Win McNamee

Investment thesis

In my view, the 2022 stock market has been a mystery wrapped in a riddle inside an enigma, and then some. I would like to think that 2023 would be less volatile but that may be wishful thinking given the caveats on the horizon related to the U.S. economy, inflation/interest rates, corporate sales growth and profit margins. On 12/7/22, Seeking Alpha reported that “98% of CEOs predict recession in 2023 – Conference Board.”

As we approach 2023, I am 99.44% sure that a recession will occur in 2023, perhaps in H1. The key question in my mind is how long and how deep. This article addresses my thesis that the closing price of the S&P 500 at 12/31/23 will be 3,774.

Me and my BA degree in Economics vs. 20 Wall Street professionals

Admittedly at the onset of my quest, I was a tad squeamish about my ability to compete against this star-studded lineup. But the fact is it is very difficult to predict more than a year in advance where the S&P 500 will be. And the “experts” have done a woeful job doing so in 2022 as the average estimate was 4,825 according to the New York Times. Here is a graph of the Index, which is at 3,844.82 as of 12/23/22:

seeking.alpha.com

So unless there is a 981 point Santa Claus Rally in the next 4 trading days, the experts will have been wrong in 2022. And this is why I believe that I have more than a “puncher’s chance.” According to financialsamurai.com, the median prediction for 12/31/23 is 4,050 with a high of 5,000 and a low of 3,675. The wide range of 1,325 in predictions underscores the lack of consensus among the Wall Street gurus. The specific metrics I used to calculate my prediction of 3,774 (which was influenced by the last 3 consecutive weeks of losses in the S&P 500) are explained elsewhere in this article.

“It’s the Fed stupid!”

Thank you James Carville for the inspiration of my slogan, which may seem simplistic to some. But my point is that the Federal Reserve is fundamentally at the core of where the S&P 500 may be headed in 2023. Jerome Hayden “Jay” Powell, the much-maligned Chair of the Federal Reserve, has become the poster child for essentially everything “wrong” with the economy in my view. Let us take a peek at what some of his detractors say about him, shall we?

Critics abound around Powell

Here are some representative snippets of anti-Powellisms: Time has said that he “has changed the Fed forever” and probably not for the good. Bloomberg News stated that he was “Wall Street’s Head of State”. Then-President Donald Trump cited Powell as “an enemy”- although to some that may be considered a compliment. My own personal favorite Powell invective was his insistence that inflation was “transitory” for what seemed like forever despite considerable evidence to the contrary. On Capitol Hill, one of the Chair’s staunchest critics is Senator Elizabeth Warren, who has incessantly vilified his tenure by stating that the Fed’s interest rate hikes will not address the primary current drivers of inflation (i.e. food and gas prices) and risk pushing the economy into a recession. I fully expect that Warren will unleash her full pit bull DNA against Powell by escalating her “How Many Millions Will be Thrown out of their Jobs?” rhetoric a nanosecond after unemployment increases by 0.10% here in Massachusetts.

Jim Cramer’s take

Jim Cramer, the irrepressible host of CNBC’s “Mad Money” is arguably one of the most vocal cheerleaders of the Powell game plan. Cramer is constantly proselytizing to his audience that Powell will stop inflation by “any means necessary” even at the risk of a recession. Why he thinks this phrase is a good thing escapes me.

My bottom line

I do not have the time (nor the inclination) to study 100 years of market crashes as Wall Street strategist Greg Boutle did to come up with his 2023 prediction of 3,400 for the S&P 500 at 12/31/23. (Spoiler alert- his 2022 prediction was 5,100) Unlike the U.S. head of equity and derivative strategy at BNP Paribas, I do not have a large (or any for that matter) staff, access to a Bloomberg terminal, copious qualitative and quantitative research reports, high-priced analytical, mathematical and statistical computer models and other tools of the trade that he and many other professionals likely have at the ready 24/7/365. So I resorted to an old-school approach:

en.wikimedia.com

The above supply and demand model served me well in my 10/27/19 article here at Seeking Alpha and I believe it is applicable for this exercise as well. If margin compression occurs, and inflation remains significantly above the historical norm of 3.8%, I believe that the stock market as a whole, and the S&P 500 in particular, will be subject to much froth in 2023, and P/E ratios will drift downward. Combined with a historic inverted yield curve, rising unemployment and waning consumer confidence will signal recessionary fears.

