Hill Street Studios/DigitalVision via Getty Images

Co-produced with Treading Softly

Few things in life last forever.

Every car has an expected expiration date. Blue jeans only last so long before they fall apart. We can often be heard saying that “they just don’t make things like they used to” and I would agree. Many items are more effective at completing the task required but lack the strength to complete the task nearly as long as the tools we used to use.

With tighter clearances, lighter materials, and the focus on mass production vs. hand-fitting components, longevity is hard to find.

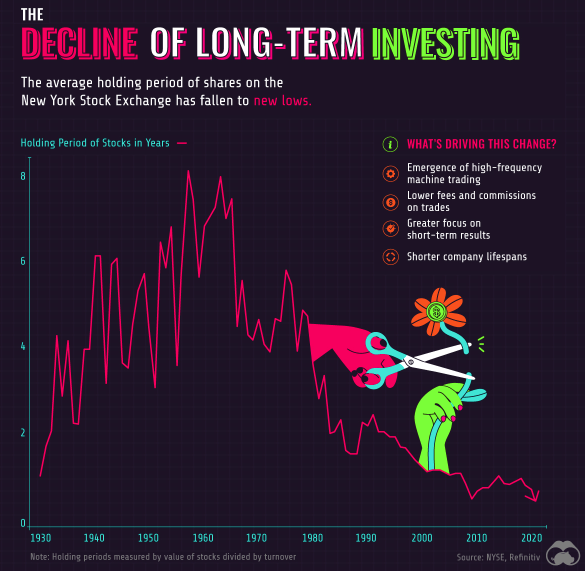

So when it comes to the market, it is no surprise to see the average holding period of an investor has declined as well.

Visual Capitalist

As this image shows, the average holding time of investors has fallen below a year. Yup, most of us don’t hold on to an investment for 365 days. This is a massive contrast to when investors held for nearly a decade.

So when I say that we aim for at least 2-3 years for our investments, we’re tripling the holding time compared to many. No wonder commenters think one week later is a good time to evaluate results! However, that is not our method or focus, we are long-term investors.

It is an even rarer occurrence when I can say I have some investments in my portfolio which will outlast me. They will be fought over by my heirs and hopefully their heirs as high-quality income investments.

These can be owned, held, passed down, and continue to provide an excellent level of high-quality income “forever”.

Let’s dive in.

Pick #1: RLJ-A – Yield 7.5%

Investors often try to divine the “whys”. Like staring at a Rorschach test, investors will stare at price movements and see various different shapes. Ask a dozen gurus, you’ll get a dozen different answers. Should you buy? Should you sell? Will the market fall more? Will there be a reversal?

On any given day, I can find very well-respected investors with very respectable track records that are on different sides of these questions. Which one should you believe?

Well, if your plan is to sell next month, I recommend consulting a Magic 8-Ball. The market will go up, or it will go down, it will probably bounce around. It will reverse, reverse again, dive off a cliff, climb a mountain, do a few loops, and through all of this ultimately end up higher.

Some might call me a “perma-bull”. I invest in the market because, at its core, it represents the economic production of the world. Economic production trends up in the long run. That’s why we aren’t all still living in caves and hunting for a living. Are people going to be wealthier next year? That’s a difficult and complex question. Are people going to be wealthier 20 years from now? The answer is an absolute yes with very little doubt. If I didn’t believe that, I wouldn’t put my hard-earned funds in the market.

Now I’ve lived through a lot of recessions, and even a few depressing ones. Well, I wasn’t depressed, but I saw many around me who were as their portfolios were down 20, 40, 60%+. What keeps my spirits up? My income.

At all times, I have core holdings that I know I can absolutely count on to maintain their dividend through thick or thin. Among those, I count RLJ Lodging Trust, $1.95 Series A Cumulative Convertible Preferred Shares (RLJ.PA) – paying $1.95/year in income rain or shine. RLJ is a hotel REIT.

If I were to construct an apocalyptic scenario for hotels, it might look a lot like a global virus that led to entire sectors of the economy being shut down. Travel would be severely restricted, international border crossings would decline to near zero as people were told to shelter in place and to go nowhere they absolutely didn’t need to go.

Crazy Sci-fi movie stuff right? Certainly, if I had predicted that in 2019, folks would have called me a nut, but would have agreed that was about a worst-case scenario as could be imagined for RLJ.

Well, it happened. What happened to RLJ-A in 2020? $1.95 per share, deposited into my portfolio in quarterly installments, and not one dividend was even a single day late.

RLJ inherited RLJ-A through the acquisition of a weaker peer, Felcor, that was negatively impacted by the Great Financial Crisis. Felcor survived, but was forced to do some reverse splits. When RLJ bought out the company, it inherited RLJ-A, which is a convertible preferred with no call option. RLJ can’t call it, and conversion into common shares can’t be forced unless RLJ common is trading above $115.82/share. Unlikely to happen, but if it does, we probably won’t mind owning RLJ common anyway because something is going really right!

The bottom line is that RLJ has no way to get rid of RLJ-A, other than trying to buy it in the public markets. It is one of those rare preferred that you can buy and hold forever.

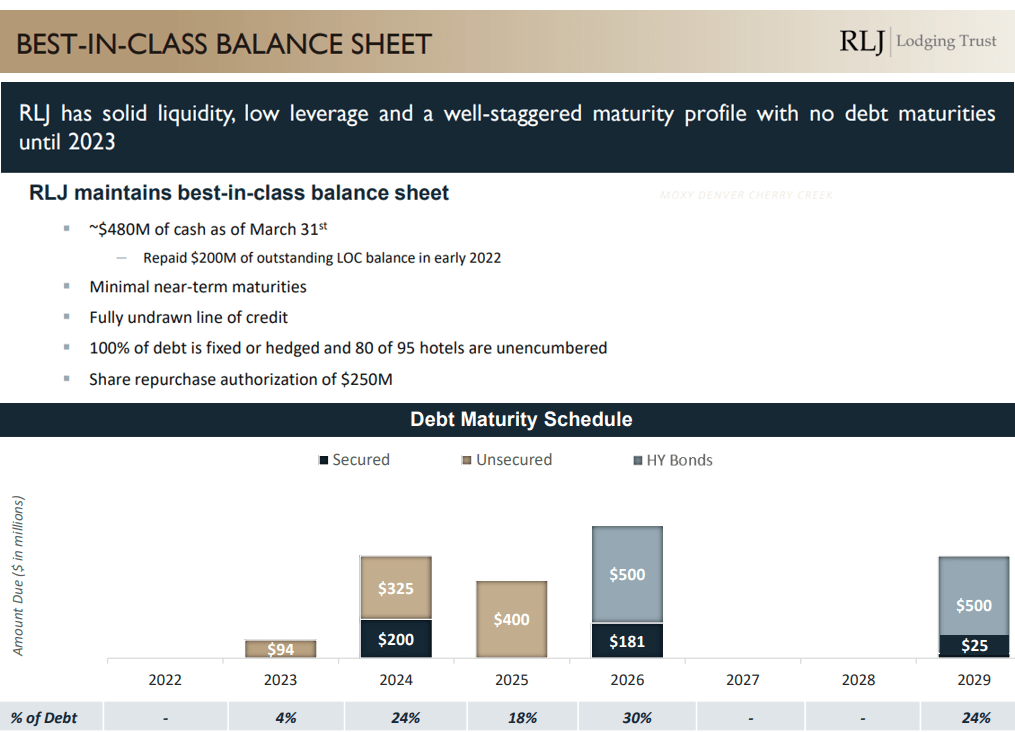

When it comes to hotel REITs, RLJ is the cream of the crop. What matters most for the preferred shares, is their very strong balance sheet and conservative debt profile. (Source: NAREIT Presentation)

NAREIT Presentation

RLJ has $480 million in cash on hand, and no debt maturities larger than that until 2024. Including its undrawn line of credit, RLJ has $1.1 billion in liquidity.

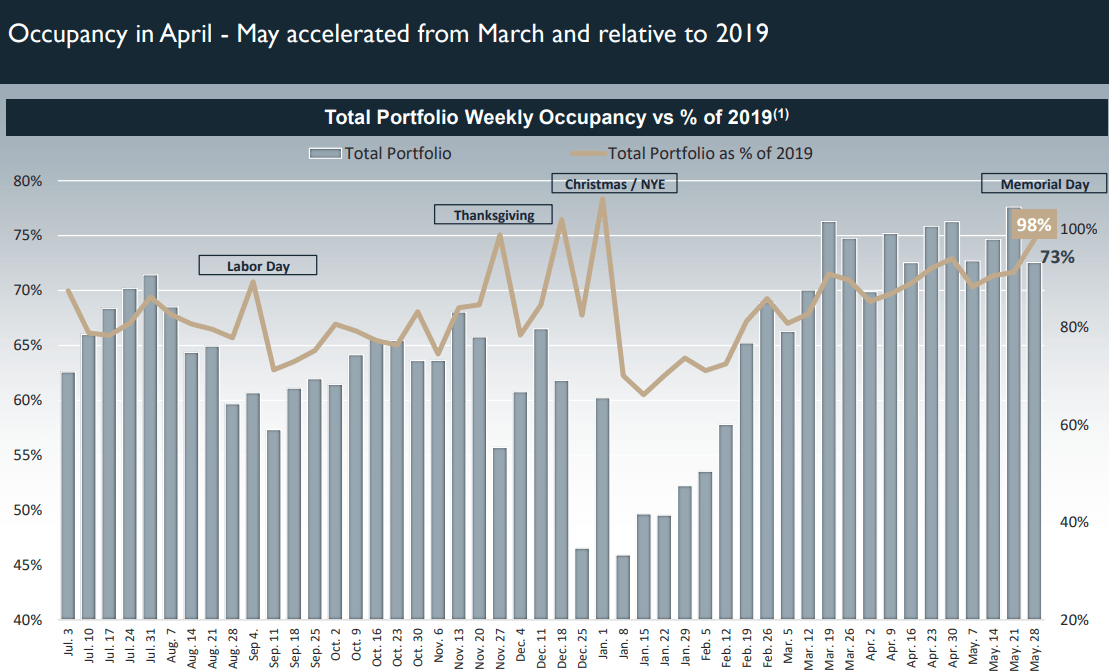

Along with this strong balance sheet, RLJ’s operations are recovering, aided by an ADR (average daily rate) 15% higher than it was in 2019.

NAREIT Presentation

Occupancy is still slightly lower at 98% of 2019 levels but is stabilizing. Overall, RLJ expects EBITDA will be higher in 2022 than it was in 2019.

When we invest in fixed-income, what we are really looking for is the security of knowing that our dividend will come in no matter what. COVID put hotels to the harshest test imaginable, and RLJ-A didn’t miss a beat. It’s hard to imagine an even worse scenario, but even if the world conjures up something we can’t imagine right now, RLJ-A is backed by a high-quality portfolio, high-quality management, and a strong balance sheet.

For these reasons, when RLJ-A starts trading near $25, I snag a few more shares. Someday, a recession will come, and when it does, I’m confident RLJ-A will be paying me $1.95/share every year.

Pick #2: CEQP-, Yield 9.2%

Crestwood Equity Partners LP, 9.25% Preferred Partnership Units (CEQP.PR) is one of my favorite preferred shares on the market. Why?

CEQP– is a preferred investment that was developed by institutional investors when the market for natural gas was really tough. As a result of these tough negotiations, CEQP- has numerous protections that are not typically seen in preferred shares available to retail investors. These include:

- No call provision: CEQP- is convertible but the company cannot force conversion until the common shares close above $136.91 for 20 out of 30 consecutive days. CEQP- is a “busted” convertible due to a reverse split.

- Voting rights: Preferred shareholders often do not get to vote on most issues. CEQP- preferred shareholders get to vote on everything the common shareholders do. What is especially crucial is that preferred investors get to vote as a separate class on changes of control. This ensures that if CEQP is ever acquired, it will be at favorable terms for the preferred.

- Missed distribution penalties: Many preferred are “cumulative” in that if a distribution is not paid, it accumulates and has to be paid in full in the future before the common units can receive distributions. CEQP- goes a step further and implements a penalty. If a single distribution is missed, the distribution immediately increases 22% to $0.2567/quarter. Plus, any accrued and unpaid distributions will be increased 2.8125% each quarter. These penalties ensure that management has a very strong incentive not to miss a distribution.

What does this mean in practical terms? It means that we can buy and hold CEQP- indefinitely, as the company cannot call it. The only option Crestwood (CEQP) has is to buy the shares in the open market. Too bad for CEQP, I’m not selling.

It also means that preferred shareholders can’t be unexpectedly ambushed with a sale of the company. If CEQP decides to sell the company, preferred shareholders get to vote after seeing what compensation they will receive, this is a rare benefit.

Finally, CEQP has a lot of incentive to stay current on the distribution. A distribution cannot be made to the common units unless the preferred payments are made in full. If CEQP suspends the preferred for even a single month, that obligation increases and starts accruing a penalty. For an MLP, paying a common distribution is quite important. So we don’t believe that CEQP would ever suspend the distribution lightly, but if we ever are inconvenienced and a payment is missed, it is nice to know we’ll be well compensated for the inconvenience.

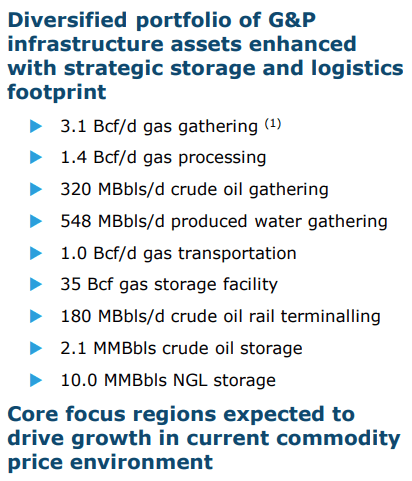

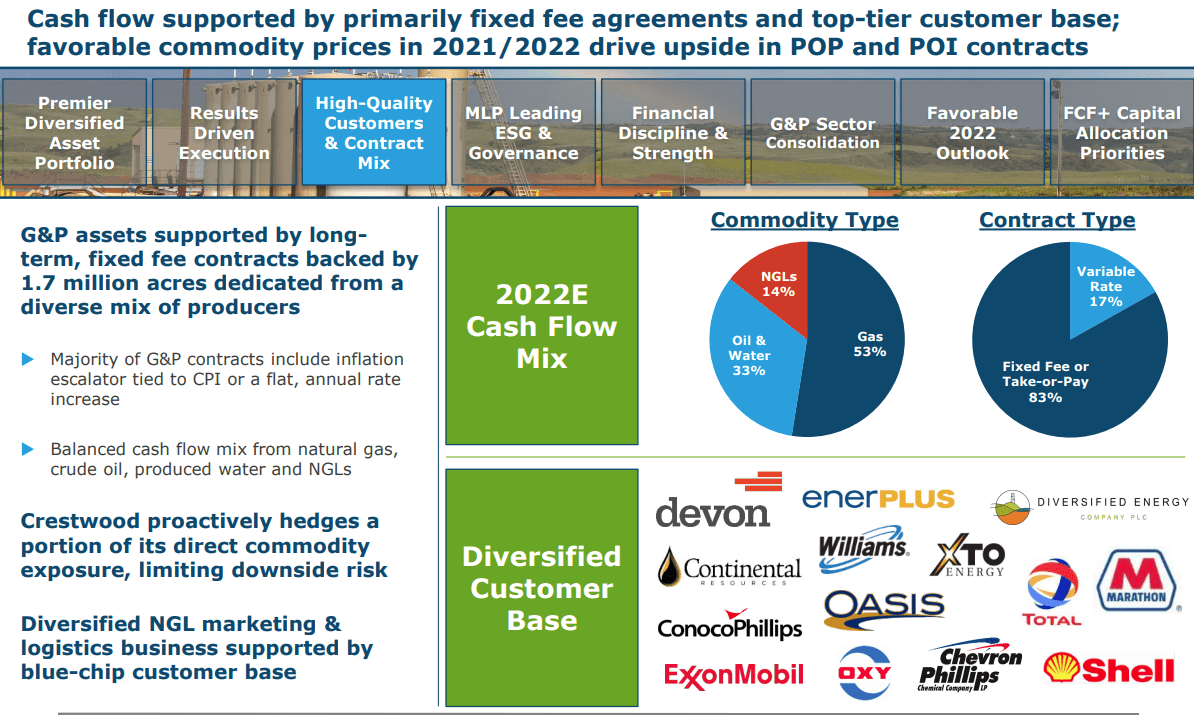

Of course, this is all just theoretical, CEQP is firing on all cylinders right now. CEQP has a well-diversified portfolio of assets providing storage and logistics for their customers. (Source: Investor Presentation)

Investor Presentation

CEQP also has a solid base of fixed-fee contracts, ensuring stability even when events like COVID happen.

Investor Presentation

U.S. gas, NGLs, and oil are all taking a prominent role in the global energy shortage. U.S. production will continue to increase as demand is robust locally and abroad.

One crucial difference is that companies are being a lot more careful with their expansion today than they were during the shale boom. Energy investors remember the shale boom, and the following bust when commodity prices collapsed.

Today, we are seeing commodity prices as high as they were during the shale boom from 2011 to 2014. We are not yet seeing the kind of reckless expansion we saw back then. This means that prices are likely to remain elevated for an extended period. The world needs more oil, gas, and NGLs, but nobody is in a hurry to kick production into high gear. Instead of hot burning growth, we’re seeing a more methodical expansion, which will benefit CEQP for a long time because it will be far more sustainable.

CEQP has been expanding through several acquisitions over the past year. This has been beneficial for common unit investors, and with the expansion that CEQP is likely to enjoy in the coming year, we can’t blame anyone who wants to invest in the common.

With a yield of 9.2%, fantastic investor protections, and an option that can be held forever, we prefer to be first in line with the preferred. Buy it, store it away, and collect the income “forever”.

Note: Each broker has its own ticker symbol for the Crestwood preferred. Crestwood issues a K-1 tax form which can create UBTI tax consequences if CEQP- is owned in a retirement account. More details here.

Shutterstock

Conclusion

The unique nature of RLJ-A and CEQP- combined with the quality of their underlying companies provides a stable means to have excellent long-term income.

It’s also the type of holding that retirees can pass on down the line to their loved ones, or not have to worry about their significant other having to buy or sell after they’ve gone on before them. These are excellent antithetical holdings to the market norm. When buying them, plan to hold for the long term, not under a year. As bulls run and bear roar, you’ll enjoy the reliable and steady income from these two forever-type investments.

That’s my kind of income investment, and I think it’s the type a great number of us will enjoy for decades to come.

Be the first to comment