JuSun

Income stocks have largely missed out on the market rally over the past 6 months, and while it’s easy to get FOMO and want to chase high-flyers like Super Micro Computer (SMCI) or Nvidia (NVDA), I continue to prize real cash flows over paper gains on stocks with speculative valuations.

Hence, I believe that REITs with strong balance sheets and durable hard assets remain a good choice for value and income, and this brings me to UDR Inc. (NYSE:UDR), which I last covered in September last year, noting its undervaluation and well-placed portfolio.

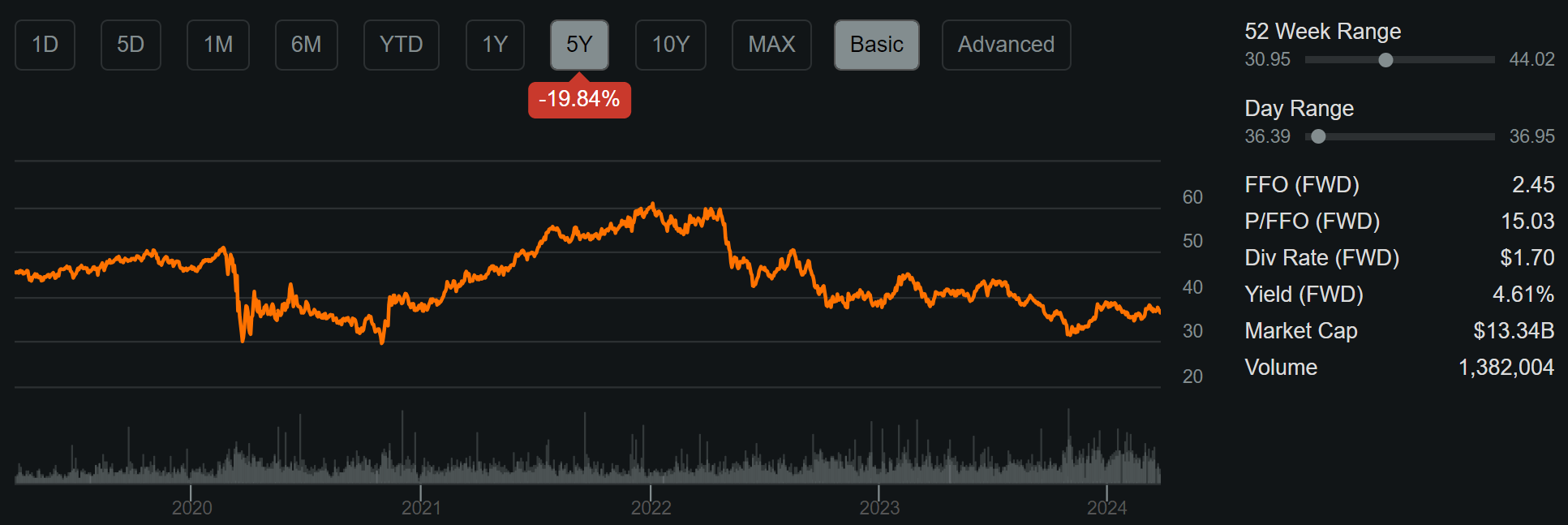

It appears the market still has not caught onto this opportunity, as UDR is down by nearly 3% since my last piece (virtually flat on a total return basis including dividends). As shown below, UDR currently sits well below its high of $60 reached during 2022.

UDR Stock 5-Yr Trend (Seeking Alpha)

In this article, I revisit UDR and provide key updates around its operating metrics, and discuss why it remains a good bargain for income and potentially strong long-term gains, so let’s get started!

Why UDR?

UDR is a large multifamily REIT, that for one reason or another, isn’t as well known as other favorites such as AvalonBay Communities (AVB) and Essex Property Trust (ESS). It’s been around for 51 years, is a member of the S&P 500 (SPY) and has an ownership interest in 60K apartment homes across the U.S.

What sets UDR apart from peers is its ‘hedged’ portfolio of properties that are in both U.S. Tier 1 markets as well as secondary markets such as the Sunbelt region. This makes UDR somewhat of a hybrid between Tier 1 multifamily REITs like Equity Residential (EQR) and Secondary market REITs like Mid-American Apartment Communities (MAA).