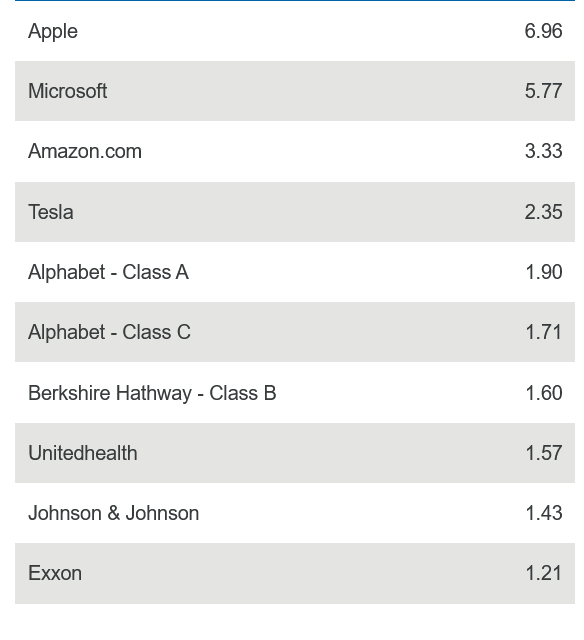

I took a top-down approach in my attempt to predict the closing price of the S&P 500 at 12/31/23, and focused on the following top 10 market capitalization stocks (and their respective %s ) of a popular S&P 500 Index Fund:

www.fidelity.com

On an aggregate basis, the 5 tech stocks in this group- Apple Inc. (AAPL), Microsoft Inc. (MSFT), Amazon (AMZN), Alphabet Inc. (GOOGL) and (GOOG) make up ~20% of the S&P 500. They have decreased an average of 36.6% during 2022, and most stock pundits expect a slowdown in this sector in 2023. I share this view, but I also believe that AAPL and AMZN are the 2 big tech stocks that have the best chance of rebounding in 2023. However, I also think that it is unlikely that Exxon Mobil Corporation (XOM) can duplicate its 70+% increase in 2023, which means that the energy sector as a whole is vulnerable YOY. The health sector may do well, and I consider UnitedHealth Group Incorporated (UNH) best of breed. I computed expected earnings for each of the above group, and extrapolated (as best I could) the earnings of the rest of the cohort. Specifics are contained elsewhere in this article. But first let me try to put the Chair’s role in perspective.

The Chair is not the Grim Reaper

In my view, Powell’s missteps, especially the fact he was late to the party in terms of addressing inflation – which has since reached a 40 year high- are venial sins, so to speak. He was not responsible for the $5T in stimulus funds issued by the Biden administration, which materially increased the money supply and contributed to the increase in inflation. The Russian invasion of Ukraine was an event virtually no one saw coming, and has wreaked havoc on our economy. In addition, the recently-passed $45B aid package To Ukraine will further hamstring our citizenry in my opinion. But what I ponder the most is – has Powell learned from his mistakes? The jury is still out, and I think he risks losing much of his credibility if the Fed-mandated recession escalates, and we fall into a deep and protracted economic downturn with significant job losses. 2023 is the tipping point of his tenure as Fed Chair and will likely in large measure determine his legacy.

The 12/31/23 S&P 500 close

As I previously stated, I focused on the top 10 market capitalization stocks in a popular S&P index fund to predict the S&P 500 at 12/31/23. Admittedly my rigor was somewhat limited and non-traditional to many of the other contestants in this contest. But keep in mind readers that the stock market is my avocation, and not how I make my living. However, as the saying goes, “you have to be in it to win it” right? That said, I estimated 2023 earnings of $43.66 for the top 10 market capitalization stocks and $178.34 for the rest of the cohort. I then assigned a P/E multiple of 17 to this $222.00 total. This resulted in an S&P 500 of 3,774 at 12/31/23.

Black swans and other risks

The future of the war in Ukraine is probably the risk factor that is the most unpredictable at present and so the bet on the economy also includes a bet on the future of the war in Ukraine. I am agnostic about how this situation may evolve in 2023, as geopolitical winds could swirl more when the Republicans regain control on the House. And the Democrats appear to be lurking ominously and ready to pounce on any future Powell gaffes. In terms of other risks, one fear that I have is the possibility of military aid to Taiwan beyond the $10B annually until FY27 that was recently approved. This would result in widespread ramifications, and would prolong challenging economic times for an indeterminate period of time in my view. And of course derail my chance to capture 1st place in this contest.

Conclusion

2022 has been a disappointing year for the stock market, as evidenced by the 19.84% YTD loss in the S&P 500. As the Chair of the Federal Reserve, Jerome Hayden “Jay” Powell has faced harsh criticism for his handling of the economy. He is hell-bent on reducing inflation to 2%, a goal which I consider fanciful for 2023. I think his strategy runs the risk of failing miserably, especially if world turmoil clouds the economic climate, both domestically and globally. Based on current conditions, it appears that recessionary fears may rise precipitously in H1 2023, possibly as early as mid-Q1. Potential headwinds include a weakening of the U.S. labor market, declining corporate sales, narrowing operating margins and lower profitability across the broad spectrum of industries. Time (as well as a horde of strong constituencies) will not be on Powell’s side if our economy goes from bad to worse. And the chances of a soft landing would be somewhere between zero and none, especially if the Fed pivots. Let us all hope this does not happen, and 2023 is less volatile stock market wise and otherwise.

Editor’s Note: This article was submitted as part of Seeking Alpha’s 2023 Market Prediction contest. Do you have a conviction view for the S&P 500 next year? If so, click here to find out more and submit your article today!

Be the first to comment