Natali_Mis

BDCs looked as if they were set for a rally this year, but that thinking may have been premature, as many of them have since sold off from their January highs. While this may lead some to seek bargains, it pays to be choosy with high quality in this space.

This includes the income favorite, Sixth Street Specialty Lending (NYSE:TSLX) which as seen below, trades well off its 52-week high of $24. In this article, I highlight why TSLX is a solid buy for income on the recent dip.

Why TSLX?

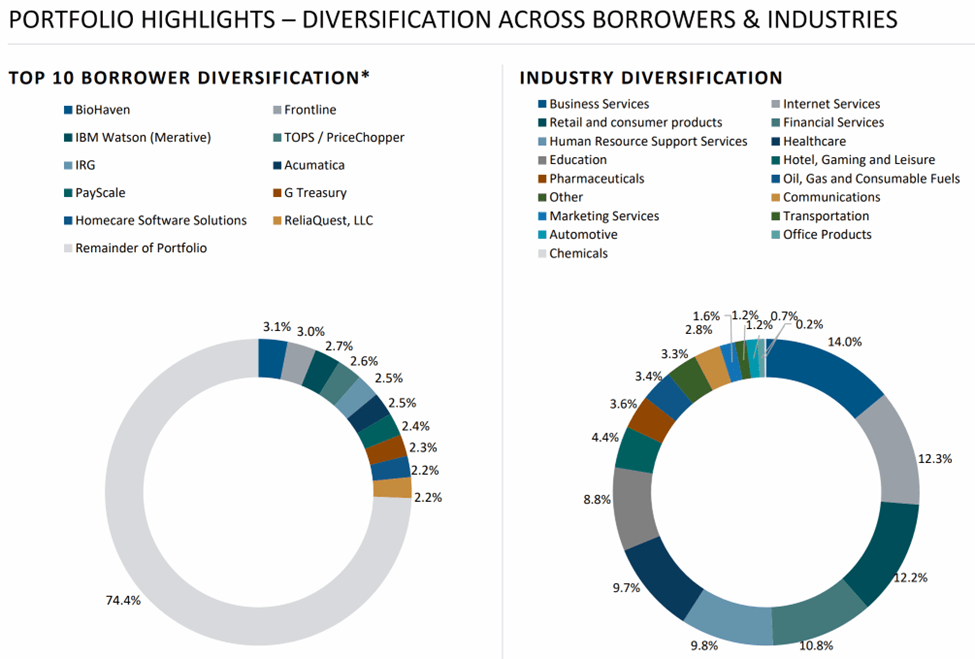

Sixth Street Specialty Lending is a BDC that invests in the U.S. middle market space, primarily through senior secured loans, and equity investments in portfolio companies. It targets portfolio companies with $10 to $250 million in annual EBITDA. As shown below, TSLX maintains a well diversified portfolio in mostly defensive industries, including business services, consumer products, internet services, and financial services.

TSLX Portfolio Mix (Investor Presentation)

Notably, TSLX benefits from its affiliation with its external advisor, Sixth Street, a global investment firm with over $50 billion in assets under management. This robust management platform gives TSLX valuable line of sight and deal sourcing opportunities that it would not otherwise have.

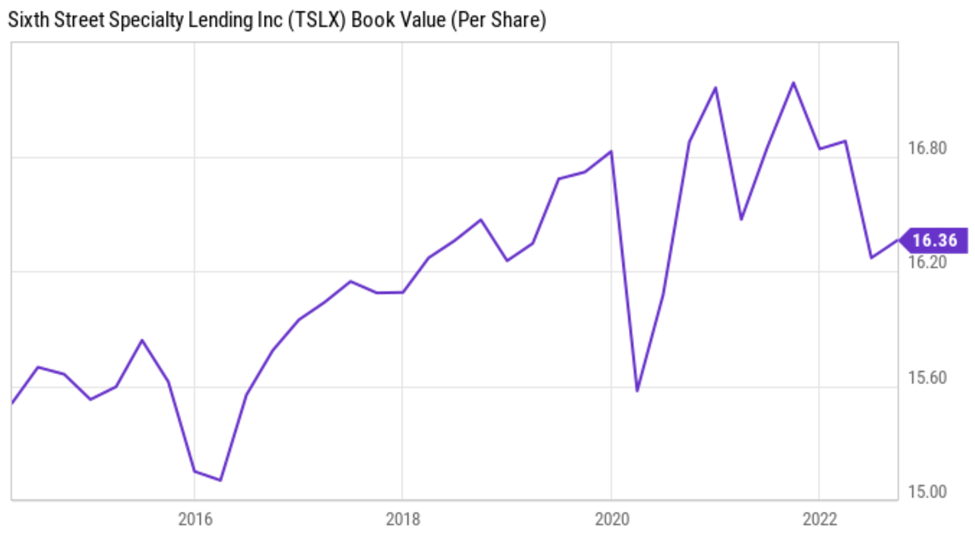

Importantly, management at TSLX has done a solid job of growing net asset value per share over the long run. As shown below, while TSLX’s NAV/share has seen its ups and downs over the years, its overall trajectory has been up since its IPO in 2014.

TSLX NAV/Share (YCharts)

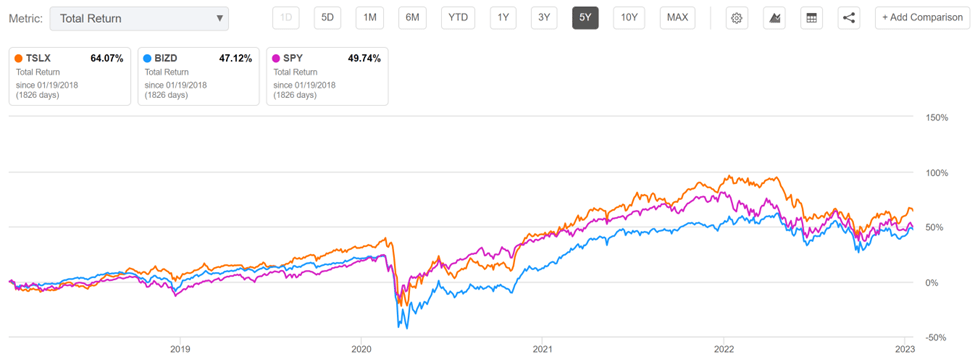

At the same, TSLX has rewarded shareholders with a regular dividend that’s risen since IPO and has never been cut, plus special dividends along the way. In fact, TSLX has paid $20.06 in cumulative dividends since IPO far surpassing its $14.71 IPO price. This has contributed to market beating returns over the past 5 years. As shown below, TSLX has produced a 64% total return since 2018, far surpassing the 47% and 50% total returns of the VanEck Vectors BDC Income ETF (BIZD) and the S&P 500 (SPY).

TSLX Total Return (Seeking Alpha)

Good reasons behind TSLX’s strong shareholder returns include prudent investment management with 90% of the portfolio being in the form of first-lien secured debt (92% total secured, including second-lien). Importantly, investments on non-accrual represent just 0.01% of the portfolio total, with no new investments added to non-accrual status in the last reported quarter. Management is also actively involved with its direct sourced investments, as it has effective voting control on 89% of debt investments.

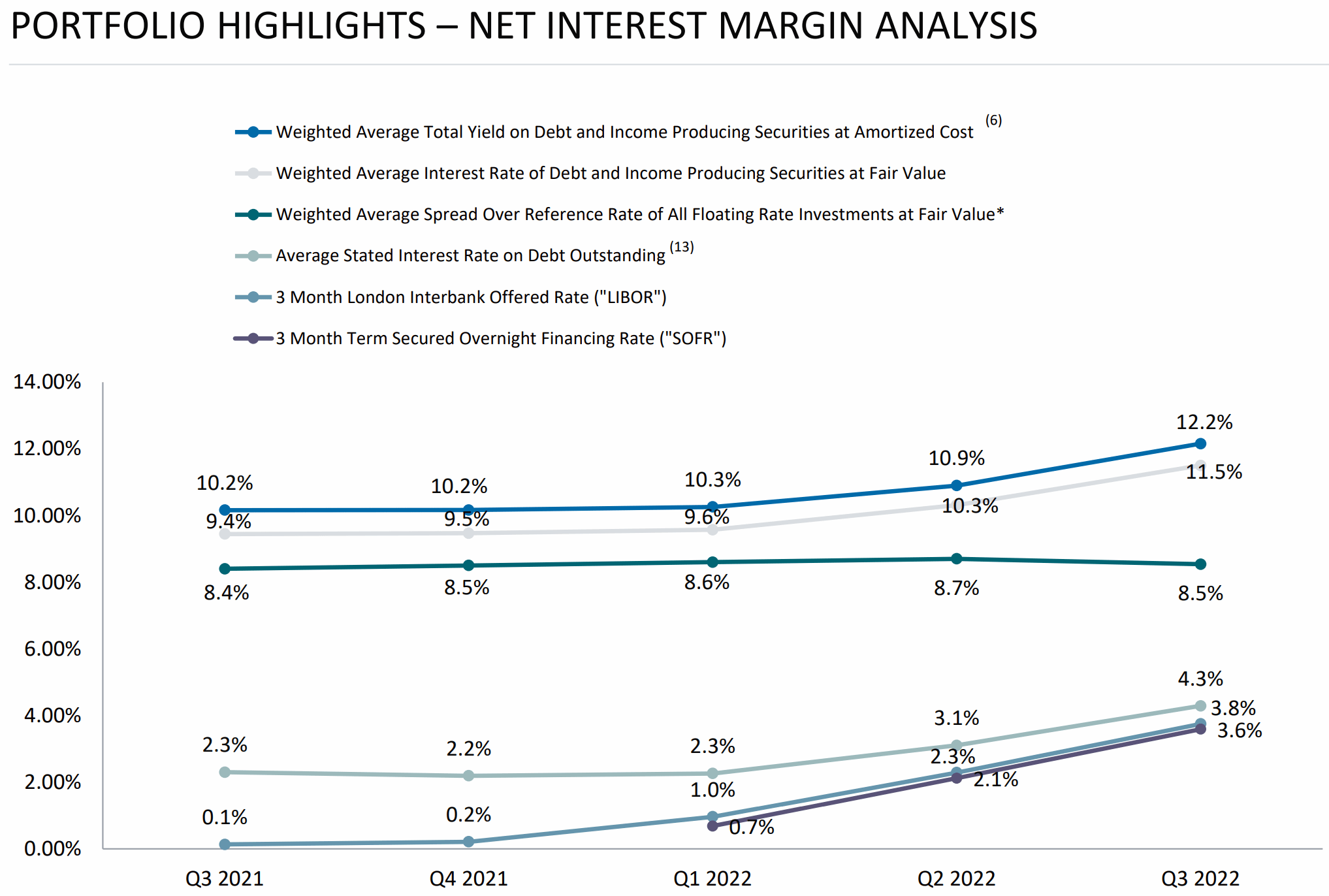

Moreover, TSLX is benefitting from rising interest rates, as 99% of its investments are floating rate. As shown below, this has contributed to weighted average total yield on debt and income producing securities improving by 200 basis points YoY to 12.2% in the last reported quarter.

TSLX Yield On Debt (Investor Presentation)

Meanwhile, TSLX maintains a BBB- investment grade rated balance sheet, with a debt to equity ratio of 1.17x, sitting well below the 2.0x statutory limit, and within management’s targeted range of 0.9x to 1.23x.

Notably, in December, TSLX hiked its regular quarterly dividend for the second time this year to $0.45 (up by $0.03 from $0.42 previously). This remains covered by TSLX’s NII per share of $0.47 during the third quarter, and is a positive sign that the fourth quarter’s NII per share may come in higher on a sequential basis.

Lastly, I find TSLX to be attractive at its current price of $18.46 with a price to book value of 1.13 (based on NAV per share of $16.36). As shown below, TSLX has generally traded at a higher premium to NAV over the past 5 years and the current valuation sits on the low end of its 2 year range.

TSLX Price to Book (Seeking Alpha)

Analysts have a consensus Buy rating on the stock with an average price target of $21, implying a potential one-year 24% total return including dividends, and the potential for special dividends would be an added bonus.

Investor Takeaway

TSLX is a premium quality BDC with a strong track record of shareholder returns. It has a very low percentage of investments on non-accrual and should continue to benefit from higher interest rates as most of its portfolio is floating rate. Lastly, TSLX pays a very high dividend yield and currently trades at an attractive valuation compared to historical levels. As such, income investors may want to take advantage of the recent dip in price to lock in the high yield.

Be the first to comment