Kwarkot

Do you know the story of real estate investment trusts, or REITs? I’m trying to remember if I’ve written about it before in any real detail.

I’m sure I’ve at least mentioned it before. But the full account truly is an interesting one, both educational and entertaining.

I know the term “I persisted” is often associated with feminism. It might also come to mind if you saw that dramatization of the McDonald’s (MCD) franchise story, The Founder.

I believe it was the very last line of the movie, in fact. And it wasn’t a positive one.

Fortunately, that’s not the case with REITs. You could maybe say that the men behind their creation weren’t entirely altruistic. That’s almost undoubtedly an accurate statement.

However, you can be interested in getting something personal out of life without being selfish. That’s hopefully each of our stories as we strive to make money in the stock market.

We give our money to companies. Those companies use that money to fund their businesses. We then (hopefully) reap the rewards as the companies grow.

It’s an I-scratch-your-back, you-scratch-mine scenario. Or, put another (more encouraging) way, we help them out and they help us out in return.

That system encapsulates the best (and yes, sometimes the worst) of the capitalist system you and I engage in every time we trade.

And if the IRS gets a little less of our money in the process… how many of you are really going to object?

No Taxation Twice: the REIT Story Begins

So here’s how REITs came into existence, starting with this quote from The Intelligent REIT Investor:

“… few assets are more illiquid than commercial real estate such as office buildings, shopping centers, apartments, and the like. They’re also very expensive to own and operate, which made them a ‘boom and bust’ business in the past. Fueled by unreliable information (or at least a serious lack of good information), fortunes could be lost on these purchases.

“Then again, fortunes could also be made – provided one already had a small fortune to begin with. Commercial real estate was the quintessential ‘you’ve got to have money to make money’ example before the mid-twentieth century. It was a wealthy man’s game until REITs came along.”

Again, the first REIT model wasn’t developed with all of us in mind. It was instituted by a real estate management company in Boston, Massachusetts, for a real estate management company in Boston, Massachusetts.

The group wanted to avoid paying double taxes, and so it created a business trust model to do so.

The smirks of having outsmarted Uncle Sam only lasted so long though. The company was taken to court over its “evasive” actions and found at fault.

But that wasn’t that.

Down but not defeated, it hired Goodwin Procter to create a tax-efficient cake that could be eaten, too. The idea went all the way to Congress under the argument that commercial real estate investments should be available to the proverbial little guy.

Average Joe and Jane should have the same opportunities as the wealthy. Don’t you think? This is America after all…

In the end, Congress agreed. And this time, the legal decision went in favor of the real estate investors, who just wanted to make – and keep – a buck.

The Reality of REITs

As a result, REITs don’t have to pay the typical corporate taxes. Though there are catches to that corporate money kept, including:

- REITs must distribute a minimum of 90% of their annual taxable income – minus capital gains – to investors by way of dividends (most pay out 100%).

- REITs must have no less than 75% of their assets invested in something real estate-related, whether actual physical properties, mortgage loans, or shares in other REITs. The only exceptions to that rule is cash or government securities, which are allowed in the mix as well.

- At least 75% of REITs’ gross income has to come from rents, mortgage interest, or the proceeds from real property sold.

- REITs must have no less than 100 shareholders. And less than 50% of those outstanding shares can be held by five or fewer individuals.

This helps keep them from bending the rules to suit only their interests. They have to keep their investors – including the little guys and gals – in mind at most every turn.

There are still ways for them to mess up, naturally, unintentionally or otherwise. So never put your full trust in a REIT any more than with any other investment.

Overall, though, these entities really are a great tool for average investors. The wealthy can invest more into REITs and, therefore, reap greater rewards, naturally. Yet the little guy can enjoy commercial real estate gains he never would have been able to otherwise.

The dividends – which usually offer higher yields – sweeten this reality even further. Not only do we have stock price appreciation potential, we get compensated regardless. And in ways that allow us to put that extra money back into the stock for greater appreciation possibilities.

For all those reasons and more, I’m recommending the following REITs to my fellow investors – big and little alike.

3 REITs for the “Little Guy”

Mid-America Apartment Communities, Inc. (MAA) is a real estate investment trust that builds, acquires, manages, and leases multifamily residential properties. MAA was founded in 1977, went public in 1994, and is headquartered in Germantown, TN.

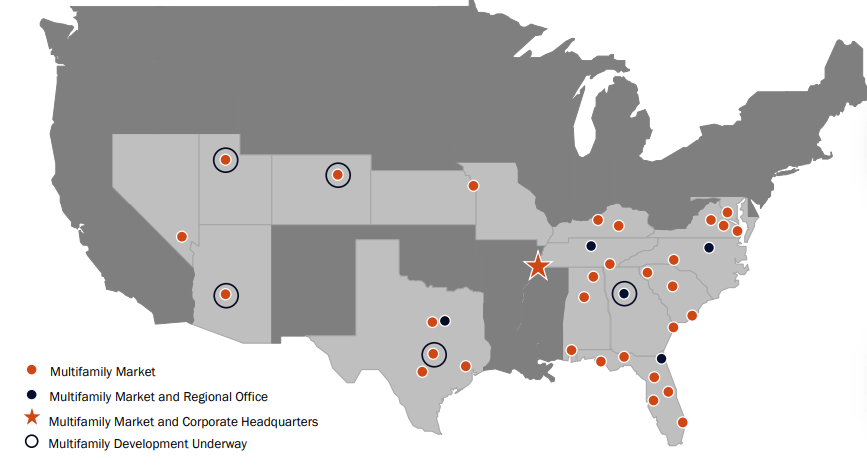

MAA has approximately 102,000 apartment units primarily located in the southeast, the southwest, and the mid-Atlantic.

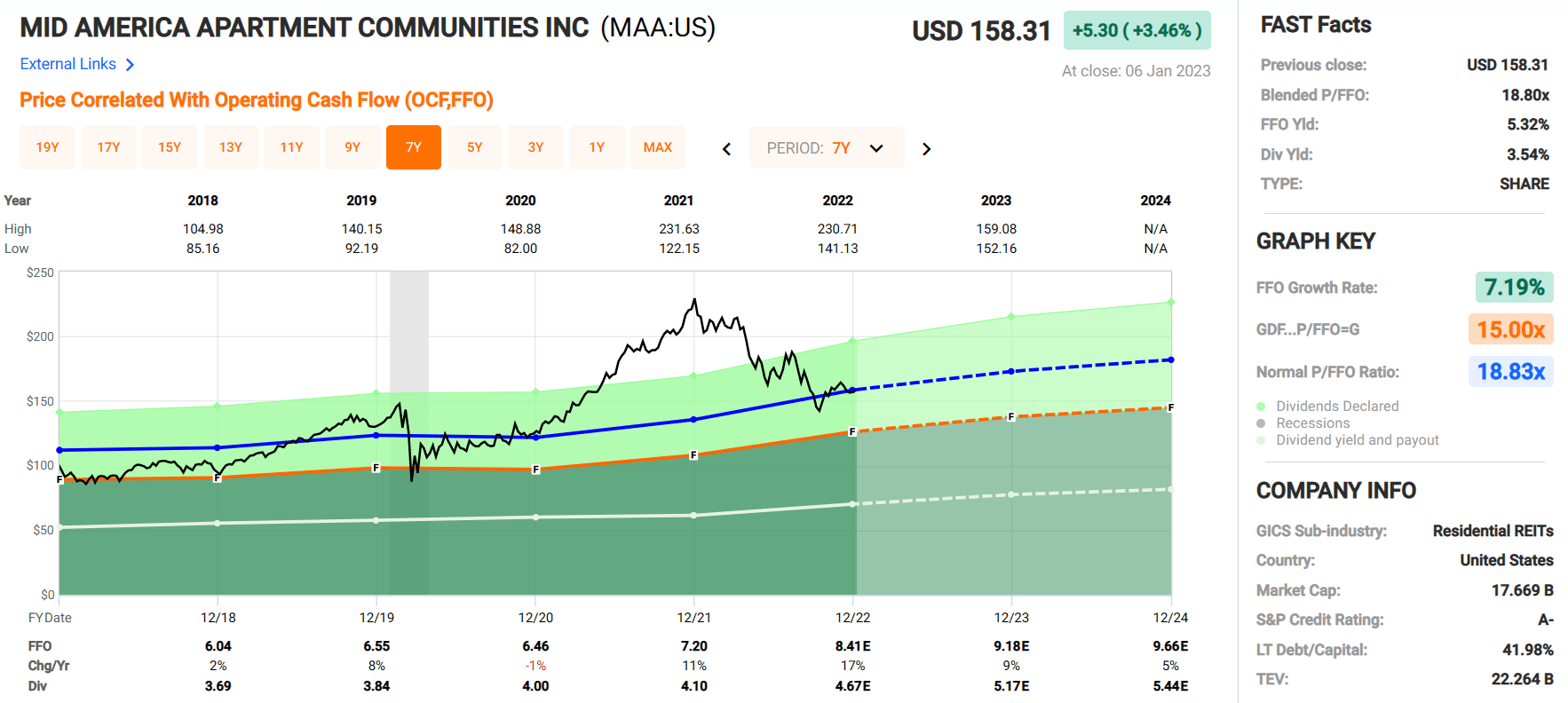

MAA – Investor Presentation

MAA has maintained a conservative balance sheet and has strong debt metrics. They have a weighted average interest rate of 3.4%, a weighted average maturity of 8 years, and 97.2% of their debt is fixed rate.

MAA’s Fixed Charge Coverage ratio is 6.1x, their Net Debt to Adj. EBITDAre is 3.97x, and they are investment-grade rated with a rating of A-.

MAA – Investor Presentation iREIT/BASE

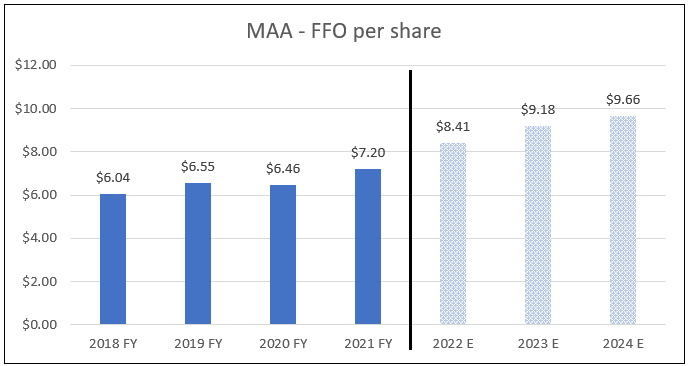

Mid-America Apartment has shown solid growth in its funds from operations (FFO) over the last several years, with an average FFO growth rate of 7.19% since 2018. Analysts are projecting 9% FFO growth in 2023 and 5% FFO growth in 2024.

MAA recently announced it expects to release 4th quarter and full-year 2022 results on February 1, 2023. FFO for 2022 is expected to come in at $8.41 per share.

FAST Graphs (compiled by iREIT)

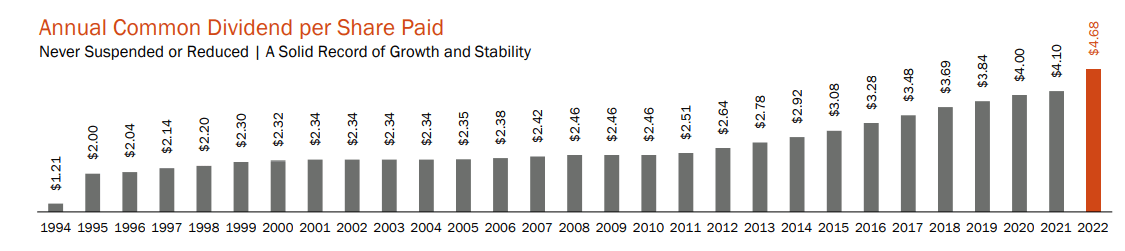

MAA has a great dividend track record as well. Since its IPO the dividend has never been reduced or suspended and has been increased consecutively for the last 13 years.

In December 2022, MAA declared a quarterly dividend of $1.40 which is a 12% increase over the prior quarterly payout of $1.25. The expected FFO growth trajectory should continue to fuel dividend growth over the coming years.

MAA – Investor Presentation

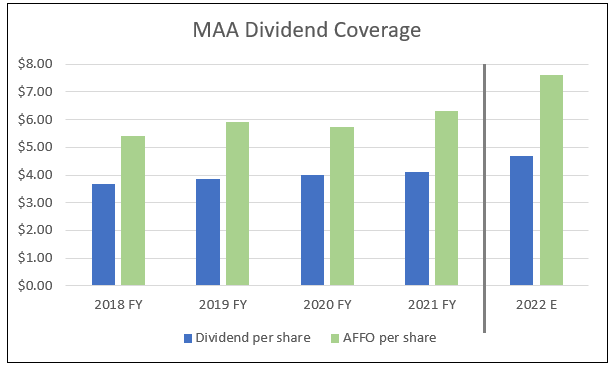

MAA currently yields 3.54% and the dividend is well-covered with an expected Adjusted Funds from Operations (AFFO) payout ratio of just 61.45%. The conservative payout ratio provides MAA the flexibility to grow the dividend or maintain the dividend if adverse events arise.

FAST Graphs (compiled by iREIT)

Currently MAA trades at a blended P/FFO multiple of 18.8x, which is in line with their historical average and trades just slightly over their Net Asset Value (“NAV”) with a P/NAV ratio of 1.02x.

While MAA is not trading at a significant discount to its normal valuation, this is a high-quality REIT that rarely goes on sale. It has a strong balance sheet with sound debt levels and a well-covered dividend that has been raised each year for over a decade.

At its current price, I would put MAA in the category of a great company for a fair value. At iREIT, we rate MAA a BUY.

iREIT FAST Graphs

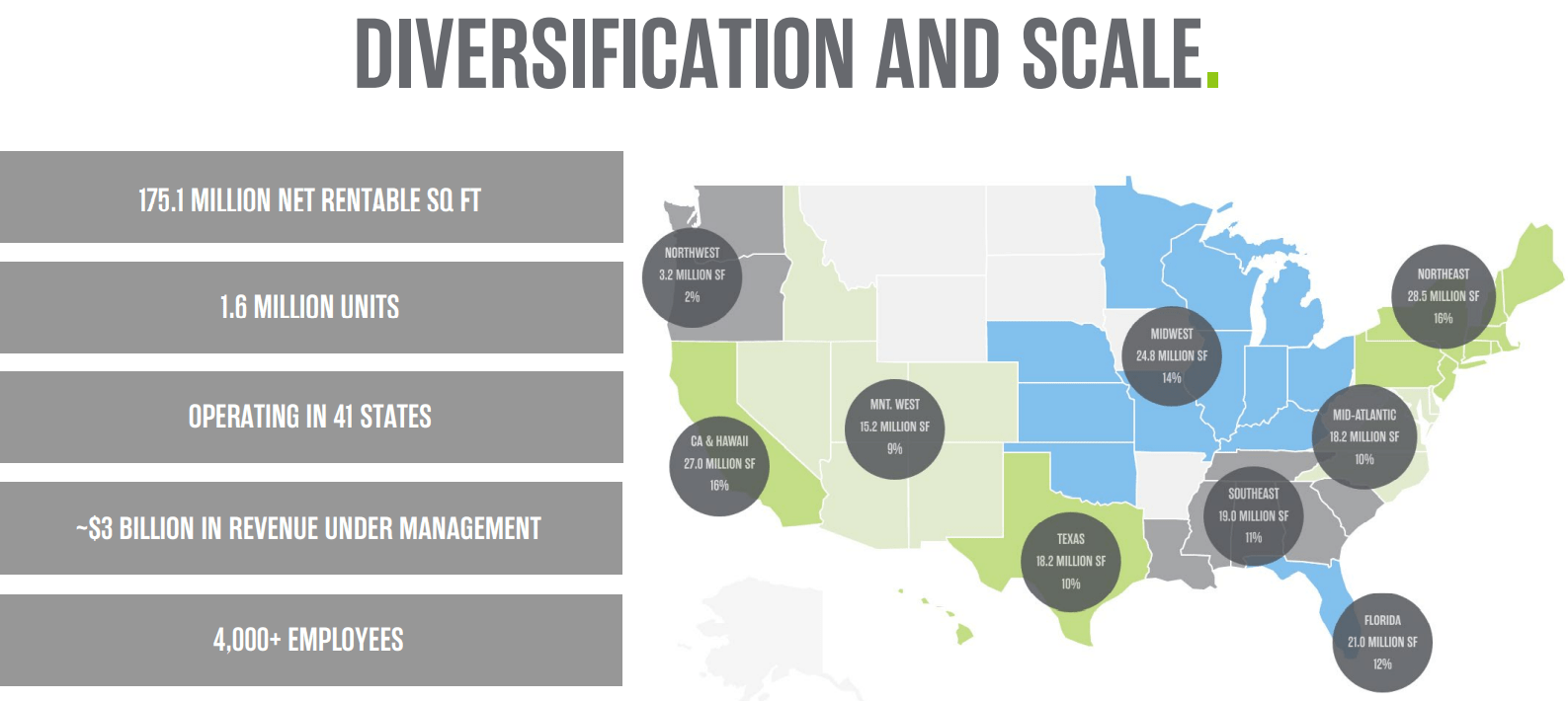

Extra Space Storage Inc. (EXR) was founded in 1977 and went public in 2004. It is currently the 2nd largest owner / operator of self-storage units in the U.S. with an interest in 2,327 properties. EXR owns 1,126 properties and has a joint venture (JV) that includes 315 properties, while managing 886 properties.

In all, EXR owns or operates 1.6 million units across 41 states for a total of 175 million rentable square feet.

EXR Investor Presentation

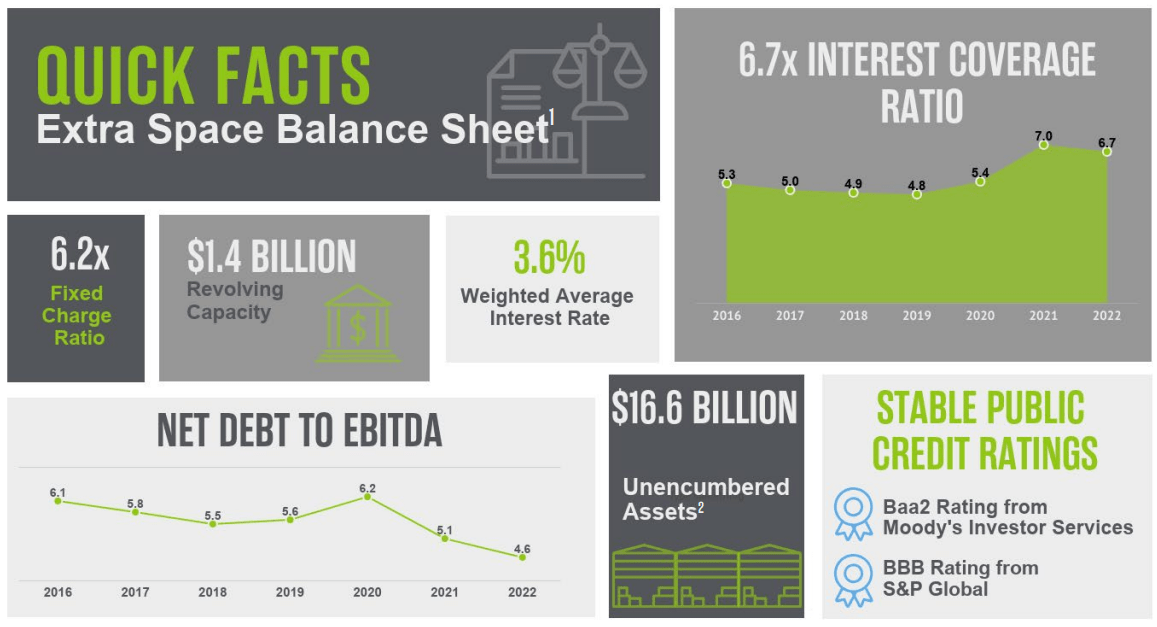

EXR has a strong balance sheet with a Net Debt to EBITDA of 4.6x, a Fixed Charge Coverage of 6.2x, and a weighted average interest rate of 3.6%.

They have a BBB credit rating from S&P Global and $1.4 billion capacity on their revolving lines of credit.

EXR Investor Presentation (Jan 2023)

The only concern that I see regarding their debt is that a relatively large amount of it is variable-rate.

As of 9/30/22, EXR’s percentage of fixed rate debt to total debt was 62.2% and their variable-rate debt made up 37.8% of their total debt.

In the current interest rate environment, this is something to keep in mind, especially if rates continue to rise and are sustained at higher levels.

EXR Form 10-Q

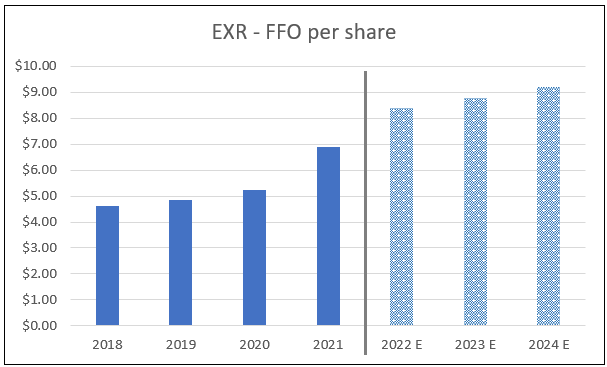

EXR has had outstanding growth in its funds from operations (FFO), with an average annual growth rate of 11.24% since 2018. EXR’s FFO is expected to grow by 21% in 2022 and then level off to a growth rate of 5% in both 2023 and 2024.

FAST Graphs (compiled by iREIT)

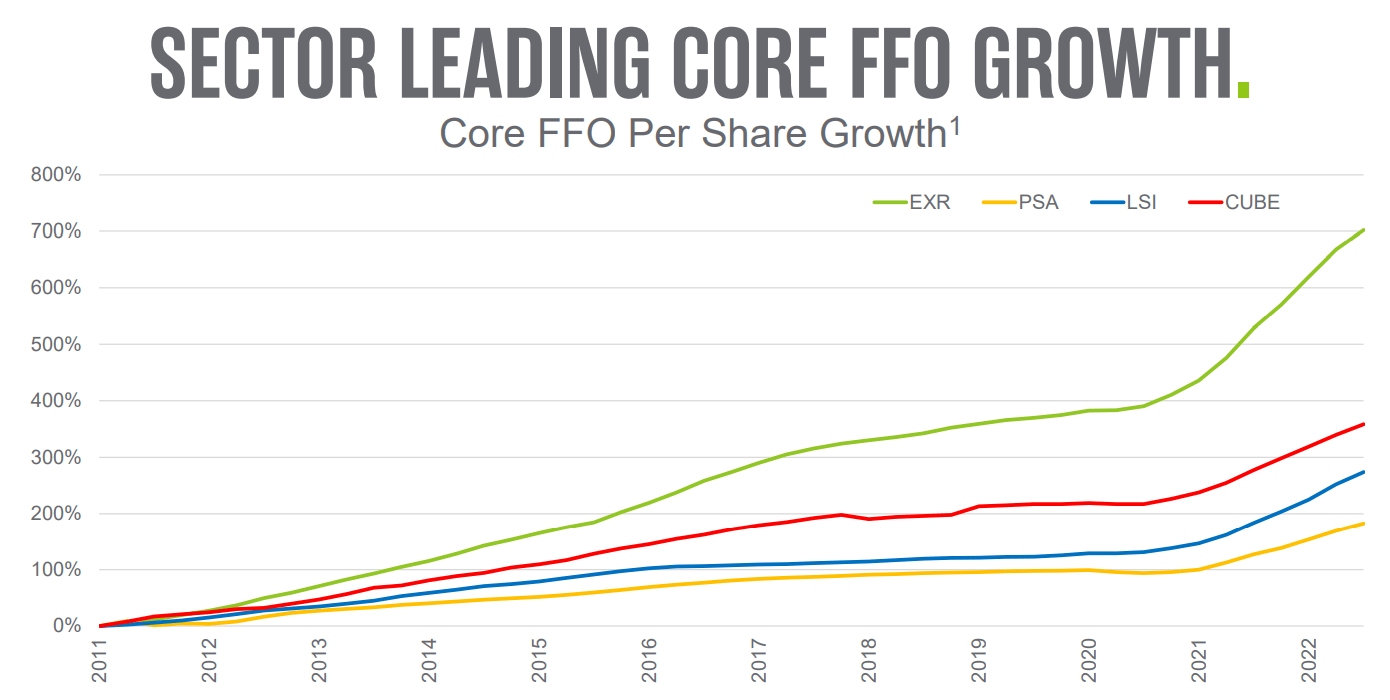

When compared to its peers, EXR’s Core FFO growth has been dominant since 2011 with almost 700% total growth since that time. From the chart below, it looks like FFO growth really accelerated in the years after the pandemic, but even prior to 2020, EXR was growing FFO at a much faster rate than its peers.

EXR Investor Presentation (Jan 2023)

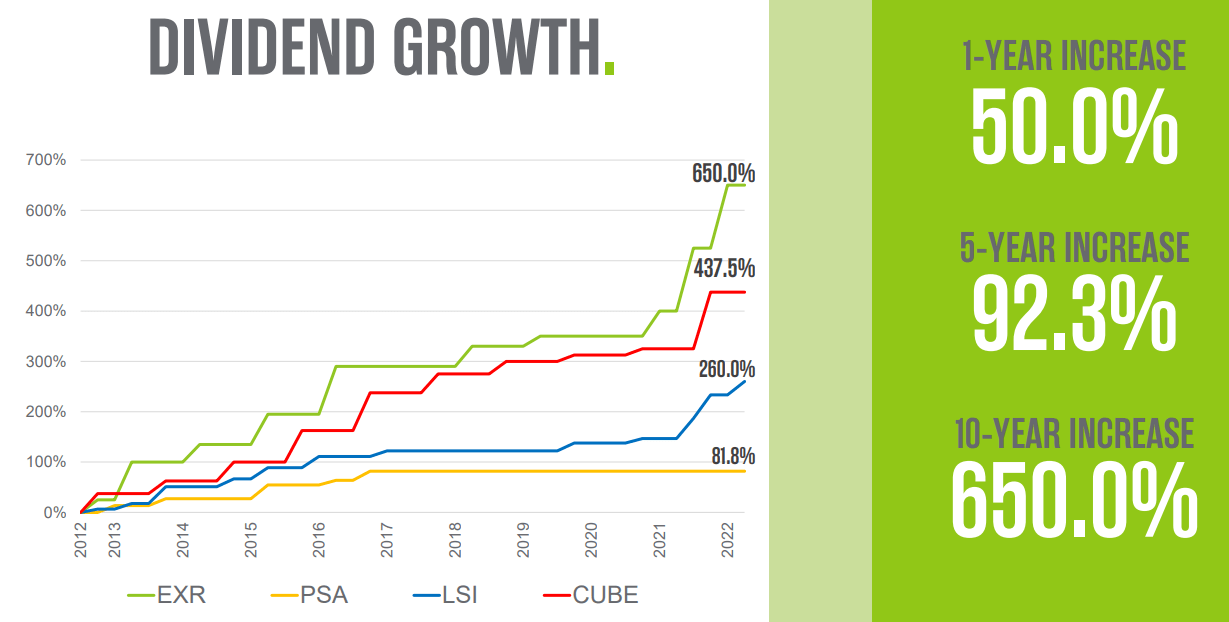

The outstanding growth EXR has exhibited also applies to its dividend. EXR’s dividend growth far exceeds that of its direct peers. Over the last 10 years, EXR has increased its dividend by 650%. For comparison, the largest self-storage REIT, Public Storage (PSA), had a dividend growth rate of 81.8% over the same period.

EXR Investor Presentation (Jan 2023)

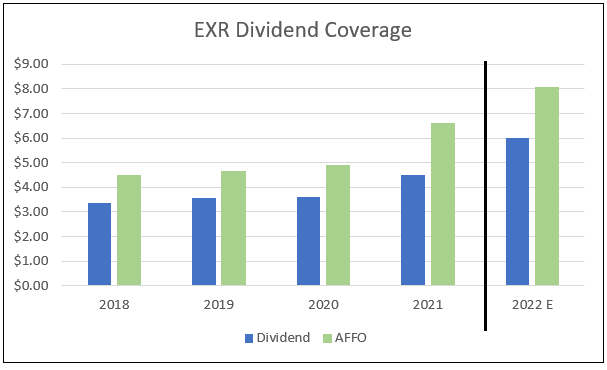

EXR’s dividend is well-covered, with an expected AFFO payout ratio of 74.34% in 2022. It’s impressive that EXR has been able to grow its dividend at such a rapid pace while maintaining a conservative AFFO payout.

FAST Graphs (compiled by iREIT) iREIT

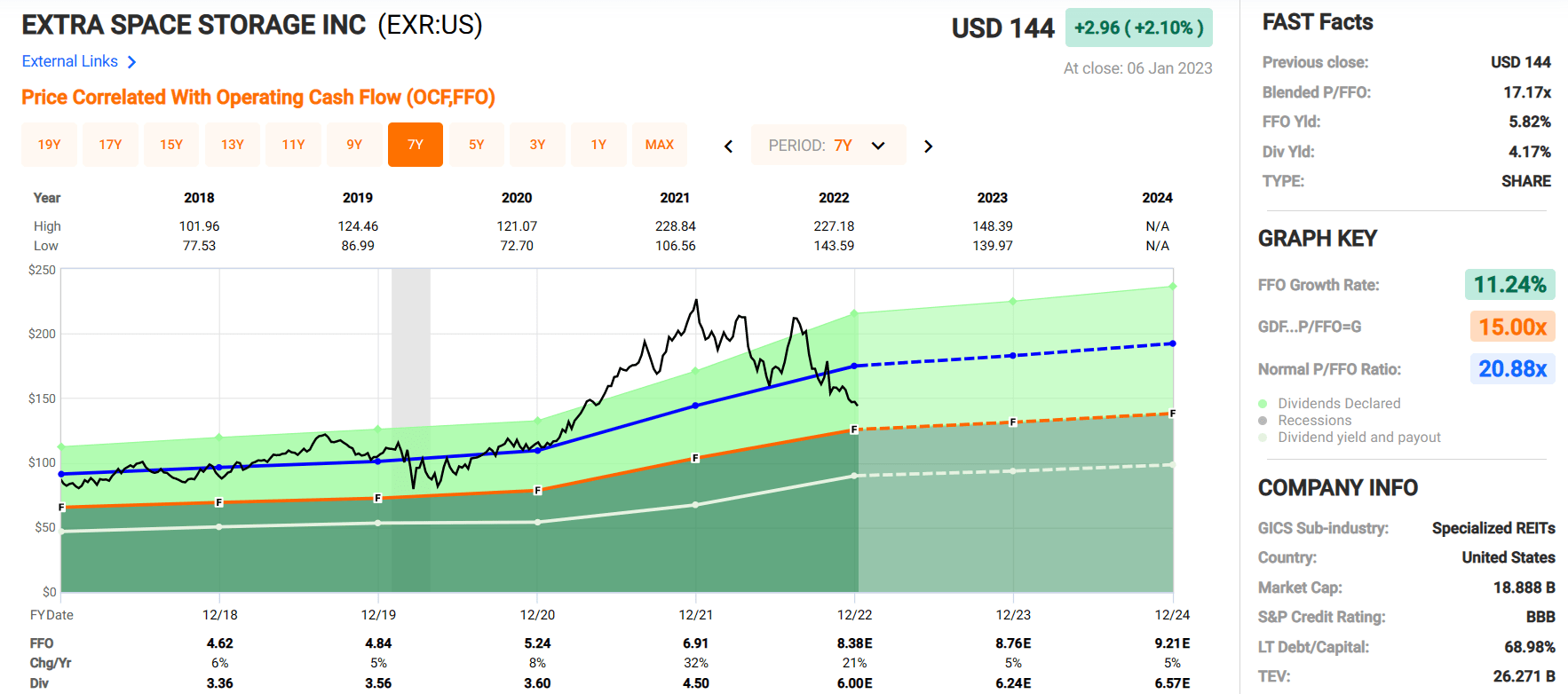

EXR is currently trading at a discounted valuation when compared to its historical average. Currently, EXR trades at a blended P/FFO of 17.17x while its normal P/FFO multiple is 20.88x.

EXR has a dividend yield of 4.17% that is well-covered and has shown very impressive growth rates over the last decade. At iREIT, we rate EXR a STRONG BUY.

FAST Graphs

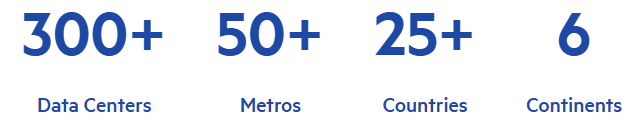

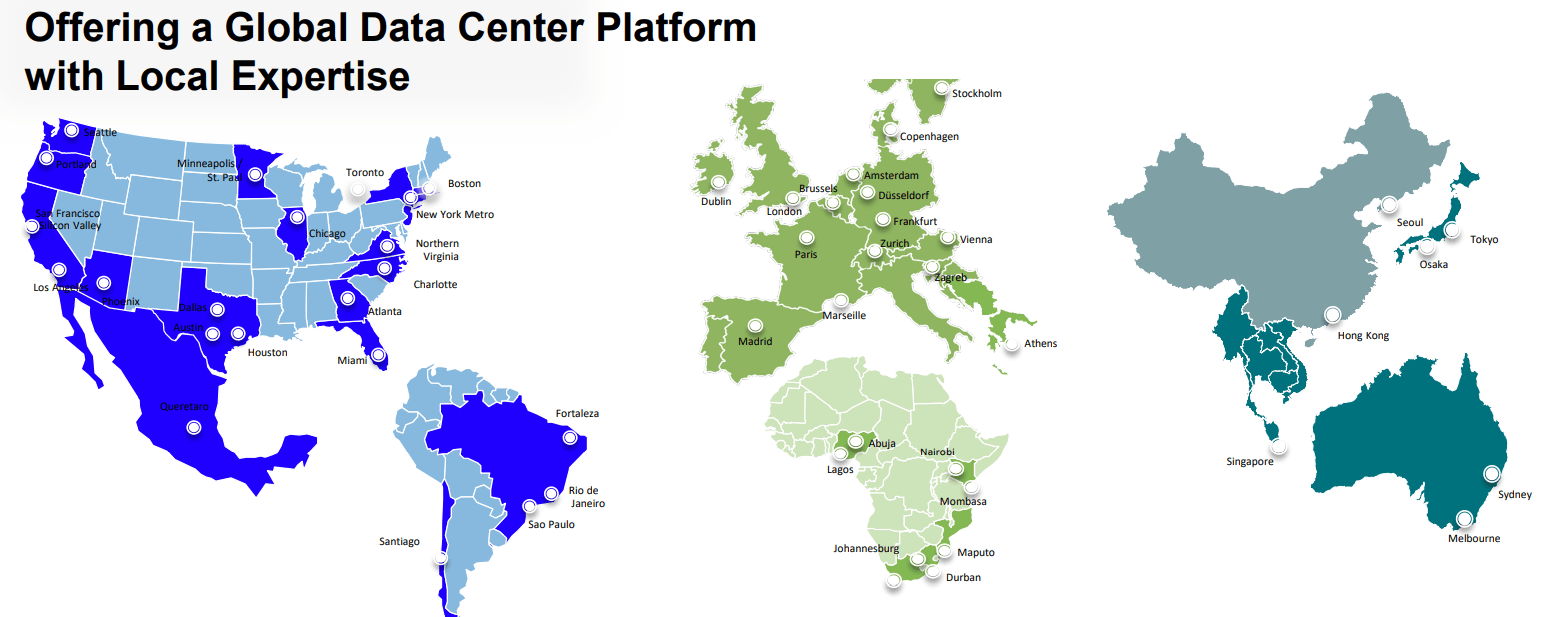

Digital Realty Trust, Inc. (DLR) is a data center REIT that was founded in 2001 and went public in 2004. They own over 300 data centers across more than 25 countries on 6 continents.

I read a comment the other day saying in effect that any building with a wide-open space could house servers and that data centers don’t need specialized layouts or open parking with easy access.

In no way am I trying to be critical or disrespectful about the comment, but I would like to use this as an opportunity to clear some things up.

Data centers are VERY specialized buildings. Servers housed in data centers use a lot of power and produce a lot of heat. Data centers must be designed with an infrastructure that enables them to pull in enormous amounts of electricity.

They often do that with electrical substations that tap into the electrical grid and manage the flow and voltage levels coming into the center. Data centers often have on-site generators and other alternative energy sources that can be utilized if the main grid goes down.

Servers and the information stored on them are critical to companies, so data centers need backup systems in place to mitigate any potential issues.

The servers that require so much power produce a lot of heat, so data centers must be designed with cooling systems to help monitor and manage temperature and humidity levels to keep the IT equipment working at optimum levels.

Then there’s security. Try walking into a data center some time and see how far you get. The sensitive and proprietary information stored in these centers must be protected from unauthorized access and cyber-attacks.

Data centers have multiple layers of security built in, from high security fences and cameras, to guarded main entry points, access badges and iris scans. The list goes on, but suffice it to say you cannot just gain entry unnoticed.

DLR website DLR Investor Presentation (Nov 2022)

In December 2022, DLR terminated its CEO William Stein without cause and appointed Andrew Power as the new CEO. Andrew Power was formerly the CFO for DLR, and prior to joining the company Andrew Power held various investment banking positions, most recently as the managing director of real estate investment banking with Bank of America.

DLR Form 8K

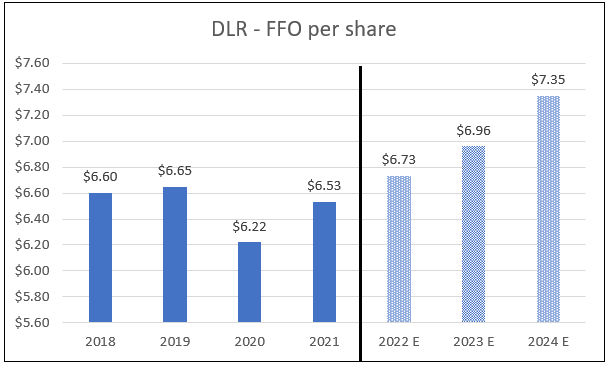

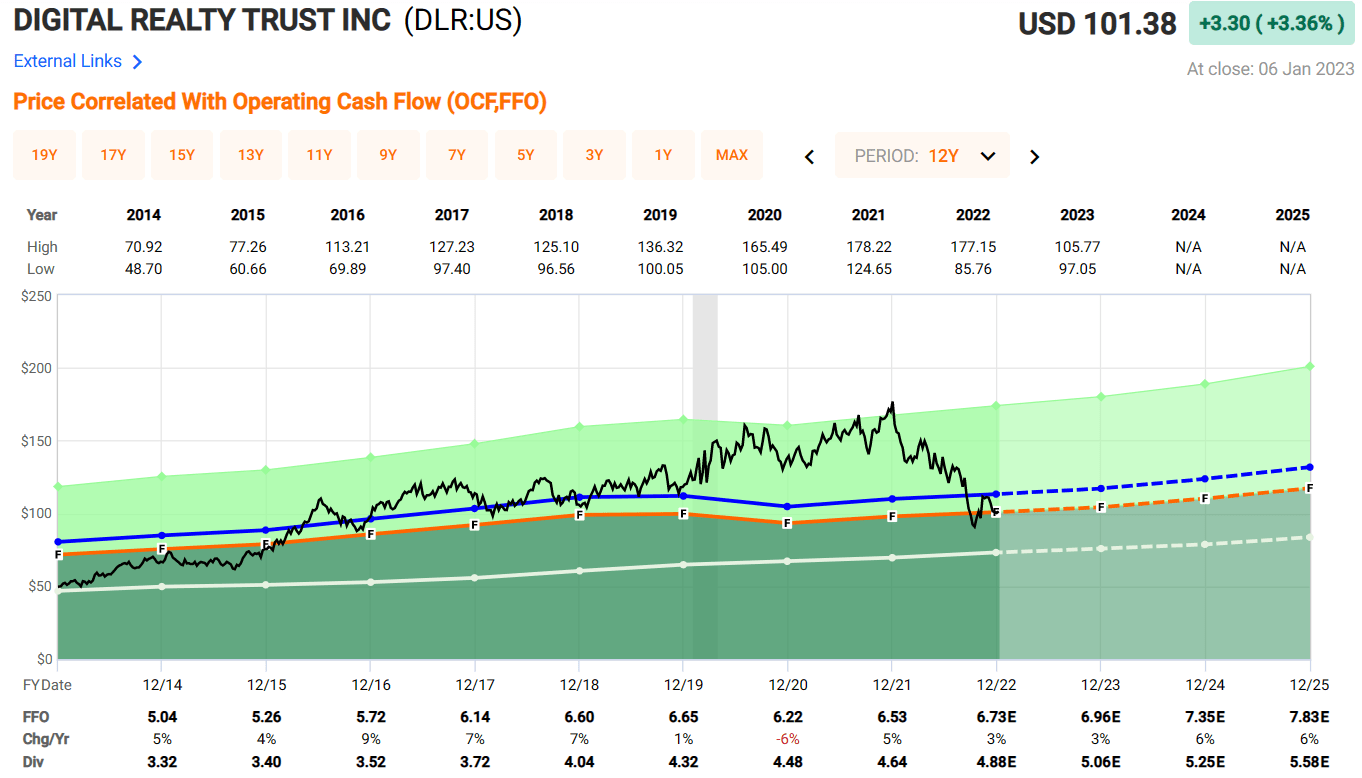

Since 2010, DLR has had an average FFO growth rate of 6.33%. 2020 was the only year since 2010 where DLR did not see some level of FFO growth, when it declined by 6%.

It later rebounded to 5% growth in 2021, and is expected to have a growth rate of 3% in 2022 and 2023. In 2024, analysts project FFO growth of 6%, back in line with its historical average since 2010.

FAST Graphs (compiled by iREIT)

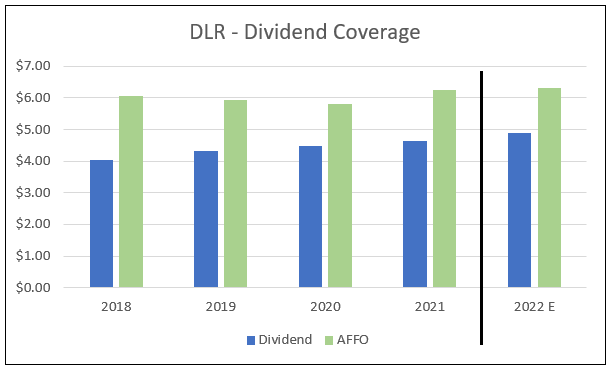

DLR pays a dividend yield of 4.81% that is well-covered with an AFFO payout ratio of 77.46%. DLR has maintained this payout ratio for the last several years and has increased its dividend consecutively for the last 17 years. Over the last 5 years, DLR has averaged an annual dividend growth rate of 4.90%.

FAST Graphs (compiled by iREIT) FAST Graphs (compiled by iREIT)

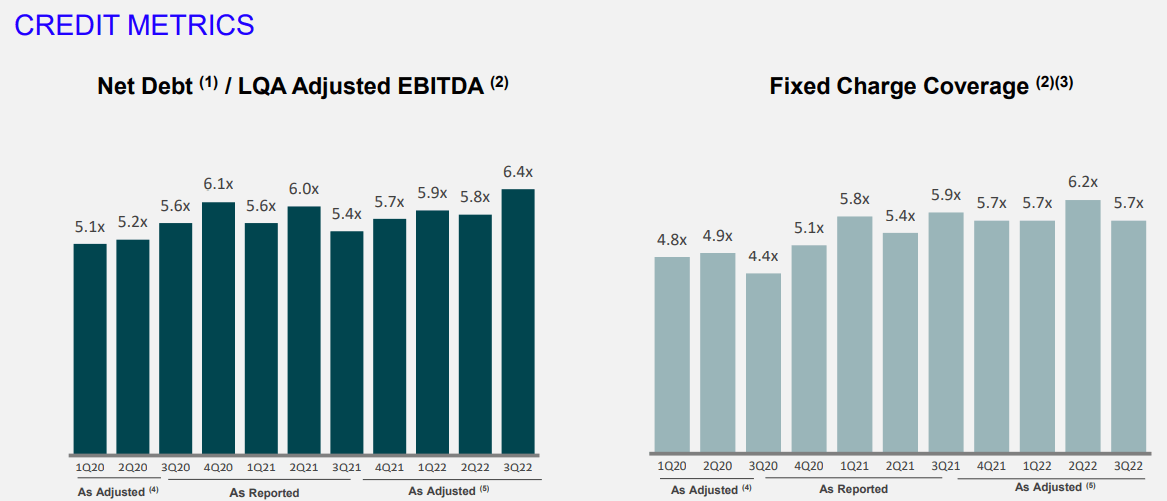

DLR has a sound balance sheet with good debt metrics. Its Net Debt to LQA (latest quarter annualized) Adj. EBITDA is 6.4x and its Fixed Charge Coverage is 5.7x. As of the third quarter of 2022, DLR had $1.5 billion revolver capacity.

DLR Investor Presentation (Nov 2022) DLR Investor Presentation (Nov 2022)

DLR trades at a significant discount to its normal valuation. Currently DLR is trading for a P/FFO multiple of 14.69x, which compares favorably to its normal P/FFO of 19.21x.

Likewise, the stock trades under its Net Asset Value with a P/NAV of 0.75. DLR’s price decline over the last year has presented an attractive entry point, especially considering its FFO and dividend growth prospects. At iREIT, we rate DLR a STRONG BUY.

iREIT FAST Graphs

REITs Are Made For Dummies

I’m very excited to be writing a new book, REITs For Dummies.

As you may know, Dummies books are not actually for dummies; they’re instructional books intended to present non-intimidating guides for readers new to the various topics covered, and of course, my book is on REITs.

With a growing subscriber base of around 15,000 customers (across multiple platforms), I’m really excited about publishing this Dummies book because of the company’s worldwide success with editions in numerous languages.

To put it in simple terms, I plan to write prose for the little guy and gal, that include bold icons and sections called “parts,” which are groups of related chapters. Another common thread for Dummies books is “The Part of Tens,” a section at the end of the book where lists of 10 items are included.

I want to thank Seeking Alpha and my 105,000+ followers for providing me with the platform to engage, learn, and add value. Without you, this book would not be possible.

As always, thank you for reading, and happy SWAN investing!

Be the first to comment