At the end of each of the weeks leading into the last one, I have done a market update, reflecting the changes that occurred in the week, not just to market values, but also to investor psyches, and each week, I have hoped that it would be the last one needed for this crisis. That hope was dashed last week, as markets continued on their downward spiral, and here I am again, writing another viral market update. In this week’s update, I will begin by again first chronicling the market damage, across asset classes, and within equities, across sectors, industries and company types, but I will follow up by looking at four different investment strategies for those who have the capacity and the willingness to look past the near term, recognizing that many of you might not have that luxury.

Surveying the Market

In what has now become a common component of each of these weekly updates, I will start with a survey of overall market performance in different asset classes, and then break down the damage in equity markets across the globe.

The Macro Picture

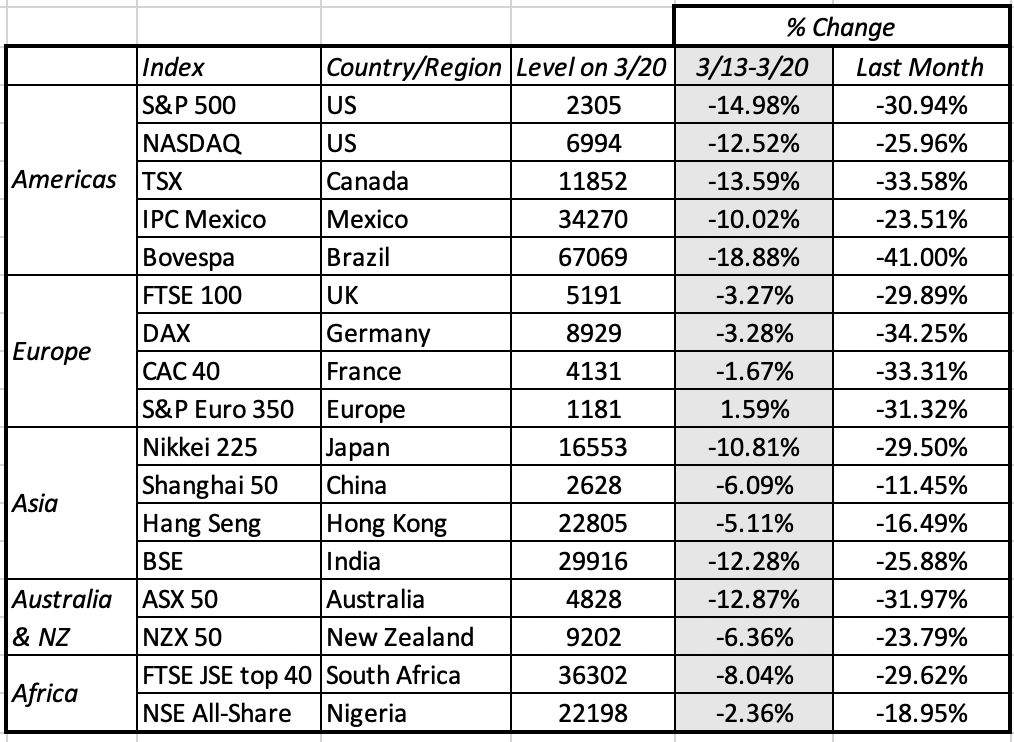

As was the case in 2008, it was difficult, perhaps impossible, to find a safe place to hold your money last week and no market was spared during the week. It was a week when equities lost trillions in value, across the world, but it was also a week when treasuries that had appreciated in prior weeks due to a flight to quality also saw no gain, oil continued its falls to multi-decade lows, and gold did not play its historic role as a crisis asset. Let’s start with equities. The week started badly and did not get much better, as fear ruled across markets:

{kind=link}

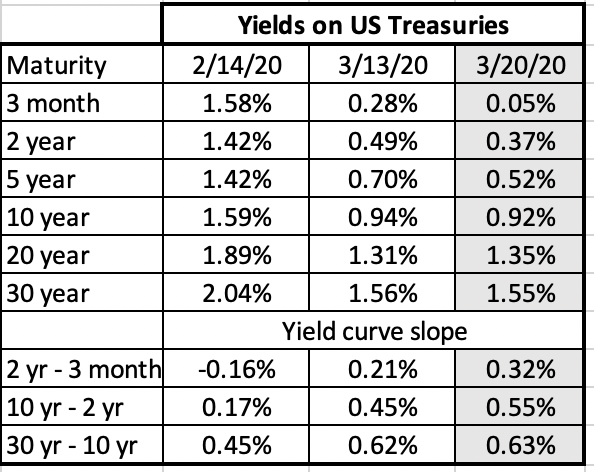

The European equity markets, at least collectively, did better than the American and Australian markets between March 6 and March 13, with the Asian and African markets falling in the middle. When equities are in free fall, US treasuries are usually the beneficiary, but last week proved to be an exception, as treasury rates at the long end stabilized, perhaps spooked by the prospect of inflation from the trillions of dollars in rescue packages being proposed:

|

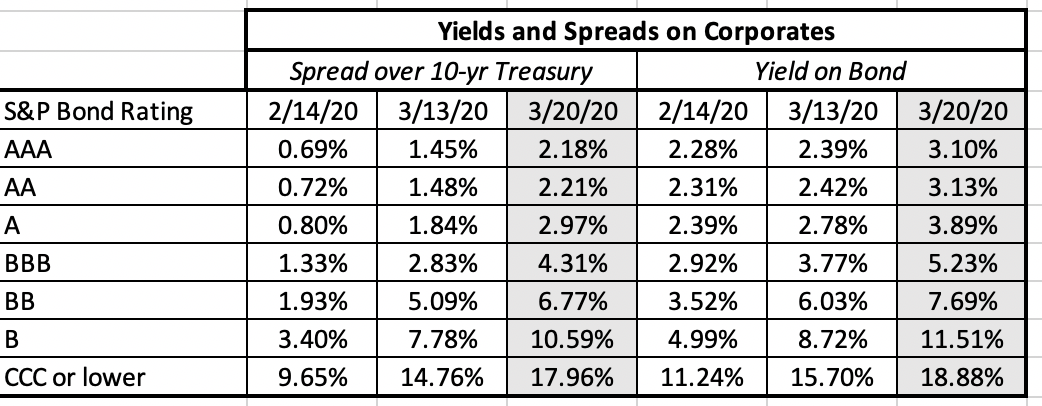

The fears that this crisis will create an extended and deep recession, which, in turn, will cause corporate defaults to rise, especially in natural resource and travel-related companies, caused corporate bonds to have their worst week of this five-week crisis period:

|

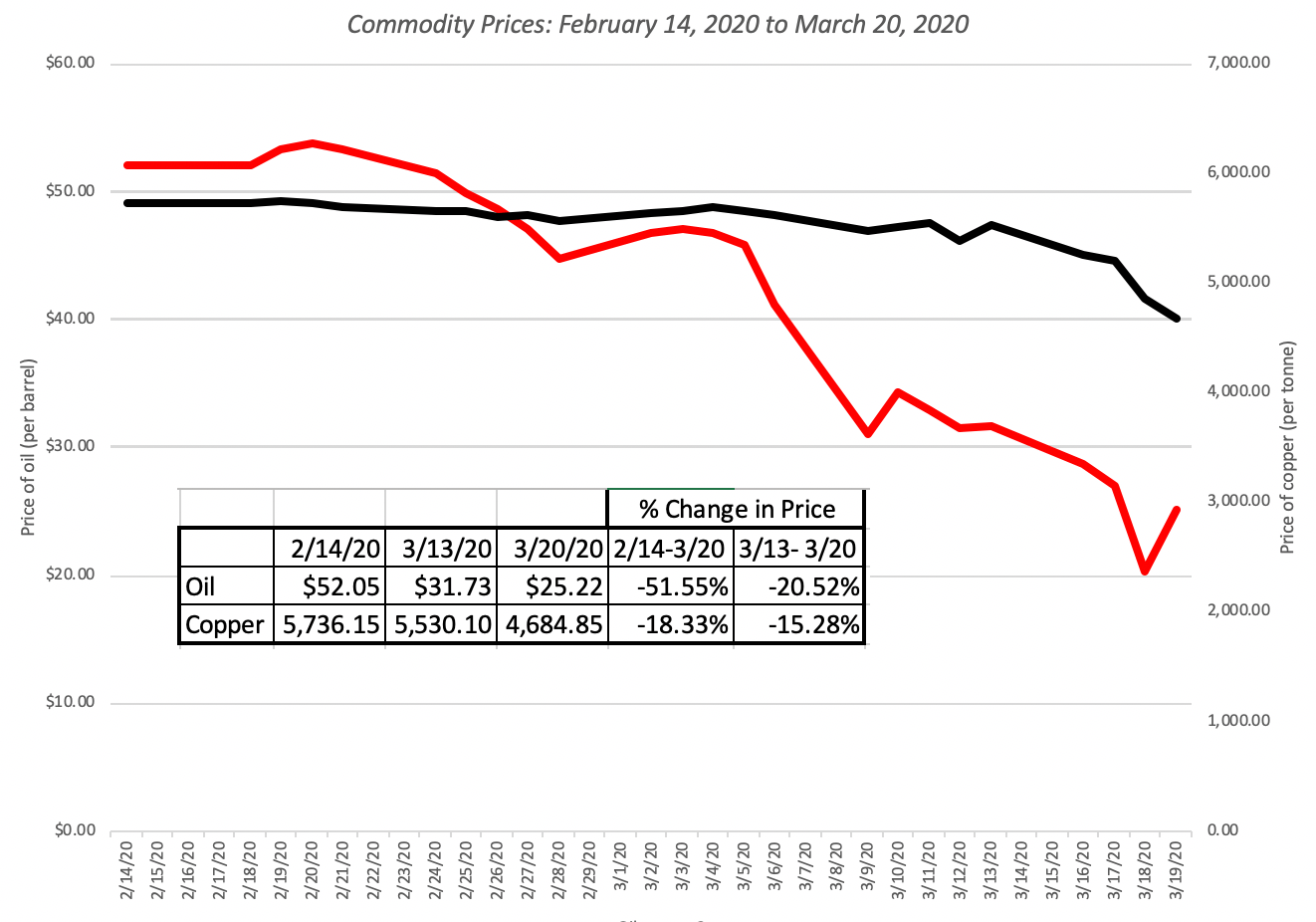

The damage in the corporate bond market, not surprisingly, was worse for lower-rating bonds, but the even highest rated bonds were not spared. Speaking of natural resource companies, oil continued on its downward trend, falling well below what many analysts had pronounced as its floor:

