Petrovich9/iStock via Getty Images

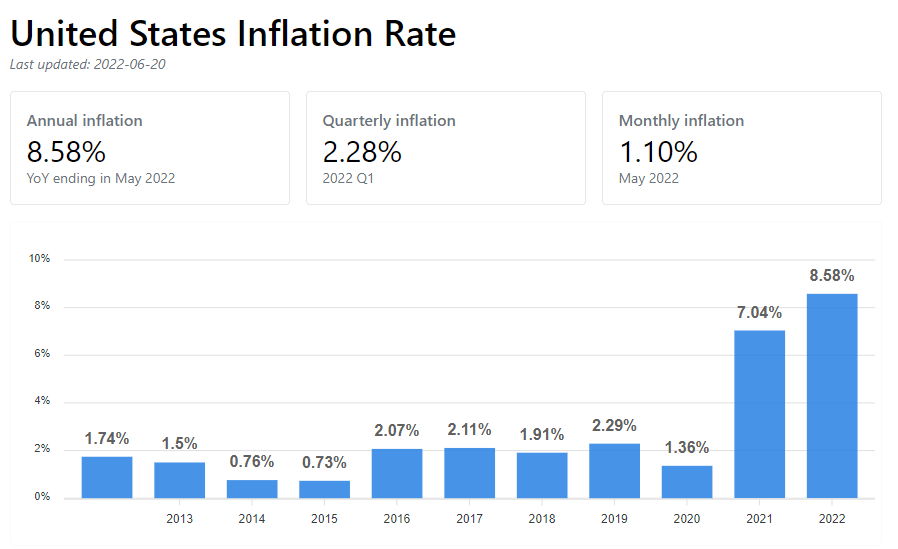

This is the worst inflation since 1981 and worse more, it hasn’t peaked.

Thus, our take on what comes next and how you should prepare for it.

The situation will likely worsen until September, October, or possibly December.

Source: inflationtool.com

Our crystal ball suggests that there will be a few more months of painful increases to the inflation rate, which we think will top out around 9% by late summer… And after that…

Inflation will likely stay doggedly high even after it peaks, ending the year around 8%, unless a recession hits and cuts back demand.

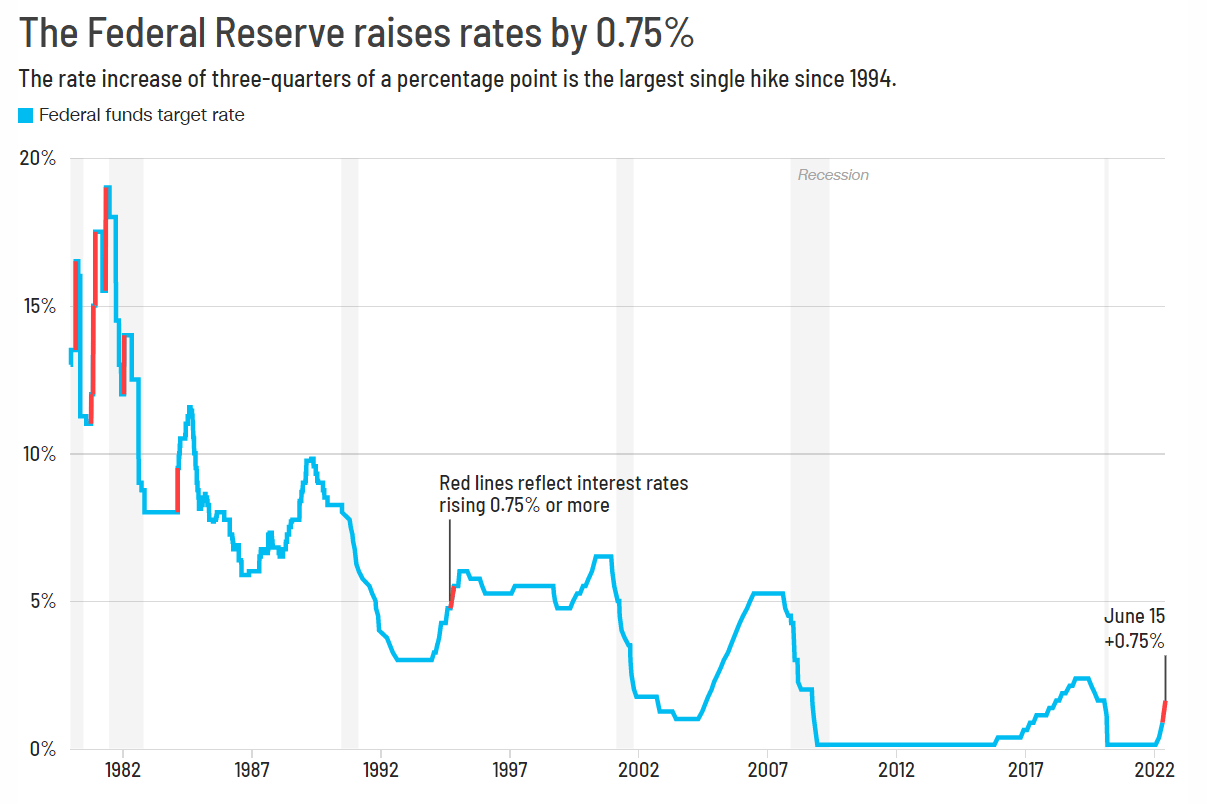

Hence the Federal Reserves’ determination to bring inflation down, as shown by its decision to raise its benchmark short-term interest rate by three-quarters of a point this week (on June 16th). The Fed hasn’t hiked that much at one time since 1994.

Source: CNN

More huge interest rate hikes are coming. The Fed has no alternative.

It’s becoming increasingly clear that The Fed must break the cycle, even if rapid tightening risks causing a recession. We believe the Fed will boost its rate by another 2% points this year.

Expect continued volatility and stocks may be headed even lower, but some good values are starting to emerge, amid the chaos.

Why Net Lease?

A few days ago I wrote a detailed article on Net Lease cost of capital in which I explained,

“Most realize that net lease properties offer investors highly defensive income in which the performance is highly predictable. These assets provide high income and require little to no management.

The cash flow is dependable because the leases are structured in a manner that reduces risk of lease-up. The transaction volume in the net lease sector is exceptionally strong, largely due to the continued demand from 1031 investors as well as the growing acceptance within the net lease REIT sector.”

I went on to explain,

“…there’s actually a benefit worth pointing out, with regard to net lease REITs in that the tenant pays for all of the expenses.

Unlike a self-storage owner or hotel landlord who must adjust their rental rates due to rising inflation, the net lease landlord does not have to worry about any of the 3 T’s (toilets, trash, or taxes). And that’s what makes them seem like bonds…”

Think about like this…

Many net lease tenants, such as Walgreen’s (WBA), Advance Auto Parts (AAP), and 7-Eleven have to increase their costs due to inflation, yet investing in triple net leases can be profitable and worry-free.

NNN properties are tenanted by essential businesses that tend to do well in tough times, so they can actually become more valuable during inflation. These triple net properties are responsibility-free, expense-free investments that produce a guaranteed monthly income that does not fluctuate.

In fact, most triple net leases include periodic rent increases to account for possible inflation. Importantly, the physical underlying real estate value also adds a layer of security and stability to the investment.

I know that in many of my net lease articles I reference the popular names such as Realty Income (O), VICI Properties (VICI), Agree Realty (ADC), and W.P. Carey (WPC) – and admittedly I do tout them a lot because I own them all. In fact, our Durable Income Portfolio consist of over 22% in net lease, which significant concentration associated with:

- Realty Income: 5.3%

- VICI Properties: 4.1%

- Agree Realty: 3.1%

- W.P. Carey: 2.5%

However, today I want to take a closer look at a few Net Lease REITs that are flying under the radar and never get much attention.

Getty-Up

Getty Realty (GTY) is a net lease REIT that owns 1,014 properties across 38 states and Washington D.C. And a clear majority – 70% – of them are located on street corners where car traffic is both convenient and high. In addition, GTY’s portfolio is 99.4% occupied with a WALT (weighted average lease term) of 8.7 years.

GTY focuses on essential, e-commerce and recession resistant, retail businesses, and year-to-date the company has invested $52.8 million across 17 properties (through April 27, 2022) by acquiring 10 car washes (for $42.0 million), 3 convenience stores (for $8.1 million) and funded development of $2.7 million.

GTY’s portfolio is largely concentrated in the northeast, however the company has been expanding its operations in growth markets in the Mid-Atlantic, South East, Texas, and Colorado.

Convenience & automotive retailers are essential businesses, and e-commerce & recession resistant, and that’s why GTY and other net lease REITs like Realty Income and Agree Realty continue to invest in these properties.

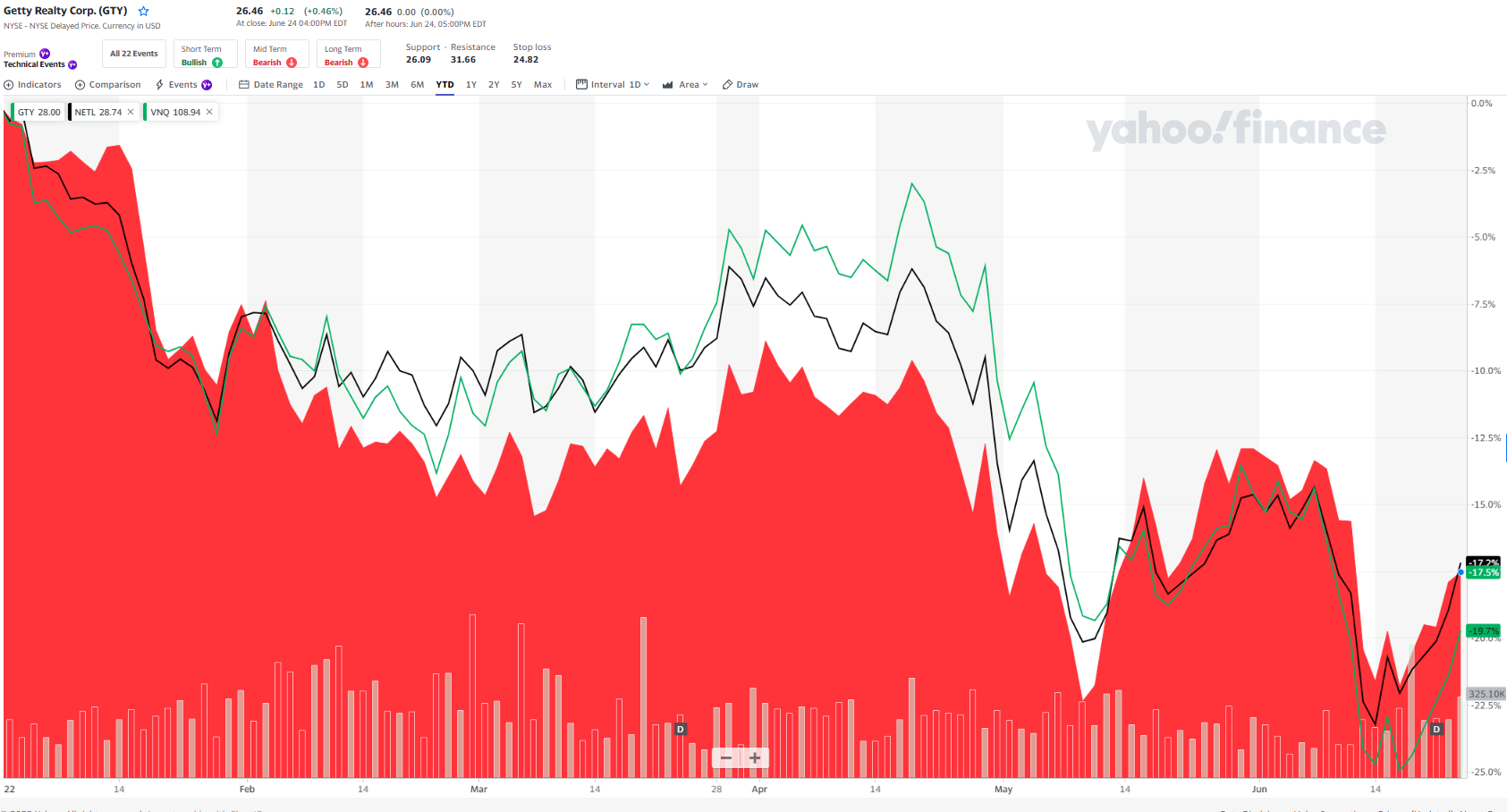

As viewed below, GTY has performed in-line with net lease REITs – used (NETL) ETF as benchmark – and outperformed the broader basket REIT ETF basket known as (VNQ).

Yahoo Finance

As referenced earlier, GTY’s leases are “NNN” and 99% of the leases are subject to rent escalation, average of 1.7% annualized rent escalation rate. Also, GTY has solid rent coverage, 4.0 fixed charge coverage.

Due to GTY’s fairly unique concentration in the gas station space, it offers REIT investors upside potential that’s indirectly related to the rise in energy prices.

Higher fuel prices should help bolster its tenants’ cash flows and balance sheets. And sales inside of convenience/gas stations are increasing at a fairly reliable pace. Obviously, that translates well into their landlords’ rent collections.

A relatively small portion of Getty’s portfolio is made up of auto repair/service, auto parts retailers, and car washes. But they’re still worth mentioning.

The industry metrics related to the automotive space point to near-term cyclical tailwinds boosting results. You can thank the rising age of the average U.S. vehicle for that.

GTY is rated BBB- with a stable outlook from Fitch. The REIT ended Q1-22 with $625 million of total debt outstanding, which consisted entirely of fixed-rate senior unsecured notes with a weighted average interest rate of 4.1% and a weighted average maturity of 6.9 years. There were no amounts drawn on the $300 million revolving credit facility.

Also, at the end of Q1-22 net debt to EBITDA was 4.6x, and total debt to total capitalization was 32%, while total indebtedness to total asset value was 35%. With low leverage, cash on the balance sheet and undrawn revolver, the balance sheet and overall credit profile are in great shape to fund the company’s growth.

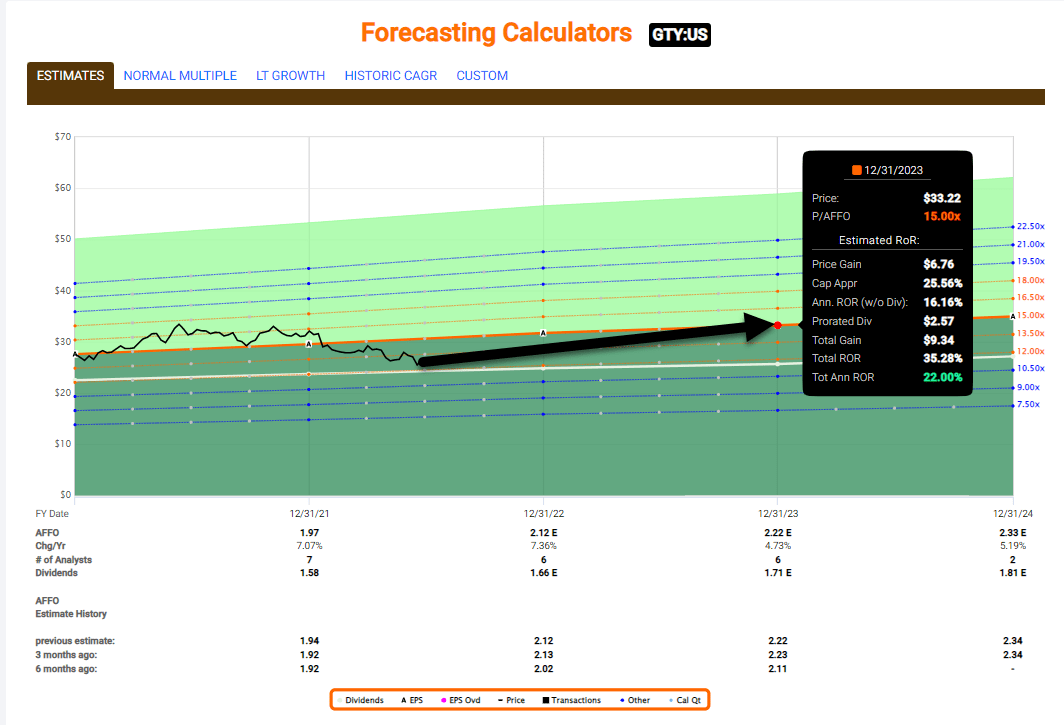

In Q1-22 GTY generated AFFO per share of $0.52, representing a year-over-year increase of 6.1% versus the $0.49 per share reported in Q1-22. As a result of investment activity GTY raised its 2022 AFFO per share guidance to $2.10 to $2.12 per share (from its original guidance of $2.08 to $2.10 per share).

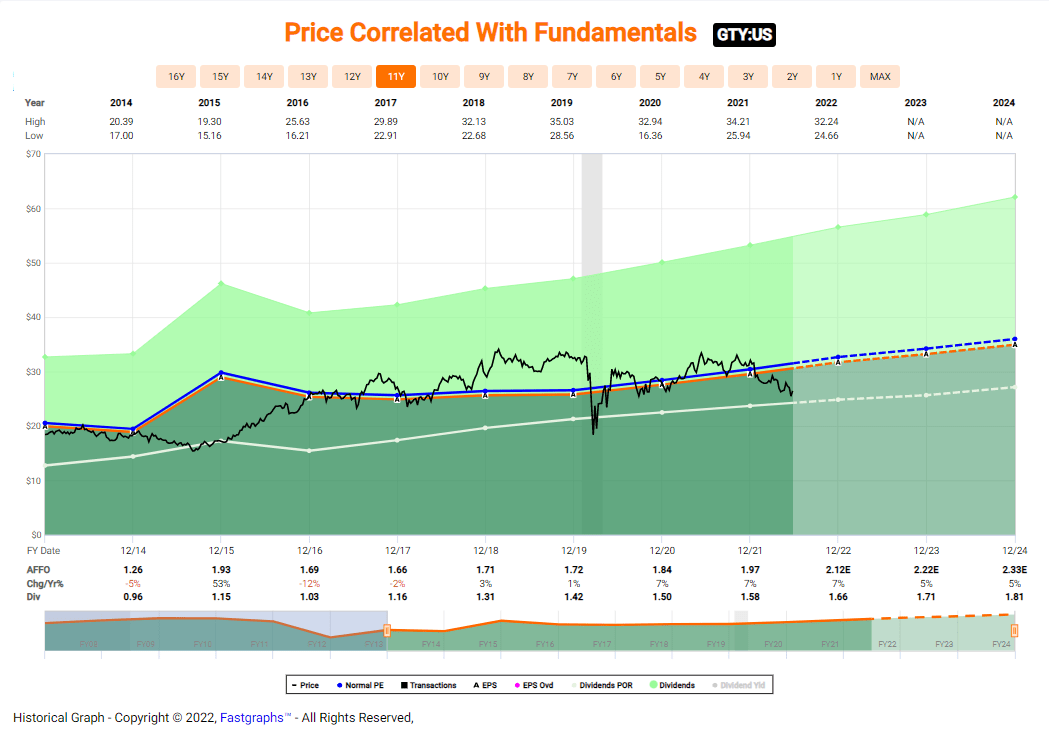

FAST Graphs

As viewed above, GTY does not have a flawless dividend record, as it cut (the dividend by ~10% in 2016, however it has since grown it by an average of 8.3% since 2017. Analysts estimate AFFO per share to grow by 7% in 2022 and 5% on 2023.

Shares are now trading at $26.46 with a P/AFFO of 12.9x (lowest in the peer group), compared to GTY’s average multiple of 15.5x. The dividend yield is an attractive 6.2%, and well-covered by AFFO (78% payout ratio).

The next time I’m filling up my wife’s car ($100…ouch) I will remember that GTY is a perfect stock in the portfolio that offers upside – iREIT targets shares to return ~20% over the next 12 months.

FAST Graphs

An Essential REIT

Essential Properties Realty (EPRT) is a net lease REIT that owns 1,451 properties in 46 states and was 99.9% leased (100% occupied) with a remaining average lease term of 14.0 years.

One of the differentiators for EPRT is that the company buys smaller properties, averaging around $2.3 million in size (similar to GTY), and this means that the underlying real estate (‘LAND’) is usually well-located. The company believes that its middle market focus provides the best risk-adjusted

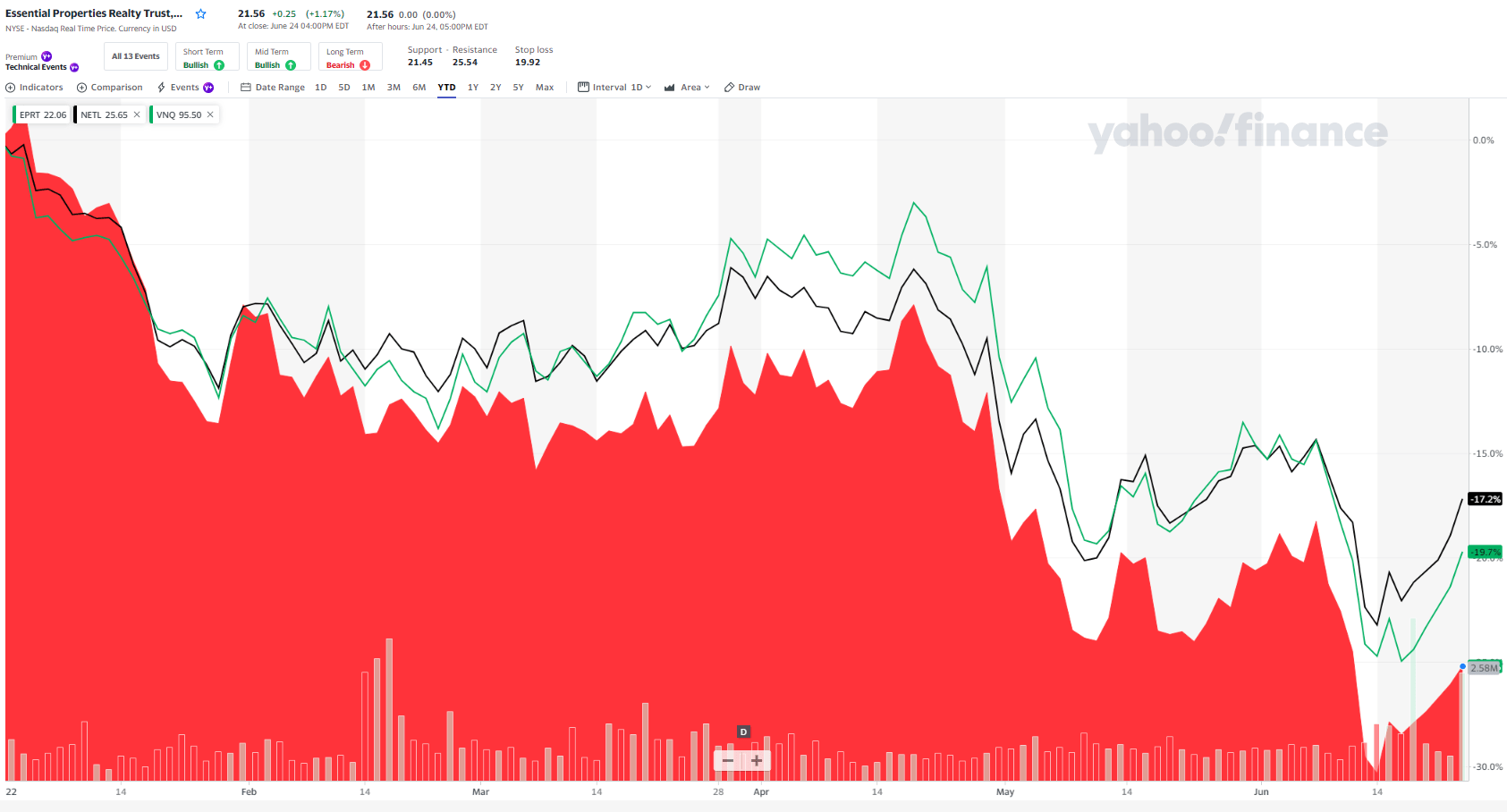

EPRT’s premium suffered a major setback during 2020, largely because of the company’s exposure to early childhood education; however the experientially-driven portfolio is back online and performing well. As viewed below, EPRT has under-performed both NETL and VNQ year-to-date:

Yahoo Finance

EPRT’s experienced Senior Management Team has an extensive track record of growing and managing public Net Lease businesses to significant scale.

The top two executives (CEO Pete Mavoides and COO Gregg Seibert) have over 46 years of collective experience investing in and managing single-tenant net lease properties; and when you include the four senior VPs, the collective net lease experience expands to over 60 years.

In addition, EPRT is more established that many peers in that it has the most comprehensive financial disclosure in the sector, and also has long-standing relationships with institutional investors.

In case you forgot, Mavoides’ (the CEO) tenure as COO of Spirit Realty (SRC) achieved an 88.1% total return, which handily outperformed the 52.4% total return of the S&P 500, the 37.2% total return of the RMS, and the 31.0% total return of the peer group.

Similar to STORE Capital (STOR), EPRT obtains unit-level reporting for most tenants (98.5%) that provides the company with real-time visibility of the business. Also, EPRT’s lease escalations average 1.5% annually and the weighted average lease term of 13.9 is the longest (duration) in the peer group.

EPRT’s balance sheet remains strong with net debt to analyze adjusted EBITDAre at 4.6x and total liquidity of $467 million. The asset base is 100% unencumbered with no secured debt and no debt maturities until 2024.

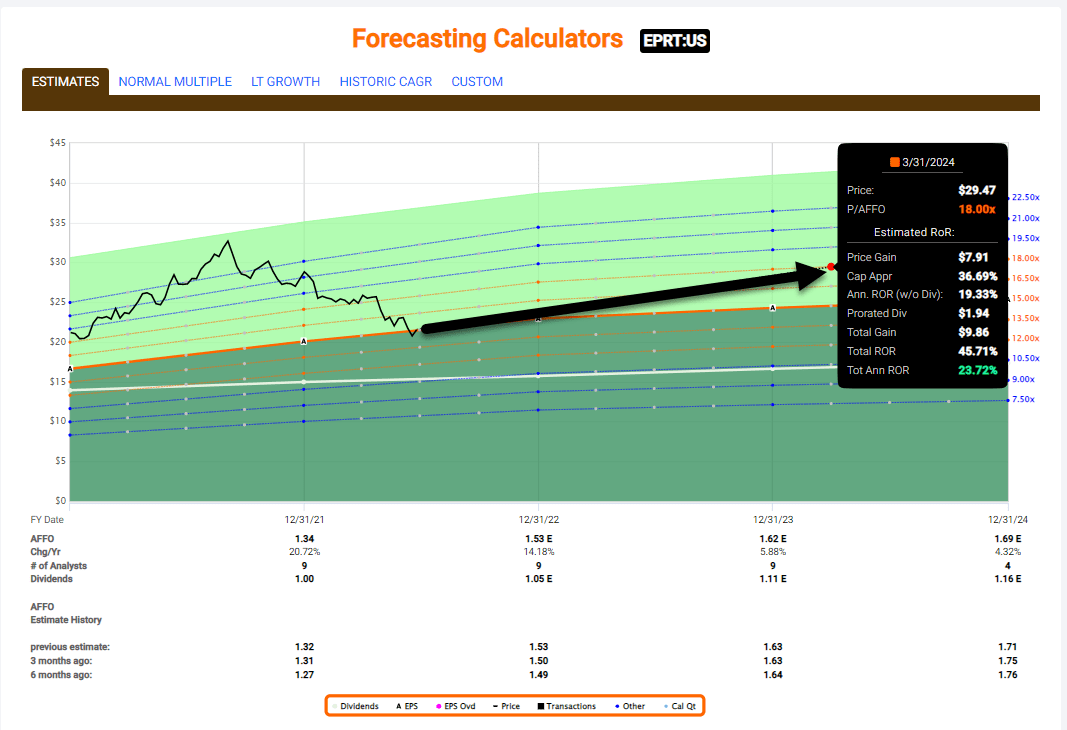

In Q1-22 EPRT generated AFFO of $48.9 million, up $16.5 million over the same period in 2021, which on a fully diluted per share basis was $0.38, an increase of 27% versus Q1-21. EPRT also increased its 2022 AFFO per share guidance range to $1.50 to $1.53, which implies a 13% year-over-year growth at the midpoint.

FAST Graphs

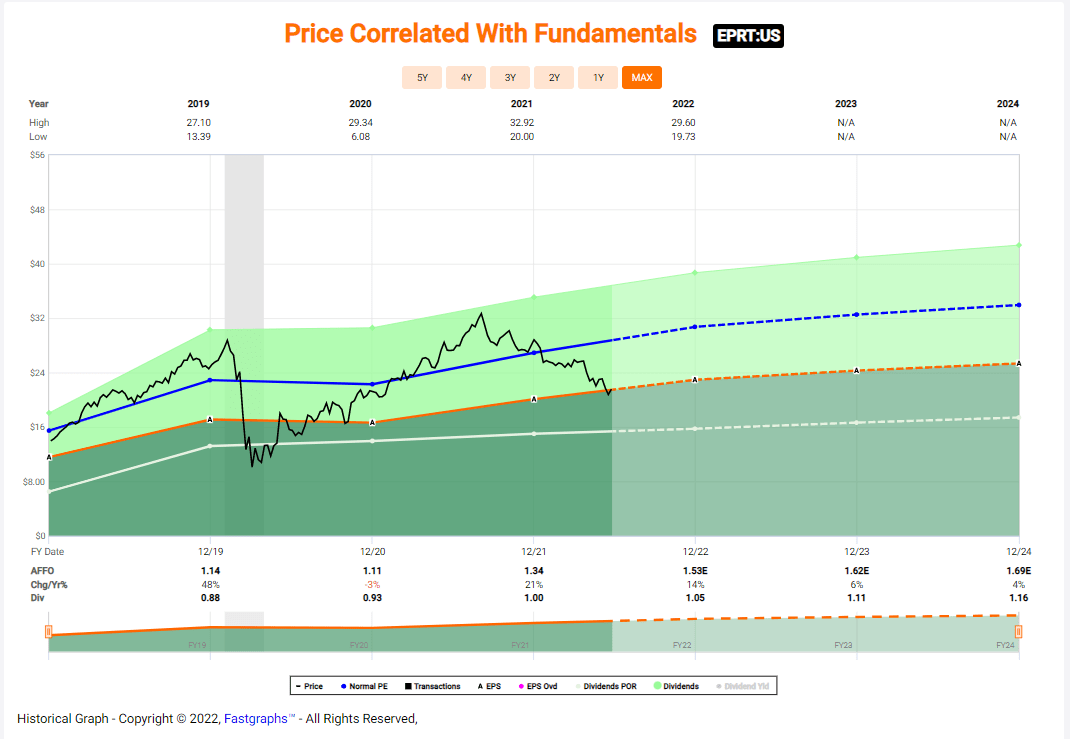

Although just a few years of history, you can see above that EPRT has generated consistent dividend growth (averaging 6% per year), with analysts forecasting AFFO growth of 14% in 2022 and 6% in 2023.

Shares are now trading at $21.56 with a P/AFFO of 15.1x (average is 20.1x) with a well-covered dividend yield of 5.0% (68% payout ratio). We like the opportunity set with EPRT and we maintain a Buy with a 12-mmonth total return estimate of 22%.

FAST Graphs

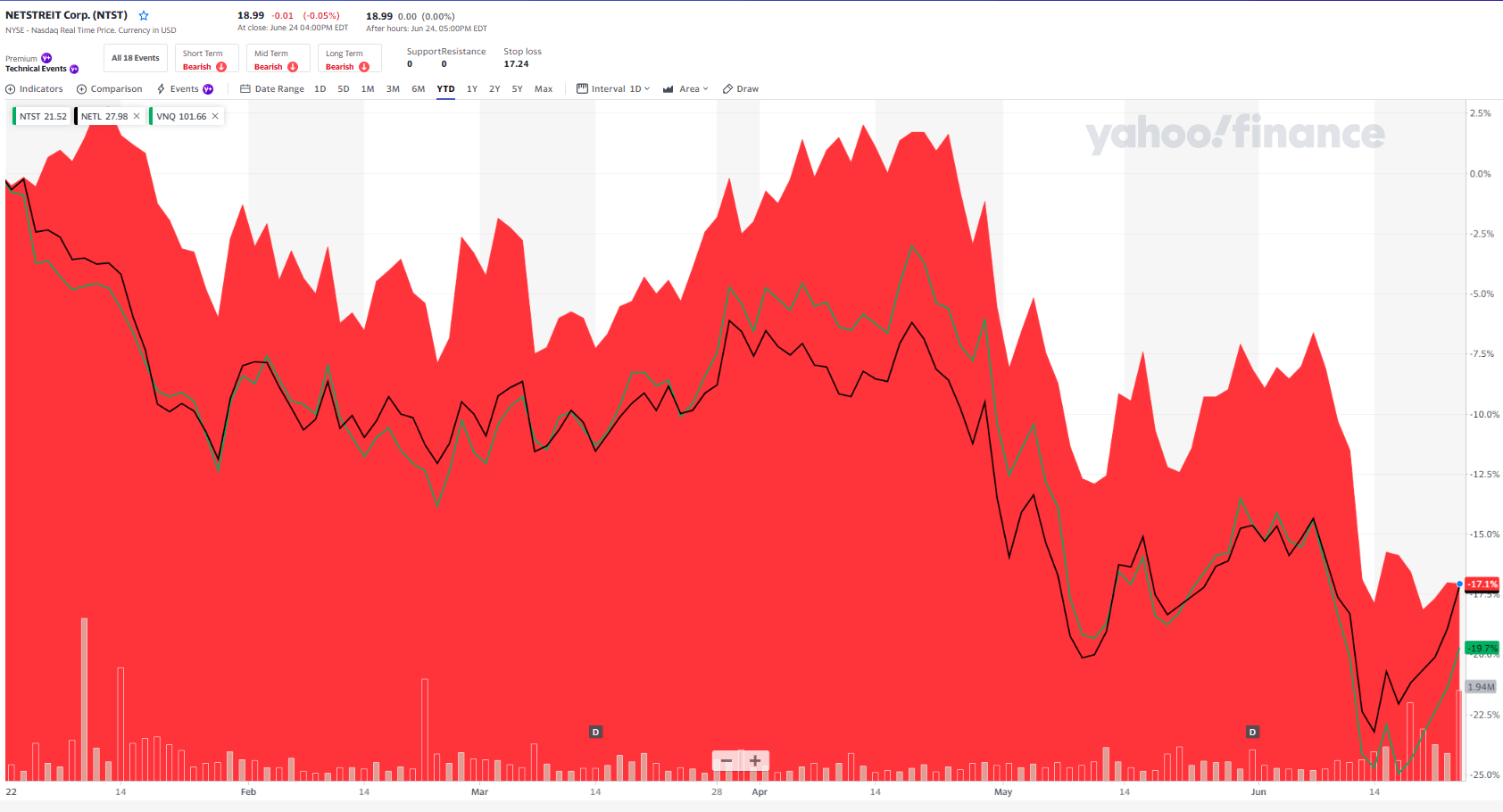

Nothing But Net

NetStreit (NTST) is a net lease REIT that owns 361 properties in 41 states with an average remaining lease term of 9.6 years.

In around two years NTST has grown its portfolio by an average of $101 million per quarter and now has a market cap of just over $1 billion.

So far in 2022 the company has completed over $135 million in net investment activity (in Q1-22) by acquiring 34 properties for $90 million at an initial cash capitalization rate of 6.3% and a weighted average lease term of 8.2 years.

Also, NTST had nine projects under development, representing $37 million of additional investment.

At the end of Q1-22 NTST’s portfolio was comprised of 71 tenants contributing $77 million of annualized base rent. The portfolio had a weighted average lease term remaining of 9.6 years with 80.6% of ABR represented by tenants with investment-grade ratings or investment-grade profiles and the portfolio was 100% occupied.

As seen below, NTST has traded in-line with NTST year-to-date, while outperforming VNQ:

Yahoo Finance

NTST IPO’s in 2020 and since that time the company has maintained prudent capital markets discipline, as of Q1-22 net debt to annualized adjusted EBITDA was 4.6x, which was at the low end of the targeted leverage range of 4.5 to 5.5x.

The company had total debt of $295 million outstanding, of which $175 million was from its fully hedged term loan with a remaining balance from the revolving line of credit. There are no debt maturities until the maturity of the revolver in December 2023, which is subject to a one-year extension option.

Also, in Q1-22 NTST reported AFFO per share of $0.29 and it declared a $0.20 regular quarterly cash dividend (was payable on June 15) that reflected a payout ratio of just under 69%. NTST also increased its 2022 AFFO per share guidance range to $1.14 to $1.17 and net investment guidance to at least $500 million for the year.

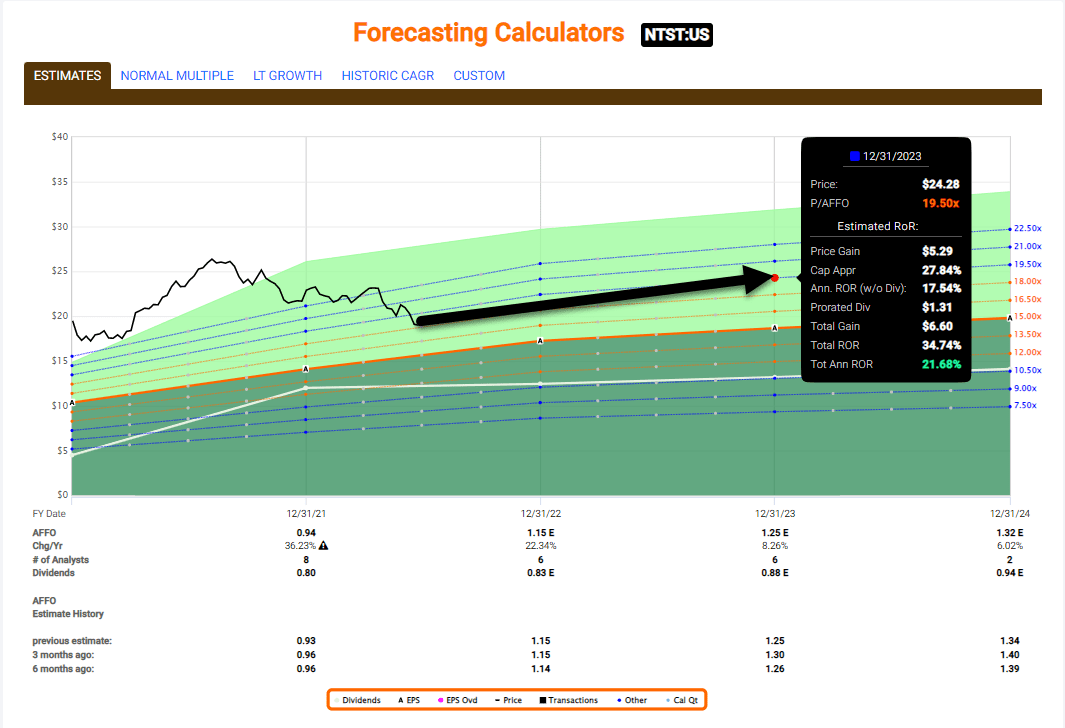

FAST Graphs

As seen above, analysts are forecasting NTST to grow AFFO by 22% in 2022 and 8% in 2023. Shares are now trading at $18.99 with a P/AFFO of 18.3x and dividend yield of 4.2%. The payout ratio (of 69%) is one of the lowest in the net lease REIT sector. iREIT maintains a Buy with a 12-month total return forecast of 20%.

FAST Graphs

REITs Aren’t Bonds

One of the biggest misconceptions within the Net Lease REIT sector is that these predictable dividend-payers are bonds, when in fact they’re not even closely related.

Net Lease REITs have two ways to grow…

- Internally, via rent bumps that average 1.5% to 2.0% annually (un-levered)…and…

- Externally, sourcing new acquisitions and development…

For income-oriented investors, now is a great time to be adding shares to various Net Lease REITs, recognizing that their tenants are responsible for paying for the 3 T’s

3 Ts Defined: Taxes, Trash, and Taxes…

I don’t know about you, but I like the prospects of owning real estate that offers dependable and predictable income, along with capital appreciation.

All three of these lesser-known net lease REITs are worth exploring…

iREIT on Alpha

Be the first to comment