deepblue4you

What next for markets after a year like none seen in a generation? Investors from BlackRock Fundamental Equities sat down to discuss the outlook for inflation, the growth and value investing styles, and key industries.

In the most recent episode of BlackRock Fundamental Equities’ Expert to Expert series, three active equity investors discussed the dynamics weighing on markets, their view on growth and value stocks, and the outlook for the energy and technology sectors. They related stories of their own experience and reflected on findings from a recent investor survey. We capture elements of their conversation here.

More time, more optimism?

In a year when it was easy to be a pessimist, a BlackRock Fundamental Equities poll of over 1,000 U.S. individual investors revealed potential hints of optimism – along with some interesting variance in sentiment by generation. Millennials were more comfortable increasing equity allocations this year, with 45% of those surveyed in May revealing they added to their exposure, well above both Gen Xers (25%) and Boomers (11%). And 49% of Millennials saw themselves adding more in the ensuing six months.

Caroline Bottinelli, a Research Analyst and Portfolio Manager on the U.S. Growth team, sees two dynamics at play. The first was shorter memory, which potentially translated into less fear:

“Investors of my generation haven’t seen a period of sustained high inflation in their lifetimes, as the forces of globalization and technology and demographics have put downward pressure on inflation and rates over the past 40 years.” This, Ms. Bottinelli suggests, may have younger investors more inclined to believe the Fed will pivot away from rate hikes, which would be positive for equities.

The second factor: Acknowledgement of a longer investment horizon, meaning more time to recoup losses and compound earnings, which Ms. Bottinelli notes is the real driver of returns over the long haul. “And we know that missing out on just a handful of the best days in the market can significantly negatively impact those returns,” she says, espousing the wisdom of “time in, not timing” the market.

Tony DeSpirito, CIO of U.S. Fundamental Equities, reflected on his 30 years in the market: “I’ve lived through multiple bear markets … 1990, 2000, 2008. At the time, they all seemed massive and quite frightening … but when you get some historical perspective, they start to look like small speed bumps on the way to good long-term returns.”

Debating inflation and recession risks

All generations homed in on inflation as the greatest risk to the market over the next six months, the survey found. Will it remain the dominant risk as we look to 2023?

Inflation is what is driving the Fed’s rate hikes, Ms. Bottinelli says, and, therefore, it does remain the bane of markets. “If inflation begins to moderate, it gives the Fed room to pause. My concern is that the inflation we’re seeing right now is supply driven and broad-based,” she says. And that could mean the Fed’s tools are insufficient to tame it without sending the economy into a recession.

Mr. DeSpirito suggests inflation may have peaked for the cycle but could be slow to trend down. He notes that the Fed’s desired “soft landing” (curbing inflation without sinking the economy) is hard to achieve and historically improbable.

“Rate hikes affect the real economy with a lag of at least six months. But most economists would tell you something more like 18 months,” he says. “So I think there’s a strong likelihood that the Fed overshoots and that we do end up in a recession.”

From style preference to style parity

With inflation and recession both at play as important market risks, the investors explored what this might mean for the growth and value styles of investing. Historical performance shows that value tends to lead in inflationary environments, whereas growth generally has an edge in slowing economies.

With both risks looming large, Mr. DeSpirito says it’s important to have both investment styles well represented in portfolios today. A recent Fundamental Equities analysis of a 50/50 blend of the highest quintiles of growth and value in the Russell 1000 Index showed the hypothetical combination is priced more attractively than the broader market.

“What that’s telling you is the stocks in the middle are actually very expensive,” Mr. DeSpirito explains. “And historically from this starting point, you (potentially) do really well blending growth and value.”

See the Q4 edition of Taking Stock for the full analysis.

2022’s top and bottom sectors revisited

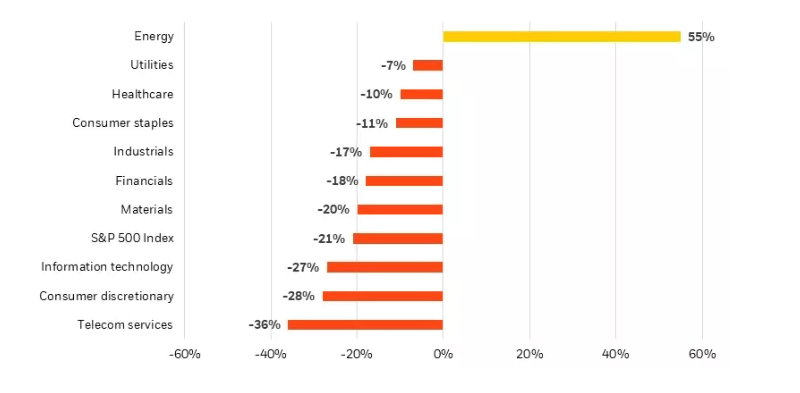

A conversation about the past year would not be complete without a look at key market sectors. Will Su, Co-Director of Research for the Income and Value team, offered his outlook for the S&P 500’s top-performing and only positive sector as of Oct. 5 – energy. See chart below.

S&P 500 sector performance, 2022

Total returns year-to-date

BlackRock Investment Institute, with data from Refinitiv Datastream and S&P, Oct. 5, 2022. Chart shows year-to-date total return of the S&P 500 Index and the sectors within it. Past performance is not indicative of current or future results. Indexes are unmanaged. It is not possible to invest directly in an index.

Mr. Su emphasizes that there are many nuances to the sustainability and energy outlook, but he sees the European winter as a watershed moment in the overall discussion, as the continent faces dire forecasts for energy shortages.

“Pushing too quickly into intermittent renewables without them achieving scale first is a recipe for inflation and energy insecurity,” he says.

Against this backdrop, Mr. Su sees opportunity in natural gas given its role as a viable and cleaner form of energy for decades to come, replacing coal and other carbon-intensive fuels. He also sees some of the largest oil and gas companies playing a key role in the energy transition.

At the other end of the return continuum, Ms. Bottinelli shared her outlook for technology, a sector that bore a large brunt of the market pain in 2022 after a strong run-up during the worldwide acceleration of digitization amid COVID-19:

“The technology sector holds a lot of these poster children of growth stocks where the earnings were supercharged during the pandemic and higher rates have had a significant impact on valuations. But … the secular tailwinds driving these businesses continue.”

Ms. Bottinelli is optimistic about the tech sector over the long term and describes today’s pricing as a more attractive entry point. But it’s important to “pick your spots” as the macro backdrop still poses risk. This, all three agree, points to the importance of active management.

Active management is about studying history, studying the current data, but then adding judgment to that. Because data and history don’t see around corners. Human judgment does. That is how we can add value as active investors.

Tony DeSpirito

© 2022 BlackRock, Inc. All rights reserved.

The survey referenced herein was conducted online in January and May 2022. Respondents (1,083 in January and 1,091 in May) were Americans aged 25+ with a minimum of $250,000 in investible assets. The survey was executed by Material Holdings, an independent research company.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of October 2022 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results.

Investing involves risk. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Diversification does not ensure profits or protect against loss.

Prepared by BlackRock Investments, LLC, member FINRA.

©2022 BlackRock, Inc. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

USRRMH1022U/S-2470900

This post originally appeared on the iShares Market Insights.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment