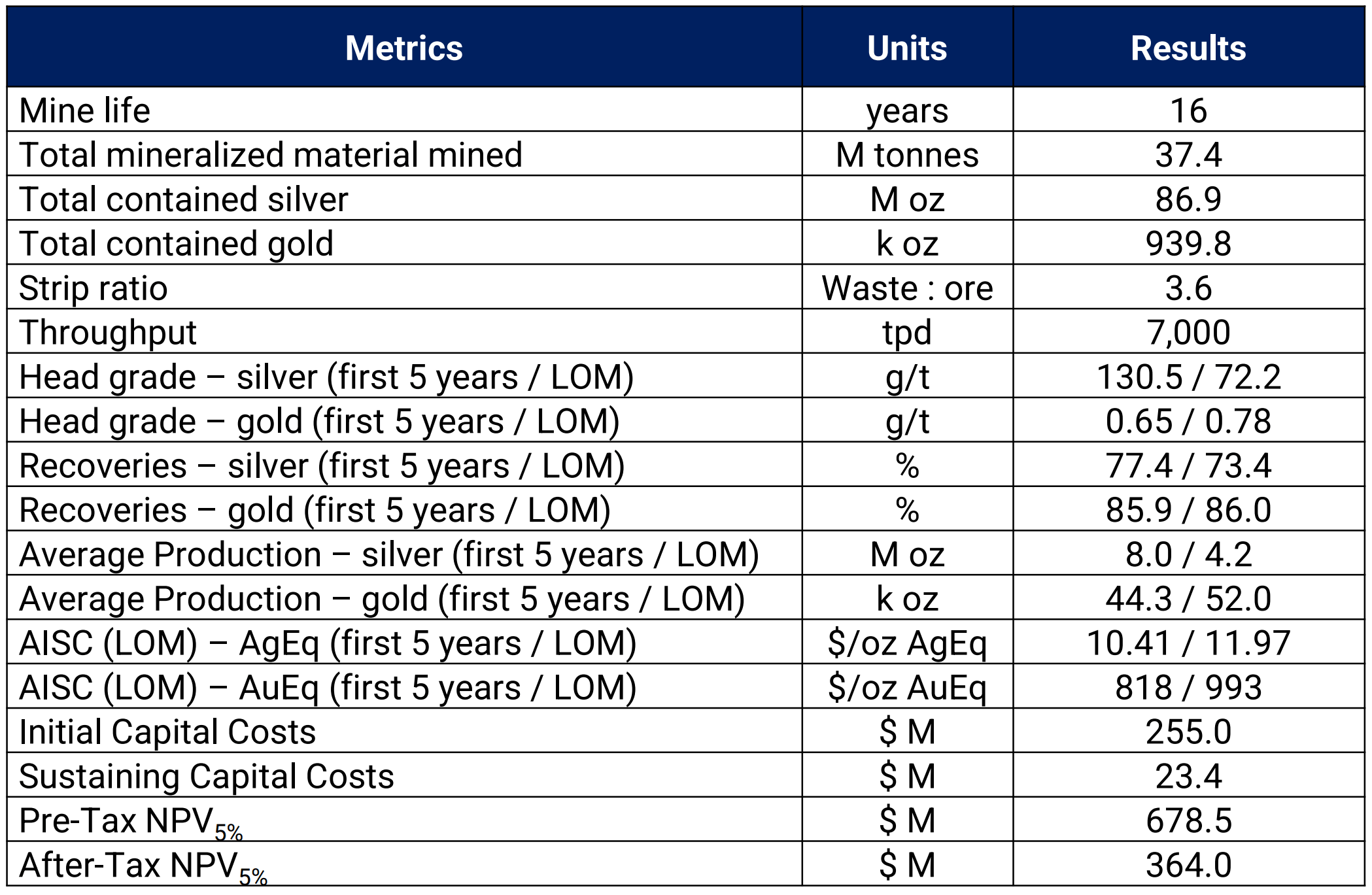

AbraSilver did in 2021 provide an updated PEA for the Diablillos project, which is likely to be an open pit heap leach project, where the grade is above open pit industry averages. About half of the resource ounces are presently in silver and the other half is gold.

The PEA indicated a 16-year mine life, with 8.5M silver equivalent ounces in annual production, and an AISC of $11.97/oz. The initial capital cost was then estimated to $255M.

With a gold price of $1,850/oz and a silver price of $23/oz, the 2021 PEA indicated an after tax NPV just below $400M.

Figure 2 – Source: AbraSilver 2022 Presentation

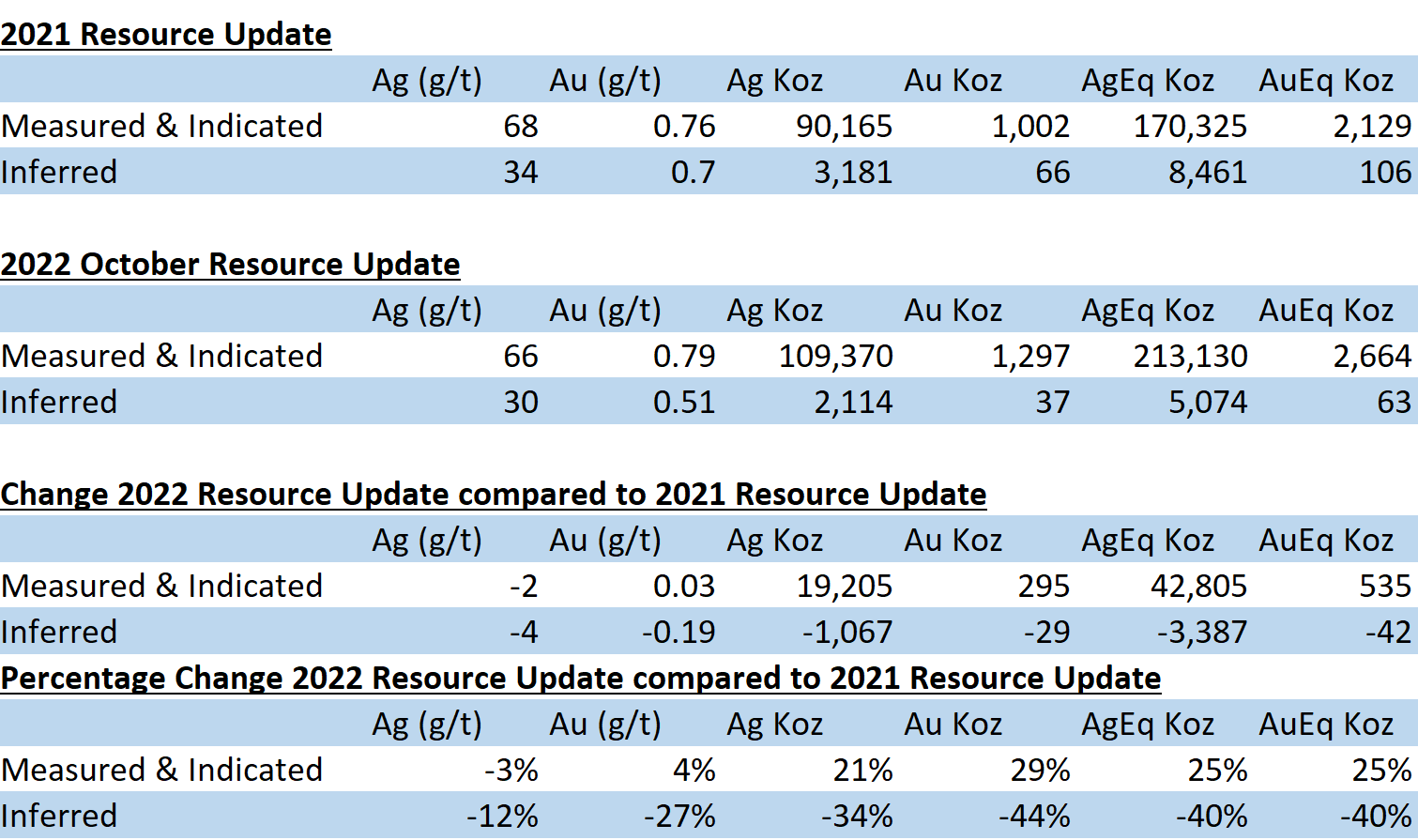

However, the company did during the fall of 2022 also provide a resource update, from the 20,000-meter Phase II drill program at Diablillos. The resource growth in 2022 was 25% compared to the data that was used in the PEA and the grade was relatively unchanged.

AbraSilver does today have a quality project with over 200M silver equivalent ounces, with very healthy open pit grades. One very underappreciated fact is that more than 95% of the resource ounces are in the measured & indicated category and there are very few inferred resource ounces.

Figure 3 – Data from Resource Updates

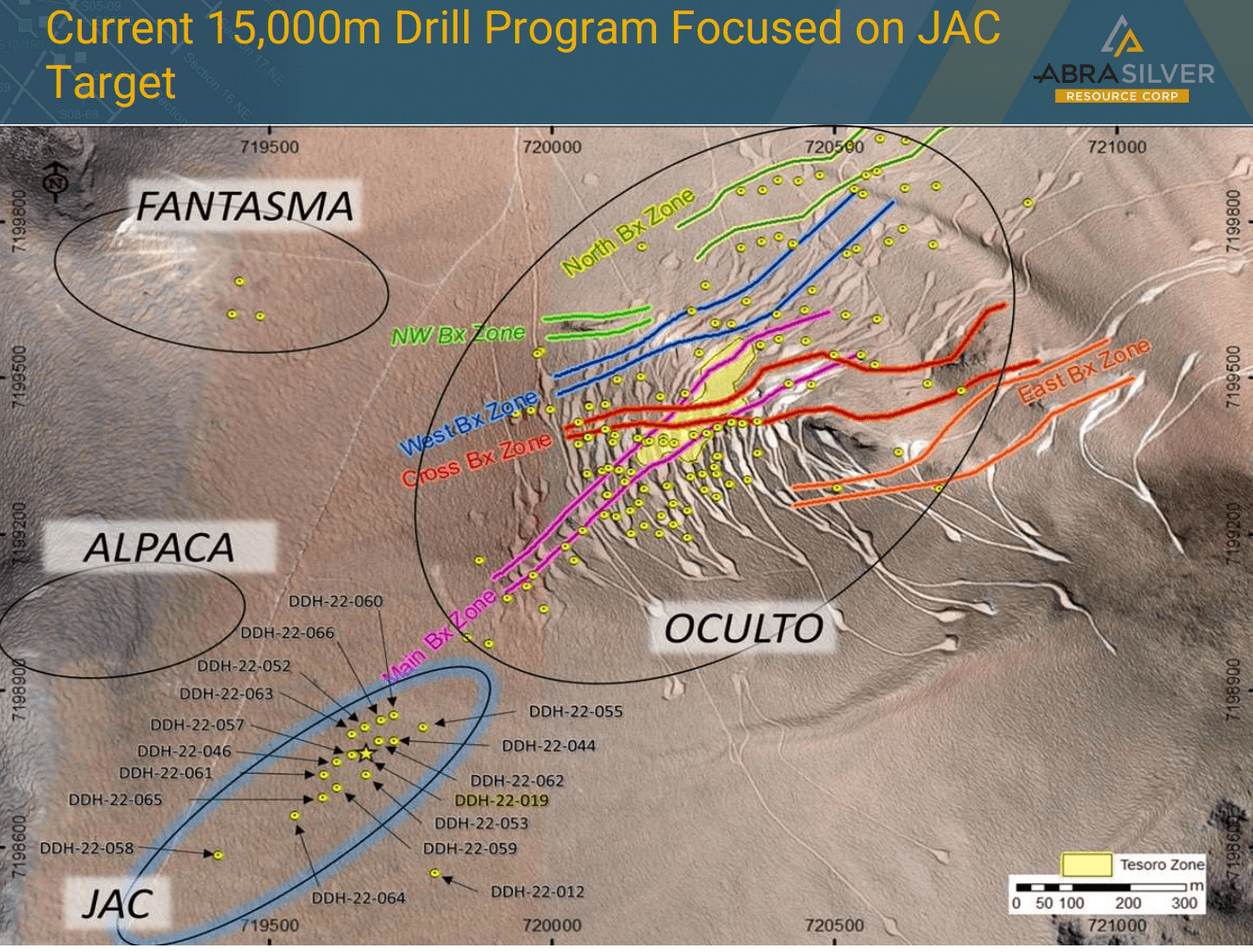

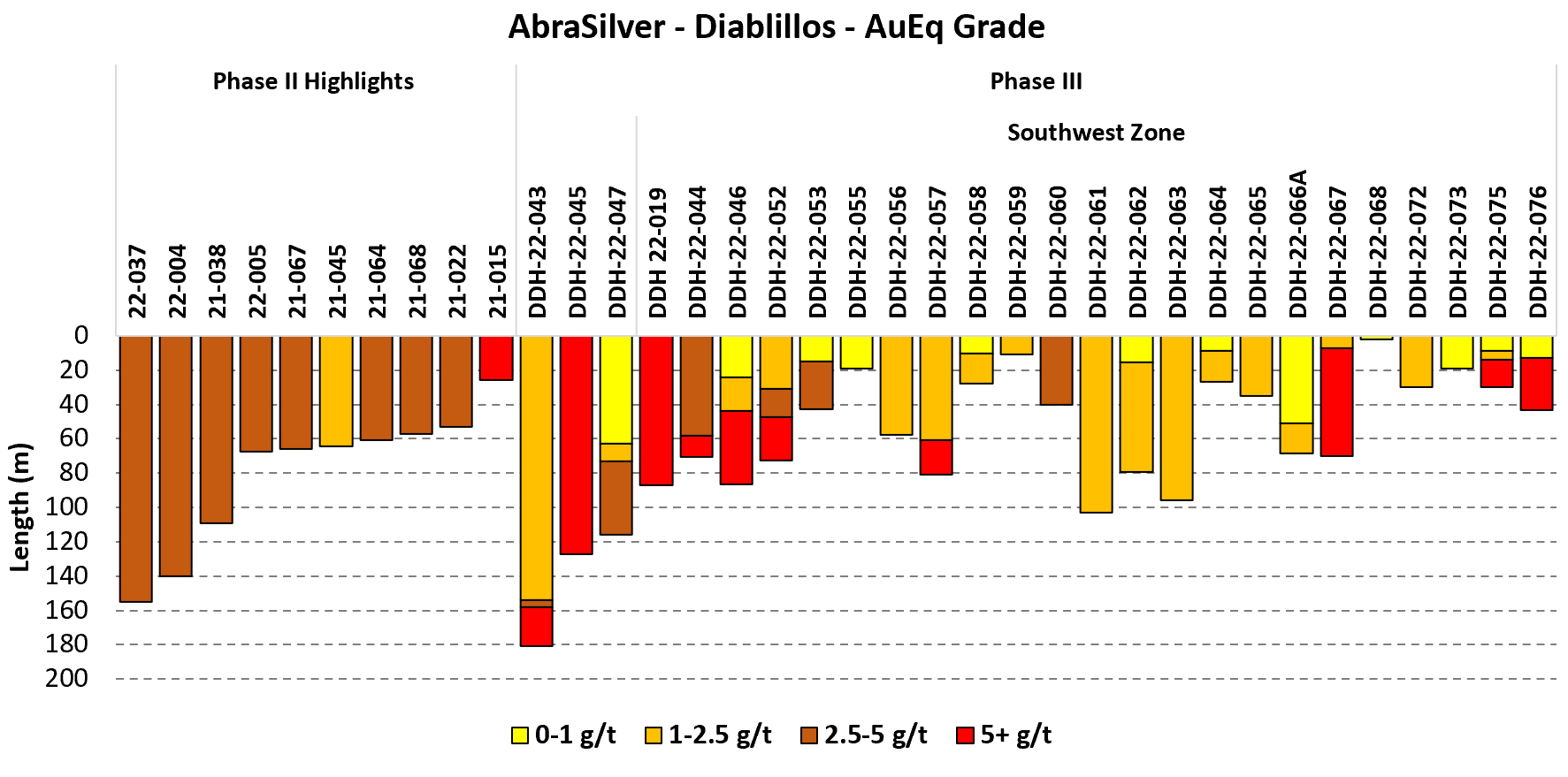

Since the cut-off for the 2022 resource update, AbraSilver has continued with a 15,000-meter Phase III drill campaign, which is scheduled to be completed in H1-2023 followed by a PFS on Diablillos. The Phase III drill campaign is primary focused on the JAC target, which can be seen in the figure below.

Figure 4 – Source: AbraSilver January 2023 Presentation

The JAC target in the southwest zone has shown to have even better grades than what we have seen elsewhere at Diablillos and the target has delivered very consistent drill results. So, I do think it is fair to assume that the resource might grow another 15-25% from the Phase III drill campaign.

Figure 5 – Source: Data from AbraSilver Press Releases

Bought Deal

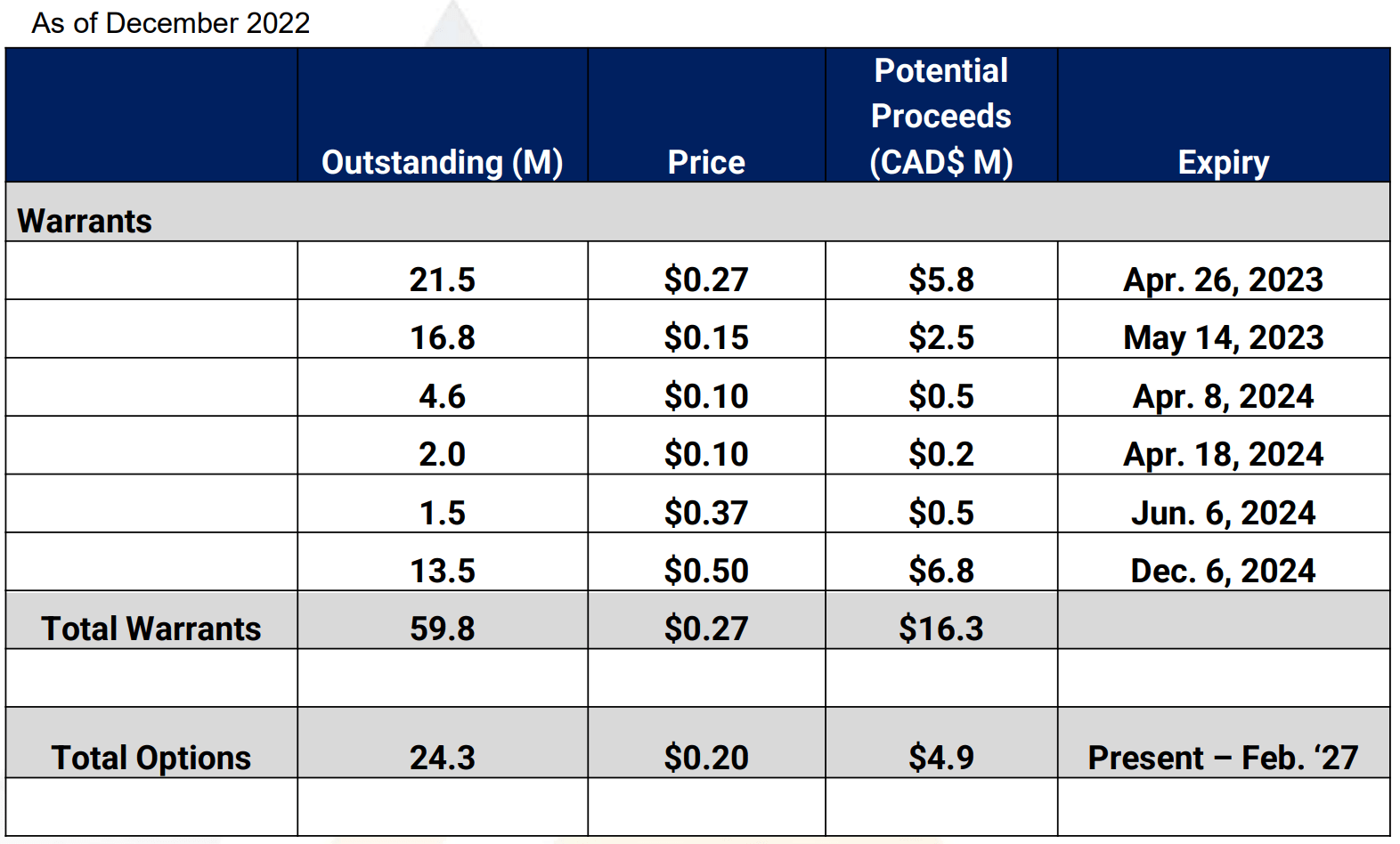

AbraSilver did in late 2022 announce and close a C$10M bought deal, which is likely part of the reason for the weak stock price performance lately. I would have preferred the company to be a little bit more patient here, given the quality project it has, but it might matter less in the long run.

A more concerning fact with the bought deal than the timing, was the use of a half-warrant. Now, the need use warrants could have been due to the poor timing. If so, that would be on management and the impact is not massive. Another potential cause for the need for warrants could be a lack of institutional interest.

There is about 60M warrants outstanding and more than half of those are likely to be exercised in H1-2023 before they expire, which will bring in some more cash, and grow the share count by about 7%. So, while the upcoming dilution from the in-the-money warrants is relatively low, I still view it as a slight concern that the company still needs to resort to warrants in the bought deal, for a project with over 200M silver equivalent ounces in the measure & indicated category.

Figure 6 – Source: AbraSilver January 2023 Presentation

Valuation

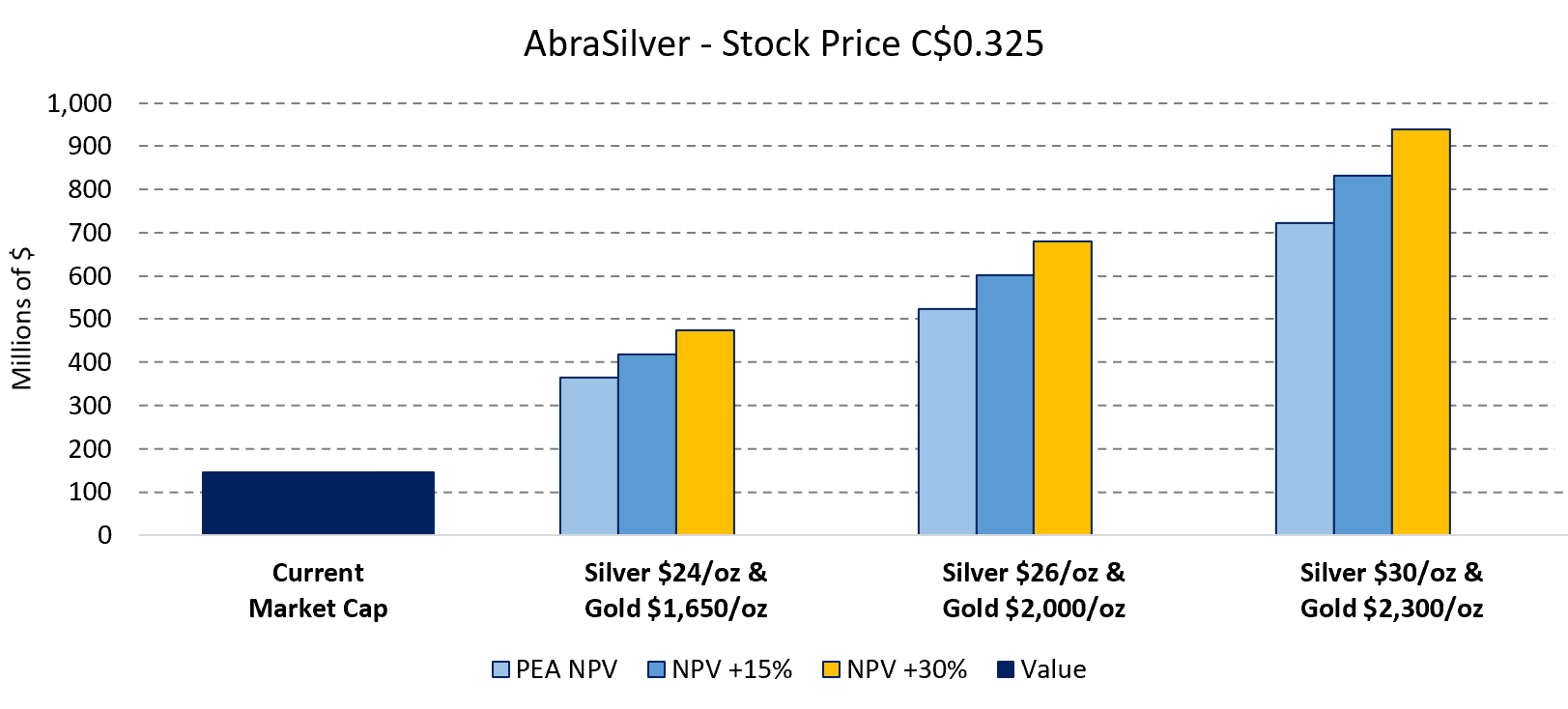

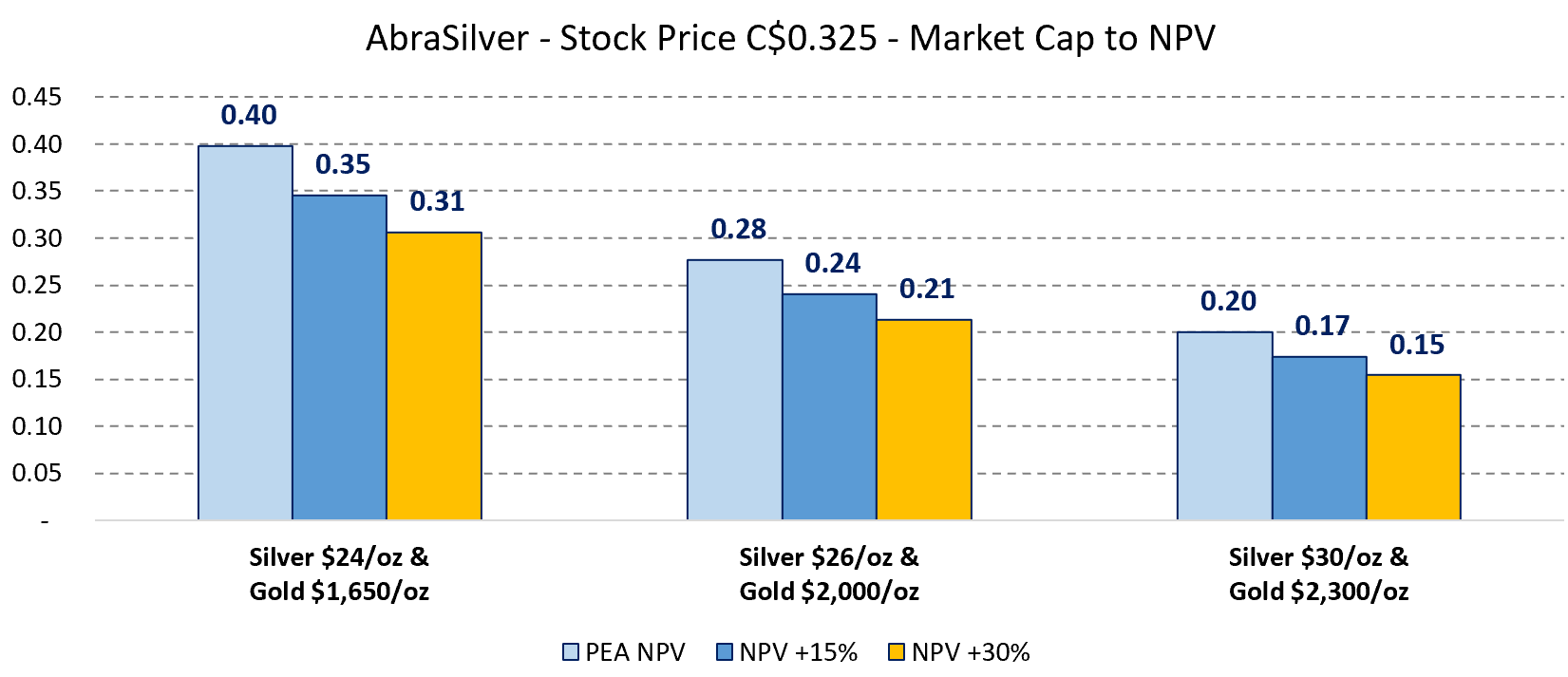

In the chart below, I have used the latest share price, shares and options from Q3-22 plus the 27M shares from the December 2022 bought deal, where the market cap is $145M. All warrants with a dilutive exercise price are also included in the share count.

Exactly how much the NPV will grow from the Phase II and III drill programs will need to be confirmed in the PFS, due to be released within 6 months from today. It is also fair to assume some inflation on the cost side, even if I think the resource growth will more than offset any inflationary impact. Keep in mind that the grade has improved as of late as well. In the chart below, we can see the current dilutive market cap in relation to the NPV estimates using a few different metal price scenarios and NPV growth scenarios. Even without NPV growth, AbraSilver is relatively cheap at this level, extremely so if we see NPV growth or the silver price recover to levels seen over the last few years.

Figure 7 – Source: My Calculations – Multiple Sources Figure 8 – Source: My Calculations – Multiple Sources

Risks

The initial capital cost, where the latest estimate was $255M, is a slight concern for a company with a diluted market cap of only $145M. So, we would need to see significant share price appreciation for AbraSilver to take this project to production by itself, without massive share dilution. However, given the scale and grade of this project, I suspect a takeout or joint venture are relatively plausible scenarios as well.

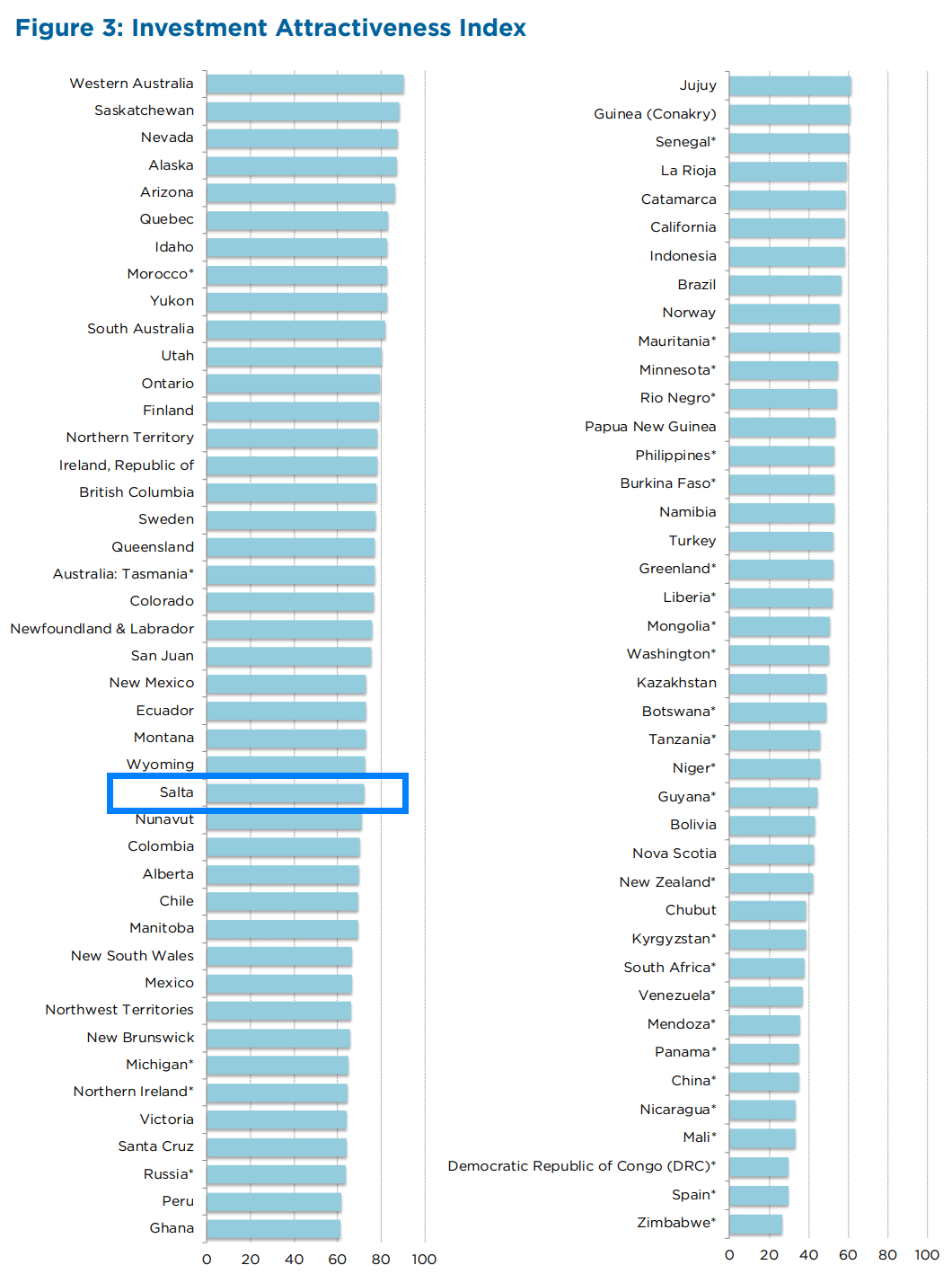

Argentina is not without political risk, but most decisions related to AbraSilver are made on a provincial level in Argentina. Where the Salta province was in the Fraser Institute Annual Survey of Mining Companies 2021 considered the second most attractive province in Argentina, above countries like Mexico and Brazil for example.

Figure 9 – Source: Fraser Annual Mining Survey – 2021

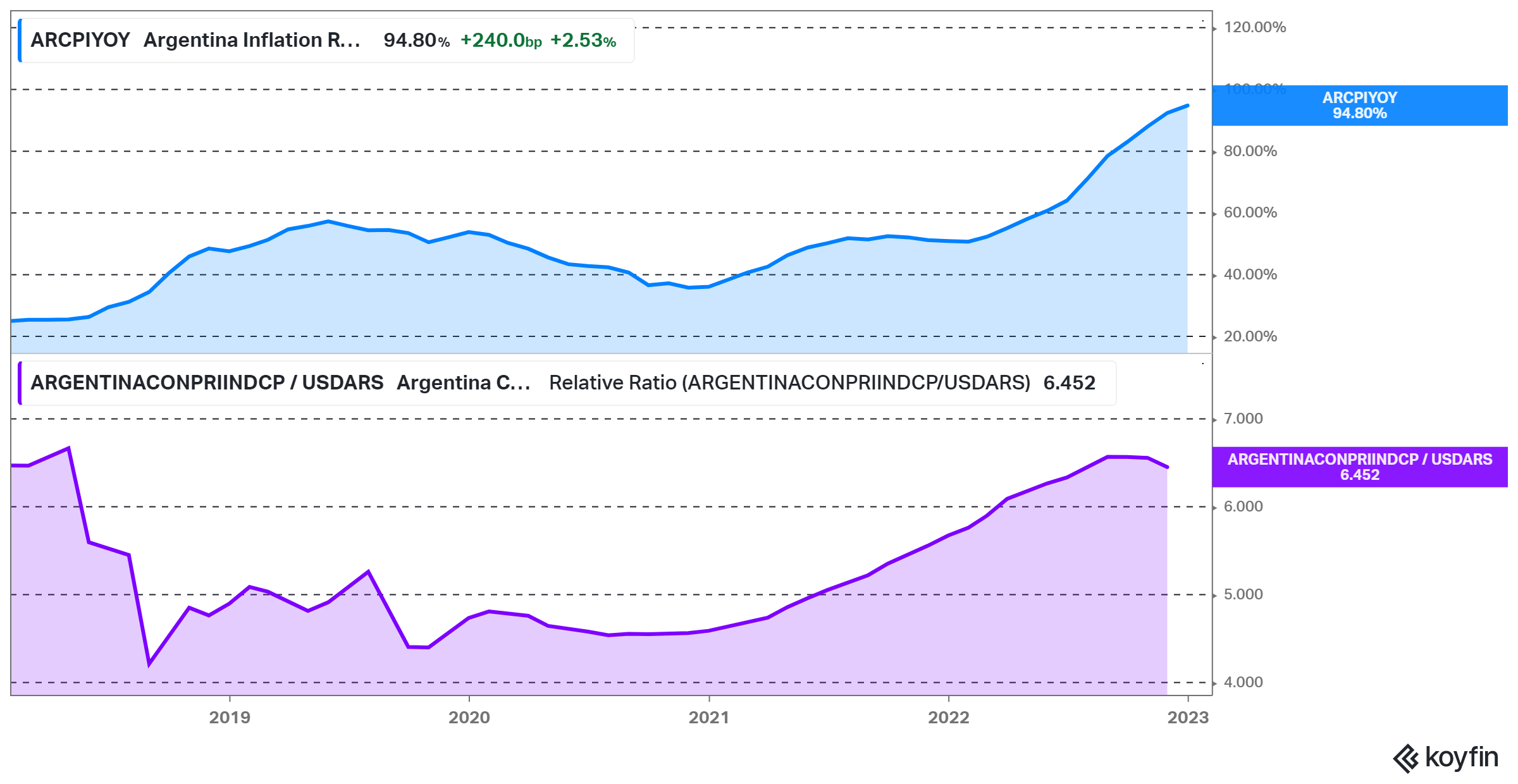

The inflation rate is presently very high in Argentina, which can lead to more political instability in the country and provinces. However, the direct impact to AbraSilver is not as large as one might imagine. The company only holds a minimum amount of cash in the local currency and most of the inflation is localized. So, if we adjust the Consumer Price Index in Argentina against the USD, we can see that the CPI has not increased much over the last 5 years, in USD terms at least.

Figure 10 – Source: Koyfin

Like all exploration and development companies, there is always a material risk for further share dilution to cover drilling, general & administrative expenses, and construction down the like. Also, not all development stories, even those with characteristics as good as Diablillos are built, which is another risk to consider. While the Salta province might be able to partly avoid some of the political pain felt elsewhere in the country, if things get bad enough, that certainly has the potential to depress AbraSilver’s share price as well.

Conclusion

Overall, AbraSilver has a very attractive project in Diablillos, which is primarily what I am interested in, even if some other projects could contribute to the value longer term.

An investment in AbraSilver is not without risks, but the potential reward here is far larger than the risks in my view, which is why I am long AbraSilver. However, everyone needs to determine which level of political risk is acceptable. There are no red flags with AbraSilver based on how I analyze companies, but I also rely on diversification to spread out the risk.

A drastic increase in political instability is probably the factor which would most force me to reevaluate my investment in AbraSilver.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment