pawel.gaul

This article was co-produced with Cappuccino Finance.

The big five (Royal Bank of Canada, Toronto-Dominion Bank, Bank of Nova Scotia, Bank of Montreal, and Canadian Imperial Bank of Commerce) are the largest banks in Canada, and they dominate the Canadian banking landscape.

Thanks to their size and the regulatory barriers on the industry, the big five banks enjoy wide economic moats.

These big five banks control substantial assets, maintain a superb balance sheet with a large amount of ready cash, and are more profitable than the other smaller banks.

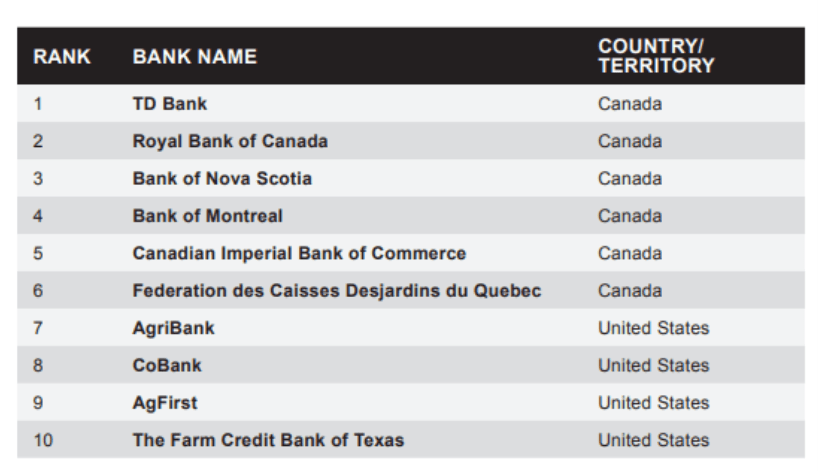

The quality of their assets and balance sheets are clearly demonstrated by their positions at the top five spots in the Safest Banks in North America list by Global Finance.

Safest Banks in North America 2021, Source: Global Finance

On top of that, they have been shareholder friendly, paying a solid dividend and buying back shares. Some of them have a dividend streak exceeding an astounding 150 years.

The 20-25% selloff of the big Canadian banks appears overdone, as dividends are growing. Near-term volatility should be expected, but investors with a buy-and-hold strategy might want to start adding bank stock to their portfolios at these levels.

The recent market volatility and concerns over a Canadian housing bubble has brought their stock price down, but I believe this is an overreaction by the market.

The Canadian big five will be just fine.

The price drops just created an opportunity to grab some stock at a bargain price and attractive yield.

The following three (Royal Bank of Canada, Toronto Dominion, and Bank of Nova Scotia) are my favorite stocks, and all of them combine dividend growth and stability.

Royal Bank of Canada (RY)

Royal Bank of Canada is a diversified multinational bank based in Toronto. The bank offers personal & commercial banking, home equity financing, mortgage loan, mutual funds, brokerage accounts, and credit card services. They are the largest bank in Canada by asset value ($1.4 T).

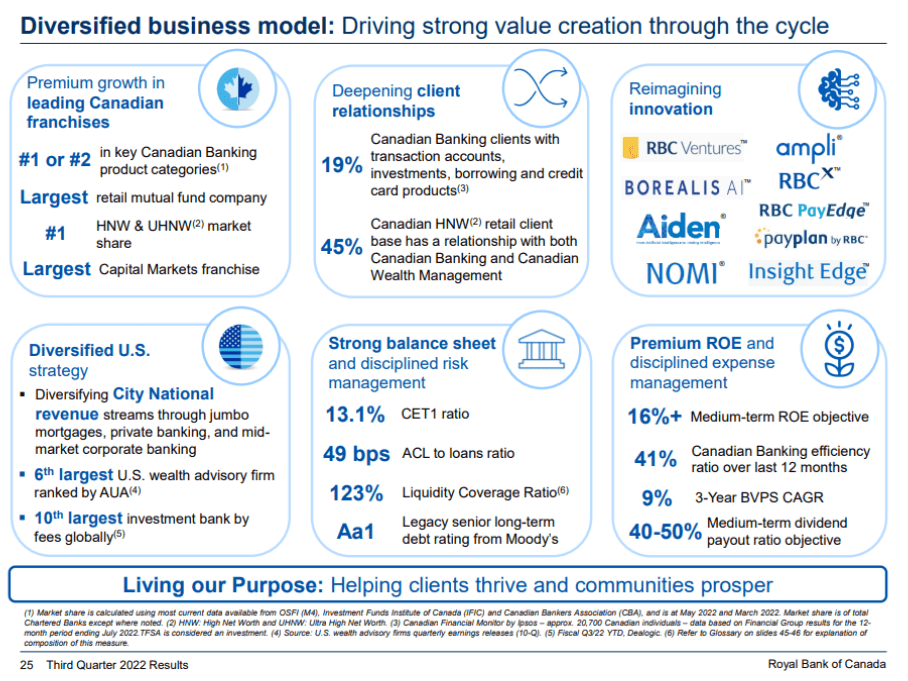

Royal Bank of Canada is the proven leader in the Canadian bank industry. They hold a very diversified portfolio, product lines that are ranked #1 or #2 in the industry, and strong relationships with clients. The balance sheet is very strong, represented by a high Common Equity Tier 1 (CET1) and solid liquidity coverage ratio (123%).

They are also more profitable, compared to others, shown by their high ROE. The recently proposed acquisition of Brewin Dolphin (U.K.’s leading wealth management) will further diversify their portfolio, as well as boost their growth trajectory.

Source: Investor Relations

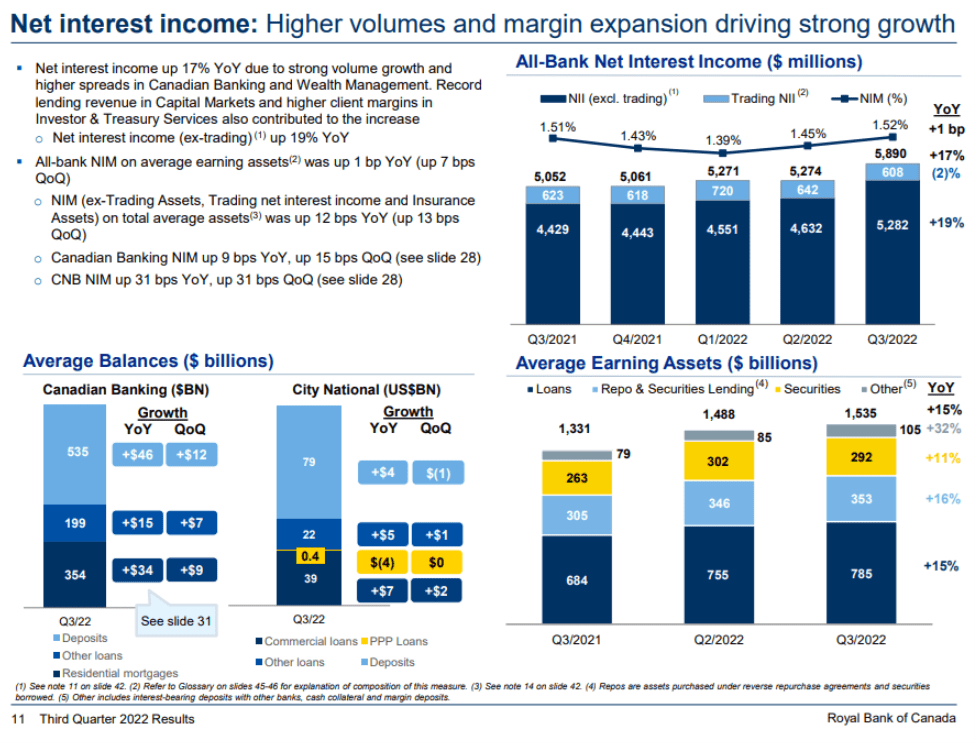

Despite noting some uncertainties in their earnings call, Royal Bank of Canada posted a strong quarter. Their net interest income grew 17% YoY, driven by strong volume growth and higher yield spreads in Canadian Banking and Wealth Management.

The average retail deposit balances are about 30% higher than pre-pandemic levels, and the corporate balance sheets and personal savings are steady and healthy across the board. Their Super Prime Group moved its cash into higher yielding offerings during the quarter.

They recognized a larger provision for credit losses, as macroeconomic conditions deteriorate, and this larger provision contributed to the lower net income during the quarter.

Source: Investor Relations

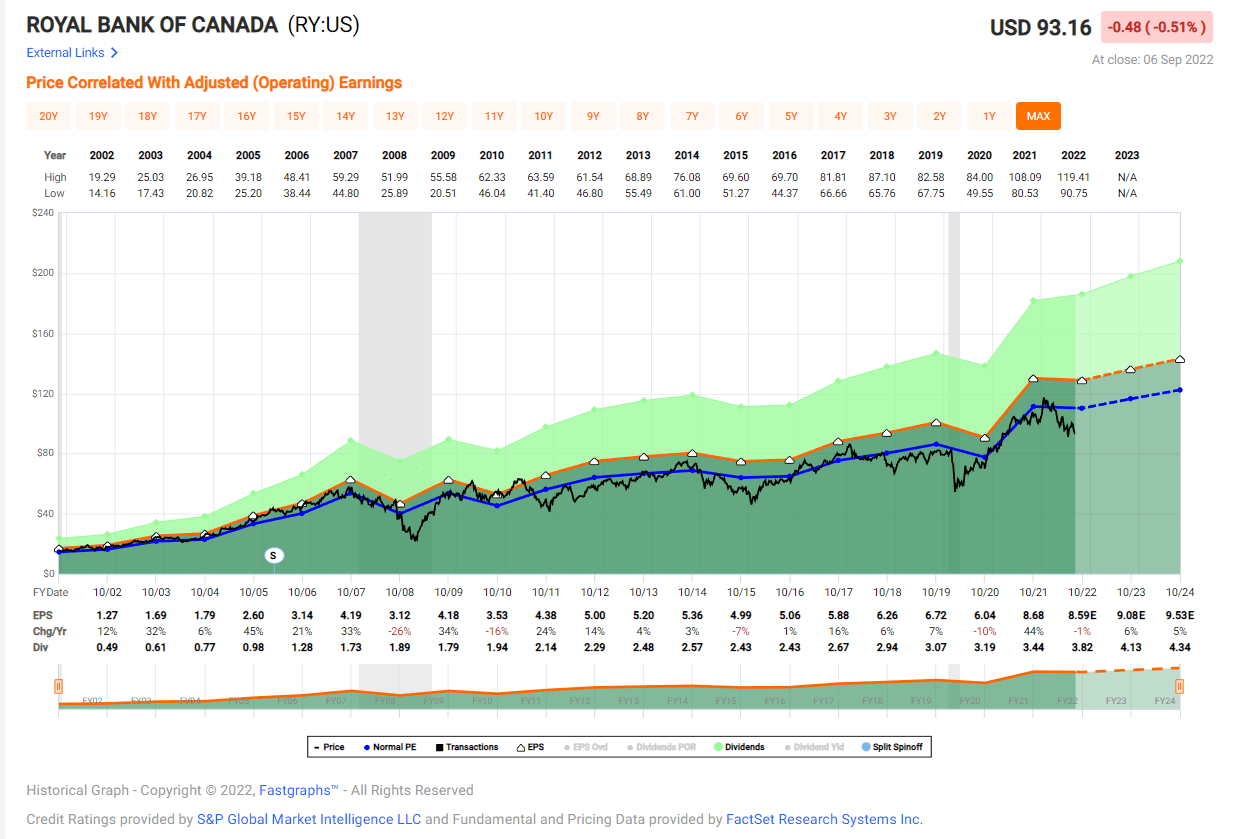

Supported by their solid performance and strong balance sheet, Royal Bank of Canada bought back 10 million shares and paid $1.8 billion in dividends this quarter. They have consistently increased the dividend (4.63%, 5-year CAGR), and I expect them to continue in the future.

Looking at their valuation, P/E ratio of 10.81x is significantly lower than their normal P/E ratio of 12.29x (5-year average). This lower valuation is caused by the recent market volatility and less rosy economic outlook for Canada and U.S. But given their strong balance sheet and wide economic moat, I expect them to comfortably weather any economic cycle.

FAST Graphs

Toronto-Dominion (TD)

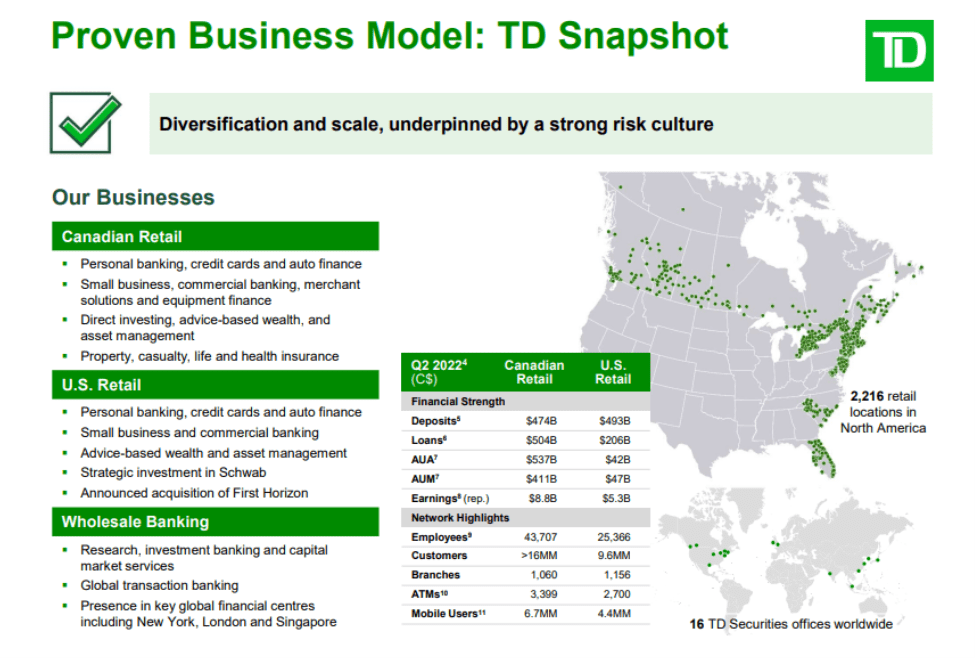

Toronto-Dominion serves more than 27 million customers worldwide, and they have more than 2,000 retail locations across North America. Toronto-Dominion operates in three major segments: Canadian Retail, U.S. Retail, and Wholesale Banking.

Source: Investor Relations

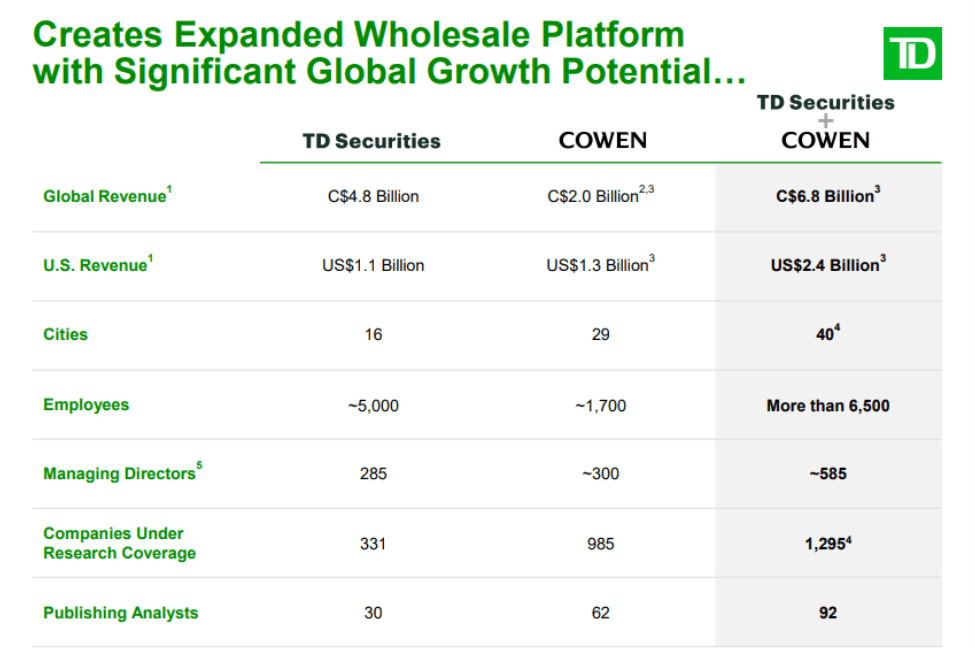

On top of the acquisition of First Horizon Bank announced earlier this year, Toronto-Dominion made another big splash by announcing the acquisition of Cowen.

As Cowen is a leading independent dealer with a strong, diversified investment bank, the acquisition will increase revenue substantially and provide depth to TD Securities services. The TD Securities will benefit from the addition of strong talent (1,700 colleagues), a larger footprint (29 cities), and long-term growth (revenue synergy of $300-350 M).

Source: Investor Relations

The term of the purchase was $39 per share, and $1.3 B in aggregate (100% cash consideration). Although Toronto-Dominion used a lot of cash for this transaction, the CET1 ratio is still expected to stay above 11%, demonstrating the strength of Toronto Dominion’s balance sheet. The expected ROIC after reaching full synergy is around 14% for the acquisition.

In the most recent quarter, Toronto-Dominion reported great earnings, beating both EPS and revenue estimates. Their Canadian retail segment earned $2.3 B from record revenue of $7 B. Their card business performed very well, with loan volume up 10% YoY as consumer spending stayed robust. Business banking segment also achieved strong growth, driven by double digit loan growth.

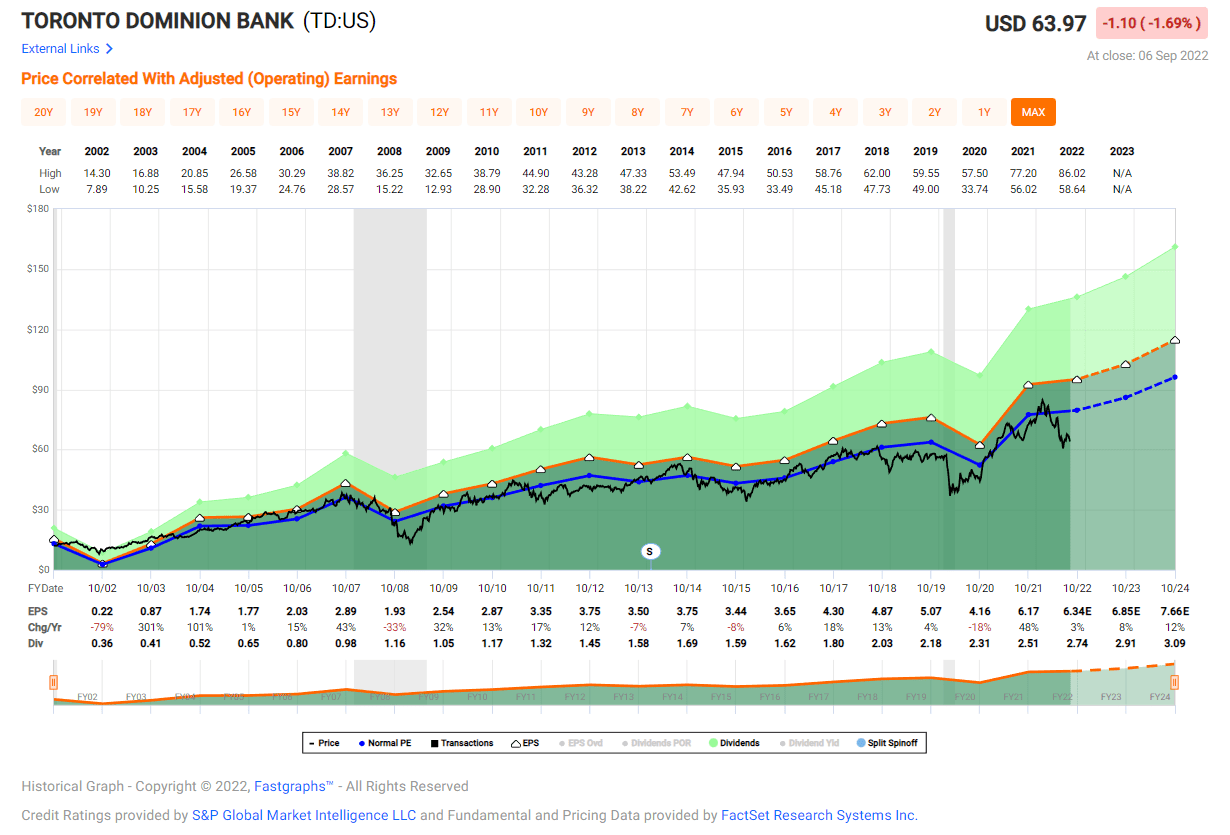

Looking at their valuation, P/E ratio of 10.1x is about 20% lower than their 5-year average (12.0x). The uncertainty swirling around the Canadian real estate market, recession fears, and hawkish central banks (both Canada and U.S.) are the main reasons for the drop in stock price and current low valuation.

Given their strong balance sheet and synergies expected from First Horizon Bank and Cowen, I expect Toronto-Dominion to keep on growing. Their revenue and profit will continue its long-term growth trajectory, and shareholders will be rewarded with a solid dividend growth and stock appreciation.

Toronto-Dominion’s dividend is well covered with payout ratio of 42%, and I expect them to continue raising the dividend (8.10%, 5-year average).

FAST Graphs

Bank of Nova Scotia (BNS)

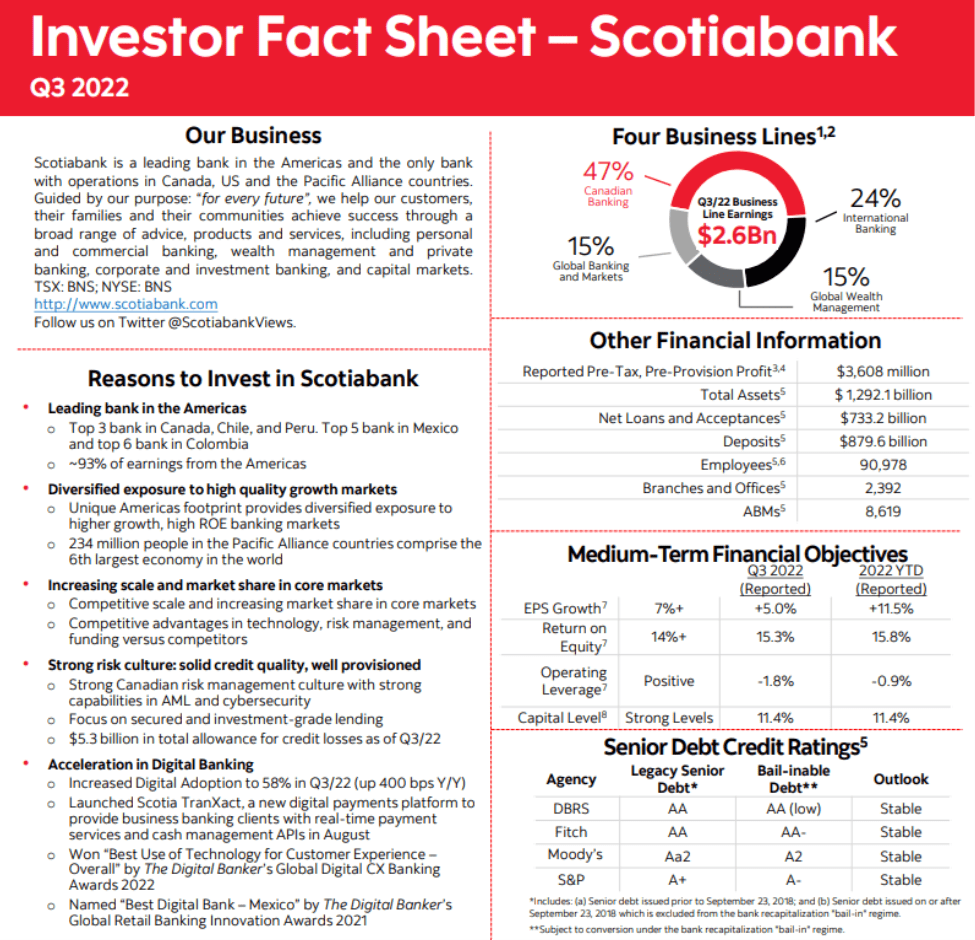

Bank of Nova Scotia, or Scotiabank, is the third largest bank in Canada, and they provide a broad range of advice, products, and services, including personal banking, commercial banking, wealth management, and investment banking.

Scotiabank has a good combination of growth and stability. Their portfolio is diversified across high quality markets that present strong growth opportunities, represented by a solid EPS growth target of 7% (11.5% in YTD 2022).

Return on Equity is reasonably high at 15.3% in 2022. As mentioned in the intro, Scotiabank is one of the safest banks in North America (ranked at 3rd), and their senior debt credit ratings are at AA, Aa2, and A+ (Fitch, Moody’s, and S&P, respectively) with a stable outlook. Literally, shareholders’ money is in good hands with Scotiabank.

Source: Investor Relations

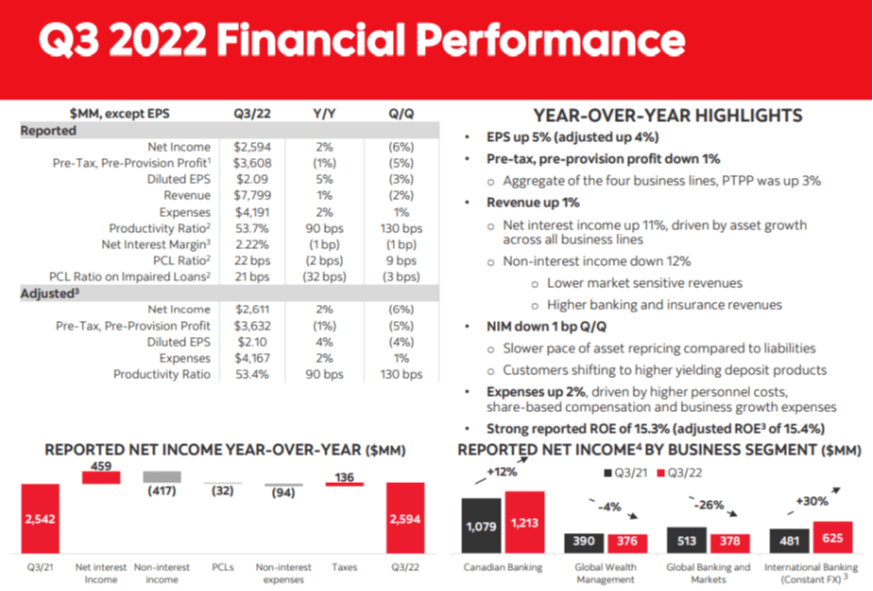

In the latest quarterly earnings call, Scotiabank reported solid earnings of $2.6 B ($2.10 per share), which was 4% higher than last year. Strong personal, commercial, and corporate banking activity drove another great quarter for Scotiabank. Net interest income increased by 11% YoY, driven by both asset and loan growth across all their business segments.

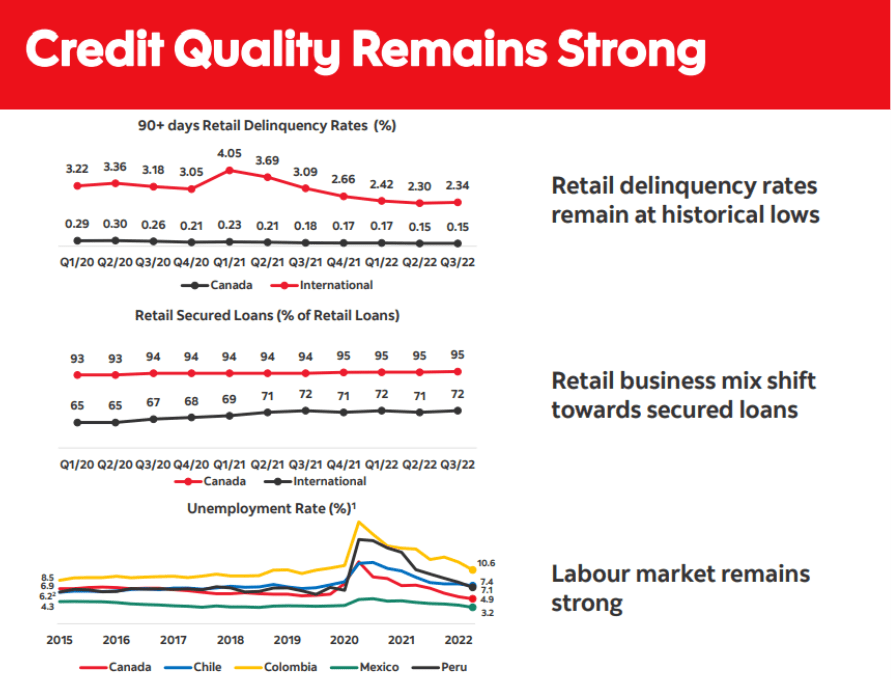

The impact of high inflation and low consumer confidence were counterbalanced by a strong labor market and low delinquencies. Overall consumer spending in Canada also showed resiliency, helped by high deposit balances and strong employment.

Source: Investor Relations

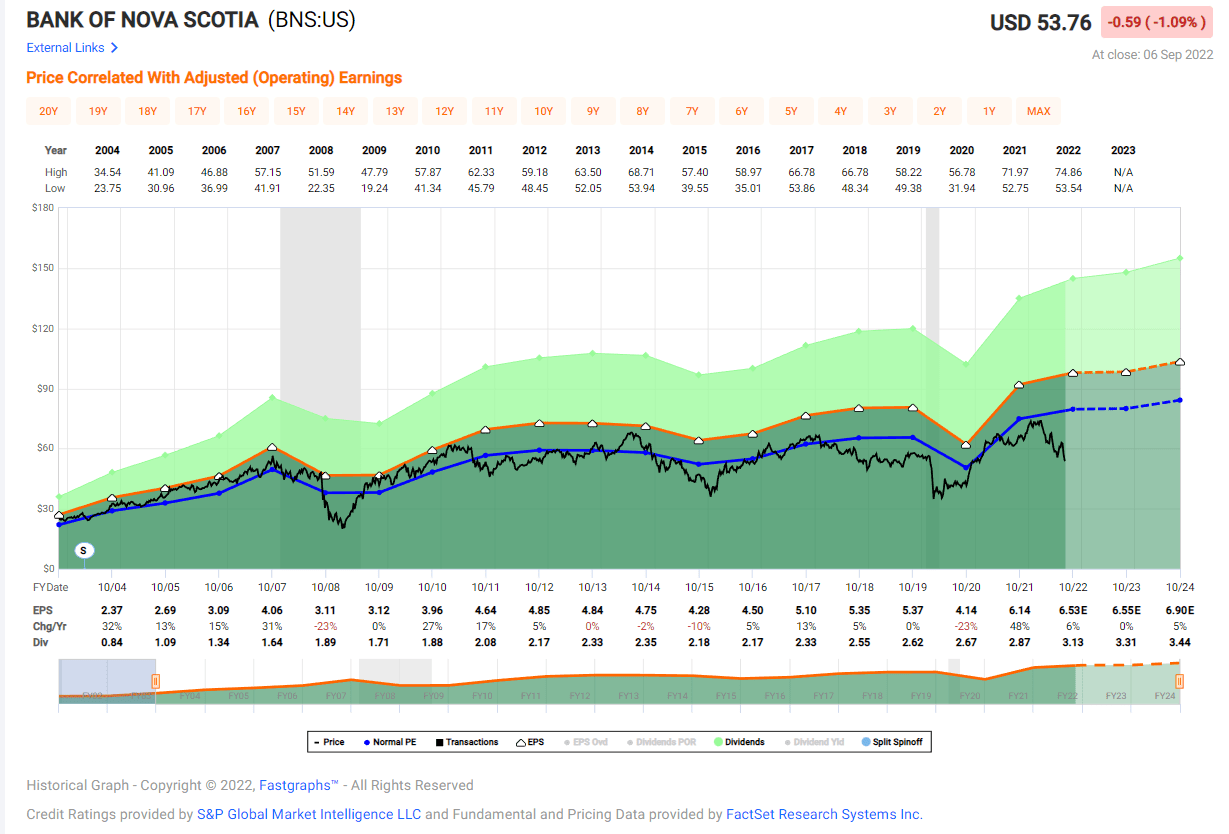

Scotiabank’s stock price has dropped from $75 per share in March to its current level around $55 per share, and it created a nice entry point for an investor seeking an opportunity for stock appreciation with a strong dividend payout.

Source: Investor Relations

Their dividend yield is at 5.86%, and given their strong balance sheet and growth trajectory, I expect their stock price to recover. Their P/E ratio of 8.17x is simply too low for a high-quality bank like Scotiabank. Also, their valuation is about 25% lower than their historical average (10.99x, 5-year average).

During the last quarter, Scotiabank repurchased about five million shares (31 million shares YTD), and they are committed to rewarding shareholders through their stock repurchase program.

I also expect them to continue increasing their dividend (4.7% growth, 5-year average). Their dividend is well covered with a 47% payout ratio. Economic uncertainty and high inflation may bring challenges to Scotiabank in the short term, but I remain confident that they will bring outsized gains in the long run.

FAST Graphs

Takeaway

The stock market, and, to the certain extent, the whole world is full of uncertainties these days: ongoing Russia-Ukraine war, oil production, high inflation, supply chain disruption, and (still) Covid lockdowns. The list goes on.

More specific to the Canadian market, there are growing concerns over the Canadian real estate market. All these uncertainties have combined to bring a great deal of volatility to the stock market.

In turn, this volatility has lowered the price for premium stocks like Royal Bank of Canada, Toronto-Dominion, and Scotiabank.

However, all three of these banks have an outstanding balance sheet with large liquidity available, so I expect them to weather through an economic dip very well and continue their long-term growth.

Also, Royal Bank of Canada and Toronto-Dominion made key acquisitions that will boost their growth trajectories.

Therefore, I will take recent drops in their price as a welcome gift. It’s a great opportunity to add these stocks at a bargain price, while collecting a juicy dividend.

Note: We published “What You Need To Know About Foreign Dividend Withholding Taxes” for iREIT on Alpha members.

Be the first to comment