carolo7/E+ via Getty Images

Politicians were mostly people who’d had too little morals and ethics to stay lawyers.”― George R.R. Martin, Ace in the Hole

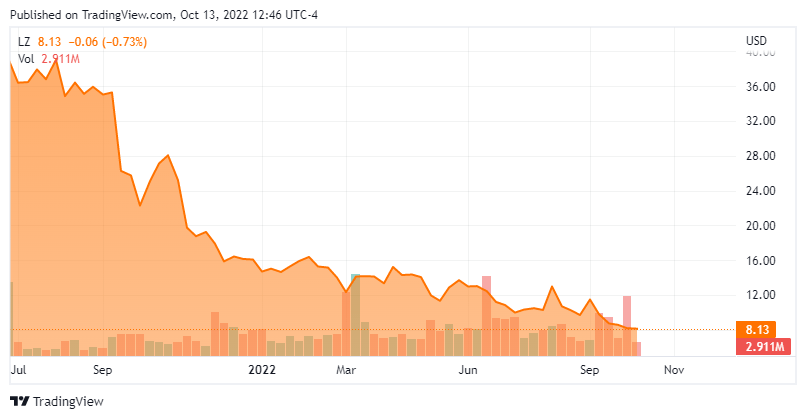

Today, we put LegalZoom.com, Inc. (NASDAQ:LZ) in the spotlight for the first time. The stock is down some three quarters of the levels it came public. However, the company has a nice profit growth trajectory in front of it and also has a rock-solid balance sheet. An analysis follows below.

Seeking Alpha

Company Overview:

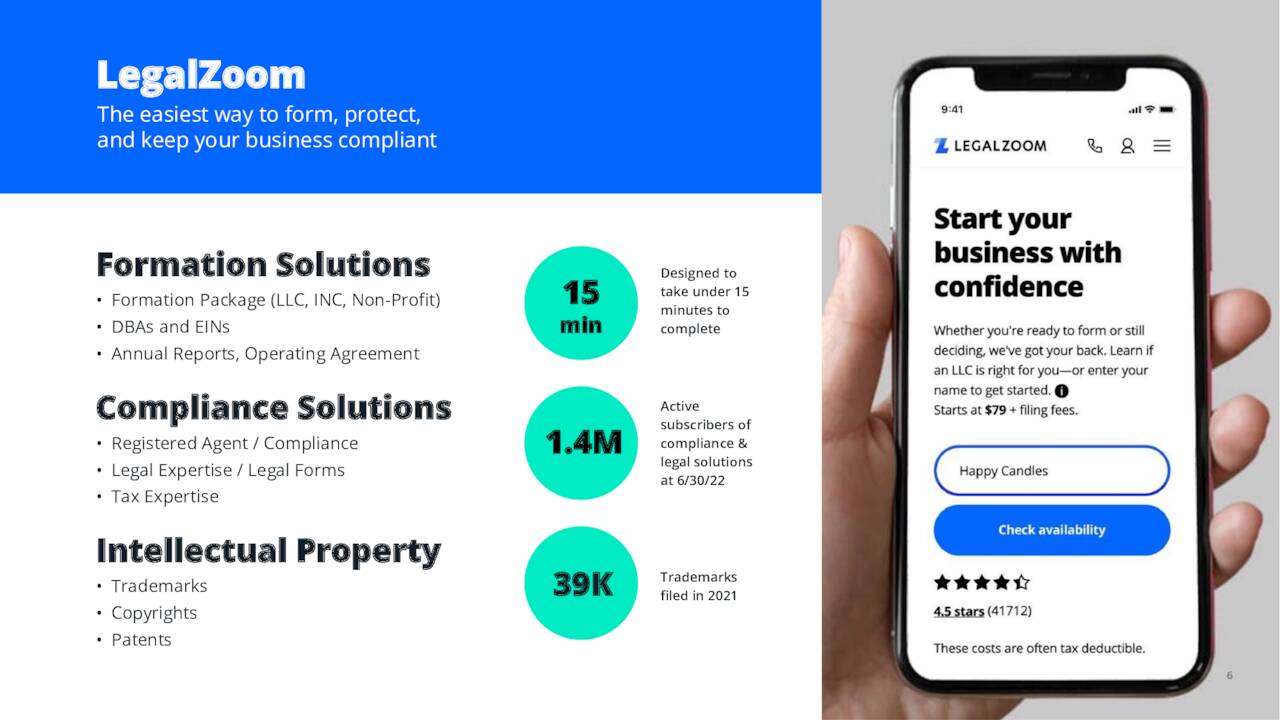

LegalZoom.com, Inc. is headquartered just outside of Los Angeles. The company operates an online platform for legal and compliance solutions in the United States. LegalZoom provides services/documents that allow their customers to execute business formations, create estate planning documents, protect intellectual property, complete certain forms and agreements as well as provide access to independent attorney advice, and connect customers with experts for tax preparation and bookkeeping services. The stock currently trades around eight bucks a share and sports an approximate market capitalization of $1.6 billion.

August Company Presentation

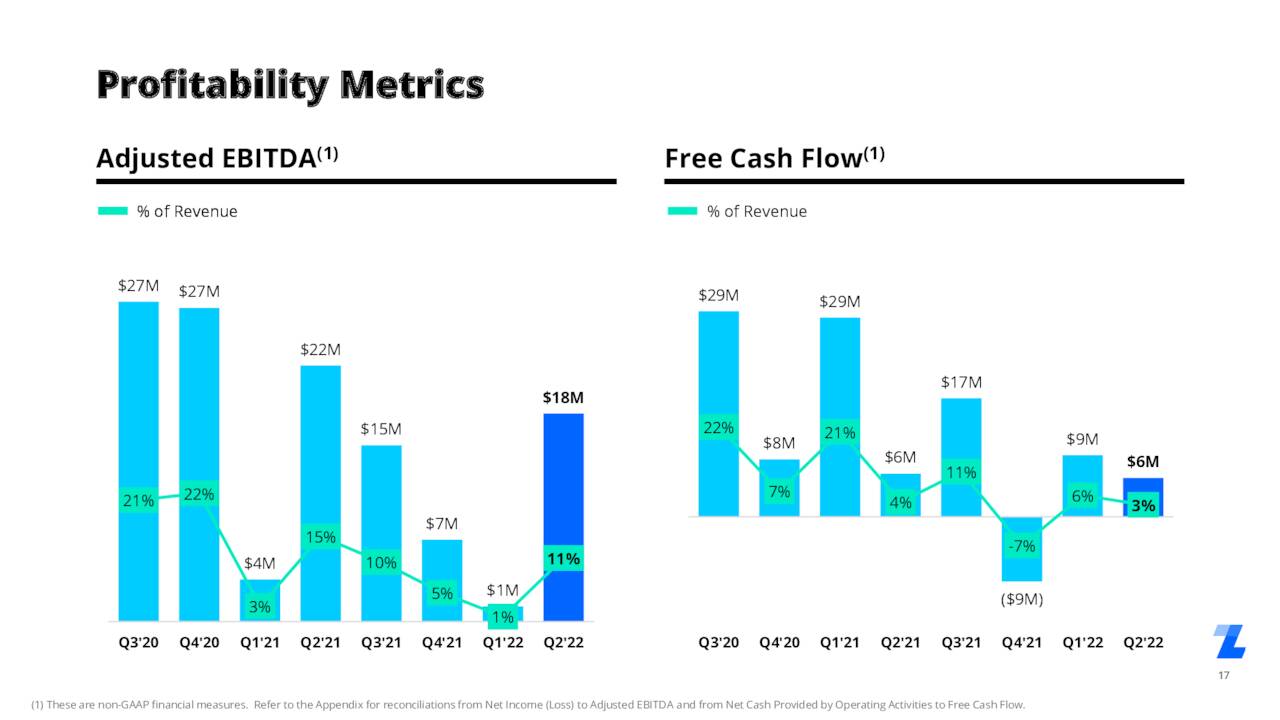

Second Quarter Results:

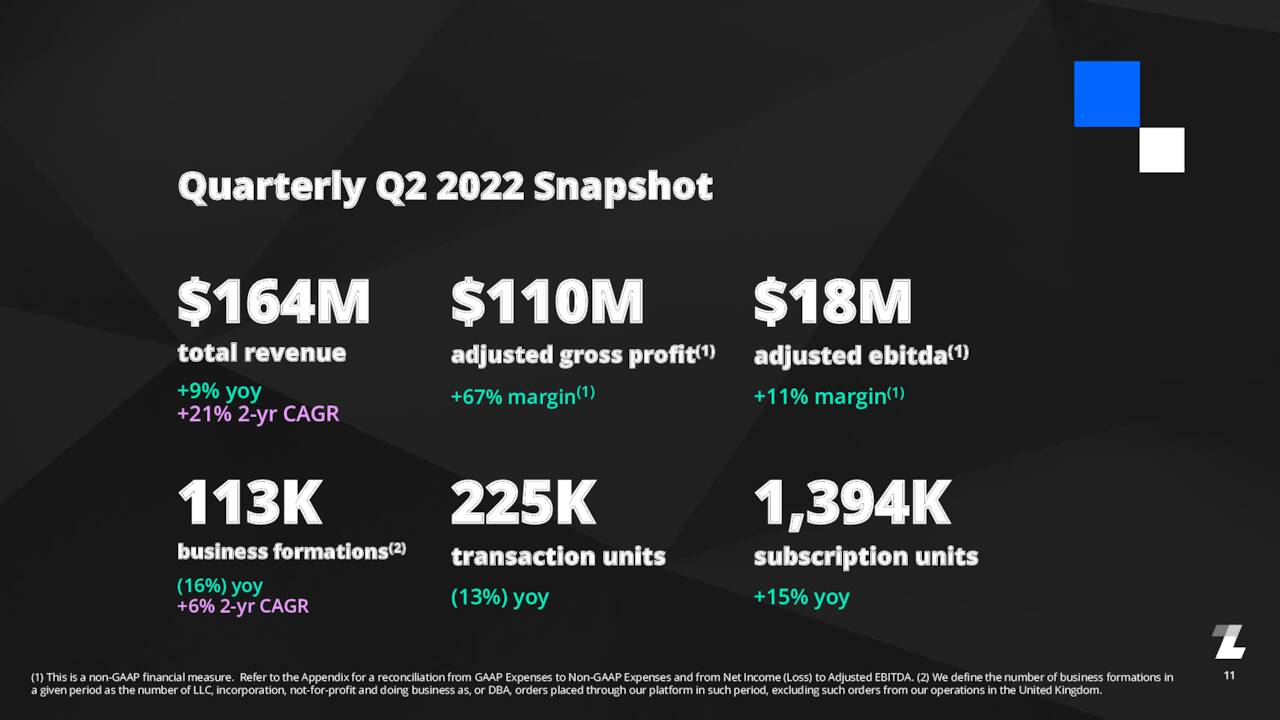

On August 11th, the company posted second quarter numbers. On a non-GAAP basis, LegalZoom earned a nickel a share, three cents above expectations. Revenues rose nearly nine percent on a year-over-year basis to $164 million, slightly beating the consensus.

August Company Presentation

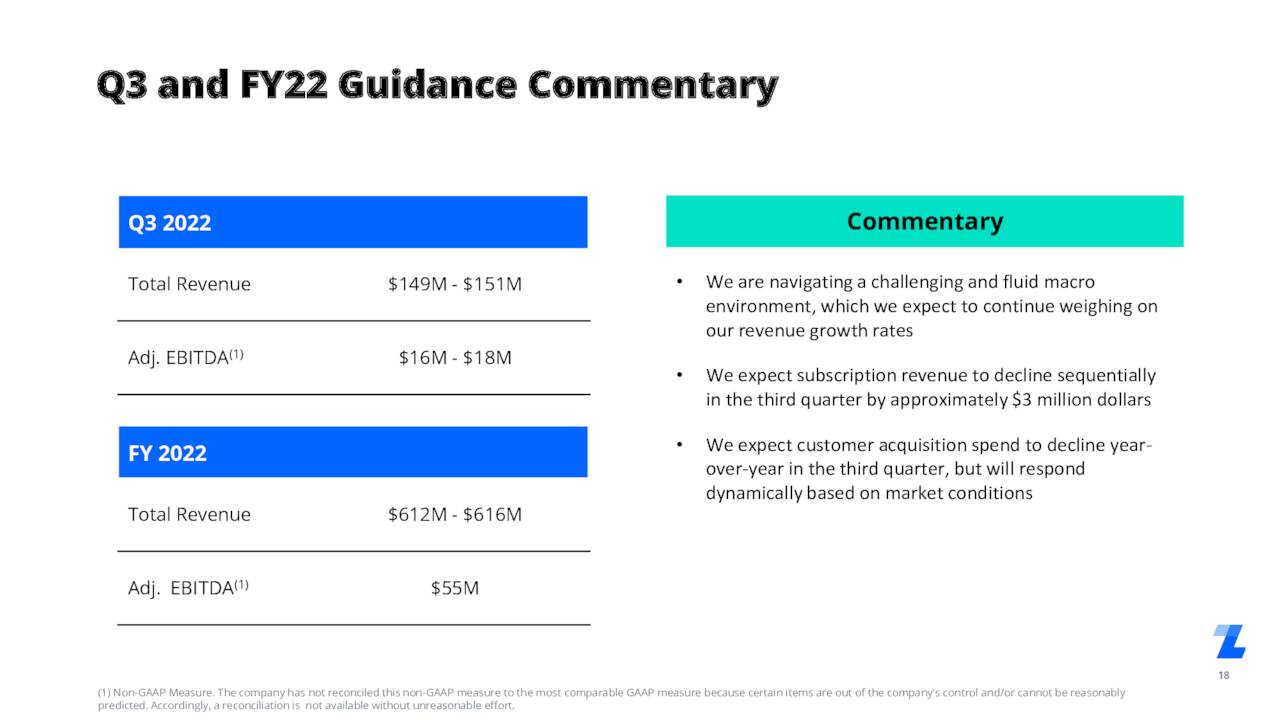

However, management then adjusted its Q3 sales guidance downward to Revenue is expected to be in the range of $149 million to $151 million, which was approximately $20 million light of the existing expectations at the time. Due to cost controls, the company was able to raise its forward Adjusted EBITDA to a range of $16 million to $18 million in Q3. Full year sales are now expected to be in the $612 million to $616 million range, down from previous guidance of $650 million to $660 million.

August Company Presentation

It should be noted that subscription revenue grew 32% year-over-year to $91.3 million and now represents 55% of overall sales. Transaction revenue fell 9% from the same period a year ago to $66.5 million. Partner revenue was also down to $6.1 million from $7.7 million in 2Q2021. Gross margins fell to 65% from 67% previously.

Analyst Commentary & Balance Sheet:

Since second quarter results were posted, three analyst firms, including Credit Suisse and Citigroup, have reissued Buy ratings. Price targets proffered range from $16 to $19 a share. Meanwhile, Morgan Stanley ($7 price target), JMP Securities and Jefferies ($12 price target) have maintained Hold or Underweight ratings on LegalZoom.

August Company Presentation

Just under seven percent of the outstanding float in the shares is currently held short. Several insiders have been frequent sellers of their shares in 2022, disposing of just over $2 million in aggregate so far in 2022. There have been no insider purchases in this equity so far this year. The company ended the second quarter of this year with approximately $215 million worth of cash and marketable securities on its balance sheet against no long-term debt.

Verdict:

The current analyst firm consensus has LegalZoom earning a dime a share in FY2022 as revenues rise 6% to 7% to just under $615 million. Next year they predict 9% sales growth and earnings of a quarter a share. The company had just three cents a share of profit in FY2021.

LegalZoom does have some positive attributes. It is becoming increasingly profitable and it has a pristine balance sheet with no debt. However, the stock is still quite expensive at approximately 80 times this year’s projected earnings and over 30 times FY2023’s projected EPS. This is especially true for a concern growing sales in the five to ten percent range. The equity is slightly less expensive if you account for its net cash position.

Analyst firms are lukewarm on LegalZoom’s prospects, there is also no insider buying despite a significant decline in the shares since the IPO. Add in the reduced sales guidance for Q3, I can’t get into the ‘buy zone‘ quite yet on LZ. If the equity fell into the $5 to $6 range, I could see myself taking a small ‘watch item‘ holding name at lower prices, however.

The minute you read something that you can’t understand, you can almost be sure that it was drawn up by a lawyer. “― Will Rogers

Be the first to comment