The oil price discussion has become extremely polarizing – even more than it already was. If we forget the environmental aspect (i.e., ESG) of it all, we’re dealing with a strong bull case based on a very tight supply. The bear case is mainly focused on demand weakness as we’re currently dealing with a rather steep decline in global growth expectations. I have been in the “supply camp” since 2020, as I believe that we’re in a new era for energy companies. I’m not just saying that because it sounds fancy, but because what we are facing is a situation where companies are not willing to drill. Oil companies would rather spend money on buybacks and dividends, which makes sense as it not only lowers long-term risks by keeping a lid on oil supply but also benefits energy investors, which includes most executives. As these are things that I have discussed frequently since 2021, I’m going to add something that truly worries me. OPEC is expected to cut oil supply even more than previously expected based on economic growth worries. At the same time, Saudi Aramco executives warn that the world is not prepared for a post-COVID scenario if China opens up again. I agree and believe that investors who don’t own energy should consider adding some exposure.

Hence, on top of a macro discussion, I’m going to present you with two stocks that I believe suit every portfolio.

So, let’s get to it!

The Supply Argument (The Big One!)

Someone once told me that it’s always about supply and never about demand. It’s partially true because if we follow basic human tendencies to accumulate as many things that we consider to be valuable, we’re only limited by supply. Supply of money, supply of goods, and whatnot.

Even the Fed’s entire policy is based on the supply side as it influences the price of money.

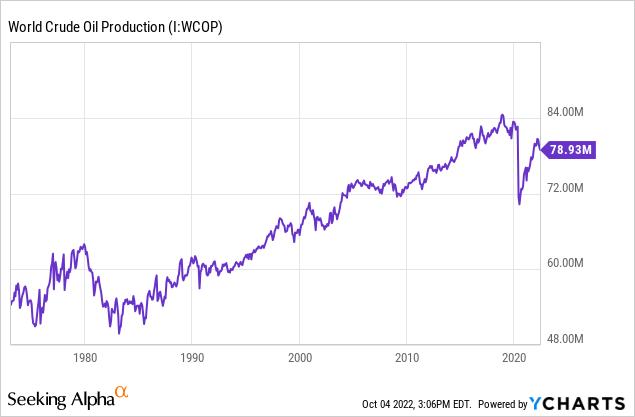

In the case of energy, we’re dealing with global oil production. Global oil production has steadily increased as a result of rising demand and new technologies. Over the past 40 years, we’ve witnessed steady growth in developed countries as well as the massive transformation of China from a somewhat passive player to an economic powerhouse. The same goes for other emerging markets that have caused demand for crude oil to soar. In the 1990s, global crude oil production rose from roughly 60 million barrels per day to almost 70 million barrels per day. This number steadily rose until it hit 84 million barrels prior to the pandemic. Since then, oil production has fallen. Even the rapid post-pandemic recovery did not result in higher oil prices.

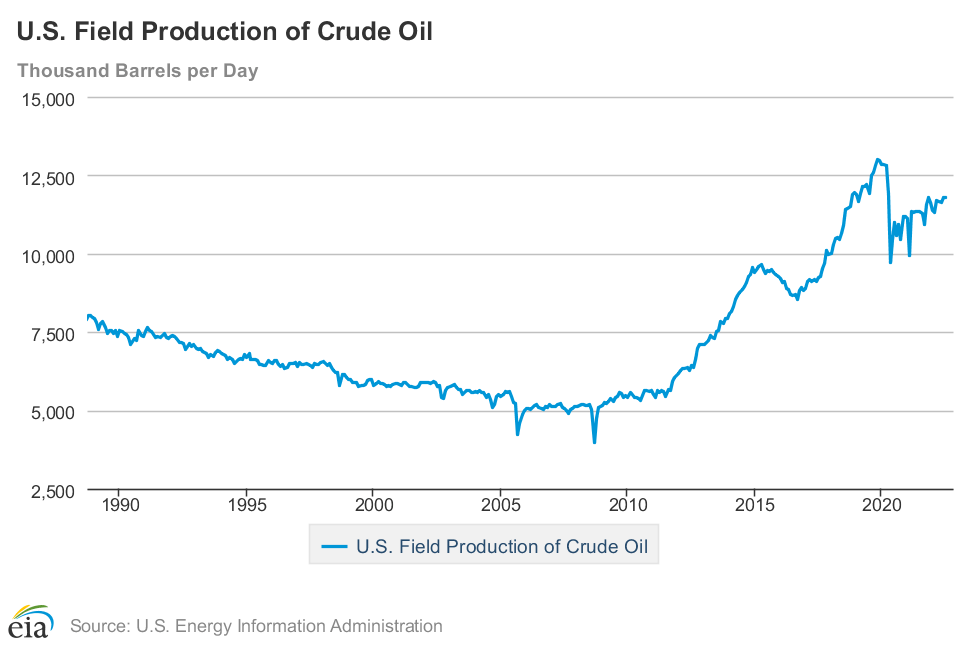

The chart below shows crude oil production in the United States. Prior to the Great Financial Crisis, the US was a net importer of energy, producing close to 5 million barrels of oil per day. That quickly changed thanks to the shale revolution, which used horizontal drilling techniques to improve drilling operations. It resulted in a massive surge to more than 12.5 million barrels of oil per day before we got the bad news out of Wuhan in 2020.

EIA

Since then, oil production has not recovered. And as I already showed global production, the same goes for other nations as well.

We’re not just dealing with the inability of some producers to hike production because of labor and material shortages (that’s a huge issue in some areas), but mainly because of the unwillingness to improve production.

See, prior to 2021, oil producers created their own misery. They boosted production to make more money. This boosted supply so much that even a slight dent in demand would cause oil prices to plummet. In 2020, it even caused WTI crude oil futures to turn negative because there was no more storage available.

On top of that, governments and NGOs have accelerated their efforts to suppress fossil fuel growth for environmental reasons. I explained that in this article.

Basically, energy companies know they shouldn’t expect any support during the next recession. After all, their death is what fits the ESG agenda, to put it very bluntly. Hence, producers have started to focus on free cash flow to repair their balance sheets and distribute cash to shareholders. They don’t care for production growth anymore. And as much as I hate getting gas at these prices, I cannot disagree with the logic of that.

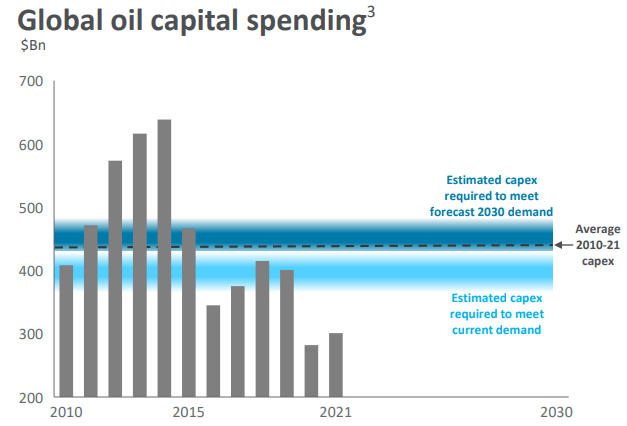

While the chart below does not include 2022, it shows that the 2015 oil price crash already caused a scenario where global oil production spending was not sufficient to meet expected 2030 demand.

Seeking Alpha

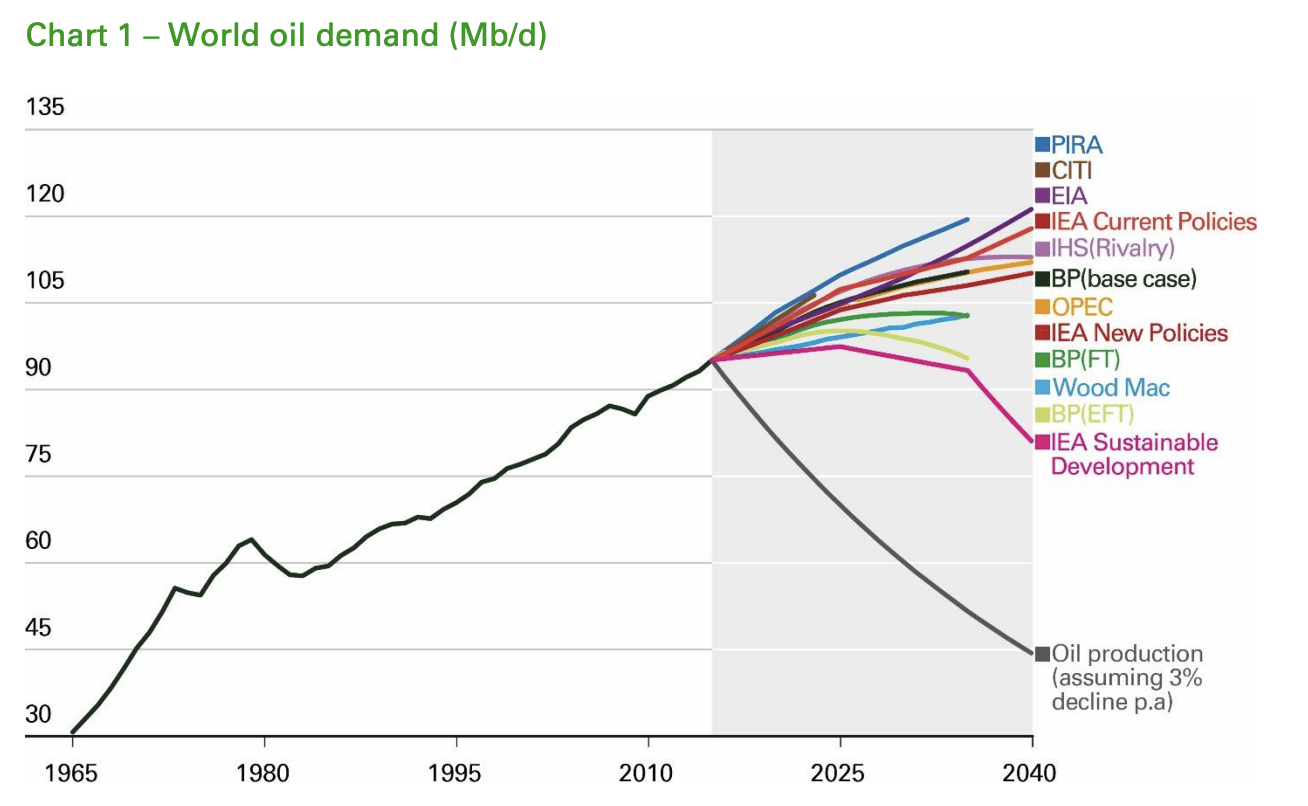

After all, this is what long-term demand looks like. Even a base case would mean we’re dealing with a long-term demand uptrend to roughly 110 million barrels per day by 2040. Only very ESG-focused scenarios see a decline. I respectfully disagree with that as I do not see a scenario where renewables can compete with fossil fuels. Especially not as emerging markets will need reliable and affordable energy to grow their middle class – among many other reasons.

