koto_feja

Overview

Note that I previously rated a hold rating for Nutanix (NASDAQ:NTNX), as the valuation has already reflected what I thought was a fair value for NTNX and that the risk/reward situation is no longer attractive. Turns out, I was wrong on where the “fair valuation” is for NTNX, as the strong business performance continued to push valuation to new heights. With the stock now trading at 6.4x forward revenue, my recommendation for NTNX is a buy rating, as I am very impressed with the execution and growth opportunities ahead for NTNX. Using a long-term DCF model to better capture the potential growth and FCF generation capabilities, I got to an intrinsic share price target of $77.

Recent Results & Updates

As I said previously, I remain positive about the business fundamentals, and indeed, NTNX continues to deliver very strong results. In 2Q24, NTNX reported non-GAAP revenue of $565.2 million, representing a growth of 16%, largely driven by strength in renewals. NTNX also showed strong progress in managing costs, where its adj gross margins came in at 87.3%, leading to an expansion of adj operating margins to 21.9% (which also shows the operating leverage that is embedded in the business). This strong execution also gave management the confidence to raise guidance across the board. FY24 revenue guidance was raised by $25 million, which is more than the amount that NTNX has beaten in 2Q24 (2Q24 revenue was guided for $550 million at the midpoint), suggesting that management is expecting (or is already seeing) strong demand that could push 2H24 performance higher than previously expected. Gross and EBIT margin targets were also raised by 50bps to 85.5% and 100bps to 13%, respectively, at the midpoint.

This is a very impressive quarter for NTNX that has led me to change my views on the business and how much the share price is worth. While the headline figures were strong, my view is that the underlying strength is seen in the 23% y/y ACV billings growth (came in at $329.5 million), which came in way ahead of what the 2Q24 guide was implying (using revenue to billing ratio), mainly driven by very strong renewal performance that really speaks well of the stickiness in NTNX products. NTNX not only saw better renewal economics and better on-time renewals, they also benefited from some early and co-terming of renewals, which I believe speaks really well of NTNX go-to-market efforts in stepping out early to convince customers to renew. And, notably, it also speaks well of the stickiness of NTNX’s product. My view is that, typically, when such contracts come up for renewal, companies are “forced” to make a choice: (1) renewal at whatever rates the vendor is charging, or (2) finding another vendor. In this case, it appears that customers did not find any reason to switch.

Because of this strength in execution, it gave me confidence that NTNX can successfully pursue the growth opportunities available. Specifically, it is NTNX’s ability to capture the VMware opportunity, for which management noted that the pipeline is substantial and growing and is a multi-year opportunity. I am bullish on this VMware opportunity because the acquisition drives a secular tailwind to NTNX, as customers that are now under VMware are “forced” to make a decision to stay on or switch given that Broadcom is the owner today. While early, NTNX has already seen a growing volume of larger deals in the pipeline, and I expect NTNX to continue growing this pipeline given NTNX investments in partner and customer incentives to drive share gains.

Yeah, why don’t I start, Jim, and Rukmini can give you color on the pipeline. So, first of all, I think, as you said, I mean, there are significant concerns from VMware customers, regarding the Broadcom acquisition. And we think that this is a significant multi-year opportunity for us to win new customers and to gain share.

Now, getting to your question a bit here, the timing and magnitude of these deals is a bit unpredictable. Our pipeline is quite substantial and growing. Now, for a number of reasons, we expect contributions to the opportunity to build gradually, right? And here are the reasons. First one, Jim, is that many customers signed multi-year ELAs, enterprise agreements, with VMware prior to the deal closing, three to five years. So, it buys them some time to make decisions.

The second, converting from VMware three-tier accounts or legacy storage accounts, which is a good chunk of VMware footprint, in many cases requires a refresh of their storage and our servers, right, one of the two, which could also impact the timing of the potential software purchases that they would make with us. Okay?

And the last piece is, like, with all these accounts, we typically have a land and expand motion. So, the first deal could be smaller, and then there’s a lot of potential for expansion further than that. From: 2Q2024 earnings call

What also gave me an extra layer of confidence in NTNX’s ability to pursue this share-gain opportunity is the progress in partnership with Cisco. Management noted that the joint offering is driving solid customer interest and has already led to multiple new wins in 2Q24. This could potentially lead to an upside surprise for FY24, as a modest contribution has been embedded in FY24 guidance. Nonetheless, I am expecting a stronger contribution from FY25 onwards.

I believe these growth drivers are huge enough to overwhelm the weak macro environment about which many investors are worried today. Management also said that demand is still stable compared to previous quarters and highlighted the modest elongation of sales cycles. Importantly, they noted that businesses are prioritizing digital transformation and infrastructure modernization initiatives, which means there are no structural changes to the secular tailwinds that NTNX benefits from. Lastly, I think NTNX FCF’s performance really shows that they are on track to continue gushing out more cash. This can be seen in the guide as well. For FY24, the FCF guide was revised upwards from $420 to $440 million, an increase of 350bps in the FCF margin. It is worth mentioning that the FY24 FCF margin of 20% is already touching the high-end of the NTNX FY25 target of 17-21% margin (mentioned during the previous analyst day), which means there is a real chance for NTNX to exceed the FY25 targets.

Valuation And Risk

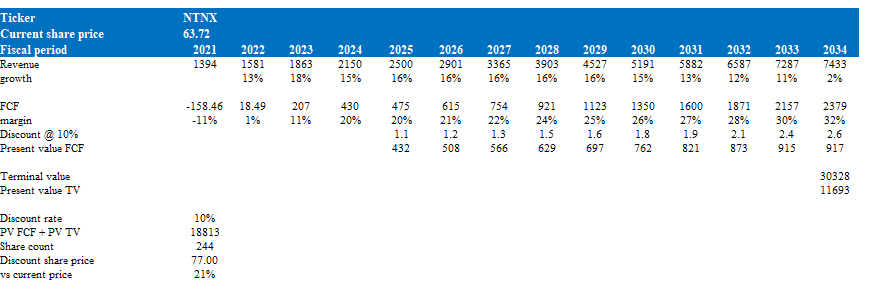

Author’s valuation model

Unlike my previous model, I am using a long-term DCF to value NTNX to better derive the intrinsic value of the business. Using a relative model is too myopic, as historical multiples do not accurately reflect the current fundamentals of NTNX business, which have improved a lot since years ago. Using the management FY24 and FY25 guide (provided during the previous analyst day), it is assumed that revenue will reach ~$2.5 billion in FY25 (implying 16% growth from FY24). Given the execution so far and pipeline opportunities, I assumed NTNX could sustain its 16% growth in the growth years through FY29, followed by a gradual reduction in growth to 2% (inflation rate) in FY34. As for FCF, I modeled NTNX to continue seeing FCF margin expansion over the long term, anchoring the exit FCF margin by benchmarking large, mature tech companies (Oracle in this instance). Pre-covid, ORCL reported around 32% FCF margin, and given that NTNX is already at 20% FCF margin and has a similar gross margin profile, I think NTNX can achieve 32% as well. Using my growth and margin assumptions along with a discount rate of 10%, I got to an intrinsic value of $77, which is 21% higher than where NTNX is trading today.

Risk

One of the key growth drivers is the partnership with Cisco. While traction so far is good, note that Cisco has a lot of partnerships with many other players, and there is no guarantee that Cisco will always prioritize selling NTNX products. If Cisco views another company’s product as a better one, it could lead to lower sales for NTNX, which could impede growth.

Summary

Summarizing this post, the recommendation for NTNX is a buy rating, and the main reason is because of the strong execution that NTNX has continued to show. In the recent quarter, NTNX exceeded expectations with strong revenue and billing growth and margin expansion. It seems that NTNX can continue to grow given the VMware opportunity and Cisco partnership. Notably, this growth comes with improving FCF margin, which is already tracking well against the FY25 target set out during the previous analyst day.

Be the first to comment