Darren415

This article was first released to Systematic Income subscribers and free trials on Sep. 15.

The steep sell-off this year has turned some of the usual income market dynamics that investors have come to rely on upside down.

The first of these patterns is that quality is no longer a reliable marker of performance during a downturn. Specifically, many investors believe that higher-quality securities will always hold up better during periods of market weakness than lower-quality securities. The fact that investment-grade corporate bonds have delivered a -17% total return this year versus the -3.5% return for much lower-quality assets like bank loans highlights that this single-dimension approach to security analysis is not fit for purpose.

The second pattern that has surprised some investors is that higher-yielding securities did not necessarily underperform this year. While some high-yielders have clearly suffered, not all have. In this article we take a look at those securities which carry attractive yields and which have weathered the current market storm very well. These securities have not only attractive yields but also provide a relatively stable capital base with which to allocate to higher-beta assets during drawdowns.

Some Ideas

It’s easy enough to find securities that have held up well this year. What’s more challenging is to find securities that offer a decent high single-digit yield that have also held up well. By and large securities that share these characteristics are modest maturity bonds.

It’s true that a number of Fix/Float preferreds have been resilient this year also, however, this has happened primarily because short-term rates have spiked higher. And while it’s very unlikely that short-term rates fall back lower in the medium term, these securities remain vulnerable to a drop in short-term rates just as they were in 2020 when they underperformed their fixed-rate preferred counterparts.

The other reason we focus on modest-maturity bonds over Fix/Float preferreds is because bonds will tend to have a lower credit spread duration relative to preferreds. In other words, by virtue of their maturity a bond has less sensitivity to changes in credit spreads than a perpetual preferred, all else equal. Having a maturity makes bonds fundamentally lower-beta than preferreds, all else equal.

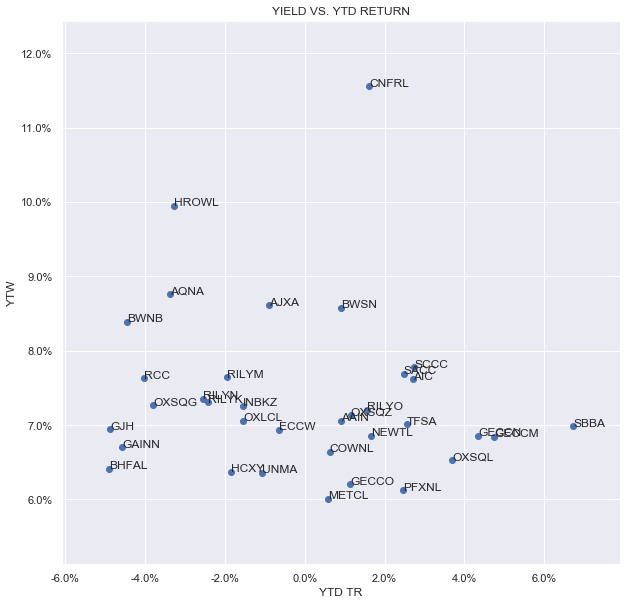

The chart below shows securities with yields above 6% and that have seen a total return this year of better than -5%. What these securities have in common are a moderate maturity, decent quality, and relatively high yield to offset a negative price move.

Systematic Income

In our view, securities that are, in effect, portfolios of financial assets can be more compelling assets than traditional companies because they are much more diversified in their holdings, much easier to analyze and, for these reasons, much easier to have a high level of conviction around. These securities include bonds issued by BDCs, CEFs and mortgage REITs.

Some of these securities that remain attractive in our view are:

CLO Equity CEF OXLC 6.75% 2031 Notes (OXLCL) trading at a 7.06% yield-to-maturity with a -1.5% total return this year.

mREIT AAIC 6.75% 2025 Notes (AIC) trading at a 7.6% yield-to-maturity with a +2.7% total return this year.

BDC OXSQ 6.25% 2024 Notes (OXSQZ) trading at a 7.14% yield-to-maturity with a +1% total return this year.

We would also include the financial services firm B. Riley Financial bonds, specifically, their 5% 2026 Notes (RILYG) which look cheap versus other bonds at an 8% yield as well as the mREIT Sachem Capital bonds such as the 6.875% 2024 (SACC) with a 7.7% yield.

Takeaways

Headlines that promise securities that will “soar”, “fly” or “zoom” are a dime a dozen. What can be more useful to some investors than promises of boundless upside are securities that don’t collapse in a period of market weakness. Such securities carry a low opportunity cost versus other even higher-yielding assets while providing investors with a relatively stable base of capital from which to chase higher-beta opportunities during drawdowns. This can allow investors to sustainably grow the income level of their portfolios and generate significant alpha over time.

Check out Systematic Income and explore our Income Portfolios, engineered with both yield and risk management considerations.

Use our powerful Interactive Investor Tools to navigate the BDC, CEF, OEF, preferred and baby bond markets.

Read our Investor Guides: to CEFs, Preferreds and PIMCO CEFs.

Check us out on a no-risk basis – sign up for a 2-week free trial!

Be the first to comment