Gam1983

I find it interesting that most Canadian real estate investment trusts (“REITs”) pay monthly dividends while just a handful of U.S. REITs pay monthly.

I suppose that’s due to the fact the there’s a larger percentage of Canadian institutional investors that prefer private real estate, and so the percentage of retail investors (in Canada) is influenced by the stickier retail investor base.

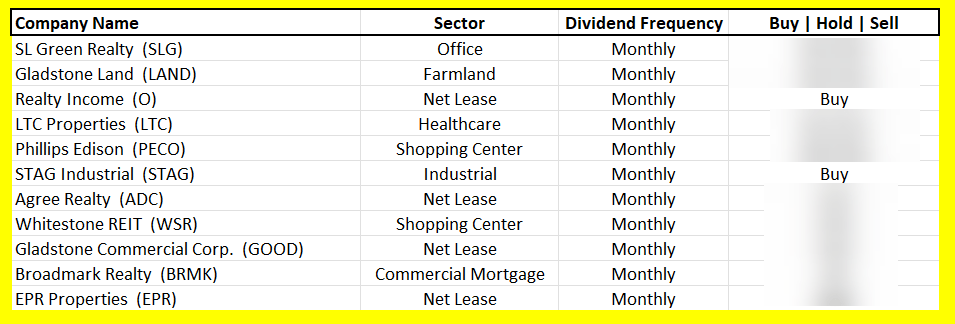

That’s just a guess, but regardless of the rationale, the retail investor base for U.S. REITs is much smaller. Here are the U.S. monthly payer in our iREIT coverage universe:

iREIT on Alpha

That’s 11 Equity REITs out of around 150.

What’s crystal clear is that institutional investors don’t care whatsoever whether the dividend is paid monthly or quarterly.

In fact, I would argue that these big money investors would be content if they got paid once a year, because they’re more interested in total returns.

Of course, I make the case often that REITs should pay monthly, because it doesn’t really cost them much of anything to deliver a monthly check. As Joey Agree, CEO of Agree Realty Corporation (ADC), pointed out in a CEO Interview:

“It’s a great question we did a deep dive into it. So first of all, there are very diminutive frictional costs. It’s literally several thousand dollars with a transfer. We looked into it and we finally came to the conclusion that we believe that the decentralization of Wall Street is going to be a consistent theme.

Active investors moving into ETFs, individual investors moving into buying shares individually or even partial shares, and in context of our business where we get monthly rent checks with a weighted average lease term of over nine years with 70% investment grade retailers, we think it makes a lot of sense to pay out those dividends.”

Joey added,

“And we haven’t got any pushback from institutional investors. I think individual investors, including myself and the shareholders love receiving it monthly. The costs both frictional and actual are extremely diminutive.”

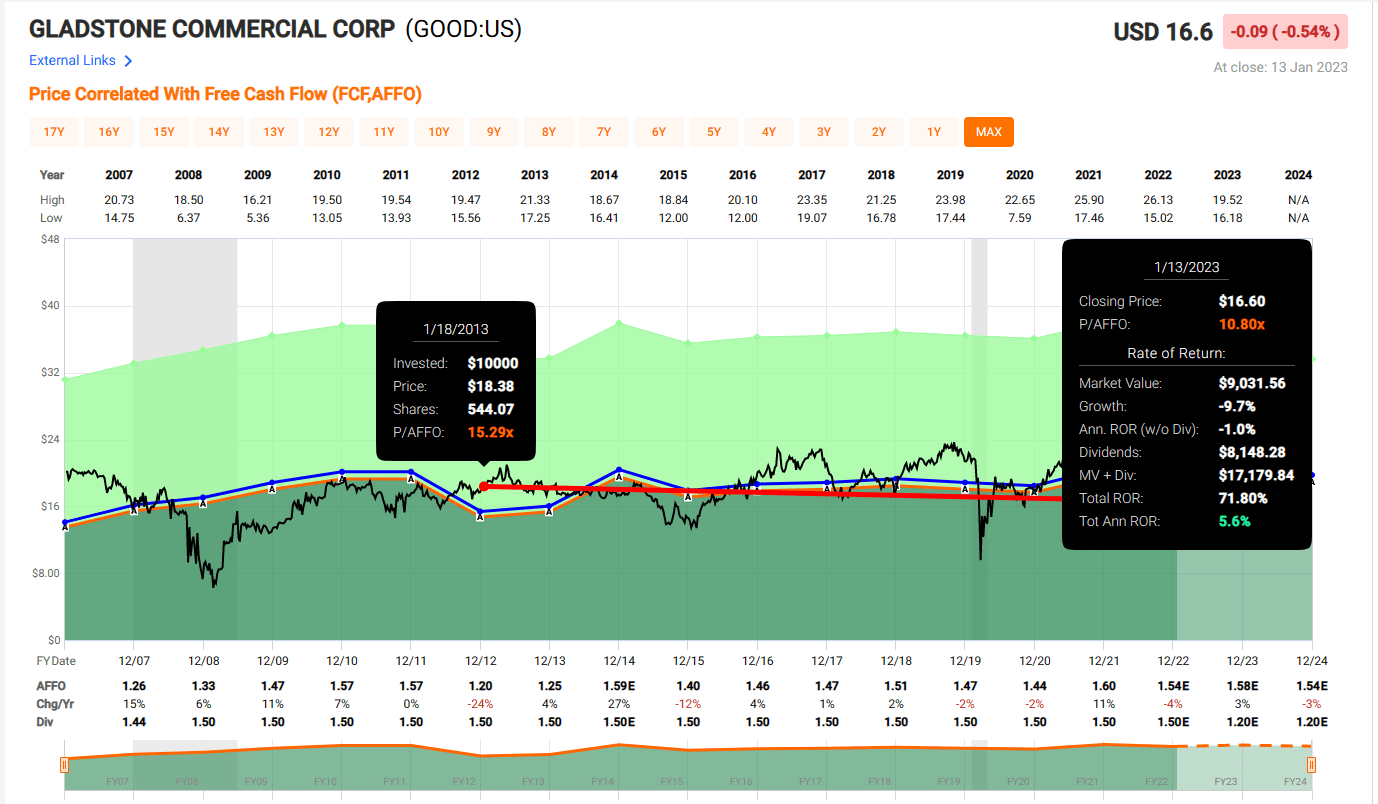

I often remind investors to always look closely at the safety of the dividend, and not to base your decision on a monthly versus quarterly dividend. Case in point: Gladstone Commercial (GOOD). In a recent article, I explained:

“…even though Gladstone Commercial is acquiring lower quality properties (at higher cap rates), the profit margins are laser-thin, suggesting that the externally managed REIT is not generated sufficient profits to sustain its dividend.”

GOOD has been attracting high-yield income for over a decade, yet the company was never able to generate enough cash flow to grow its dividend. Had you invested in GOOD a decade ago, your shares would have returned 5.6% per year.

FAST Graphs

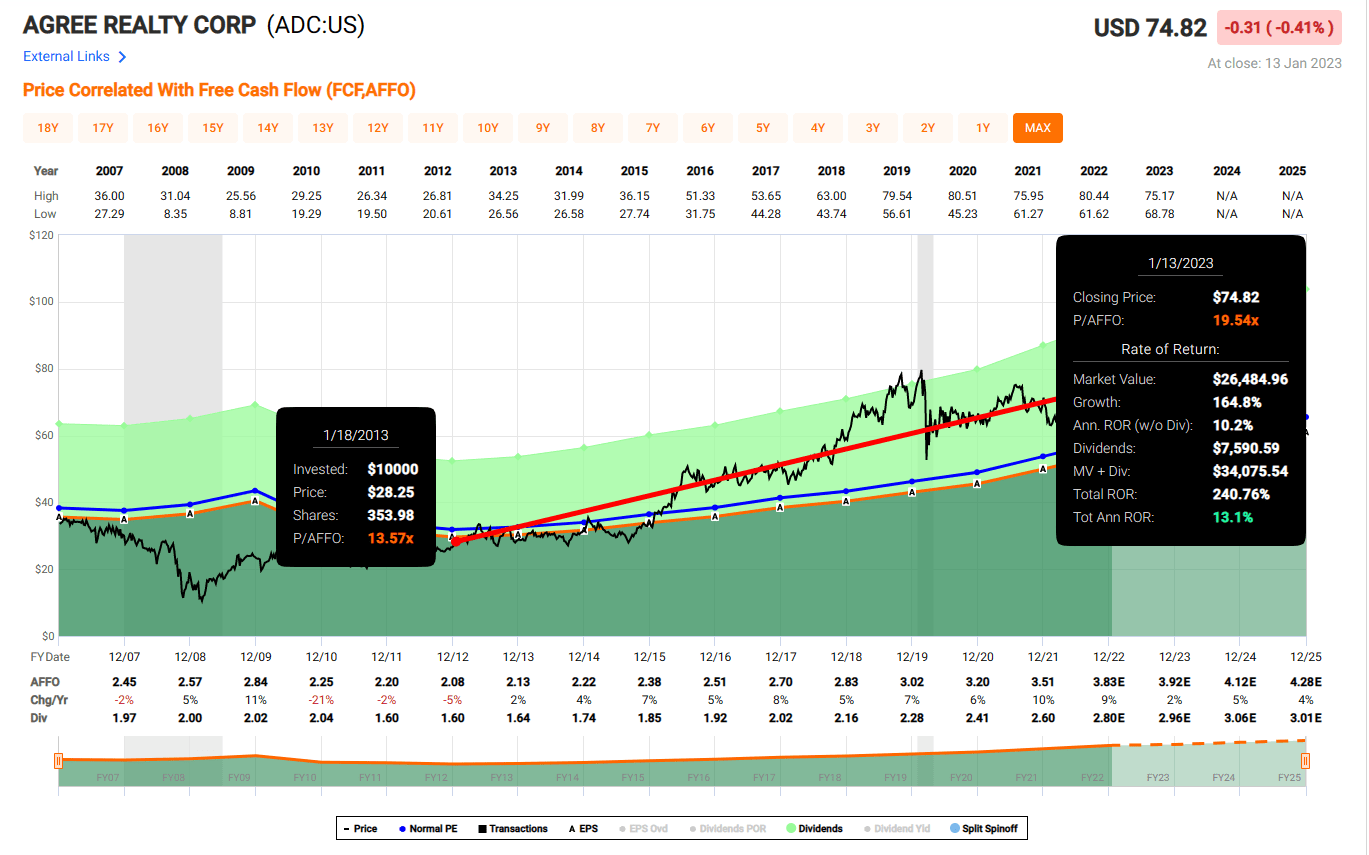

Alternatively, had you invested in Agree Realty a decade ago your shares would have returned over 13% per year, as seen below:

FAST Graphs

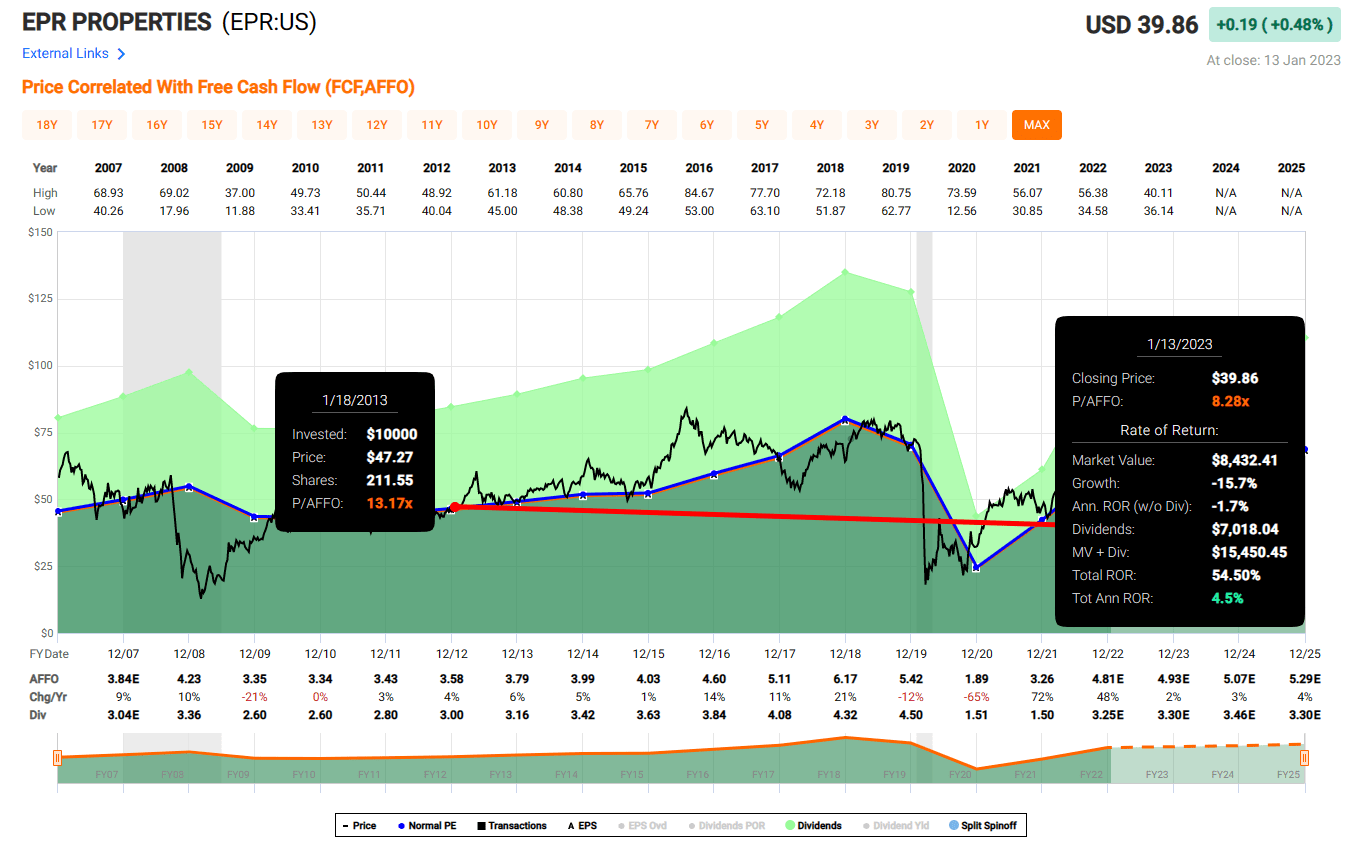

One more example is EPR Properties (EPR), another net lease REIT that we have avoided. Had you purchased shares in this monthly payer a decade ago, your investment would have returned an average of 4.5% per year, as seen below:

FAST Graphs

The point I’m trying to make here is that you must always consider the quality of the underlying dividend, and not just assume that because a company distributes monthly dividend checks that it is safe.

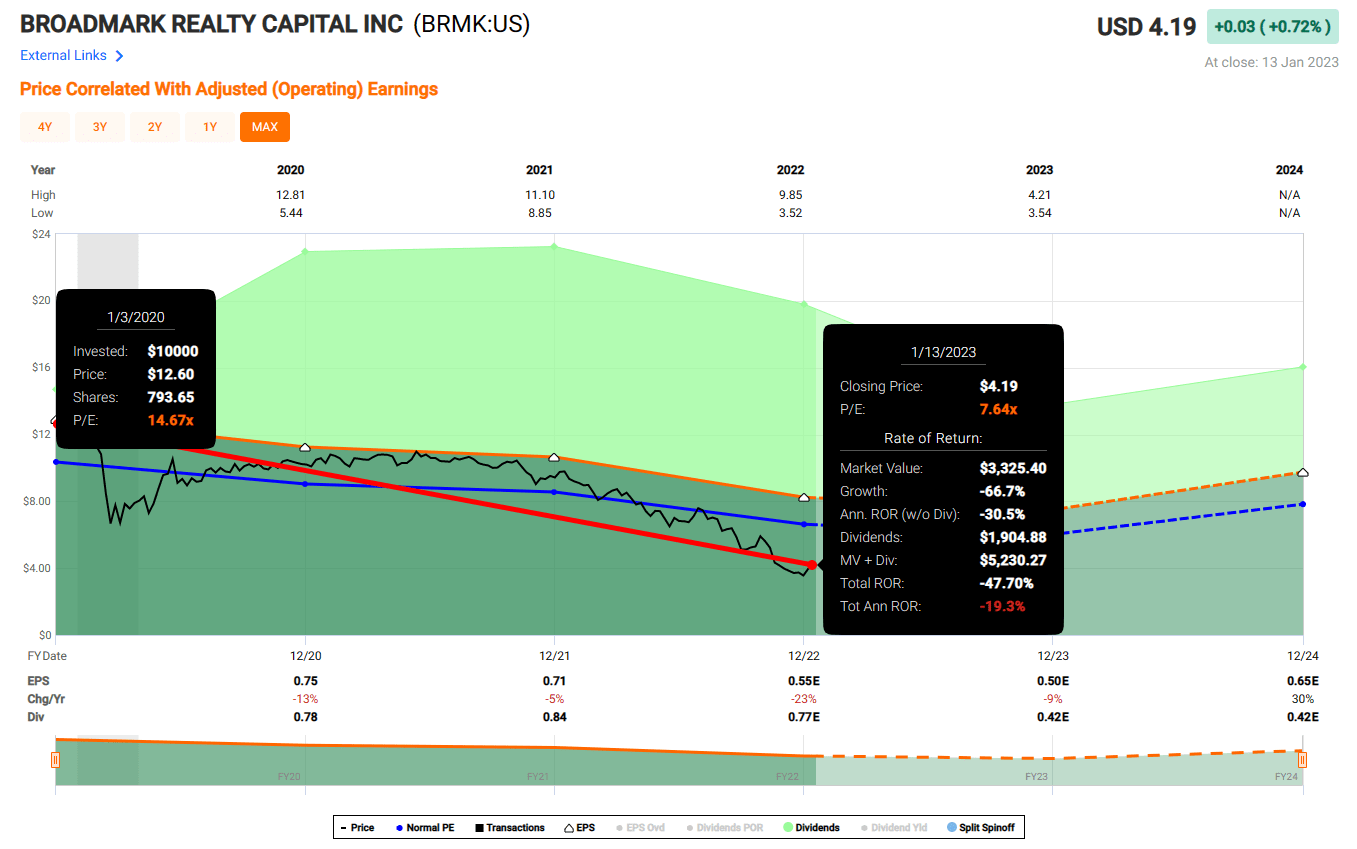

One last example, and we also spotted the cut early, is Broadmark Realty Capital (BRMK). Shares are still yielding 10% (after a dividend cut) and shares have returned -19% annually since listing (in 2020).

FAST Graphs

In full disclosure, I took a modest loss in BRMK, and happy that I unloaded shares before the eventual dividend cut. Fortunately, I avoided cuts with GOOD and EPR, as well as Global Net Lease (GNL) – that once paid quarterly – and The Necessity Retail REIT (RTL) – that also once paid quarterly.

My Monthly Dividend Picks

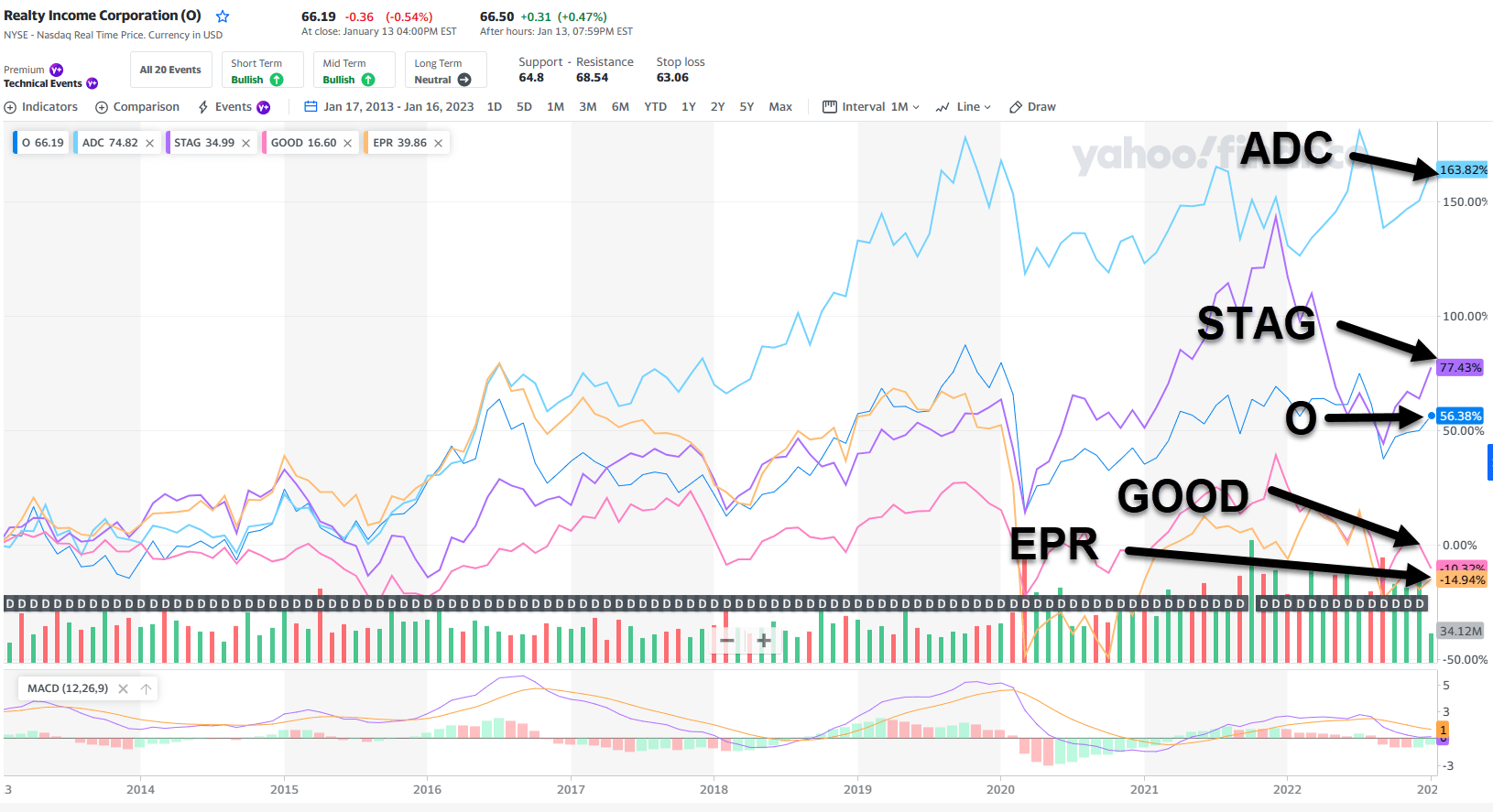

Realty Income Corporation (O)

Realty Income, The Monthly Dividend Company®, is a triple-net Real Estate Investment Trust that owns and leases single tenant free-standing properties. As of 9/30/22, they owned approximately 11,700 properties located in all 50 states with an international presence in the UK and Spain.

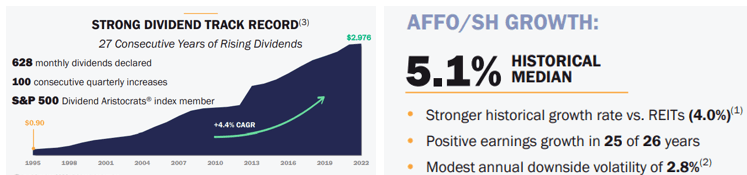

Realty Income is an S&P 500 Dividend Aristocrat with 27 consecutive years of dividend increases. Since 1995, they have increased the dividend at a compounded annual growth rate of 4.4% and support that growth with Adjusted Funds from Operations (AFFO) that has historically grown at 5.1% annually.

On January 10, 2023, they announced the 631st consecutive monthly dividend of $0.2485 for an annualized amount of $2.982 per share. Currently, Realty Income offers a 4.51% annual dividend yield.

Realty Income – Investor Presentation Realty Income Press Release

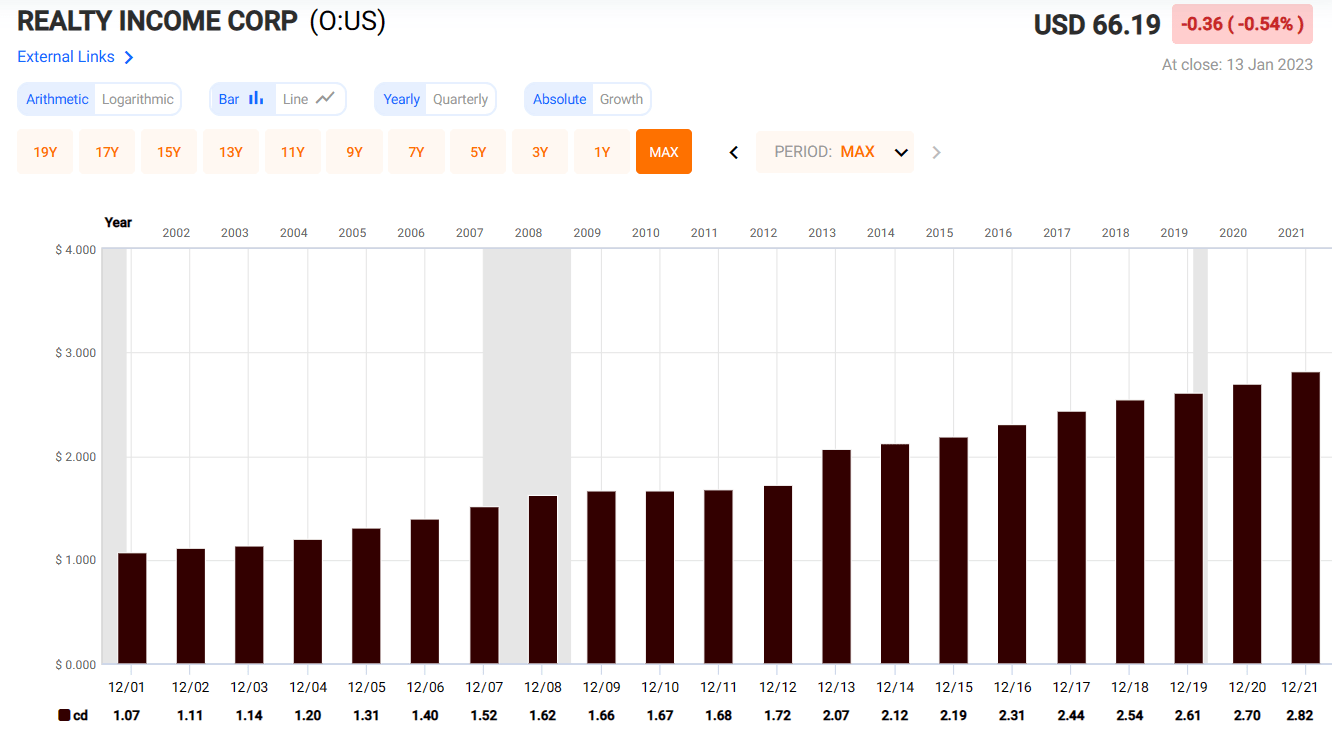

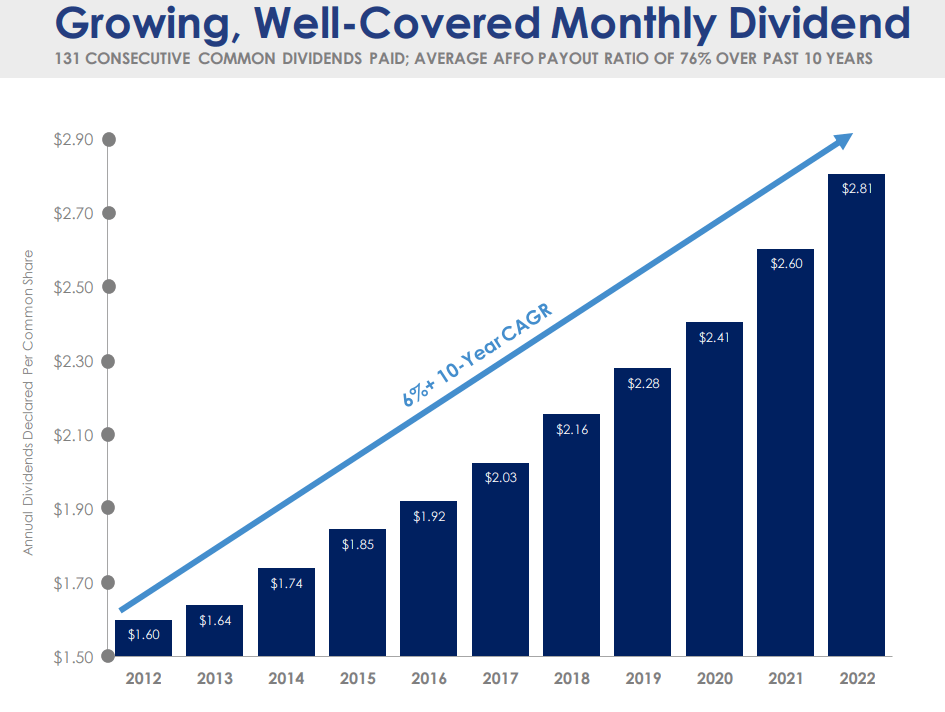

Realty Income has not only maintained but raised its monthly dividend through multiple interest rate environments and recessions, including the 2007-2009 Great Financial Crisis and more recently the covid pandemic.

FAST Graphs (Common Dividend per share)

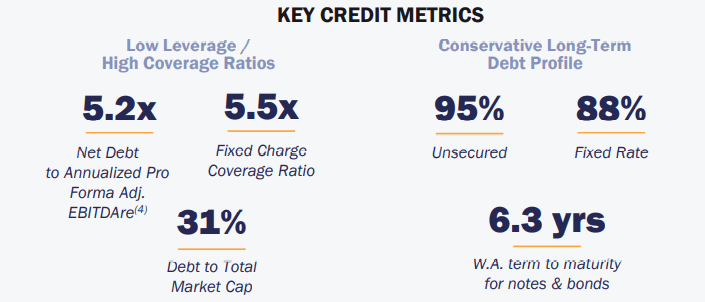

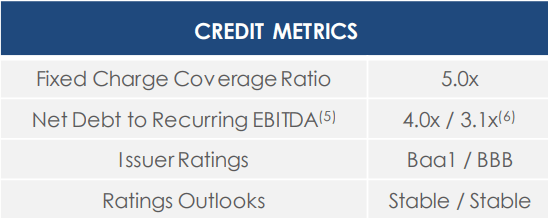

Realty Income should have no problem continuing its monthly dividend streak, as it carries a low AFFO payout ratio and has good credit metrics. They have an A- credit rating and approximately 43% of their rent comes from investment-grade tenants.

Realty Income’s Net Debt to its Annualized Pro Forma Adj. EBITDAre is 5.2x, and they have a Fixed Charge Coverage Ratio of 5.5x. Their weighted average term to maturity is 6.3x years, and 95% of their debt is unsecured with 88% of their debt held at a fixed rate.

Realty Income – Investor Presentation

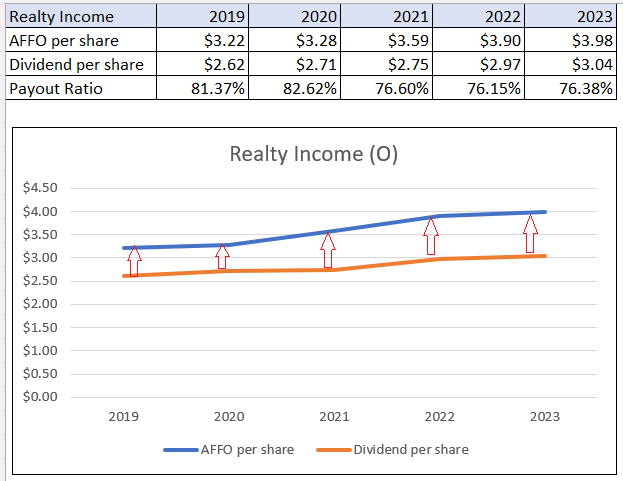

Realty Income’s monthly dividend is safe, averaging an AFFO payout ratio of approximately 79% over the last several years, with an expected AFFO payout of 76.38% in 2023.

FAST Graphs (compiled and calculated by iREIT)

Realty Income is one of only three REITs in our coverage that has a perfect 100 quality score. They have an annual yield of 4.50% and pay shareholders a dividend each month.

They have one of the most consistent dividend records of any REIT and have a conservative AFFO payout ratio which should enable them to sustain and grow the dividend.

Realty Income trades at a wide discount to their normal FFO multiple of 20.41x with a current P/FFO of 15.84x. At iREIT, we rate Realty Income a BUY.

iREIT

Agree Realty Corporation

Agree Realty is a net-lease REIT that specializes in single tenant free-standing properties and is the 2nd monthly dividend payer on our list today. ADC was founded in 1971 and went public in 1994.

As of December 31, 2022, Agree Realty owned 1,839 retail properties totaling ~38 million square feet across 48 states. In addition to their retail properties, ADC has a portfolio of Ground Leases that makes up 12.4% of their annualized base rent.

ADC has raised its dividend each year since 2012 for a 10-year compounded annual growth rate of 6%, and over that time has maintained a conservative AFFO payout ratio of 76%.

Agree Realty – Investor Presentation

Agree Realty has great credit metrics and a strong tenant base, with 67.8% of their annual base rent coming from investment-grade tenants.

Agree Realty itself is investment-grade with a rating of BBB and has an enviable Net Debt to Recurring EBITDA of 4.0x or 3.1x when factoring in the proforma settlement of their forward equity agreement. Additionally, they have a Fixed Charge Coverage Ratio of 5.0x.

Agree Realty – Investor Presentation

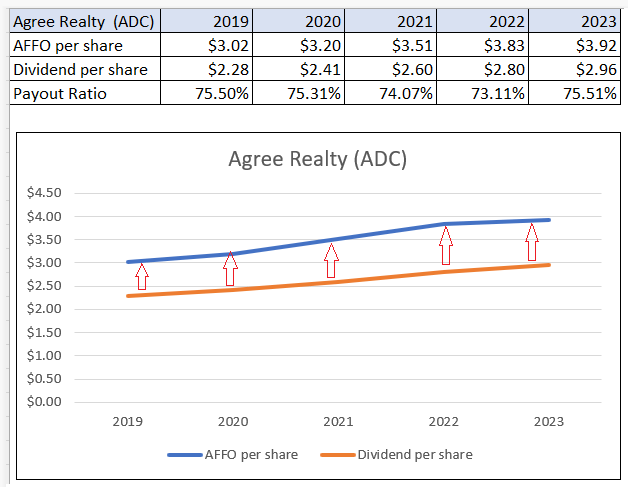

As previously mentioned, Agree Realty has a conservative AFFO payout ratio keeping its monthly dividend safe. Since 2019, they have an average AFFO payout ratio of approximately 75%, with an expected AFFO payout of 75.51% in 2023.

FAST Graphs (compiled and calculated by iREIT)

Agree Realty is one of the top REITs in our coverage in terms of overall quality. They score a 96/100 on our quality score and currently have an annual dividend yield of 3.90% with a 10-year compounded annual dividend growth rate of 6%.

ADC currently trades at a P/FFO of 17.75x, which is a discount when compared to their normal P/FFO of 21.1x. At iREIT, we rate Agree Realty a BUY.

iREIT

STAG Industrial, Inc. (STAG)

Stag Industrial is a REIT that owns and operates industrial properties. As of September 30, 2022, STAG owned 563 properties covering 111.6 million square feet across 41 states.

In addition to their geographic diversity, their portfolio has exposure to over 45 industries. Their largest tenant makes up only 3% of their annual base rent (ABR), while their top 10 tenants only make up 10.2% of their ABR.

STAG – Investor Presentation

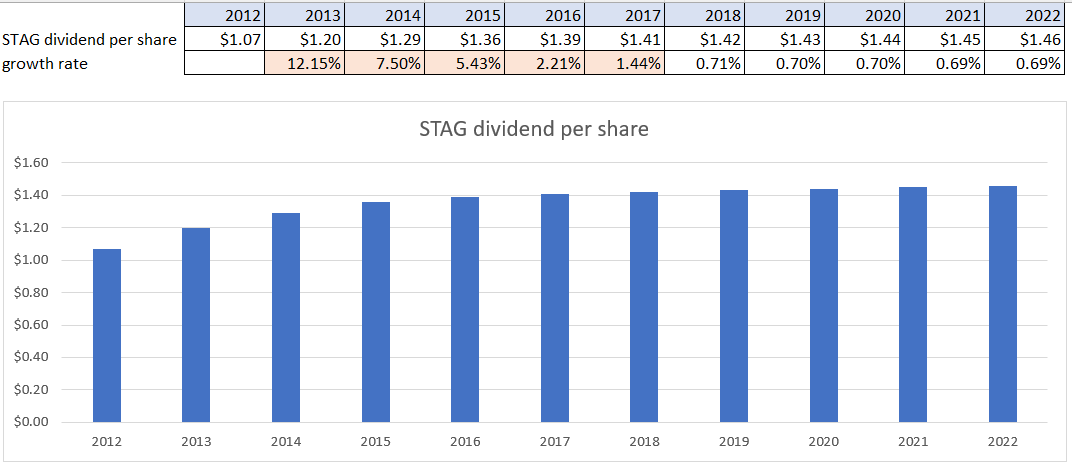

Stag went public in 2011 and started paying monthly dividends in the latter part of 2013.

Over the last 9 years, they have had an average dividend growth rate of 3.50%, although much of that growth took place between 2013 and 2017. Since 2018, the average dividend growth has hovered around 0.70%.

FAST Graphs (compiled and calculated by iREIT)

FAST Graphs

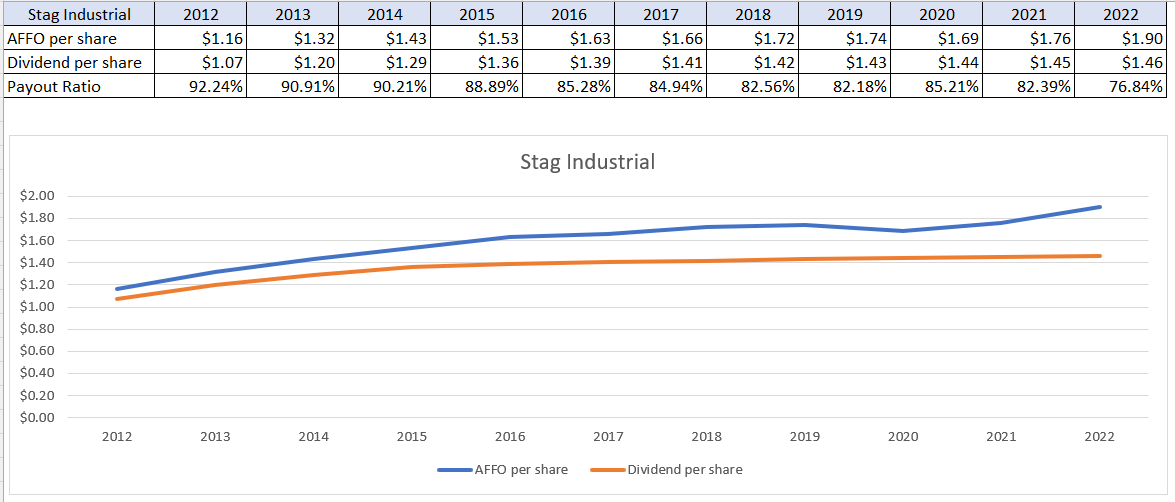

From all appearances, it seems that STAG slowed the dividend growth to improve their AFFO payout ratio. In 2012, STAG had an AFFO payout ratio of 92.24%. By 2022, this metric had improved to 76.84%.

FAST Graphs (compiled and calculated by iREIT)

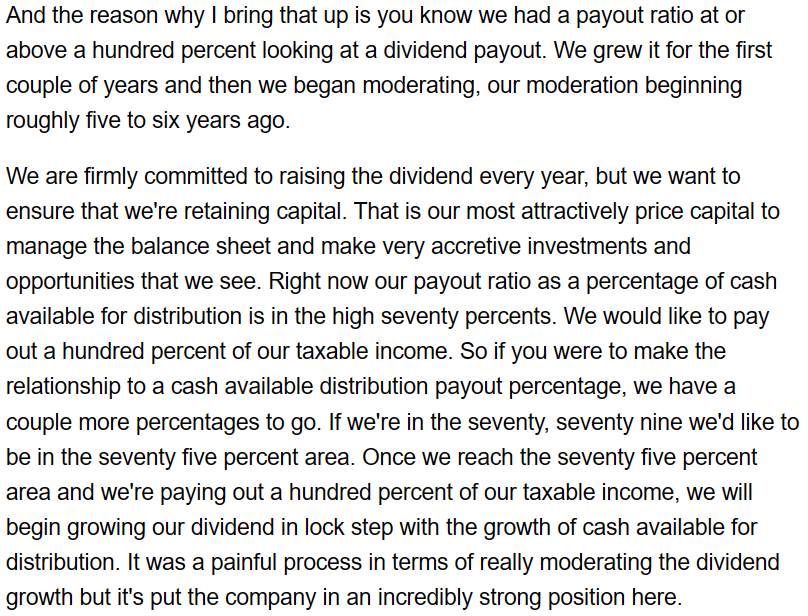

Matts Pinard, the CFO of STAG touched on this in my interview with him last month.

Matts Pinard:

iREIT

iREIT members can find the full interview and transcript at the link below:

The Ground Up Podcast: Matts Pinard, CFO Of STAG Industrial | Seeking Alpha.

While some may be discouraged by the dividend’s recent growth rate, I see this as responsible management. By slowing down the dividend growth rate, STAG has been able to shore up its financial position and payout ratio.

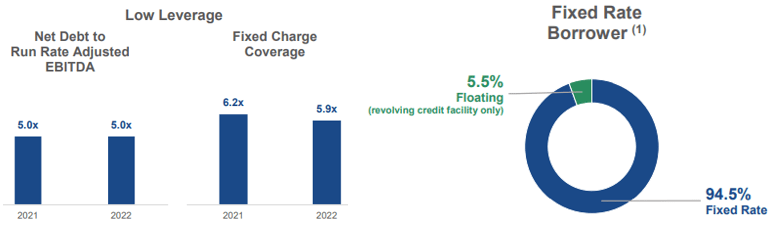

Currently, STAG is in a much stronger position, with an AFFO payout ratio of ~77%, a Net Debt to Run Rate Adj EBITDA of 5.0x, and a Fixed Charge Coverage of 5.9x. Additionally, 94.5% of their debt is fixed rate.

STAG – Investor Presentation

STAG is one of the higher-quality REITs we cover, with a quality score of 87/100. They currently have a dividend yield of 4.20% and pay the distributions each month.

The dividend is well-covered with an AFFO payout of ~77%, and STAG’s management has shown the ability to make hard decisions to improve the overall health of the company. Currently STAG trades at a P/FFO of 14.97x, which compares favorably to their normal P/FFO of 16.58x. At iREIT, we rate STAG a BUY.

iREIT

Welcome to the Club!

I’m happy to own all three REITs – O, ADC, and STAG – and I’ll continue to invest more capital into these names, recognizing that the dividends are well-covered, and the management teams are continuing to drive steady and predictable ROE.

As you know, the key to success is not the frequency of the dividend payment, buy the safety of the dividend. Whenever we see a company that’s not growing its dividend or is not able to cover it, we immediately head for the exit door.

Yahoo Finance

I would like to conclude this article with an official request from the management teams for these REITs. We obviously prefer to see all of these companies increase their dividends annually, and it would be nice to see more of them paying out monthly:

- Alpine Net Lease (PINE)

- CareTrust REIT (CTRE)

- Chicago Atlantic Real Estate Finance (REFI)

- Essential Properties Realty Trust (EPRT)

- Gaming and Leisure Properties (GLPI)

- Global Medical REIT (GMRE)

- Healthcare Realty Trust (HR)

- Highwoods Properties (HIW)

- Innovative Industrial Properties (IIPR)

- Ladder Capital (LADR)

- Medical Properties Trust (MPW)

- National Retail Properties (NNN)

- National Storage Affiliates (NSA)

- NetSTREIT (NTST)

- NewLake Capital (OTCQX:NLCP)

- Omega Healthcare Investors (OHI)

- Physicians Realty (DOC)

- Postal Realty Trust (PSTL)

- Sachem Capital (SACH)

- Starwood Property Trust (STWD)

- UMH Properties (UMH)

- VICI Properties (VICI)

Dividend payments provide investors with valuable clues regarding management’s willingness to reward shareholders. These regular dividends suggest that the company’s earnings power is durable, and its financial condition is strong.

In short, I like monthly checks, but most importantly,

Be the first to comment