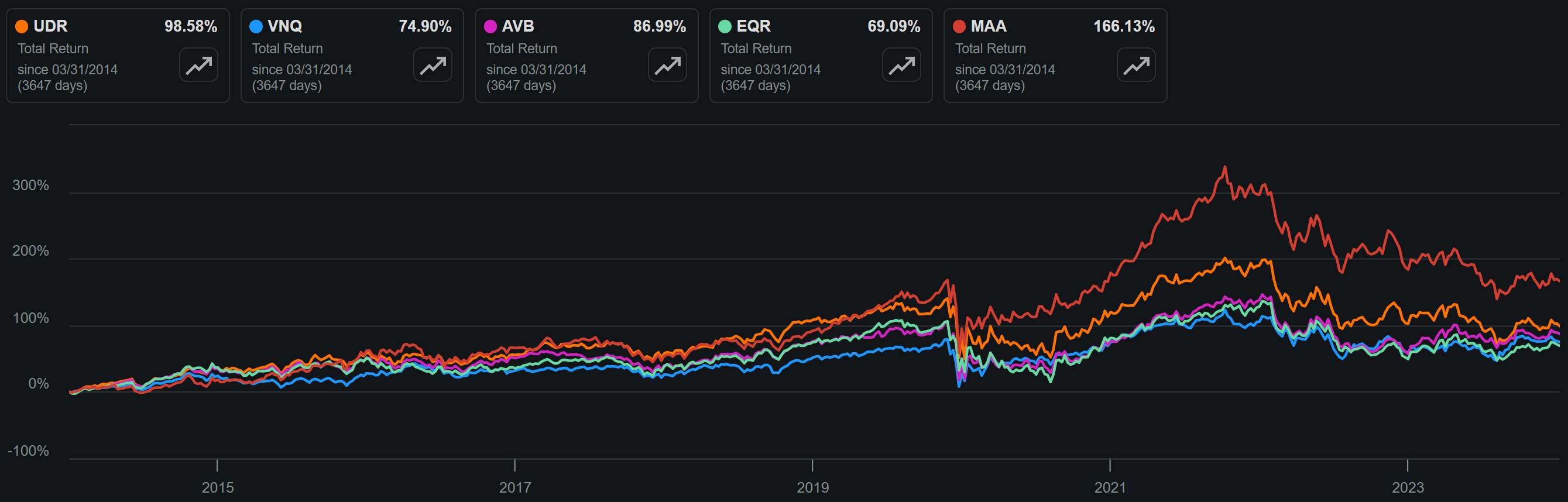

This balanced approach has helped UDR to navigate different market environments and supply/demand dynamics between Tier 1 and Secondary markets. As shown below, UDR’s 10-year total return of 99% has outperformed the 75% total return of the Vanguard Real Estate ETF (VNQ) and is sandwiched in between that of Tier 1 peers AVB and EQR’s 87% and 69%, and Secondary Market peer MAA’s 166%.

UDR vs. Peers 10-Yr Total Return (Seeking Alpha)

Notably, UDR has seen a slowdown in tenant demand and rental increases since hitting inflation and population movement-driven highs in 2021- 2022. This slowdown is reflected by Same Store NOI growing by just 2.4% YoY during the fourth quarter, reflecting a marked drop from 7.7% YoY growth in Q2 of last year, when I last visited the stock. Due to higher SSNOI growth earlier in the year, UDR still managed to produce 6.0% SSNOI growth for the full year 2023.

Despite lower SSNOI growth, UDR still managed to produce strong occupancy, which stood at 96.9% at the end of Q4, sitting 30 basis points higher than the 96.6% at the end of Q2 when I last reviewed the stock.

One of the key concerns around UDR and its peers is the impact of new supply in its markets, which was one of the reasons, besides normalization of demand, behind lower SSNOI growth. Management expects for pressure from new supply to continue this year, resulting in muted near-term market rent growth compared to its long-term average.

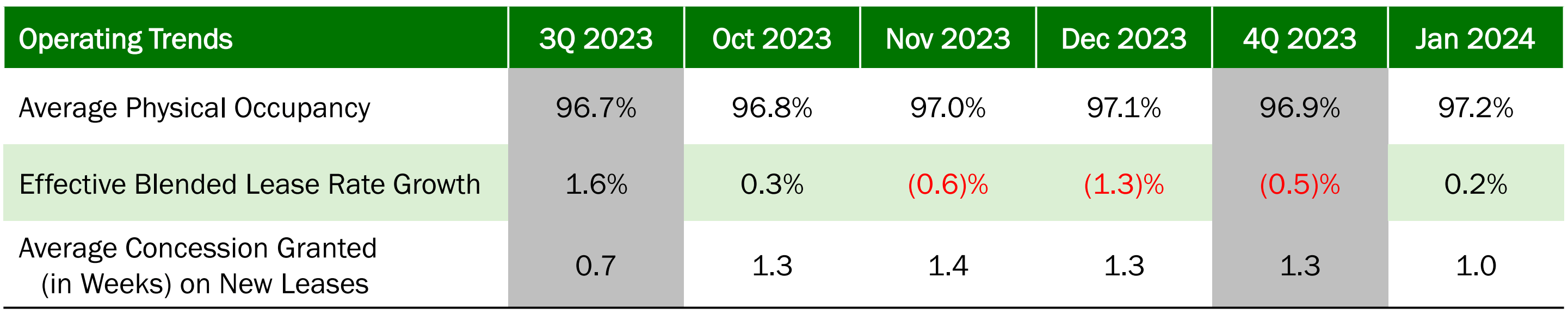

Given the cyclical nature of the industry, it’s probably a good idea to buy UDR when it’s at or approaching the bottom of a cycle, as may be the case now, rather than at when it was at the top in 2021-2022. Moreover, the market doesn’t appear to appreciate UDR’s improving occupancy, which sat at 97.2% in January of this year (30 bps higher than December) and a return to rent growth of 0.2% in the same month after declines in November and December due to seasonality, as shown below.

Investor Presentation

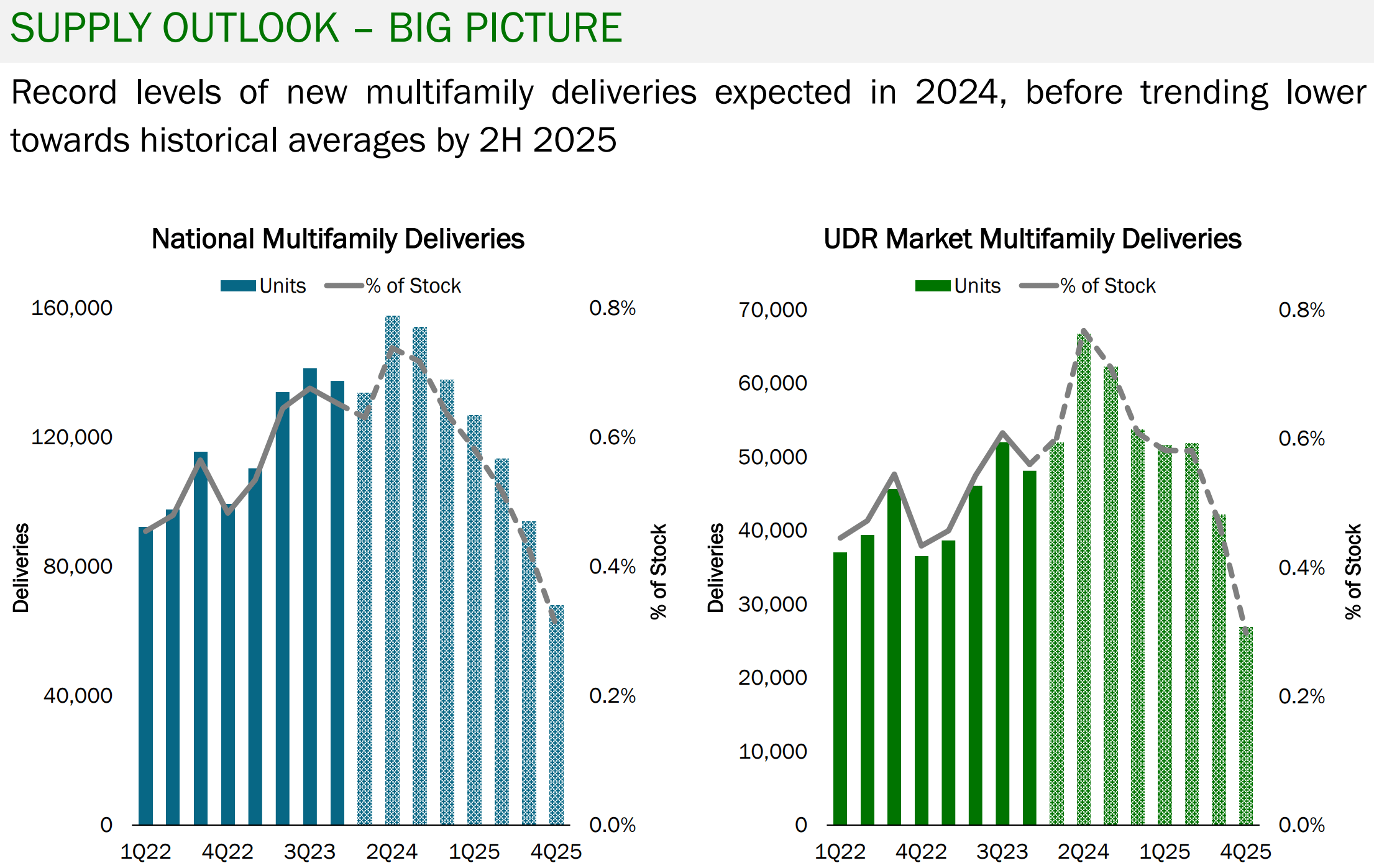

Meanwhile, I see the market as being overly-rotated on near-term results, while ignoring the big picture that market deliveries of new apartment buildings may be set to decline after this year. This is supported by the following chart based on data from RealPage (an apartment analytics firm) and CoStar. As shown below, new apartment deliveries are expected to trend back down to historical levels by the second half of next year.

Investor Presentation

Hedging against supply imbalances is also where UDR’s diversified Tier 1/Secondary market approach comes in handy, as its East Coast/Mid-Atlantic and West Coast are seeing lower new supply (under 2% of total property base in 2024) compared to Sunbelt regions, which are expected to see higher new supply at 5% of total property base in 2024. As shown below, UDR’s property base is expected to still produce 3% SSNOI growth this year portfolio-wide, driven by growth in East Coast/Mid-Atlantic and West Coast regions.

Risks to UDR include potential for a continued slowdown or even decline in demand for multifamily housing. This could be caused by a number of different factors like macroeconomic pressures as well as material new supply of single-family homes should interest rates drop, as that could result in higher-than-expected move-outs for UDR.

Over the next few quarters, I would pay attention to UDR’s occupancy ratio as anything over 95% would generally be considered to be good. I would also look for signs of a meaningful turnaround in rental rate increases, as that would be a signal that UDR is coming out of a supply-driven slump.

Importantly, UDR carries a strong balance sheet with BBB+ credit rating from S&P. It also has $965 million of liquidity, which more than covers its $82 million worth of committed development projects, and $688 million worth of debt maturities (13% of total debt) in the 2024-2026 timeframe. Moreover, UDR carries a safe net debt-to-EBITDAre ratio of 5.6x, sitting below the 6.0x level generally considered safe for REITs, and has a strong fixed charge coverage ratio of 5.1x.

This lends support to UDR’s respectable 4.7% dividend yield, which remains well-covered by a 70% payout ratio. It also comes with a 5-year dividend CAGR of 5.4% and 13 consecutive years of growth.

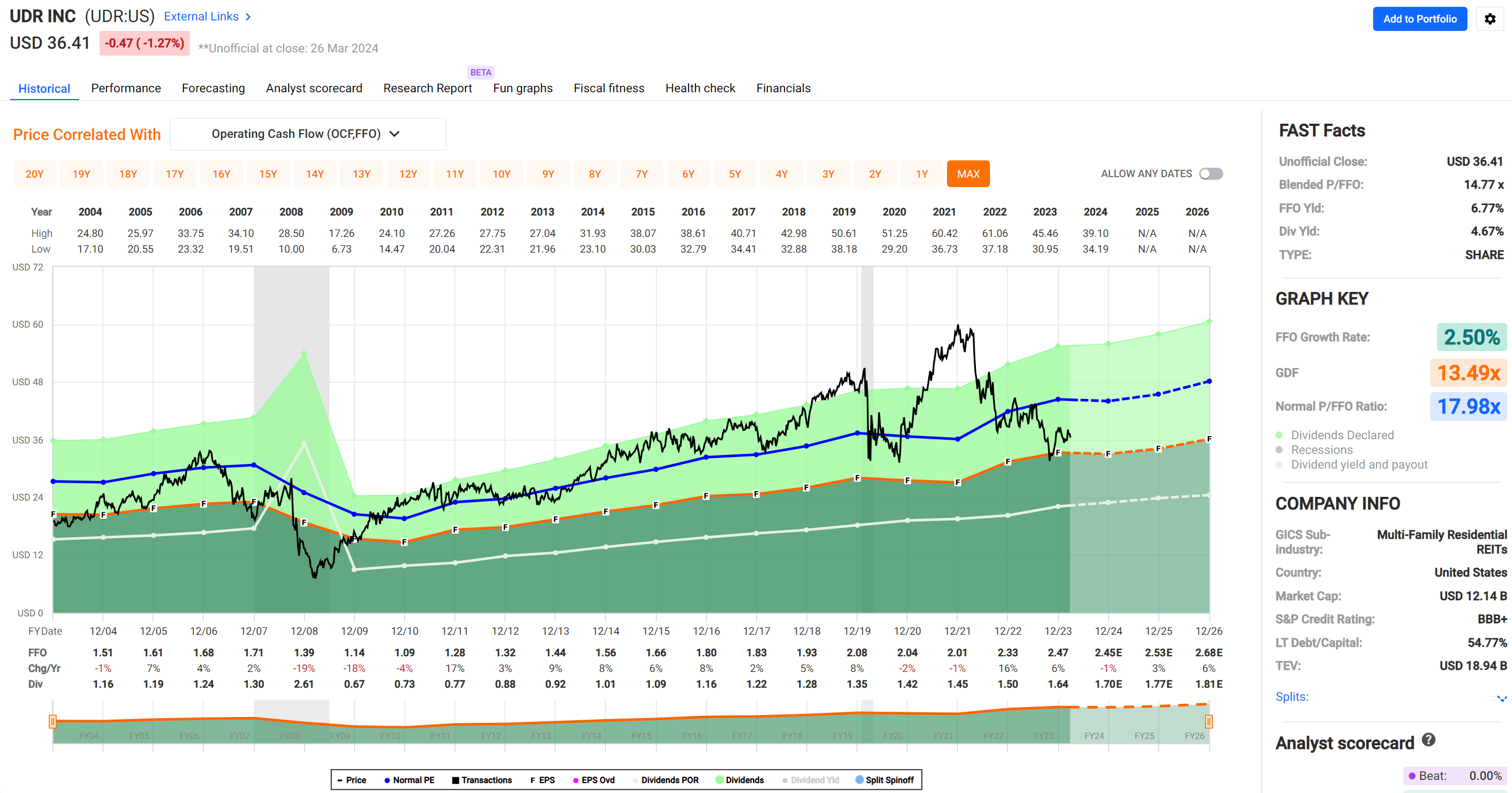

Turning to valuation, I continue to find UDR to be attractive at the current price of $36.41 with forward P/FFO of 14.9, which is slightly cheaper than the 15.2 P/FFO from when I last visited the stock. UDR also trades at a discount to its normal P/FFO of 18, as shown below. UDR’s P/FFO is also under that of AVB’s 16.6 and EQR’s 15.9 despite having a better total return performance over the past decade.

FAST Graphs

While analysts expect flat FFO/share this year, growth is expected to resume at 3% next year and rise to 6% in 2026. I believe those are reasonable estimates based on the presumption that new supply pressures will ease starting in 2025 and should interest rates decline as per the Fed’s latest guidance for 3 rate cuts this year.

Over the long run, I believe UDR can achieve a conservative base case scenario of 5% annual FFO/share growth driven by rental increases and development, which combined with the dividend could give UDR market level performance, all with a far higher yield than the S&P 500.

Investor Takeaway

In summary, UDR has seen a slowdown in SSNOI due to new supply in its markets and normalization of tenant demand after high rental growth in prior years. However, the company’s diversified Tier 1/Secondary market approach and strong balance sheet provide a cushion against these challenges.

Moreover, with new supply expected to decline in the coming years, providing support for FFO/share growth down the road. UDR also offers a respectable and well-supported dividend, making it an attractive option for income investors. Given the potential for future growth and the current discounted valuation, I believe UDR is a solid long-term investment opportunity at present and maintain a ‘Buy’ rating on the stock.

Be the first to comment