Andrii Dodonov/iStock via Getty Images

By Tracy Chen, CFA, CAIA

We identified the opportunity in agency mortgage-backed securities (MBS) in the fourth quarter of 2022, based on the cheap valuation of agency MBS spread to U.S. Treasuries. MBS valuations are attractive both relative to their own post-Global Financial Crisis (GFC) history and relative to investment grade corporate bonds. In addition, the value proposition thesis is reinforced by two improving fundamental drivers: One is the diminishing negative convexity due to the “out-of-the-money” status of mortgage holders’ incentive to refinance; the other is the potential moderation of interest rate volatility, which should bode well for MBS due to its embedded short in volatility. Lastly, the dwindling organic supply and the increasing demand from money managers provide a favorable market technical for this investment.

How did the housing market perform and impact MBS investments?

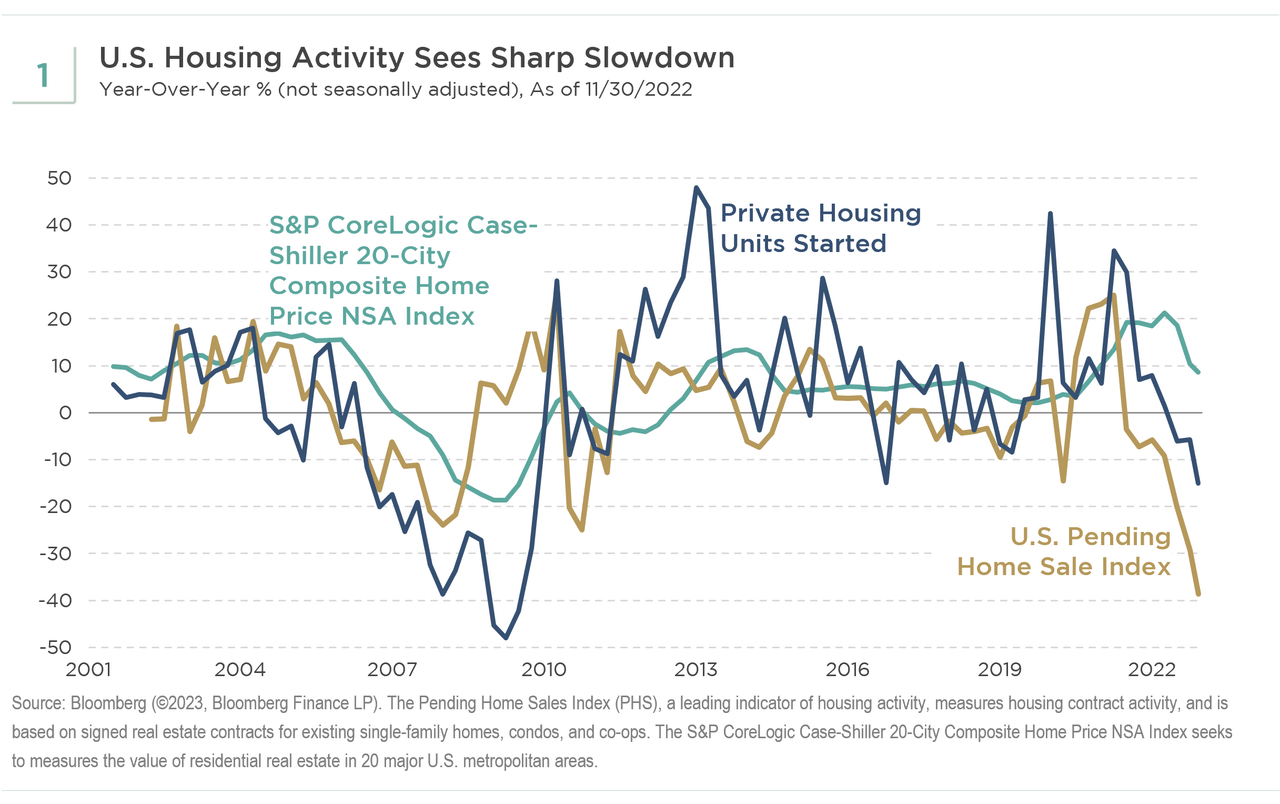

Home prices peaked in March 2022 and continued to slow to an 8.64% year-over-year rate of increase by October. More important, we observed a bifurcation between drastically slowing housing activities, including home sales, new home starts, etc., and relatively better-supported home prices, wherein the latter outperformed the former. The major driver behind this anomaly is the still low supply of existing homes due to the lock-in effect of existing homeowners. The sharp slowdown in housing activities indicates lower organic supply of MBS, slower prepayment speed, and less paying down of the Federal Reserve’s MBS holdings (see Chart 1). This outcome is more favorable for production coupon MBS than discount coupon MBS.

How is the opportunity in MBS playing out so far?

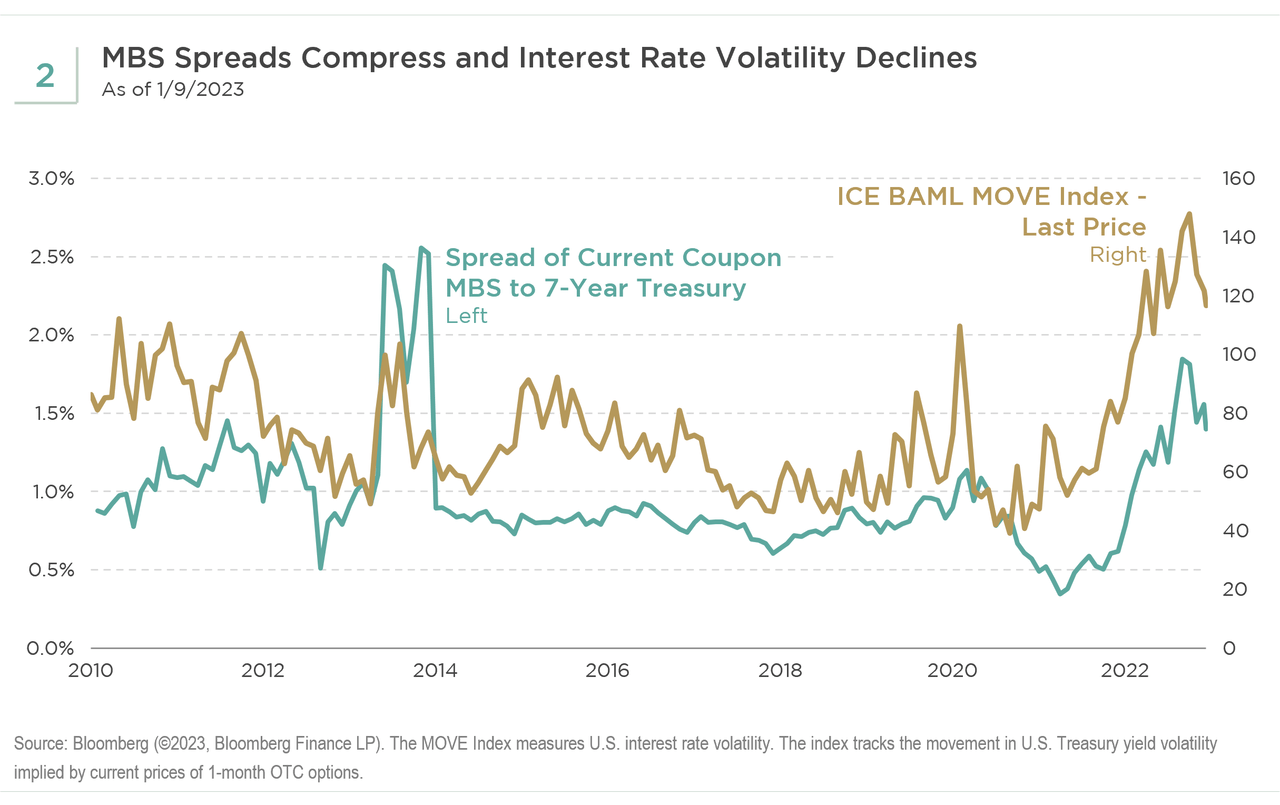

The MBS spread to Treasuries peaked in late October and has compressed by about 40 to 50 basis points (bps) along with the interest rate volatility declining (see Chart 2).

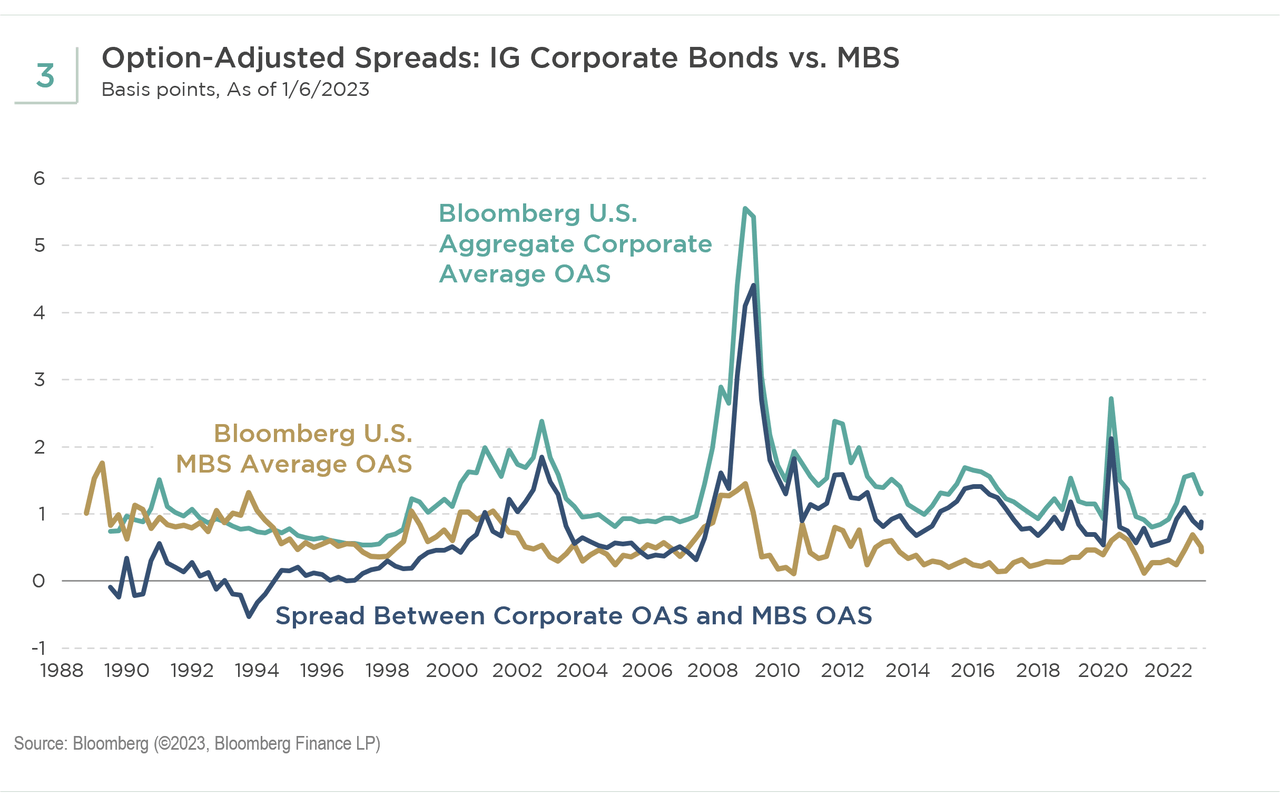

At the same time, the spread between investment grade corporate bonds and MBS option-adjusted spread (OAS) is still rather tight, which suggests more room for MBS spreads to tighten relative to higher-grade corporates since the corporate bond valuations are richer than the MBS historical pattern (see Chart 3).

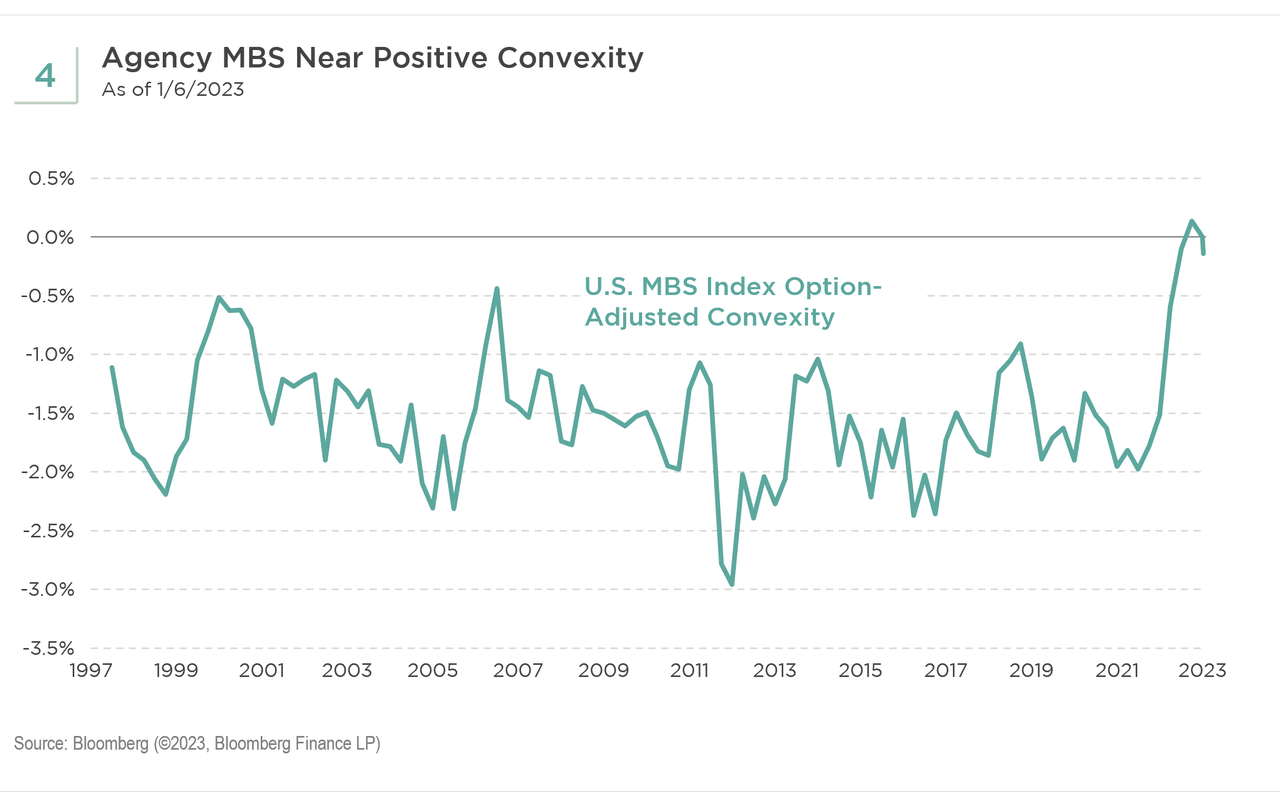

Agency MBS are starting to exhibit almost positive convexity, which is unprecedented in history, providing great fundamental value (see Chart 4).

What are the factors that continue to support the trade and what are the risks? What is our outlook for MBS in 2023?

We believe the opportunity in agency MBS has more room to run. Factors that should continue to support the investment include: The further moderation of interest rate volatility, resulting from the Federal Reserve’s effective taming of inflation and expected monetary pivot; the least negative convexity seen in some time—and even the potential for convexity to turn positive—unlocking fundamental value; and more buying interest from money managers, banks, and potentially even foreign buyers. There are some potential risks to consider though. Interest rate volatility could increase rather than moderate, triggered by runaway inflation and/or a major selloff in the global sovereign bond market. While not expected, the latter could be sparked by an event like an abrupt change in the Bank of Japan’s yield curve control, for example. Overall, however, we believe agency MBS should outperform other spread products in a recessionary scenario in 2023.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment