Lya_Cattel

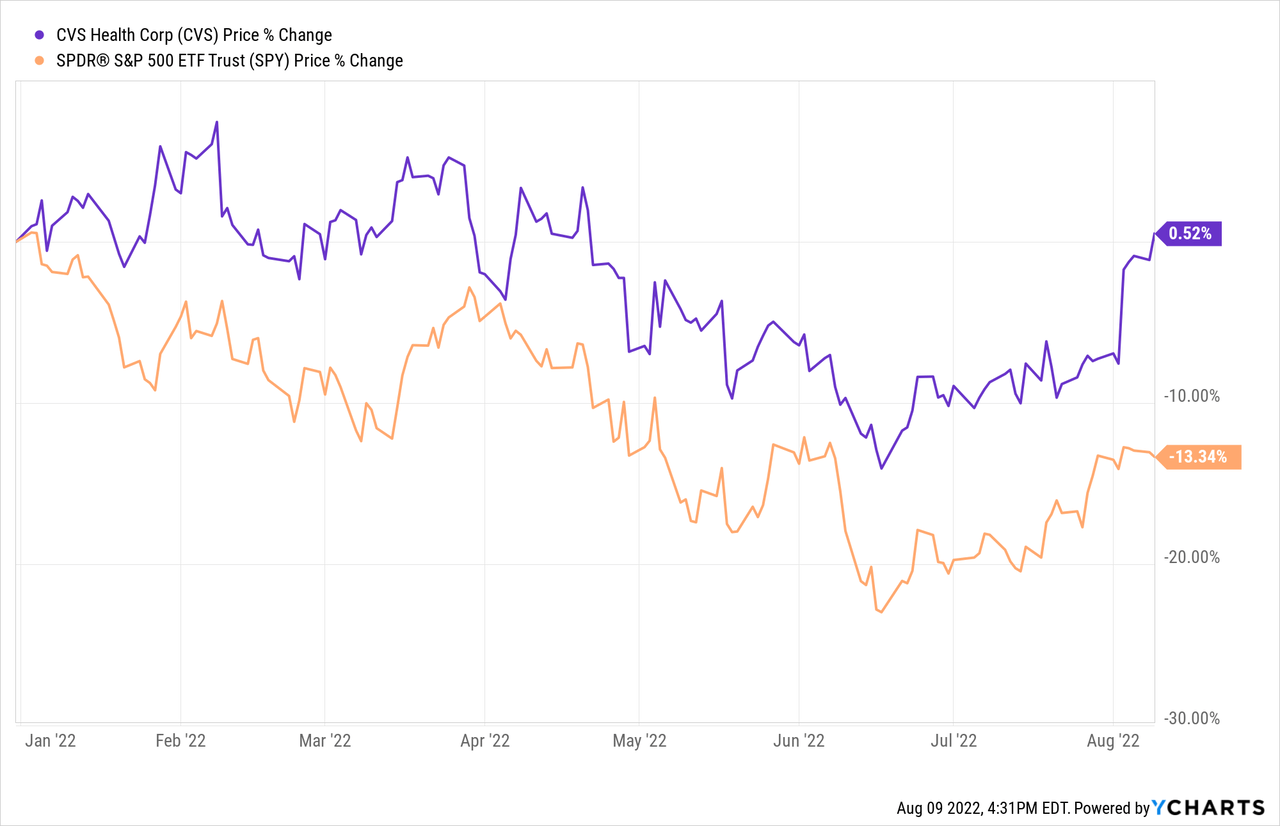

CVS Health’s (NYSE:CVS) share price has remained flat year to date, outperforming the broader market substantially, which has declined by as much 13% in the same period.

In this article, we will present three reasons why we think CVS’s stock could be an attractive investment in the current market environment and why we expect the stock to keep outperforming in the near term.

1.) Increasing revenue

In the second quarter of 2022, revenue has increased by as much as 11% vs. the prior year, reaching $80.6 billion. All three segments of the firm have been contributing to this growth.

- In the health care benefits segment revenue has increased by 10.9%, reflecting growth across all product lines.

- In the Pharmacy service segment revenue grew by 11.7% fueled by increased, pharmacy claims volume, growth in specialty, pharmacy and brand inflation, partially offset by continued client price improvements

- The segment representing the lowest growth was the retail/LTC segment, growing by “only” 6.3% year over year. The primary drivers for this segment were: increased prescription and front store volume, including the sale of COVID-19 OTC test kits, and the impact of an extended cough, cold, and flu season compared to prior year. On the other hand, decreased COVID-19 vaccinations and diagnostic testing were partially offsetting the previously mentioned positive impacts.

We expect CVS to continue doing well and grow in the current market environment. While the pandemic fueled trends may be disappearing, we believe that the demand for the company’s products and services in general is relatively inelastic. Therefore, CVS is not likely to be materially impacted by the low or declining consumer confidence.

Performance during periods of low consumer confidence

Consumer confidence is a leading economic indicator, often used to predict near term changes in the consumer spending behaviour. A low or falling consumer confidence is likely to lead to reduced spending on durable, discretionary, non-essential goods, potentially hurting the financial performance of firms manufacturing and selling such products. But as most products and services sold by CVS are considered essential, we expect consumer sentiment to have little influence on CVS’s performance the near term.

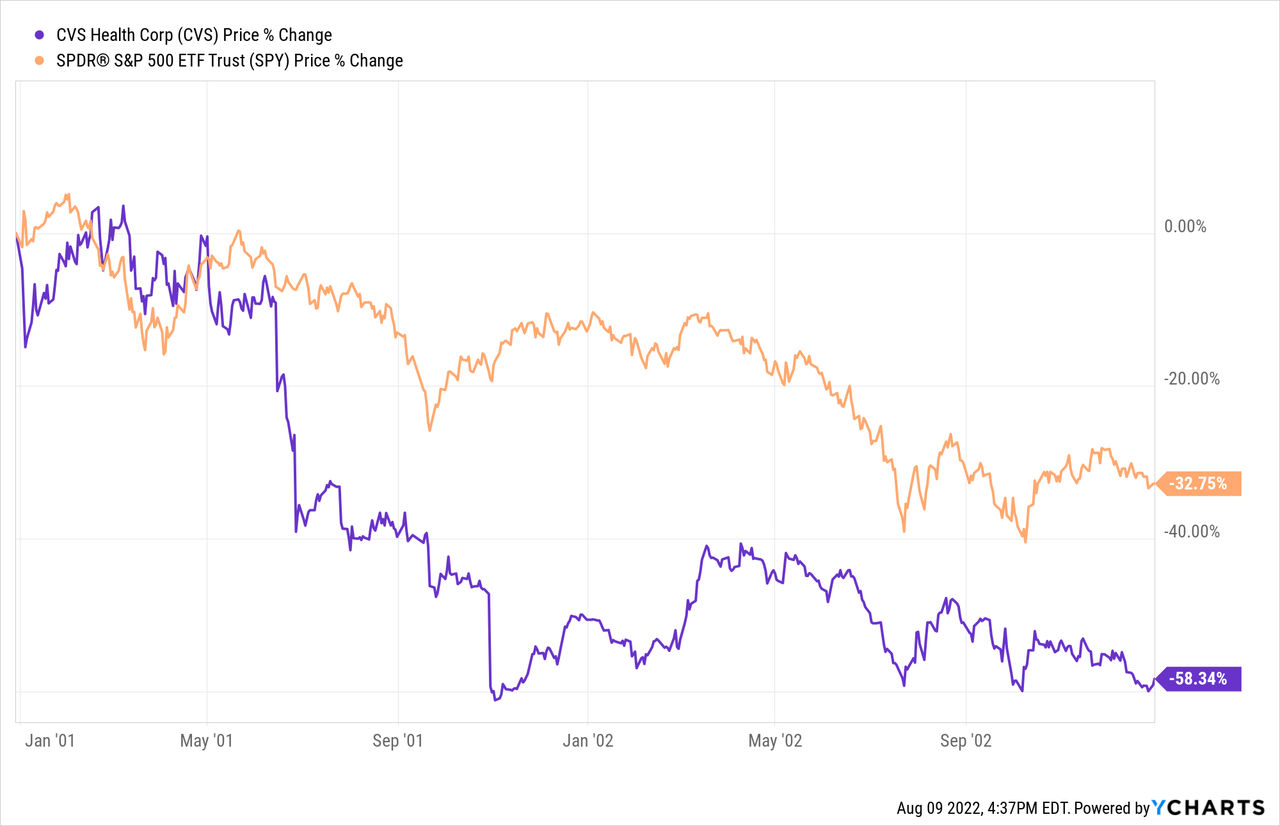

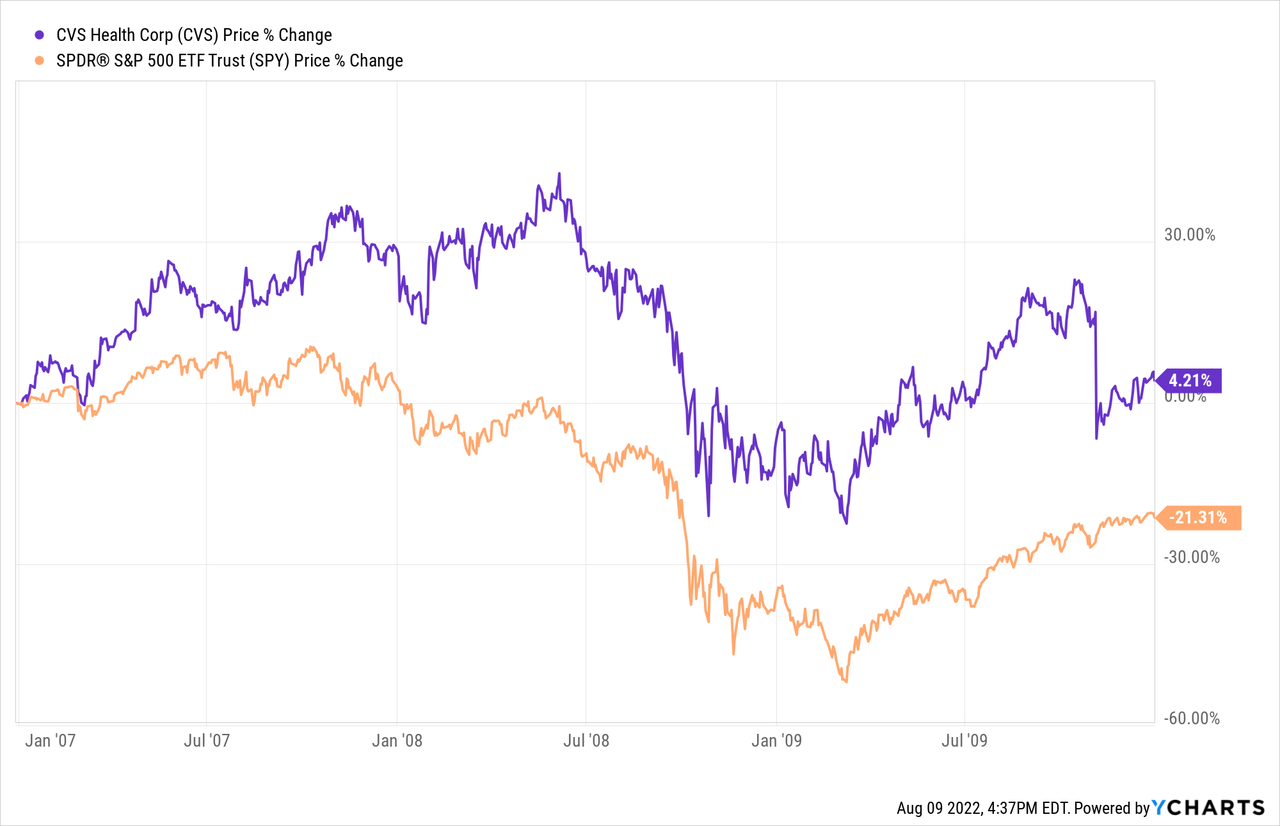

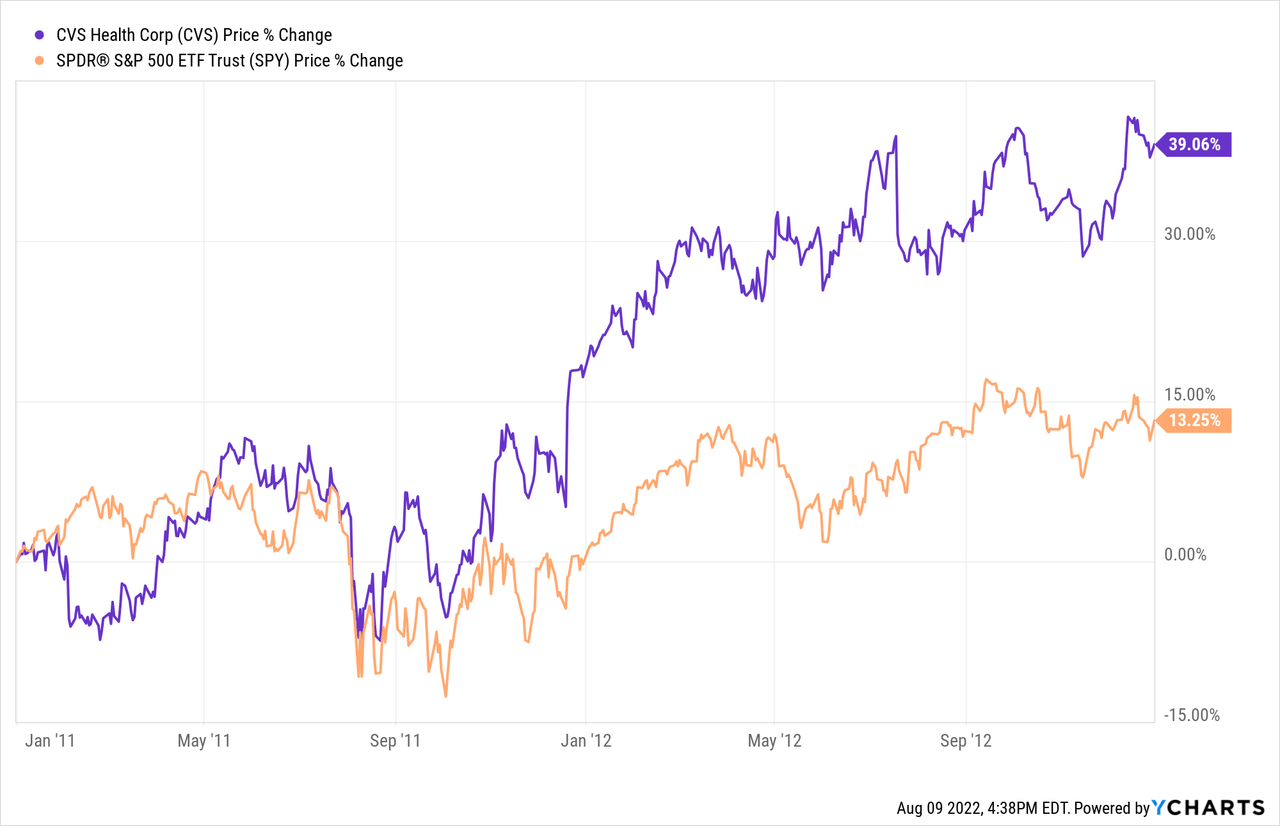

Let us take a look how CVS’s stock price has actually developed during times of low consumer confidence in the last 20 years.

2001-2003

2007-2010

2011-2013

CVS has substantially outperformed the broader market 2 out of 3 times. Although past performance is not always useful for forecasting purposes, we believe that CVS is well-situated in the current market environment to perform well.

We believe that the performance from the period of 2001-2003 is not necessarily representative, because CVS business was going through a much more difficult times than currently, including a more than 16% decline in sales and an announcement of more than 200 store closures.

Not only us, but the management also appears to be optimistic about the rest of 2022. And this takes us to the second reasons why we like CVS.

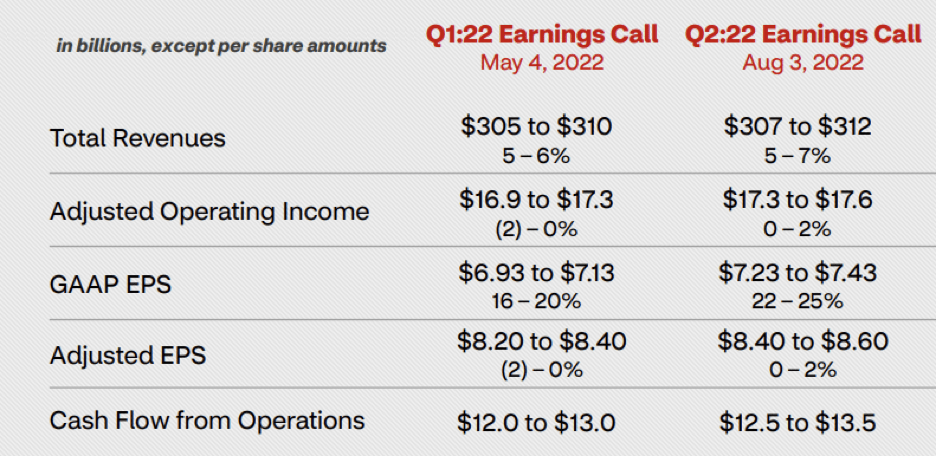

2. Improved guidance

The firm has presented a favourably updated guidance for the rest of the year on their earnings call in August.

Guidance (CVS)

Across all metrics, now CVS is expected to grow more than previously anticipated. Important to point out that, while according to the previous guidance adjusted operating income and adjusted EPS were forecasted to decline or remain flat, now even an increase appears to be possible.

The largest driver of the positive change was the increase in adjusted operating income in the retail/LTC segment and it already reflects updated COVID-19 assumptions and higher levels of investment spending in the back half of the year. The health care benefits segment guidance remained unchanged, while in the pharmacy services segment on the total pharmacy claims processed have been updated.

Also, as CVS mainly operates in the United States and North America, their financial performance, due to currency exchange risks and the strong USD, is not likely to be impacted directly.

All in all, we believe that the updated guidance is a positive sign and implies that the firm is confident in the continued strong demand for their products and services for the rest of the year.

In our opinion, the results of the second quarter and the guidance provided, further consolidate CVS as a market leader in the U.S. prescription drugs market.

Market share as of 2021 (statista.com)

And now coming to our last point: dividends.

3. Dividends

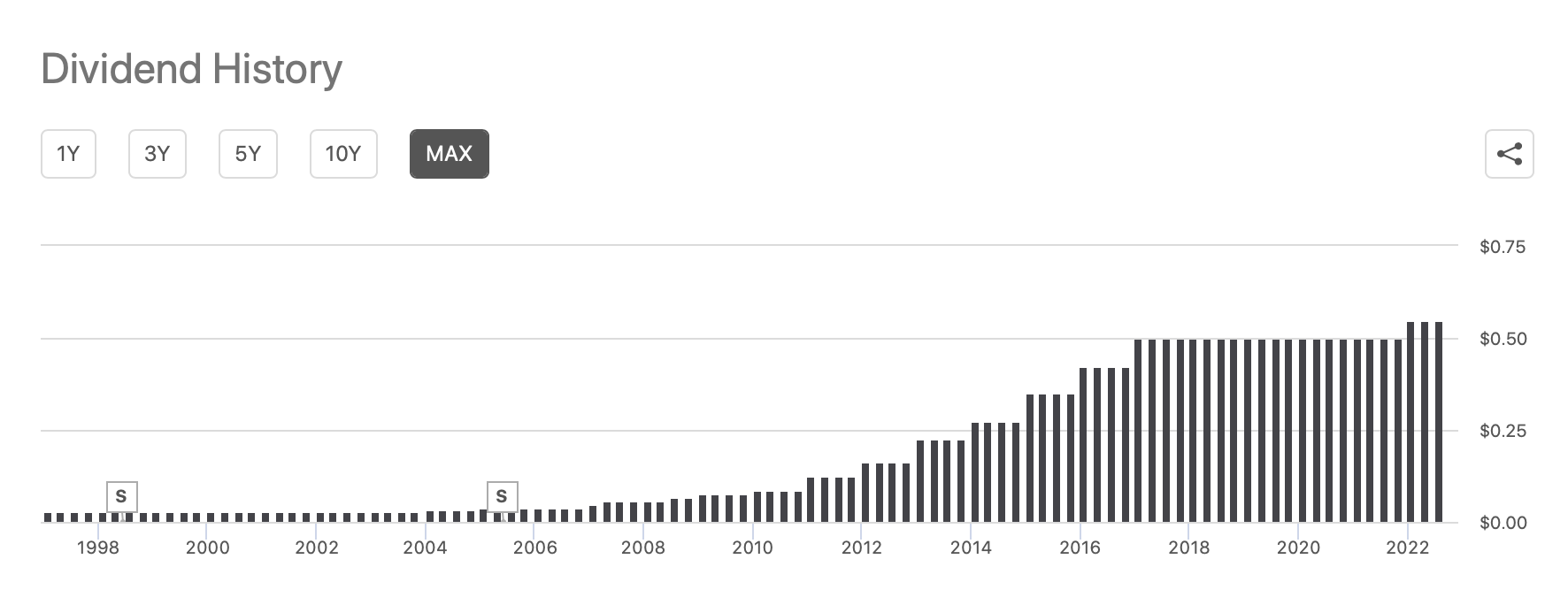

CVS has been a popular choice among investors looking for safety and dividends. The firm has been paying quarterly dividends to its shareholders since 1997, creating significant returns additionally to the realized capital gains. The company’s current quarterly dividend is $0.55 per share, corresponding to a yield of about 2.2%, annually.

Dividend history (seekingalpha.com)

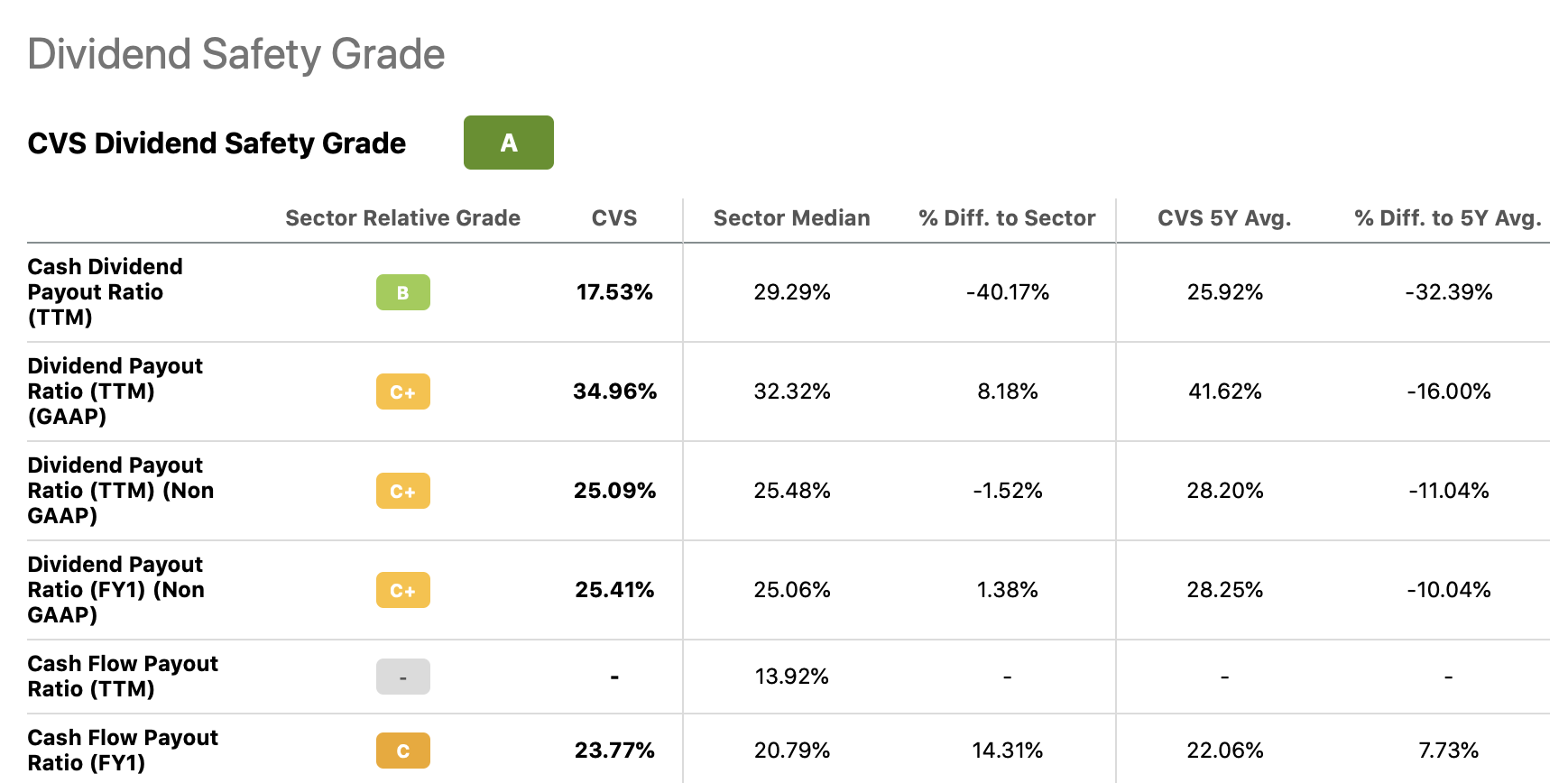

Also important to note that the current payout appears to be safe and sustainable in the near term. The following table summarizes the key dividend payout ratios.

Dividend safety (seekingalpha.com)

CVS’s Dividend Payout Ratio (TTM) (GAAP) is 35% – about in line with the sector median – and about 16% below its own 5-year average.

For these reasons, we believe that CVS could be an attractive addition to dividend portfolios.

Before concluding, let us take a brief look at the valuation of the firm.

Valuation

CVS’s stock is trading at a significant discount compared to its respective sector median according to all of the traditional price multiples.

Valuation (seekingalpha.com)

Considering that analysts are forecasting both revenue and EPS to increase in the years to come and a strong track record of recent upward revisions, we believe that CVS could be relatively safe choice at these valuations.

Key takeaways

The demand for CVS’s products and services has remained high, despite the diminishing impacts of COVID-19 induced trends.

In contrast to many firms, especially to retailers that have been struggling with inventory management and a declining demand, partially driven by a historically low consumer confidence, CVS appears to be an attractive investment option in the current market environment. The favourably updated guidance further strengthens this thesis.

The safe and sustainable dividend could make the firm appealing for dividend and dividend growth investors.

Be the first to comment