|

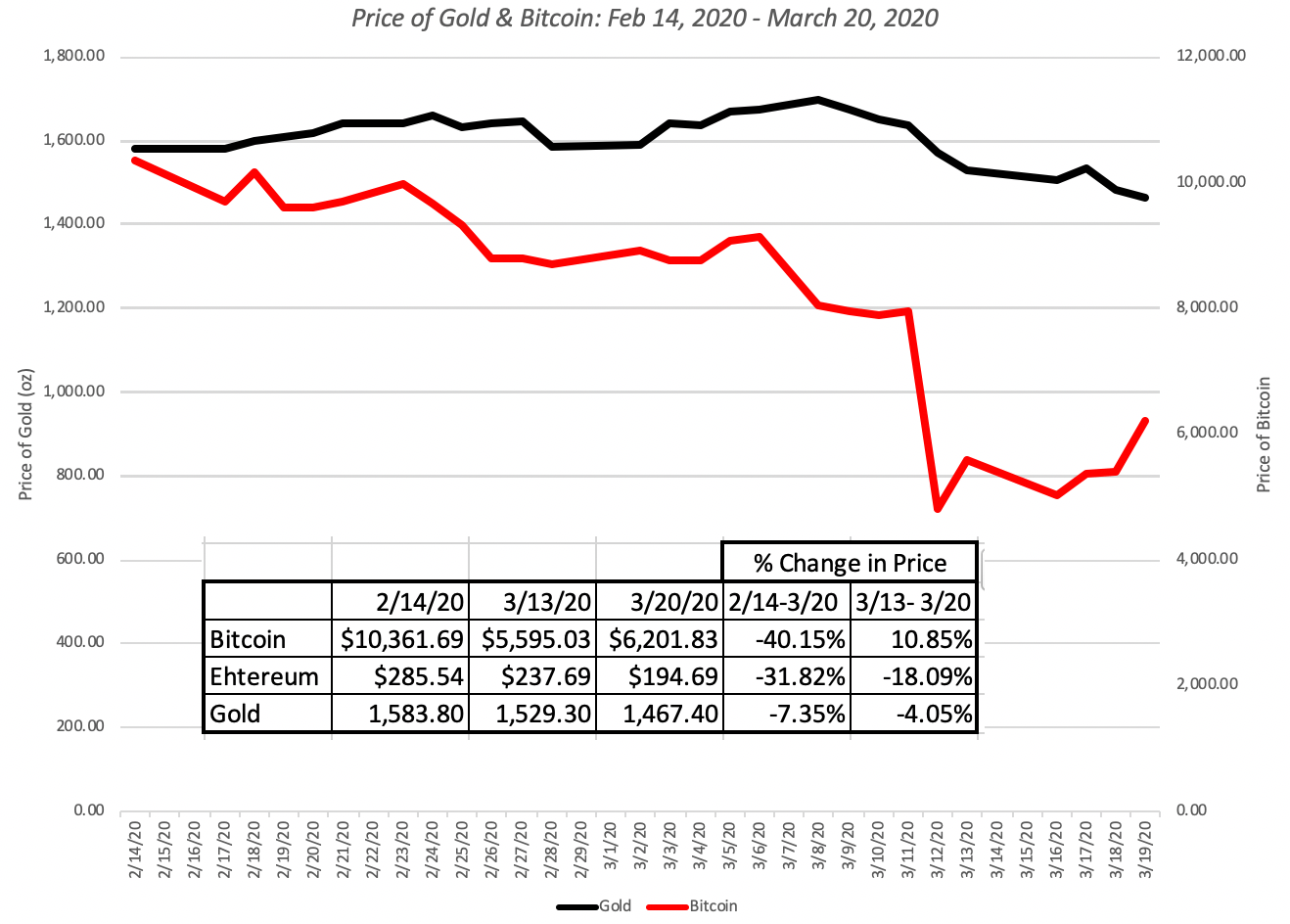

The fact that copper, another commodity sensitive to global growth, has not dropped as much shows how much of an effect the Russia-Saudi tussle is having on oil prices. Closing off, gold had a better week than stocks, but it too was down, but bitcoin ended the week on a little bit of an upswing.

|

All in all, no asset class was safe and creative asset allocation would have best reduced the pain, not eliminated it.

The Breakdown

As in the weeks before, I will take apart the drop in equities around the world and look at the differences meted out, both in the last week and cumulatively over the five weeks since February 14.

Sector and Industry

I start by looking at the loss in value, broken down by sector, with the percentage changes in value computed over a week and over five weeks:

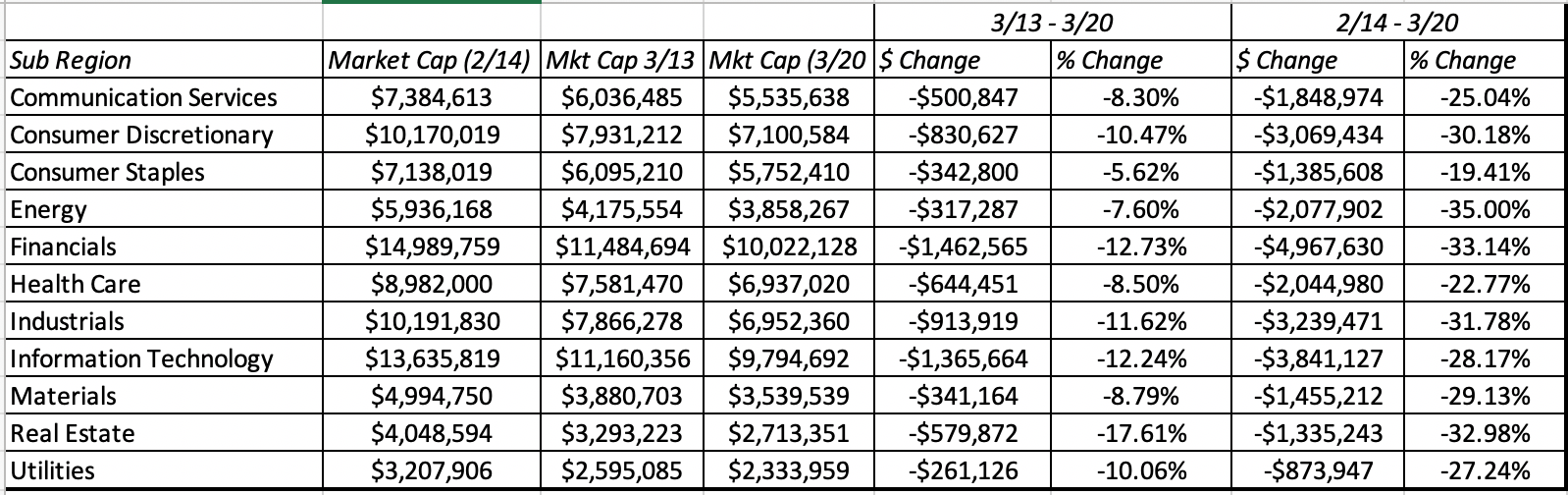

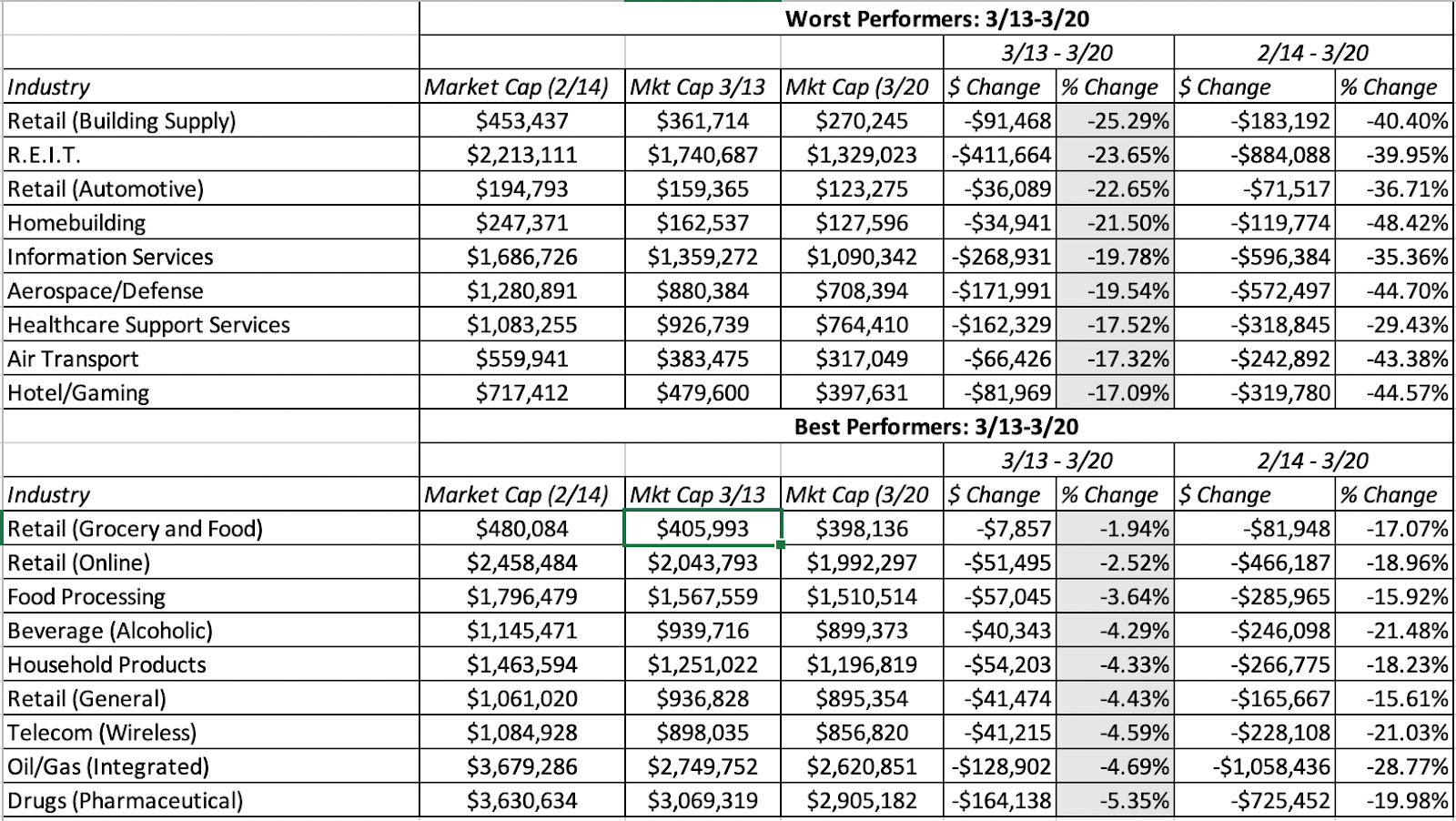

Energy remains the most damaged sector, with financial services and real estate close behind., and consumer staples and healthcare have held up the best. Breaking the sectors down to industries, and looking at the ten best and worst performers last week:

|

The industries that were worst hit were infrastructure companies (with the exception of healthcare support services and automotive retail) that tend to have debt. Read in conjunction with the earlier table on the widening of default spreads for corporate bonds, last week’s market collapse seems to have been driven more by default risk concerns than the prior weeks. The least affected businesses tend to be those that cater to non-discretionary demand.