British Petroleum

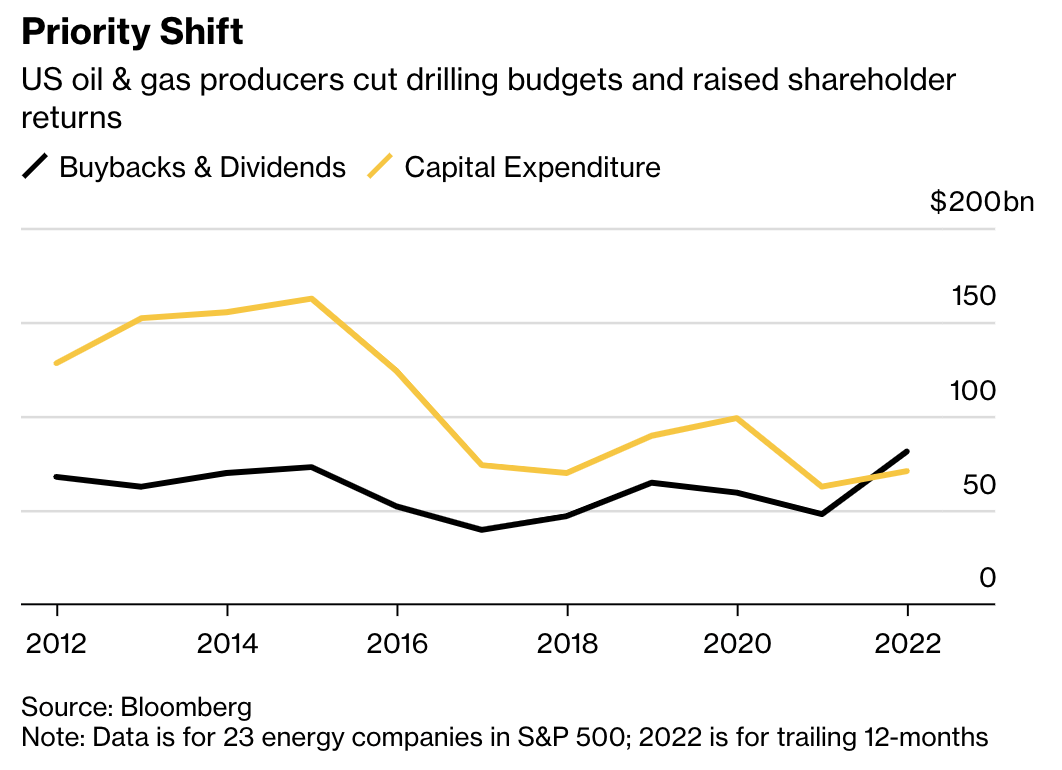

The worst part – for the consumer – is that we’re not about to see a reversal. While the energy CapEx chart above wasn’t updated, the one below is.

The 23 energy companies of the S&P 500 (“big oil”) are now spending more on buybacks and dividends than capital expenditures. This confirms everything we have discussed so far. It’s a truly wild development given that there’s a need for more supply.

Bloomberg

Now, things are getting worse. While we will continue to talk about supply, I’m going to use a new header as we need to discuss geopolitics.

OPEC & Political Fears

Over the past few weeks, we have talked a bit about OPEC in various articles. OPEC hates that oil prices have become very volatile and discussed various strategies to control volatility and total financial interest in oil transactions.

Now, they are likely going to take it a step further – a big step. OPEC+ is considering its biggest production cut since 2020. According to Investopedia:

(OPEC+) is a loosely affiliated entity consisting of the 13 OPEC members and 10 of the world’s major non-OPEC oil-exporting nations.

The group is considering an output cut of as much as two million barrels per day. On the one hand, it sounds worse as a lot of OPEC+ countries are already producing below their targets. On the other hand, OPEC discussing cuts in an environment where the American producers aren’t hiking their output for sure is a problem.

A milder, one million to 1.5 million barrels production cut is also on the table. However, even that is freaking out politicians, and rightfully so.

“It is hard to overstate how anxious the Biden administration is about a potential resurgence in oil prices,” Bob McNally, founder of Rapidan Energy, said in Vienna. “A large OPEC+ cut would antagonize the White House though officials may wait to see how prices respond afterward before pulling the trigger on policy responses.”

What we are dealing with here are political games. It’s Netflix’s House of Cards, just real and way more intense. President Biden’s visit to Saudi Arabia earlier this year in search of a new oil deal has turned out to be a total waste of time. Now, US politicians are looking into a reduction of gasoline, diesel, and other refined products, which I believe is one of the worst ideas ever given that these exports are now needed in Europe and elsewhere – especially in light of the energy crisis.

Now, I’m hearing from my contacts that the US Treasury is trying to pressure various OPEC countries with economic sanctions to halt these production cuts. The Democrats cannot risk higher energy prices, even if it is just to get gasoline prices down before the Midterm elections this year.

And, on top of that, the situation is getting very dire.

The headline below really had an impact on me as I believe it’s even more important than the OPEC news.

Bloomberg

Essentially, the world’s largest oil producer is warning that spare capacity will be completely depleted once China ends its zero-COVID strategy – as spare capacity is already low. While we can debate how long China will stick to its strategy, the fact that fierce Chinese lockdowns prevent oil from exploding is not a sustainable strategy, to put it mildly.

Hence, as Bloomberg reports:

“The world should be worried,” Saudi Aramco’s Chief Executive Officer Amin Nasser said at a conference in London. “This is where we are heading. If China opens up a little bit you will find out that spare capacity will be eroded completely.”

It’s also important to note that the Saudis are criticizing the Americans – and Western governments – for their stance on fossil fuels. I believe this is a reason why OPEC won’t be the force to bring back supply. Why should they bring back the oil supply to bail out Western governments?

What I find to be extremely interesting is that there are about two million barrels per day of capacity that could be brought online to prevent supply shutdowns.

That’s exactly the number OPEC wants to take off the table.

In other words, OPEC is actively looking to maintain a tight market for political reasons. Given complex geopolitical developments, we can debate about its motives, but regardless of how we look at it, it’s bad.

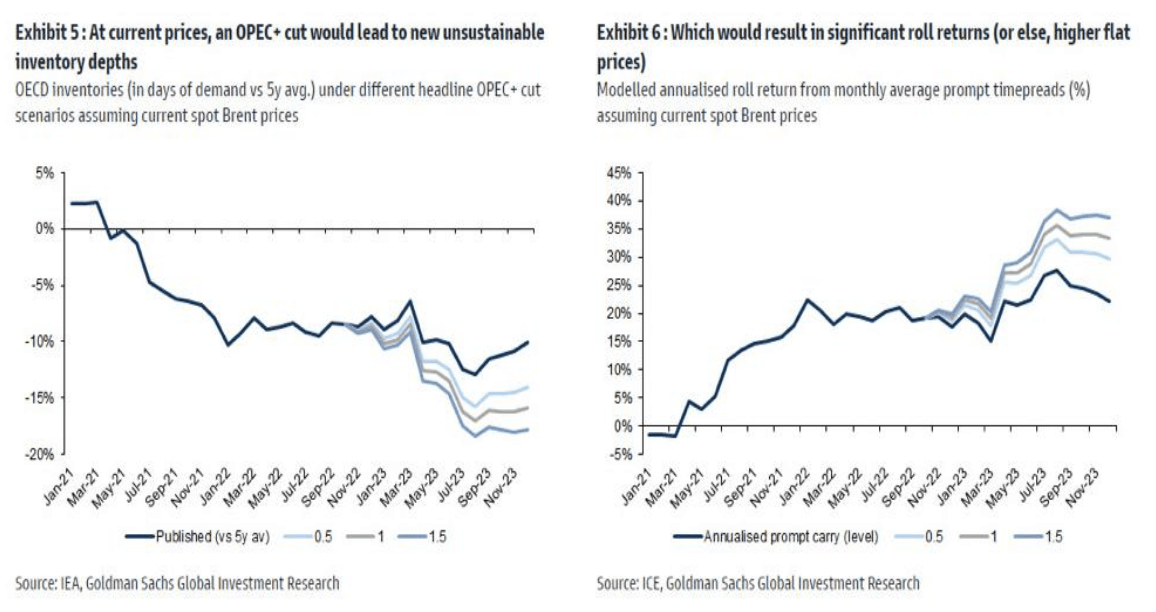

This is how bad it could be according to Goldman Sachs:

Goldman Sachs

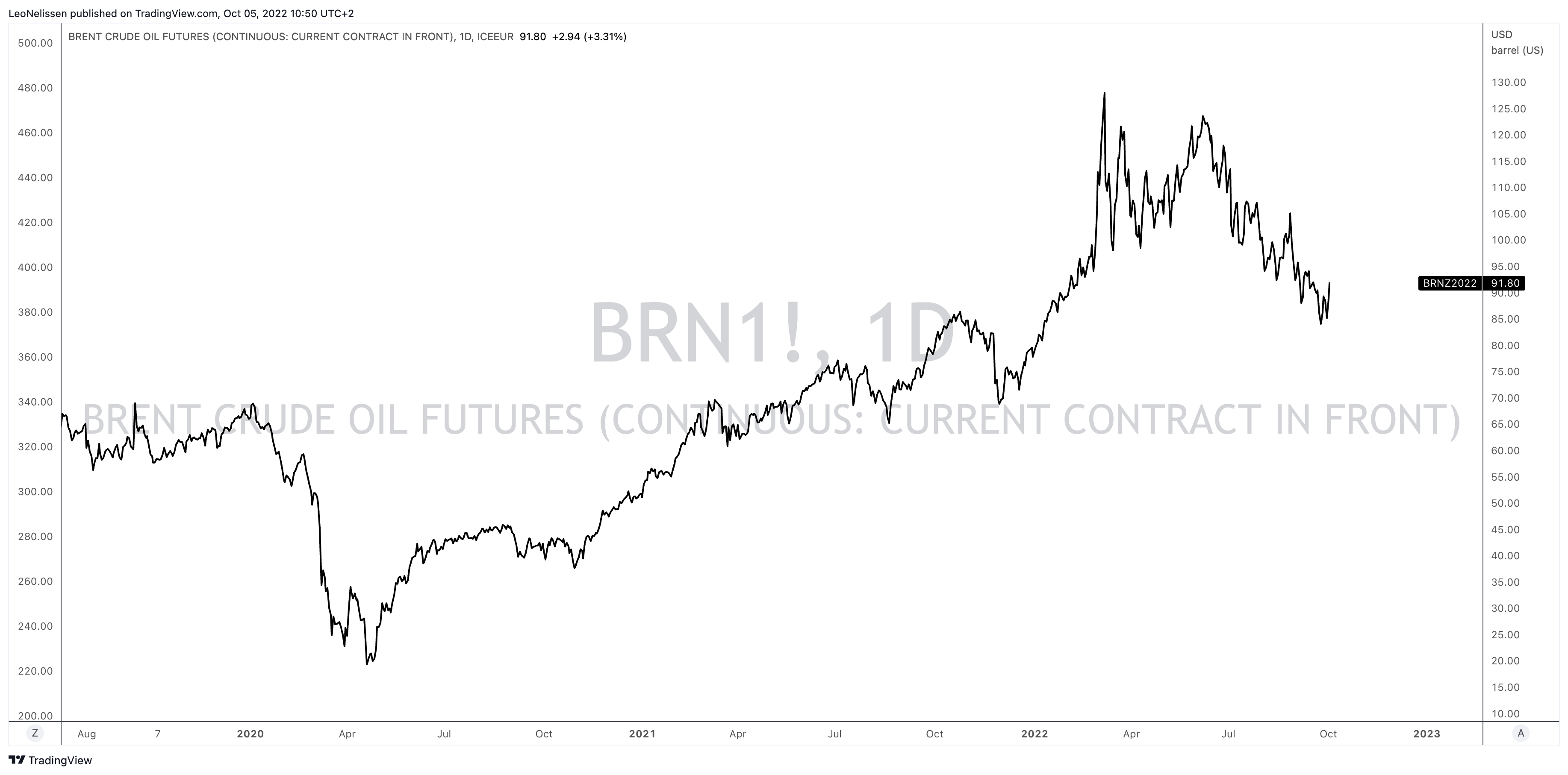

The timing is also interesting. Brent crude has lost roughly a third of its value since early June of this year. While Brent didn’t fall below $80, it’s still a considerable decline, driven by demand fears.

TradingView (ICE Brent)

In a recent article, I discussed growth slowing and the role of the Fed in fighting inflation. The economic indicator ISM manufacturing index came in very weak earlier this month, which is set to continue unless rates start to drop.

Wells Fargo

If we ignore an already tight market, it does make sense to cut output into an economic growth slowing trend. However, the risks of oil exploding higher when demand expectations rebound are very high.

In other words, oil can continue its decline as economic growth is in a very bad place. However, I remain in the bullish camp as I buy energy stocks on a long-term basis for capital gains and income. My bull case keeps growing as supply is even worse than I expected. Hence, even if oil doesn’t rally immediately, I think that we will see the start of a rally to $120-$130 as soon as the Fed starts to pivot, which could be in early 2023.

So, in addition to a lecture on supply and OPEC, I’m including two oil picks in this article, and I own both. On top of that, my articles combining macro and actionable ideas were very well received (thanks for that, btw!). Hence, I will try to focus a bit more on articles like this one.

With that said, I have close to 20% energy exposure between my dividend (growth) portfolio and my trading account. While I do not hope that my bull case turns out to be correct (it would be a huge headwind for the consumer), I think it will happen as expected. So, why not benefit from it?

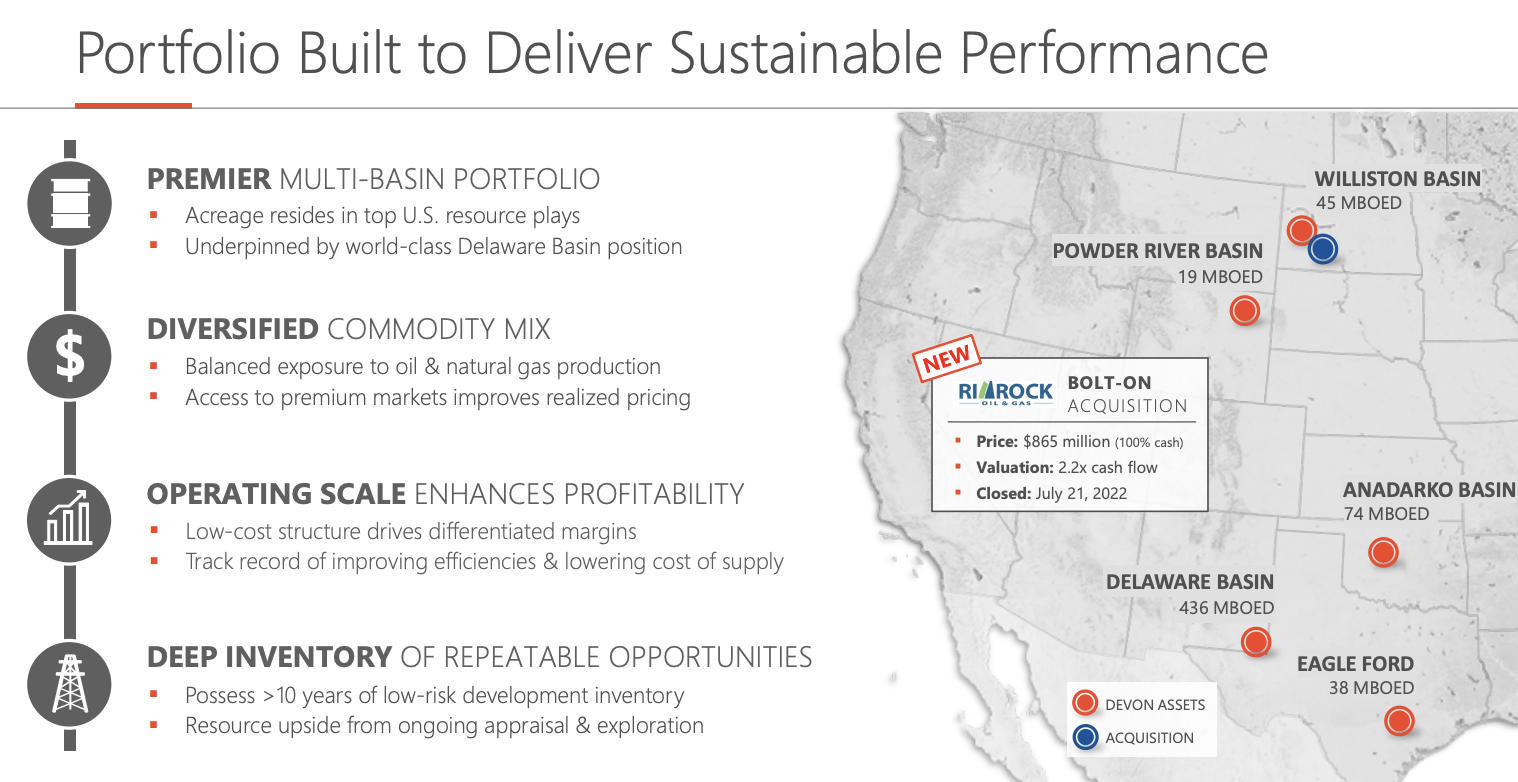

Devon truly has it all. With a market cap of roughly $45.2 billion, the company is one of America’s largest onshore oil producers with assets in the famous Delaware Basin, Texas’ Eagle Ford, as well as the Williston Basin, Powder River Basin, and Anadarko.

Devon Energy

In 2Q22, the company produced roughly 616 thousand BOE (barrels of oil equivalent) per day. Roughly half of that came from oil. The other half consisted of natural gas and natural gas liquids.

On top of offering both natural gas and oil, the company has a very low breakeven price. Devon Energy is cash flow breakeven at $30 WTI. That’s the lowest breakeven price I have ever covered – and I have covered a lot of companies.

The company has also hedged just 20% of its production.

What this means is that the company is able to generate a lot of cash when oil prices are high. It loses very little money on hedges and benefits from very efficient operations that even allow the company to make money at prices we usually only see during steep recessions.

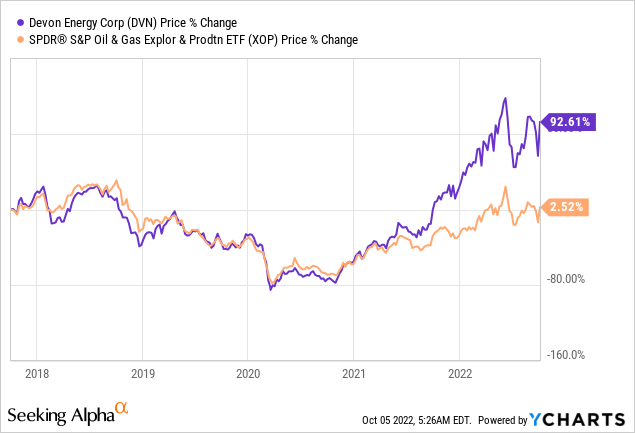

Thanks to these characteristics, the company not only consistently outperformed its peers since the 2020 oil bottom as the chart below shows, but the company’s cash flow priorities have shifted to a fixed and variable dividend, share repurchases, and balance sheet health – in that order.

The company has no major debt maturities above $600 million in the future, $6.5 billion in available liquidity, and $3.5 billion in cash.

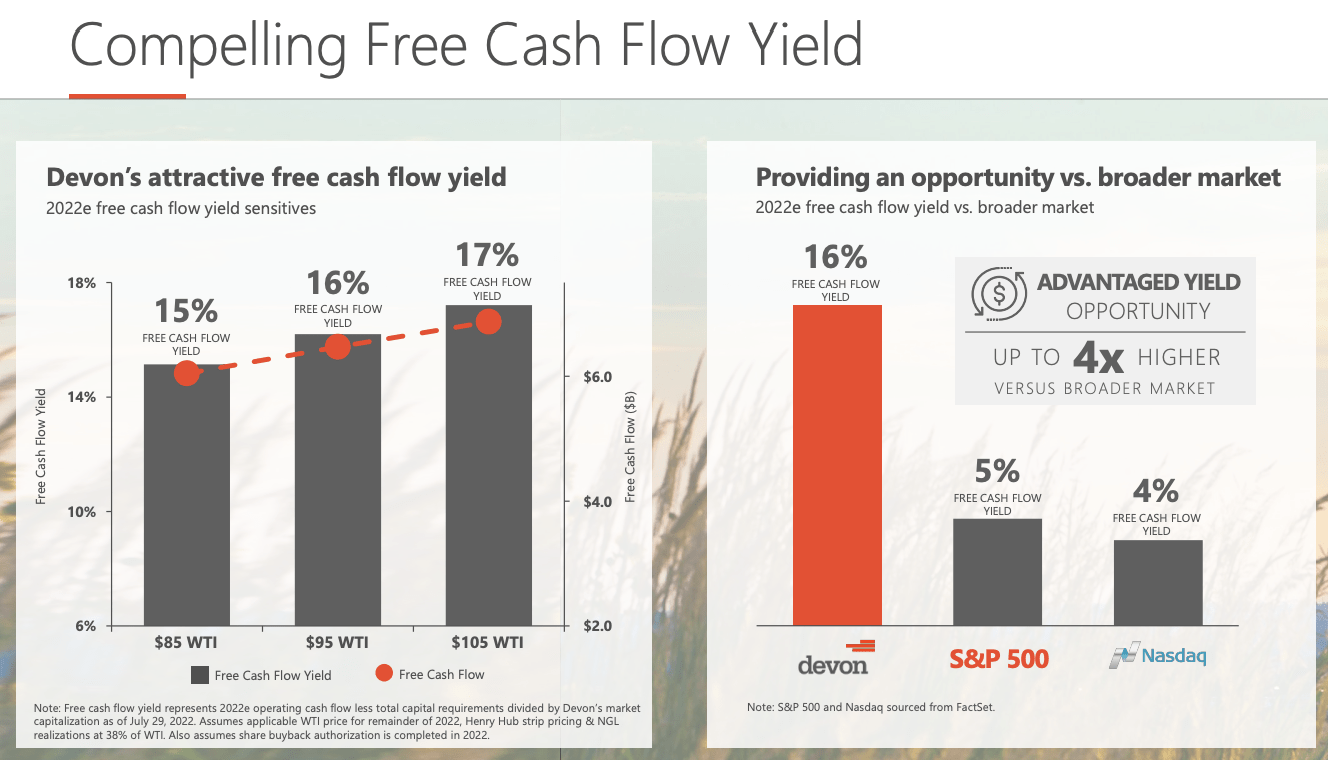

Using the company’s stock price on July 29 (low $60s), the company generates a free cash flow yield of 17% at $105 WTI. We’re currently far away from that, but even at $85 WTI, it’s a high, double-digit number. As the company’s balance sheet is healthy, one can imagine what this means for (expected) dividends at these oil prices.

Devon Energy

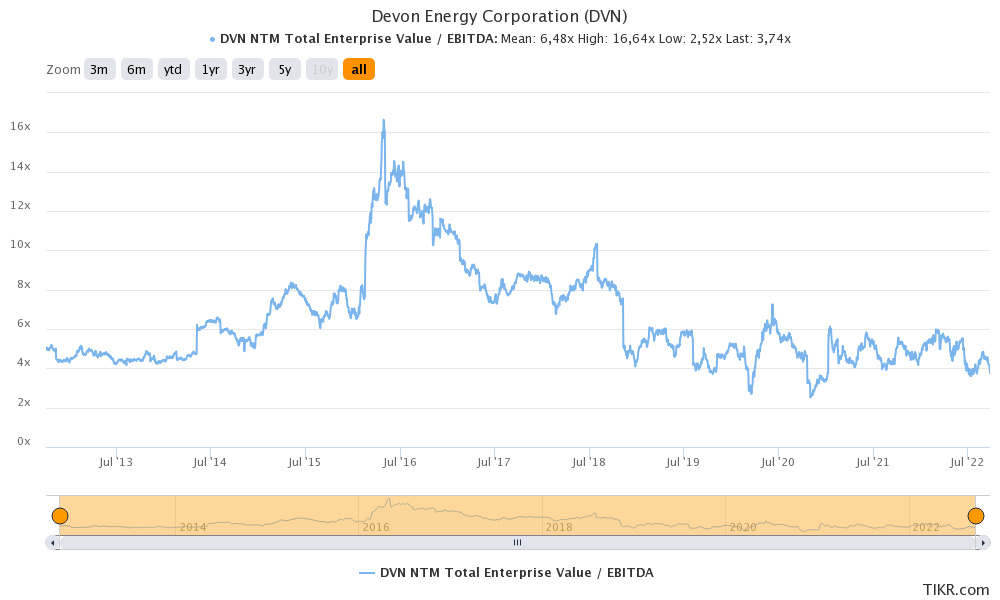

Valuation-wise, the company remains very attractive. DVN is trading at 4.7x 2023E EBITDA of $10.3 billion based on its $41.0 billion implied enterprise value. This enterprise value consists of its $45.2 billion market cap, $2.6 billion in expected net debt, and $570 million worth of pension-related liabilities and minority interest.

TIKR.com

I believe that even a 6x NMT EBITDA valuation would be fair.

Stock number two is a lot less volatile and much, much bigger. It’s a company I bought in 2021 with the proceeds from an agriculture trade because I wanted consistently growing energy dividends backed by a well-diversified portfolio and a long track record of great performance throughout cycles.

With a market cap of $309 billion, Chevron is playing in a different league than Devon. The company has upstream and downstream assets, which means global drilling and refinery operations. The company also engages in renewables as it slowly but steadily expands into hydrogen, renewable fuels, and related projects. However, the company does not go all-in on renewables as some of its European peers. I believe that is not the way to go given my long-term view on oil.

If anything, it seems that the company is making investments in “new” technologies to satisfy potential threads of activist investors like Engine No. 1.

ESG pressures have forced the supermajors to shrink their upstream businesses. Other consequences are now emerging as well. Large sums are being redirected away from the traditional upstream businesses, which sport extremely high energy efficiency, into renewables which are much less efficient.

Nothing demonstrates this better than what Chevron did back in February. Rattled by Engine No. 1’s Exxon success, Chevron committed to invest $10 bn to reduce its carbon emissions through 2028 and be completely carbon neutral by 2050. As a first step, Chevron announced the acquisition of Renewable Energy Group, an Iowa-based producer of biodiesel and renewable diesel, for $3 bn.

Chevron will remain an oil-focused player for decades with what I believe will be a continuation of past outperformance.

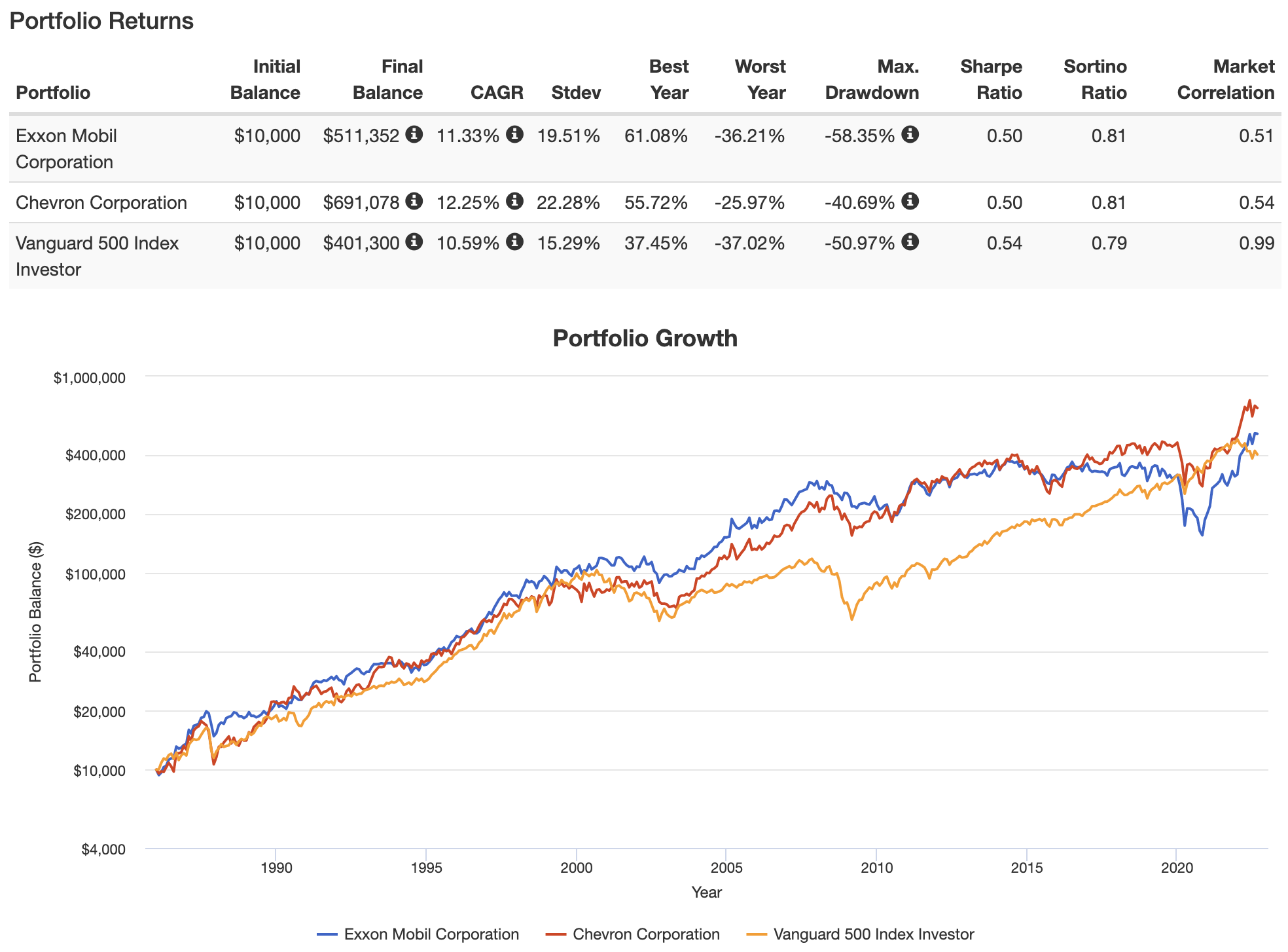

Going back to 1986, Chevron has returned 12.3% per year, including dividends. This beats XOM by almost 100 basis points. The standard deviation during this period was 22.3%. The S&P 500 returned 10.6%, with a low standard deviation, which makes sense as it’s a basket of stocks and less cyclical than energy. Yet, Chevron was still able to beat the S&P 500 on a volatility-adjusted basis (Sortino ratio).

Portfolio Visualizer

Moreover, while commodity stocks, in general, lost momentum in 2011, Chevron still has returned 7.9% per year during the past 10 years. That’s more than 250 basis points above the annual average performance of Exxon Mobil.

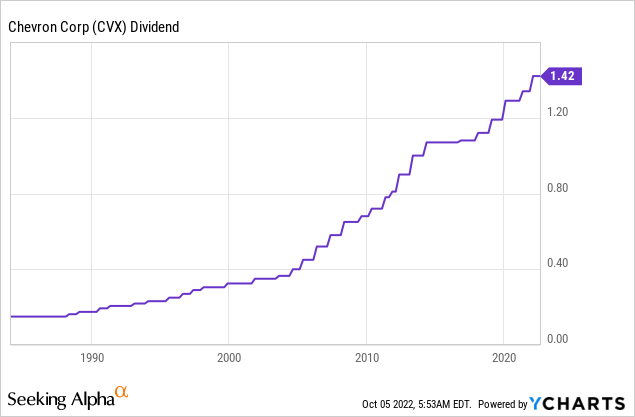

The company is also a very reliable dividend stock. Using the Seeking Alpha dividend scorecard, the dividend aristocrat scores an A+ on consistency, and an A- on growth.

Over the past 10 years, the average annual dividend growth rate was 5.1%. That’s not a bad number as we’re dealing with a high-yielding stock.

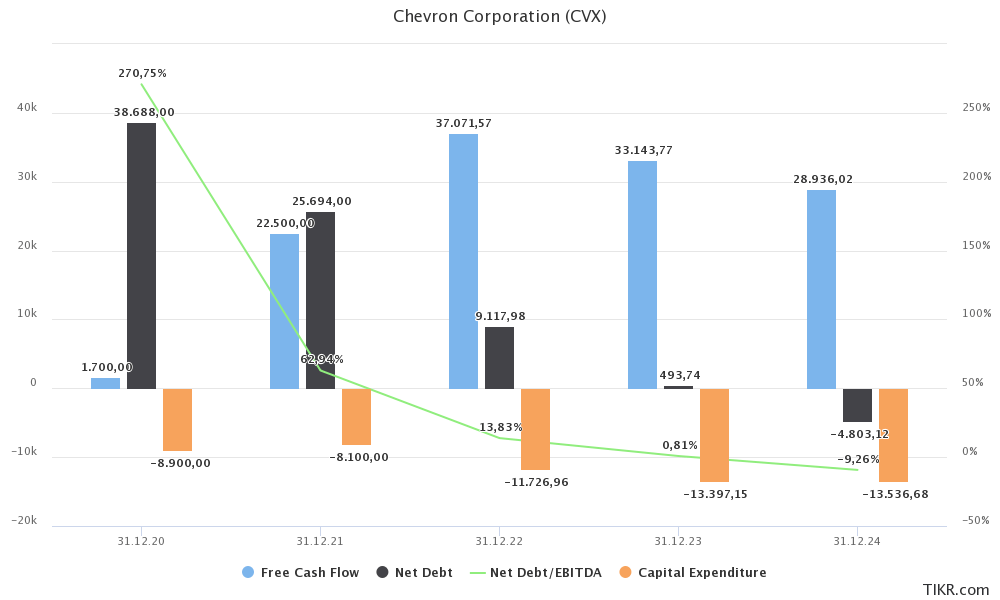

However, I expect dividend growth to pick up as the company is now in a position where it can accelerate free cash flow while maintaining steady CapEx. Things are looking so good that net debt is expected to turn negative in the future. That likely won’t happen due to share repurchases (which is even better), but it shows how much potential this company has.

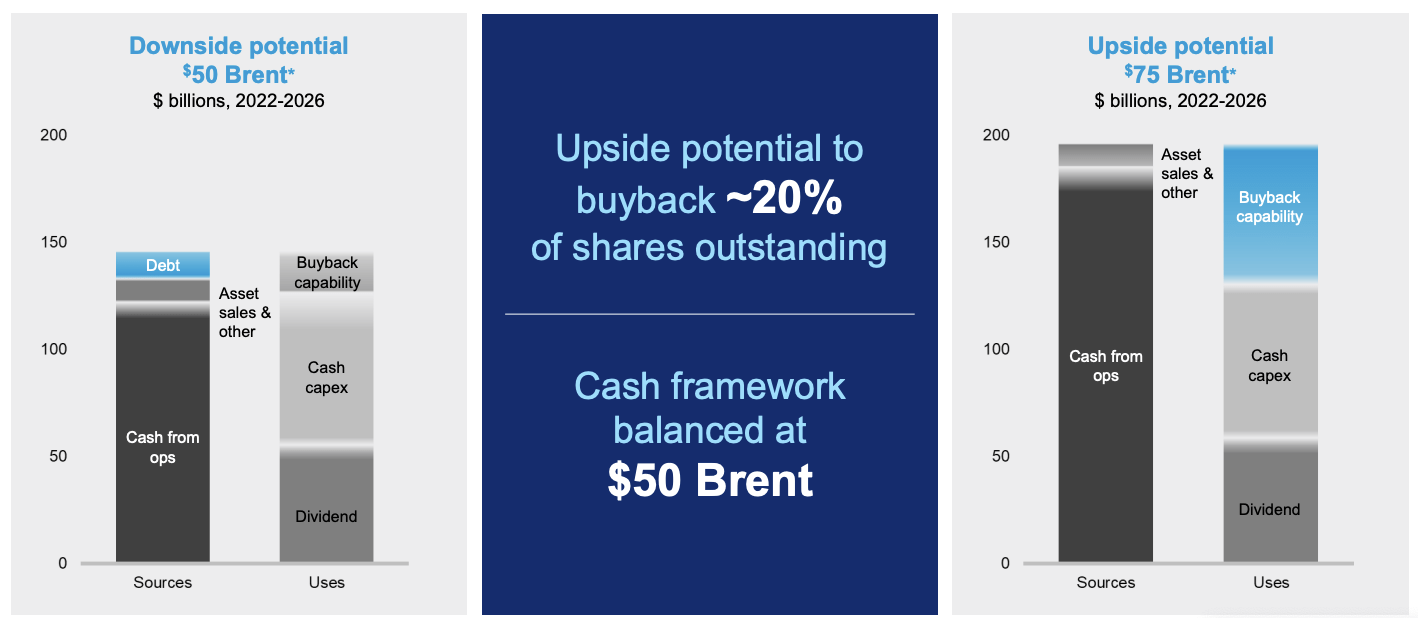

What’s interesting is that at $75 Brent, the company can do $40 billion in annual operating cash flow (almost $200 billion in total until 2026). This sustains the dividend, investments in operations, and buybacks equal to dividends. At a current rate, that implies more than 7% in annual shareholder distributions, which is truly impressive. Now, imagine if oil remains consistently close to $80-$90 billion. The impact would rise significantly given consistent CapEx plans.

Chevron Corporation

It also helps that the company has an AA- debt rating, which makes it more secure than a lot of developed countries.

When it comes to the valuation, the company is attractively valued, trading at just 5.1x 2023E EBITDA of $62.0 billion based on its $315.6 billion enterprise value consisting of the $309 billion market cap, $1.0 billion in minority interest, and $5.6 billion in pension-related liabilities. Net debt is expected to be negative next year, so I made that a zero in my calculation.

Hence, my opinion is still that CVX is at least 30-40% undervalued from “fair value”.

Takeaway

Despite demand fears, the long(er) term bull case for oil isn’t weakening. If anything, new political issues and findings regarding emerging market demand make the supply situation even worse. OPEC is already producing less than it expected and is now about to cut expected supply even further, making it extremely unlikely that the world will see a major upswing in oil supply unless the economy runs hot. An economic rebound is unlikely until at least 2023 as central banks are busy fighting inflation – hurting growth in the process.

If the Fed pivots and China somewhat eases its strict COVID policies, we’ll likely encounter an oil rally beyond $120 per barrel.

The only thing that could solve this issue is if Western governments were to change their view on fossil fuels. Yes, less pollution is great, but “we” cannot force oil and gas companies to reduce output as it created the situation we’re in now. Unfortunately, I do not expect that to happen, which is why it is important to own energy exposure to protect a portfolio against inflation.

That’s the reason why I presented two stocks in this article — Devon Energy and Chevron. Devon is smaller but leaner and more efficient. If oil rallies again, Devon will be a source of sky-high dividends.

Chevron is larger. Its yield is lower. Yet, the company has been the backbone of many high-yield portfolios for a good reason. It has a reliable and decent yield, and a lot of room to accelerate shareholder value for (what I believe to be) decades to come.

However, as bullish as all of this sounds, please do not go overweight energy and be aware of the risks that come with owning very volatile assets. Demand risks are still high, and we could see another leg down before the long-term bull case continues to unfold itself.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment