wildpixel

It has become a hackneyed tradition among market analysts to make predictions for the year ahead at the start of every New Year. More than 25 years in the business have taught me to refrain from this practice due to the sheer number of variables involved in predicting that far ahead into the future. For 2023, however, I’m making an exception and will offer up four predictions of what look like probable occurrences in the coming months.

With so many critical social, economic, and geopolitical trends in play right now, to not discuss these factors would be a dereliction of duty for any market analyst. With that said, let’s take a look at four key developments that I see taking place in the year ahead.

Prediction #1: Inflation will persist

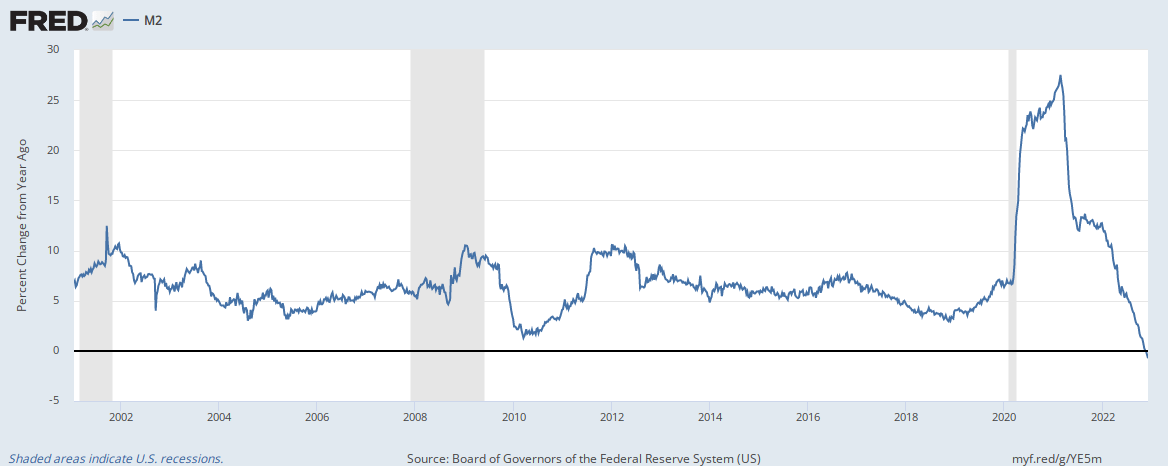

One of the themes frequently bandied about in the final months of 2022 was that inflation had peaked and would begin diminishing sometime in 2023, likely around mid-year. A chart that has gained currency in the economic blogosphere of late is the year-over-year percentage change in the M2 money supply. It shows a precipitous collapse into negative territory after the stratospheric rise to record levels in the wake of the events of 2020. This graph is being widely used as Exhibit A in the case that inflation is on its way out.

St. Louis Federal Reserve

One problem with using this graph to make inflation predictions is that it obscures the fact that 2020-2021 witnessed an obscene increase in M2 in the wake of the shutdown. In other words, it’s a mistake to make comparisons with that once-in-a-lifetime outlier event. Of course the M2 growth rate looks much better now compared to then. But the overall M2 money supply is still in a long-term growth trajectory.

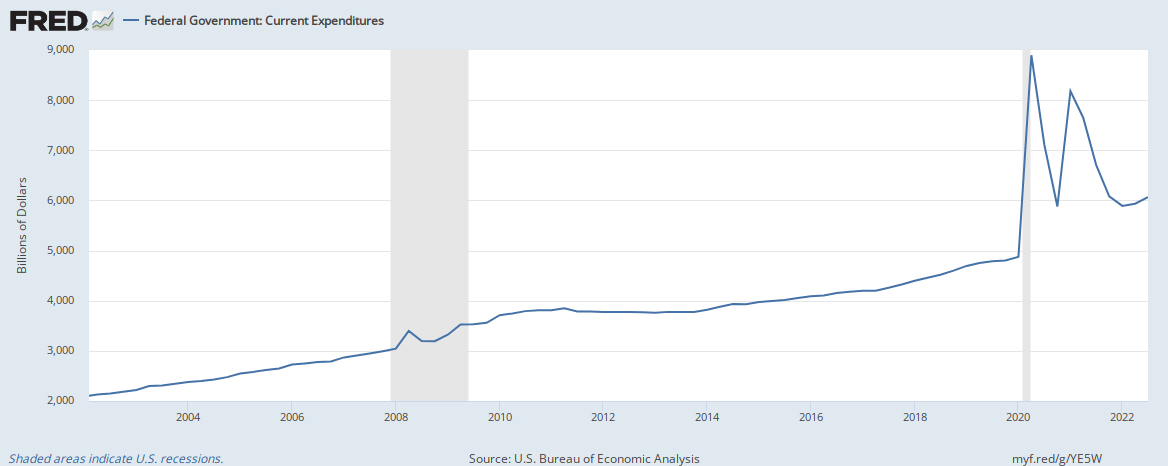

Another point is worth making on this subject. We’re all familiar with the bromide made famous by Milton Friedman that “inflation is always and everywhere a monetary phenomenon.” But inflation is also a political phenomenon, and this is made is abundantly clear by the runaway government spending levels of the last three years (see chart below).

St. Louis Federal Reserve

Even with the year-over-year M2 growth rate collapsing, government transfer payments are near record levels and are keeping people out of the workforce (hence the widely known problem of understaffed businesses). This in turn is fueling a chronic problem of undersupply and understaffing across many industries, which in itself can be inflationary. (Remember, the classic definition of inflation is “too much money chasing too few goods,” which means the supply component is as important as the monetary component.)

Another reason for expecting inflation to remain a problem in 2023 is the phenomenon known as “cost-push,” which involves rising wages and higher prices for the commodities used to make goods. One factor that kept consumer prices from spiraling out of control last year was the relentless strength in the U.S. dollar index. But with the dollar now beginning to weaken, commodity prices are likely to increase in the coming months. This in turn means the currently high prices that consumers are now paying on the retail level likely aren’t going to diminish anytime soon and may actually increase further.

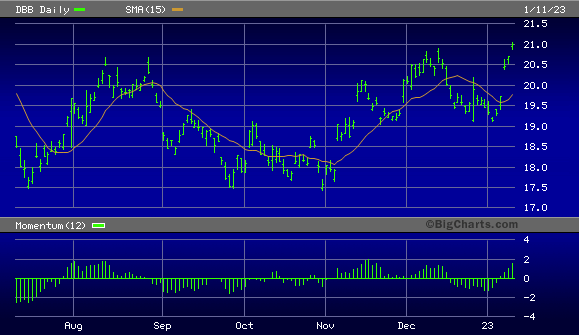

An example of a highly inflation-sensitive commodity group already showing signs of galloping higher is industrial metals. The Invesco DB Base Metals Fund (DBB) has just hit its highest level since last summer—a harbinger of the newfound strength in the metals and other commodities as the dollar weakens.

Big Charts

Yet another factor likely to propel persistent inflation pressures this year is China’s economic rebound—a virtual certainty in 2023 after its government dropped its zero-Covid measures last month. China’s hunger for raw materials as its manufacturing sector recovers will add to the cost-push inflation for the global economy. Which leads us to prediction number two…

Prediction #2: China and emerging markets will outperform

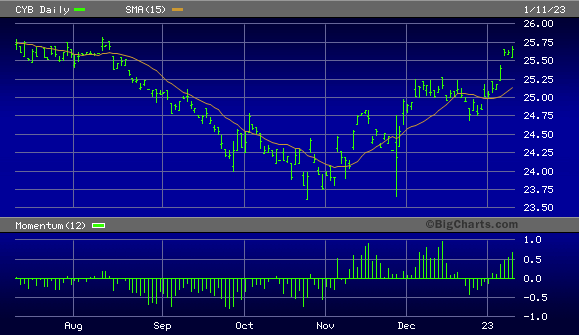

Among last year’s biggest losers were China and the emerging markets. A combination of restrictive Covid policies and a strong U.S. dollar put downward pressure on the economies of many foreign countries, led by China. But with the aforementioned weak dollar trend now in play, foreign currencies are in in the ascendant, including China’s Yuan currency. The powerful rebound in the WisdomTree Chinese Yuan ETF (CYB)—my favorite yuan proxy—tells the tale.

Big Charts

What China’s currency rebounding tells us is that its economic picture has brightened considerably in the wake of Covid measured being abruptly loosened. Travel demand is already starting to boom abroad, while consumer spending is slowly coming back in China. That gradual return to normal spending levels will likely accelerate in 2023 now that the restrictions have been lifted.

As a Bloomberg article on the emerging markets recently pointed out, “a strong U.S. currency generally means higher debt servicing costs and tighter financial conditions in the emerging world, and vice versa.”

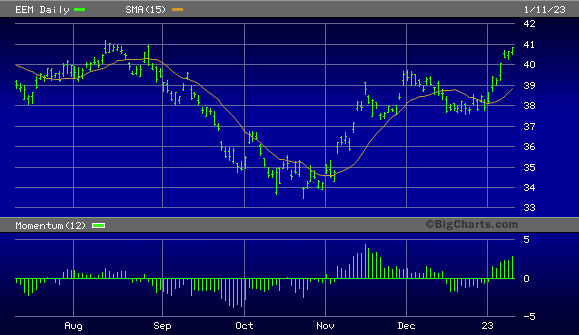

Along this line, as the trend toward de-dollarization expands in much of the emerging world economies continues, investors should expect stronger stock markets in countries like Argentina, India, Mexico and South Africa. The iShares MSCI Emerging Markets ETF (EEM) is a good way to have exposure to this trend, and I’m predicting a strong overall performance for EEM in 2023.

Big Charts

Prediction #3: No U.S. recession in 2023

Another forecast that has been widely disseminated in recent months is the supposed inevitability of a U.S. economic recession at some point this year. The reasons why many analysts are predicting recession are varied, but one of the indicators most commonly pointed to is the Treasury yield curve (specifically, the 10-year minus 2-year spread) which inverted in late 2022.

While it’s true that every yield curve inversion has been followed by recession within a year or so, the last inversion which preceded the 2020 recession comes with an asterisk. For that particular (and short-lived) recession was artificially created, the result of a nationwide economic shutdown. Without the induced shutdown, it’s questionable that a recession would have occurred that year.

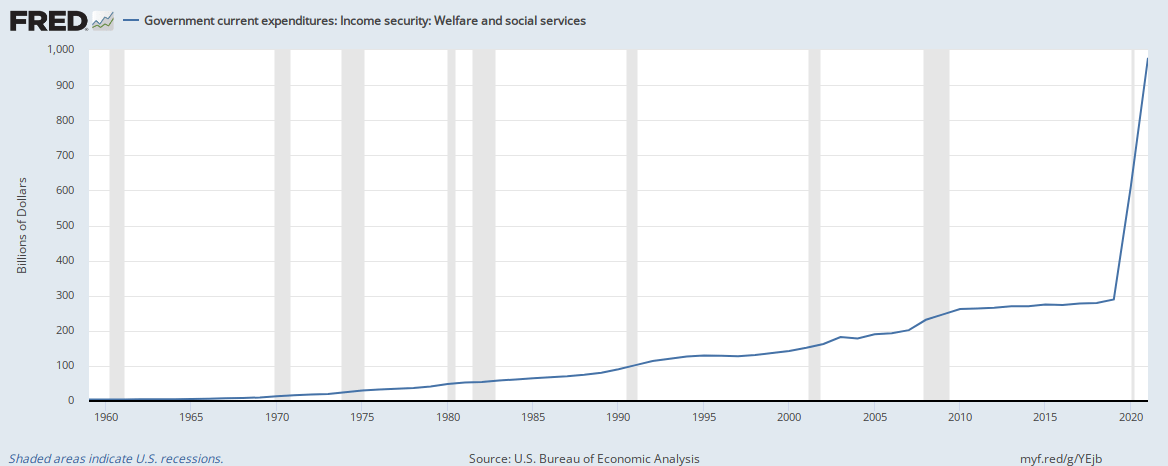

In any case, a strong reason for believing that recession will be averted this year can be summarized in the single “picture” shown below. This graph illustrates the explosive increase in government welfare and social services spending in the last couple of years. It partly accounts, IMO, for the chronic understaffing problem mentioned above. But I also think it explains the U.S. economy’s ability to dodge recession despite last year’s 40-year inflation peak.

St. Louis Federal Reserve

Transfer payments, in other words, are keeping millions of Americans above water. My prediction is that the relentless federal spending levels we’ve seen since 2020 will rescue the consumer once again in 2023 and avert recession.

Prediction #4: Wall Street rebounds

I discussed this theme in my previous Seeking Alpha article, so I won’t say as much about it here. Suffice it to say that near-record levels of small investor bearish sentiment, massive levels of short interest buildup and record numbers of bearish “dumb money” options trades suggest (from a contrarian’s perspective) that the stock market is setting up for a potentially big upside year in 2023. It certainly wouldn’t require much of a spark to ignite a massive short-covering rally.

In my opinion, that “spark” is likely to come from a combination of bottom fishing among investors seeking bargains among beaten-down assets (of which there are plenty), a resurgence in risk appetite (partly induced by the China/emerging markets rebound) and “hot” money inflows into basic materials and commodity-oriented stocks (including industrials) as the dollar weakens.

Be the first to comment