Region

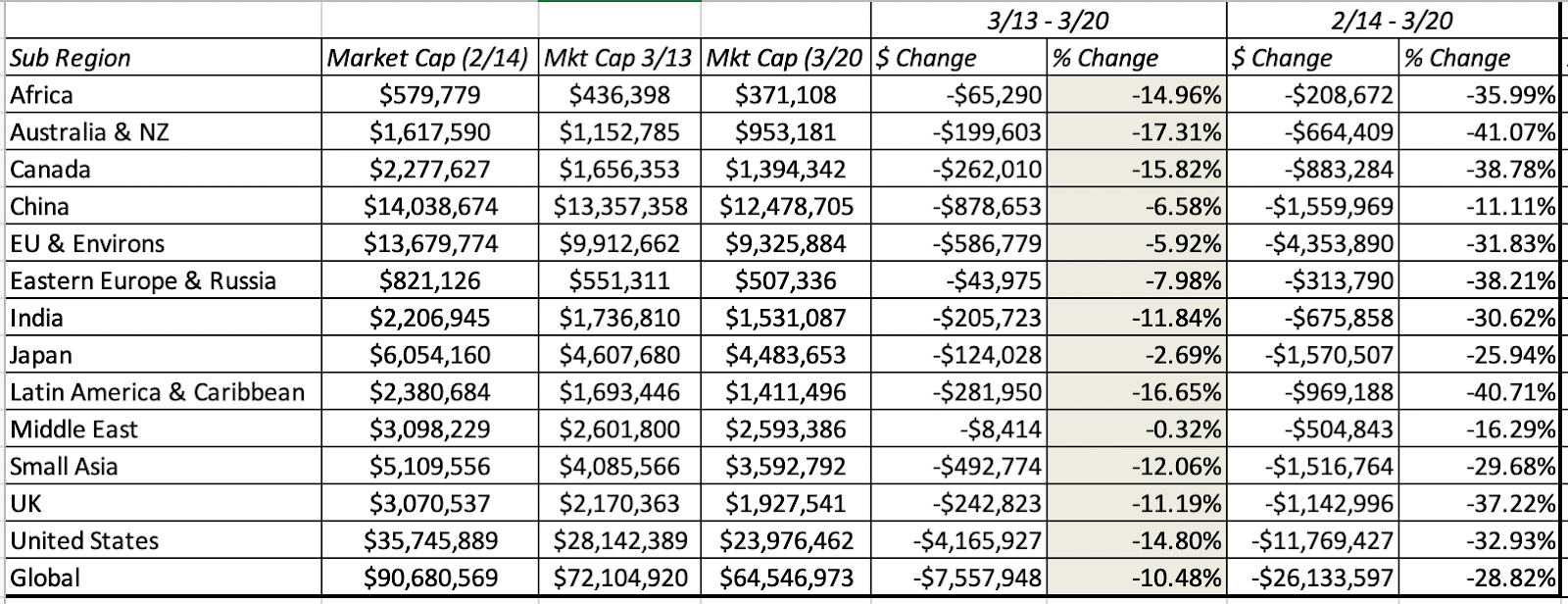

Earlier in this post, I looked at market indices around the world to conclude that stocks listed on the American and Australian continents were more affected than European stocks. Expanding on that proposition, I look at the market value lost, both in dollar and percentage terms, across regions:

Globally, companies have lost $26.1 trillion in market capitalization over the last five weeks, and US stocks alone have lost $11.8 trillion in market cap. Canadian, Australian and Latin American stocks have been worst hit, in percentage terms, and China and the Middle East have taken the smallest hits, in percentage terms.

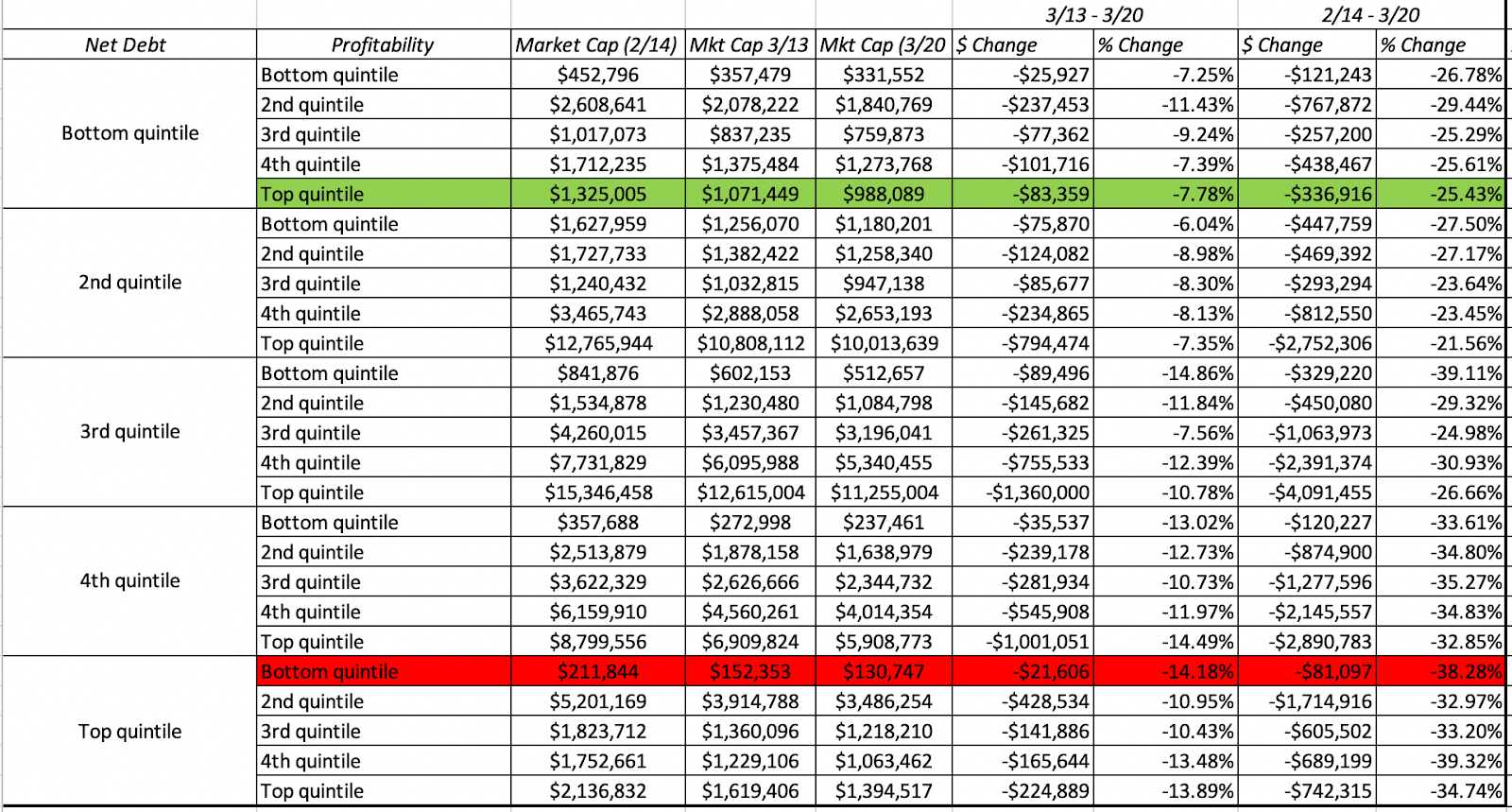

Net Debt and Profitability

It looks like debt concerns rose to the top of the worry heap last week, and to see how this shows up at the company level, I broke companies down into five quintiles, in terms of net debt ratios, and five quintiles in terms of operating profit margins. Specifically, I want to see how much having a profit buffer and low debt has protected companies during this meltdown.

I apologize if this table is a little overwhelming, but the way to read it is to look at the combinations of net debt and profitability. For instance, companies with the least debt are in the bottom quintile of the net debt column and companies with the highest profitability are the top quintile of the profitability column. I don’t want to read too much into this table, but if you look at last week’s action, stocks with lower net debt ratios (in the bottom two quintiles) did much better than stocks in the top debt quintile. At least for the moment, the profitability effect is being drowned out by the debt effect, since there is little discernible relationship between operating profit margins and market markdown. If you squint hard enough, you may be able to find something, especially in the middle quintile, but I will leave that up to you.

Looking Past the Crisis

In one of my first posts on this viral market crisis, I mentioned that the first casualty in a crisis is perspective. As you get deeper and deeper into the specifics of the crisis, you will find yourself not only getting bogged down in numbers, and in despair. I have had moments in the last few weeks, when I have had to force myself to step back from the abyss, think about a post-virus world and to reclaim the initiative as an investor. If you are a pessimist, you may view this as being in denial about what you see as an economic catastrophe that is about to unfold, but I am a natural optimist, and I believe that this too shall pass!

The Economy

There is no disagreement that the virus will cause the economy to go into a deep recession, since commerce is effectively shut down for at least a few weeks. During that period, economic indicators such as unemployment claims and measures of economic activity will hit levels not seen before, but that should come as no surprise, given how large and broadly based the shock has been. There are two questions, though, where there can be disagreement.

- How quickly will the global economy come back from the shut down, and when it does how completely will it recover?

- How much permanent change will be created by this crisis in terms of both consumer (and investor) behavior and economic structure?

There are some who are more optimistic than others, arguing that once the viral fears disappear, there will be a return to business as usual for most parts of the global economy, stretched out over months rather than years, and that the changes to consumer behavior and economic structure will be small. At the other end, there are many more who feel that economies take time, measured in many years, to recover from shocks of this magnitude and also that there will be significant changes in consumer behavior and economic structure in the making.

Investment Strategies

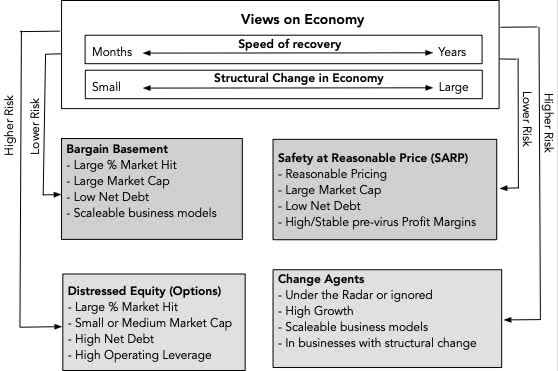

Your views on the economy, both in terms of how quickly it will come back from this shock and how much change you see in economic structure, will determine your next steps in investing. If you believe that recovery will be quicker and with less structural change, there are two strategies you can adopt.

- Bargain Basement: In this strategy, you focus on stocks that have been pounded in the last few weeks, losing 50% or more of market value, but which have the ingredients that you believe will allow them to survive, perhaps stronger, in the post-virus economy. Key among these ingredients will be low net debt ratios (Net Debt to EBITDA less than one) and pre-virus operating margins that were solid enough to take the hit from the crisis. To the extent that survival until the turnaround occurs is key, you may also keep your search restricted to larger market cap companies.

- Distressed Equity: There is a more risky strategy you can adopt, where you also look for stocks that have seen a significant loss in value over the last five weeks, but focus on the most endangered of these, with high net debt and fixed costs. You are effectively buying options, with some already out-of-the-money, and as with any strategy built around doing that, you will see a significant number of your investments go to zero. The payoff from this strategy comes from the companies that make it back to life, with equity values increasing by enough to cover your losses. At first sight, the airlines and Boeing (NYSE:BA) meet these criteria, but there is a catch, insofar as they are large enough to be targeted for government bailouts, which are a mixed blessing, since they allow companies to survive, while wiping out or severely constraining equity claims. Thus, smaller companies that have to make it through on their own may be better candidates for this strategy than companies that are too big to fail, that attract large bailouts.

If you are more pessimistic about economic recovery, both in terms of its length and strength, and believe that the recovery will restructure the economy and how companies operate in many businesses, there are two strategies that you may find work for you:

- Safety at a Reasonable Price (SARP): Here, you focus on companies that are best positioned to not just survive a long downturn, but have the ammunition to make it work to their advantage. Large market cap firms with low debt ratios and high cash balances, that had high growth and profit margins in the pre-virus economy, would be good candidates. Facebook (NASDAQ:FB), Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL), Apple (NASDAQ:AAPL) and Microsoft (NASDAQ:MSFT), for instance, clearly fit these criteria, but since these companies are already sought after in a market where safety is rare and highly valued, you should add pricing screens that allow you to get them at reasonable prices.

- Change Agents: This is as much a bet on changes in consumer behavior and economic structure as it is on individual companies. Thus, if you believe that this crisis will make people more comfortable with delivery services for a wider range of goods and online interaction (in business and education), you could seek out companies that are innovators in these spaces. Again, the highest profile players, like Zoom (OTC:ZOOM), may be priced out of your reach, but there are others like Chegg (NYSE:CHGG) that may meet your criteria.

The picture below summarizes the four strategies:

My views on the economy are mixed. I do think that the global economy will come back, but it will take more than a few months, and there will be structural changes in some sectors. I ran screens for all of the strategies, other than the Change Agents strategy (which is less about screening, and more about detecting macro trends), across all publicly traded stocks (about 40,000+) on March 20, 2020. As I look at the companies that go through the screens, I realize that there is more work to be done and better screens that can be devised, but think of it as work in progress, and if you have access to a large database, try your own.

YouTube Video

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment