JasonDoiy/iStock Unreleased via Getty Images

23andMe (NASDAQ:ME) has been a relatively well-known consumer product company for many years. After the company went public via a SPAC, investors poured into the name with a heightened belief that 23andMe could one day monetize their significant proprietary data set, hosting over 13 million consumer genetic tests.

Revenue during the most recent quarter grew 9% yoy, but adjusted EBITDA loss reached $50 million, down from the $27 million loss in the year-ago period. And with the company having $479 million of cash left on the balance sheet, the current run-rate FCF loss of $70 million gives them just 1.5 years left of operating before they need a capital raise.

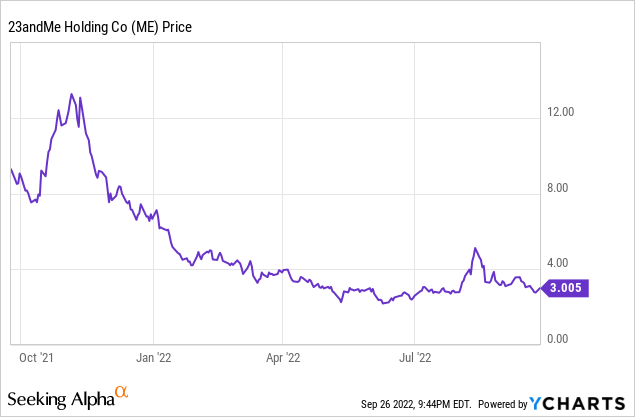

Since the company completed their public offering via a SPAC, the stock has fallen from $10 down to $3 as investors continue to see disappointing financial results. And while there continues to be progression with the company’s co-development programs, investors have yet to see a therapeutic program become mainstream and gain full regulatory approval.

While the company reported disappointing results, investors should continue to look at the company for what they actually are. They are not a high-growth, profitable, cash flow generating company. However, they are the leader in DNA collections, hosting significant amounts of proprietary data for the potential co-development of future drugs.

For now, I continue to be a believer in the long-term potential of the company and given the ongoing stock weakness, one may start to think of 23andMe as a possible acquisition target for a larger drug development company.

23andMe Overview

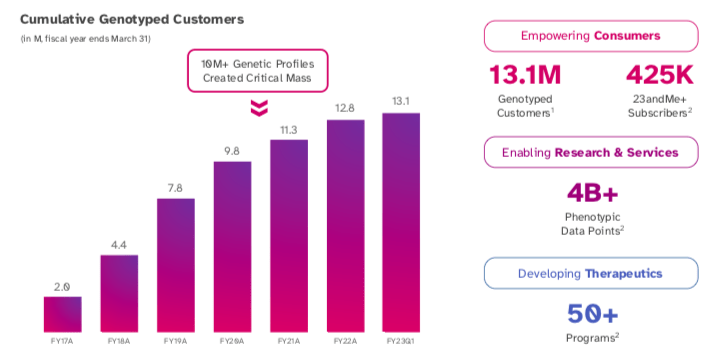

For those who are unfamiliar, 23andMe provides consumers with DNA genetic testing products, providing insights into an individual’s ancestry, DNA, and genetics. With over 13 million consumers being genotyped and 80% of those opting-in to 23andMe’s research, the company has developed a vast amount of proprietary data into DNA sequencing.

23andMe

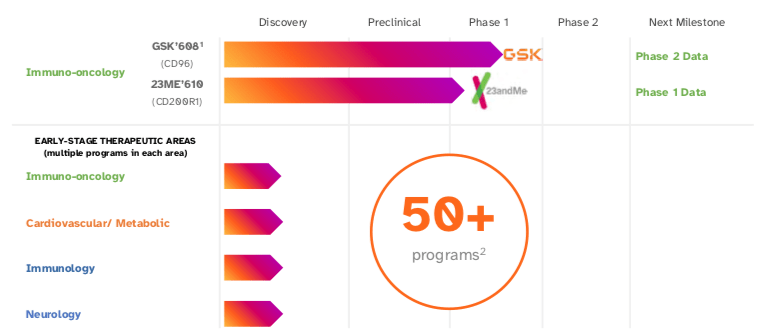

Given this vast amount of data, 23andMe has developed 50+ programs, largely in early-stage therapeutic areas. With the hope of co-developing a drug, 23andMe has a strategic collaboration with GSK (GSK), giving 23andMe access to GSK’s technology and platform while GSK gets access to 23andM3’s data sets.

Recent Financial Results

The company reported FQ1 earnings in early August, with revenue growing 9% yoy to $64.5 million. As a backdrop, the company will likely continue to grow revenue in the 5-10% range as they are more focused on data collection for the potential co-development of future drugs. So while the near-term financial metrics are unattractive at face value, I continue to believe the real value of the company lies within their database.

Regarding FQ1 revenue growth, management called out a few moving pieces. Investors should also remember that the company’s Research Services revenue is largely made up of their collaboration with GSK, representing around 13% of total revenue.

First quarter revenue growth was primarily due to the inclusion of a full quarter of telehealth services and an increase in subscription revenue. These increases were partially offset by lower revenue in the other areas of Consumer & Research Services.

23andMe

From a profitability standpoint, the company reported an adjusted EBITDA loss of $50 million, which was nearly double that of the $27 million loss in the year ago period. Combined with increased costs from the previously acquired Lemonaid’s telehealth business, 23andMe also saw increased labor costs.

Given the ongoing losses, investors will naturally start to look at the company’s balance sheet and their ability to operate as an ongoing concern. At the end of FQ1, 23andMe had $479 million of cash, though they burned through ~$75 million of cash just during the most recent quarter. At this run-rate, the company would have a little over 1.5 years left of operating before one of two things would need to happen.

First, and likely the most preferable, 23andMe would need to significantly improve their cash burn and start to move towards profitability. While investors likely don’t expect to see profitability in the near-term, by better managing their cash burn, 23andMe would have a safer buffer of cash.

If that does not occur, then option two would be for the company to raise capital, either through issuing debt or equity. Given that the stock remains significantly down from the company’s original listing price (down around 70%), raising meaningful equity would significantly dilute current shareholders.

23andMe

For the full-year, the company reiterated their revenue guidance of $260-280 million, which compares to consensus expectations for $275 million. Adjusted EBITDA loss is also expected to be $195-215 million, which reiterates my belief that the company may need to raise capital in the near future unless they are able to get expenses under better control.

While the financial situation has seen better days, 23andMe continues to succeed in building out their moat around human genome data.

In our therapeutics efforts, we continue to use our research platform to create a pipeline of more than 50 programs backed by human genetic data with two now in Phase 1 clinical trials. We also just started the fifth year of our exclusive target discovery collaboration with GSK. Our collaboration with GSK has been very productive and we believe GSK’s decision to exercise their option for a fifth year further demonstrates the value of our unique database for discovering novel targets for drug development. We believe the new therapeutics that come out of our discovery engine will eventually play a significant role in helping people benefit from the human genome.

For now, I believe investors will continue to focus on the path towards financial improvement and while the positive updates on the data and GSK operating side of the business are great to see, ultimately the stock will move in relation to a combination of both financial and operational acumens.

23andMe

With the company now having 13.1 million genotyped customers and 425k 23andMe+ subscribers, they continue to build out their proprietary dataset, thus further giving them a competitive advantage. Their co-development partnership with GSK has also enabled 23andMe to be involved with 50+ programs aimed at developing therapeutics. While the success rate remains very low with all therapeutic investments, it only takes one major breakthrough for the company to achieve scaled success.

Valuation

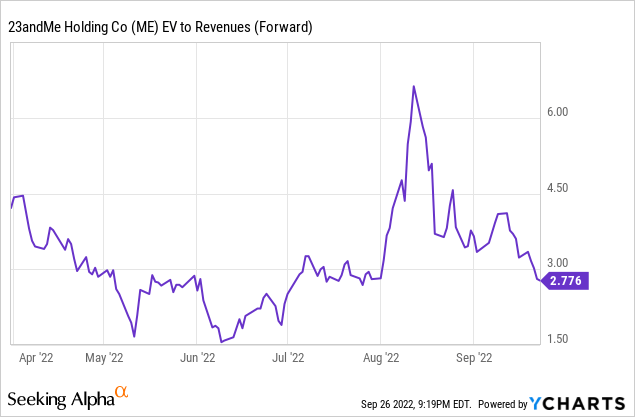

Given the challenged financials combined with the long-term growth partially relying on a new drug/therapeutic discovery, this is a very challenging name to value. Add in some uncertainty around how long the company can continue to burn cash before they need to raise funds, and it’s no shock to see the stock remain under significant pressure during these challenging macro times.

With the company’s enterprise value just under $1 billion, it also would not be surprising to see the company be a potential acquisition target for a larger drug development company. Additionally, given their close relationship with GSK, who has a market cap approaching $60 billion, 23andMe could become a strategic acquisition given their significant proprietary data.

While I have not seen of any acquisition rumors, it would not surprise me if this type of headline hit the news over the coming quarters. Yes, the macro environment and rising interest rates makes an acquisition a little less attractive now, however, with 23andMe’s enterprise value continuing to move south, this could end up being a plausible outcome.

For now, I continue to believe that the stock has some long-term upside potential. Yes, I have been wrong about this company and have seen shares drop from $10 to $3, but given the negative sentiment, long-term therapeutic co-development potential, and possible acquisition target, I believe this is a name worth holding on to.

Be the first to comment