Denis_Vermenko

This year has been an interesting one for stocks, to say the least, with inflation and higher interest rates being hot topics that caused substantial market turbulence. If there is anything to be learned from 2022, it’s that growth stocks can’t go up forever, and when the music stops, it’s no fun to be the bag holder.

While I’m bullish on certain names like Google (GOOG) (GOOGL) and Amazon (AMZN), I’m more inclined to add to high yielding stocks of quality companies at attractive prices. This brings me to MPLX LP (NYSE:MPLX), which, after the recent drop in price, is now yielding close to 10%. This article highlights why now may be an opportune time to add to this big distribution name.

MPLX Stock (Seeking Alpha)

Why MPLX?

MPLX (issues schedule K-1) is a master limited partnership (issues K-1) that was spun off from Marathon Petroleum (MPC) in 2012. It has a straightforward business model, owning and operating long-lived assets, including pipelines and storage tanks, which are used to transport energy products from one place to another. MPLX also has an inland marine business, docks, and NGL processing and fractionation facilities linked to key U.S. supply basins, particularly in the Appalachia region.

MPLX’s asset base was built primarily to serve its original equity sponsor, Marathon Petroleum. While the two companies may seem intertwined, make no mistake that MPLX is an independent company. That’s because Marathon Petroleum exchanged its general partner economic interests including IDRs (incentive distribution rights) for common equity in MPLX in 2017. This is a shareholder friendly move as it removes potential for conflicts of interest.

Meanwhile, MPLX continues to drive respectable results, with adjusted EBITDA growing by 6% YoY to $1.47 billion during the third quarter. This was driven by a strong demand environment, with total pipeline throughput of 5.8 million barrels per day during the quarter, representing a 5% increase over the prior year period. Moreover, natural gas gathering and processing volumes both rose as well, by 6% and 2%, respectively.

These strong results enabled MPLX to return $935 million of capital to shareholders, including $755 million of distributions, and $180 million of unit repurchases. Notably, MPLX raised its distribution by 10% and it still remains soundly with a DCF (distributable cash flow) to distribution coverage ratio of 1.6x.

Having a sound coverage ratio is important for MPLX not only to protect the distribution for unitholders, but also to enable a self-funding model on growth projects, making it less reliant on external capital markets (both debt and equity) for funding.

As one can imagine, cash is king when it comes to a high interest rate environment. Moreover, MPLX has a BBB rated balance sheet and carries low leverage with a net debt to EBITDA ratio of 3.5x, sitting well below the 5.0x level that most credit agencies deem safe for midstream companies.

Looking forward, MPLX’s relationship with MPC appears to be solid, as this year, 2 companies renewed a transportation service agreement for another decade. The contracts also have an automatic renewal provision that extends them through 2042. Importantly, investor concerns around a potential roll-up of MPLX into MPC can put their minds to ease. This is supported by the following comments (bolded by author for emphasis) made by management during the recent conference call:

We’ve received questions on the structure of MPLX and whether MPC will acquire partnership’s outstanding public units. So we want to restate what we’ve said in the past. First, we’ve grown MPLX into an entity with a public float of approximately $12 billion, which compared to recent MLP roll-ups is substantially larger. MPLX is a strategic part of MPC’s portfolio. MPLX has continued to demonstrate earnings growth, with the increased distribution announced today, MPC expects to receive $2 billion of distributions from MPLX annually.

As MPLX pursues its growth opportunities, we expect the value of this strategic relationship will continue to be enhanced. MPC believes that its current capital allocation priorities are optimal for its shareholders and MPC does not plan to roll-up MPLX. As we continue to grow our cash flows, we also remain focused on executing the strategic priorities of strict capital discipline, fostering a low-cost culture and optimizing our asset portfolio.

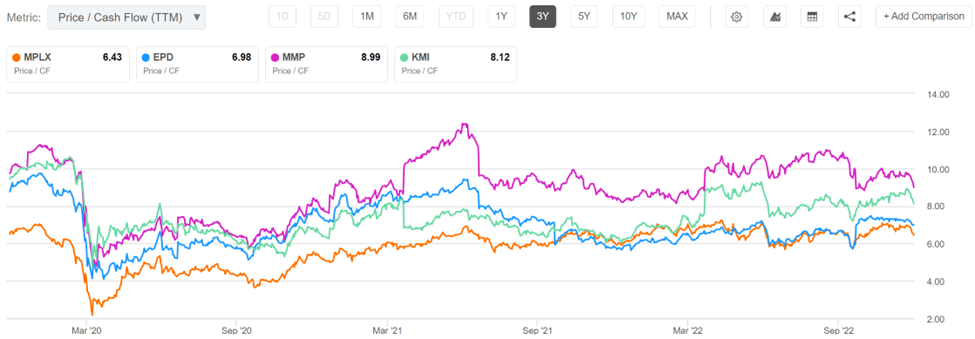

Lastly, I see value in MPLX after the recent drop in price to $31.37, resulting in a 9.9% distribution yield. As shown below, MPLX trades at a price to cash flow of just 6.4x, sitting below that of midstream peers Enterprise Products Partners (EPD), Kinder Morgan (KMI), and Magellan Midstream Partners (MMP).

MPLX Price to Cash Flow (Seeking Alpha)

Given the quality of MPLX’s asset base, strong operating fundamentals and balance sheet, I believe MPLX deserves to trade at least a 7.5x valuation. Analysts have a consensus Buy rating on MPLX with an average price target of $37.68, implying potential for total returns well in the double digits.

Investor Takeaway

MPLX’s strong operating results are supported by its quality asset base, sound management team and focused strategy. Its relationship with MPC is solid with a long-term transportation service agreement in place, while its balance sheet remains healthy despite a high interest rate environment. Lastly, I see the recent drop in MPLX’s price as presenting a strong opportunity to add to this high quality and high-yielding name.

Be the first to comment