Melissa Kopka/iStock Editorial via Getty Images

Elevator Pitch

I assign a Hold investment rating to General Mills, Inc.’s (NYSE:GIS) stock.

With General Mills’ shares nearing all-time highs, certain investors might be eager to take profits on the stock and rate it as a Sell. But GIS isn’t overvalued despite its share price strength, as peer and historical comparisons suggest that General Mills is at a fair valuation now. In addition, GIS’ strong stock price performance is justified by its ability to tackle inflation and its healthy long-term growth prospects. Nevertheless, GIS is currently fairly valued, and this suggests that the stock deserves a Hold rating.

GIS Stock Key Metrics

GIS issued the company’s Q4 FY 2022 (YE May 31) earnings press release on June 29, 2022, before trading hours, and its key metrics help to explain why its shares have reached historical highs.

The key financial metrics relate to General Mills’ earnings per share or EPS and its shareholder capital return.

The company’s non-GAAP adjusted EPS expanded by +23% YoY from $0.91 in the fourth quarter of fiscal 2021 to $1.12 in the recent quarter. General Mills’ Q4 FY 2022 EPS was +11% higher than the sell-side analysts’ consensus earnings estimate of $1.01 per share. This follows on from a +8% EPS beat for GIS in Q3 FY 2022.

On the back of a substantial earnings beat, GIS increased its quarterly dividend per share payout from $0.51 to $0.54. This translates into a very decent annualized dividend yield of 2.9% based on General Mills’ last traded stock price of $75.51 as of July 7, 2022.

GIS isn’t merely returning more excess capital to the company’s shareholders via higher dividends. General Mills also highlighted in its fourth-quarter results media release that it expects to implement “an increased share repurchase plan in fiscal 2023” which should lead to “a 2 to 3 percent net reduction in its average diluted share count.”

Why Has GIS Stock Gone Up?

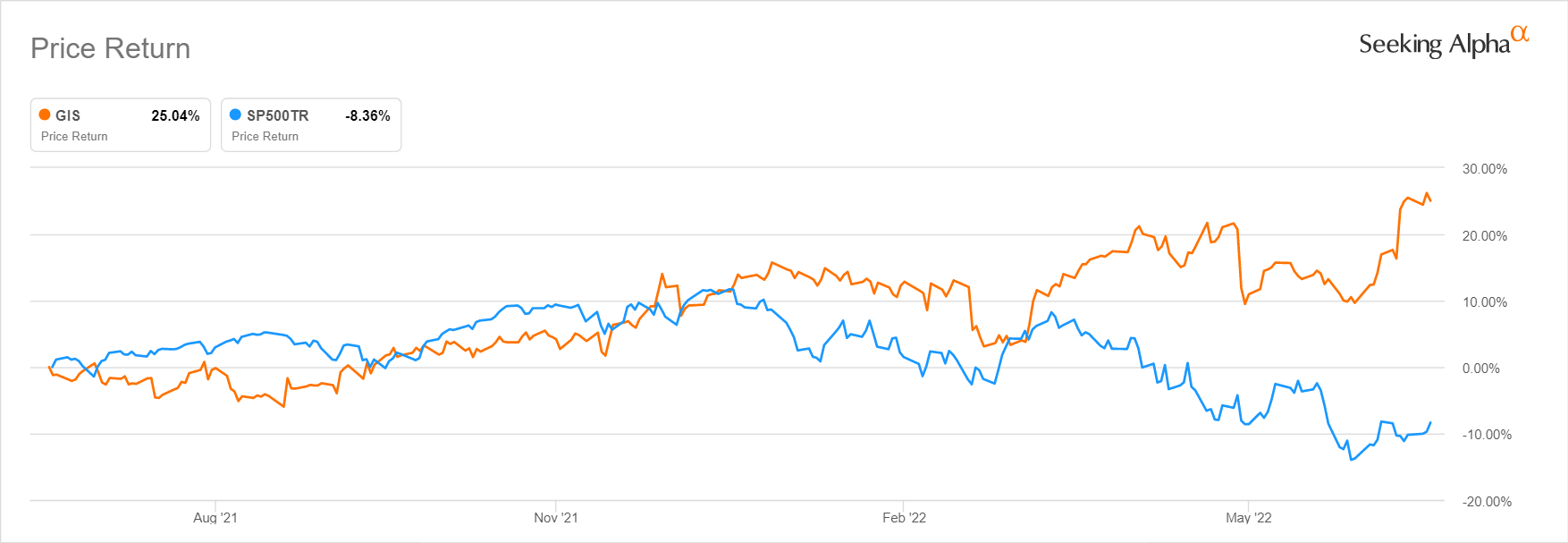

As per the chart below, GIS stock has gone up by +25.0% in the past year, which represents a substantial outperformance as compared to the S&P 500’s -8.4% decrease during the same period.

General Mills’ Historical One-Year Stock Price Chart

Seeking Alpha

General Mills’ shares are also near all-time highs. GIS registered a new 52-week and historical peak stock price of $76.73 during intra-day trading on July 6, 2022. GIS’ last done share price of $75.51 as of July 7 is about -1.6% below its historical high.

In my view, there are two key reasons for the significant rise in General Mills’ share price in the past year.

One key reason for the positive share price momentum for General Mills is that the consumer staples sector is becoming “a safe haven” for investors, with GIS being one of the proxies for this sector.

A recent June 29 Seeking Alpha News article cited a BofA survey which mentioned consumer staples were one of the few sectors “seeing inflows” from funds and highlighted this as a sign that “investors once again are taking some shelter in consumer defensive stocks.”

Within the consumer staples sector and food companies in particular, GIS is among the key names that investors watch closely. As an example, General Mills is the second largest holding in the Invesco Dynamic Food & Beverage ETF (PBJ) with a 5.49% stake as of June 30, 2022.

Another key reason for General Mills’ share price strength is that the company has demonstrated its ability to successfully counter the negative impact of inflation.

In the previous section, I noted that GIS has been able to deliver bottom line growth above market expectations in the recent quarter, while still having the capacity to return more excess capital to its shareholders via higher dividends and more share repurchases.

Looking ahead, General Mills guided at the company’s Q4 FY 2022 investor briefing that its “price realization, and the combination of HMM (its cost optimization program which it refers to as Holistic Margin Management)” can “largely offset the dollar cost of the 14% inflation that we’ve called” in full-year fiscal 2023. Investors agree with the company’s optimistic view, with the Wall Street’s consensus financial projections obtained from S&P Capital IQ pointing to the gross margin for GIS contracting marginally from 33.00% in FY 2022 to 32.95% in FY 2023.

In the next section, I discuss whether these positives have been fully priced into General Mills’ current valuations.

Is GIS Stock Overvalued?

General Mills’ valuations appear to be fair now, even though its current share price is close to historical highs.

Based on valuation data sourced from S&P Capital IQ, GIS is currently valued by the market at 18.9 times consensus forward next twelve months’ normalized P/E. In absolute terms, a forward P/E multiple of below 20 times for a leading food company with well-known brands like Cheerios doesn’t seem to be expensive. From the perspective of historical valuations, General Mills’ current P/E multiple only represents an +11% premium as compared to its 10-year average forward P/E of 17.1 times.

I touch on General Mills’ peer valuations in the subsequent section.

How Does General Mills Compare To Its Competitors?

I compare GIS against its competitors and peers in the packaging food and consumer staples space on various valuation and financial metrics in this section of the article.

Peer Valuation Comparison For GIS

| Stock | Consensus Forward Next Twelve Months’ Normalized P/E Multiple | Consensus Forward Next Twelve Months’ EV/EBIT Multiple | Consensus Forward One Year Revenue Growth | Consensus Forward Two Years Revenue Growth | Consensus Forward One Year Normalized Net Profit Margin | Consensus Forward Two Years Normalized Net Profit Margin |

| Post Holdings, Inc. (POST) | 28.1 | 19.0 | +2.7% | +1.9% | 3.6% | 4.4% |

| UTZ Brands, Inc. (UTZ) | 27.0 | 20.9 | +4.2% | +3.4% | 6.0% | 7.0% |

| The Hershey Company (HSY) | 26.9 | 22.2 | +3.6% | +2.7% | 17.1% | 17.4% |

| Mondelez International, Inc. (MDLZ) | 21.0 | 21.1 | +4.3% | +3.0% | 14.0% | 14.4% |

| General Mills | 18.9 | 17.6 | +2.4% | +2.0% | 12.4% | 12.7% |

| Kellogg Company (K) | 17.7 | 18.2 | +1.8% | +1.8% | 9.7% | 9.8% |

| Campbell Soup Company (CPB) | 17.0 | 14.7 | +2.2% | +0.9% | 9.9% | 10.2% |

| The J. M. Smucker Company (SJM) | 16.5 | 14.3 | +3.5% | +2.7% | 10.4% | 11.4% |

| The Kraft Heinz Company (KHC) | 14.1 | 13.3 | +0.4% | +1.4% | 13.2% | 13.4% |

Source: S&P Capital IQ

General Mills’ consensus forward next twelve months’ P/E and EV/EBIT multiples are right in the middle of the pack among its peers as per the table presented above, which seems fair. GIS boasts similar low-single digit percentage consensus forward revenue growth rates in line with its peers, and the company is ranked fourth in the peer group of nine companies based on its expected profit margins for the next two years.

What Is The Long-Term Outlook For General Mills?

General Mills had reiterated its long-term growth targets at the dbAccess Global Consumer Conference on June 15, 2022, where it highlighted its expectations of achieving “2% to 3%” top line expansion and “mid-to-high single-digit EPS growth.”

The long-term financial goals are largely aligned with the sell-side analysts’ consensus financial forecasts. As per S&P Capital IQ, General Mills’ revenue and EPS are projected to grow by CAGRs of +1.8% and 5.9%, respectively for the FY 2023-2027 period.

It doesn’t seem a stretch for GIS to realize the company’s long-term growth ambitions.

A revenue growth of +2%-3% can be generated by new products and portfolio restructuring (exiting or selling businesses with slower growth and reinvesting capital in faster growing ones). With respect to profitability improvement, General Mills can rely on positive operating leverage and cost optimization efforts to expand its profit margins in the future. Moreover, GIS mentioned at the February 2022 CAGNY Virtual Conference that it is targeting “a 1% to 2% average annual reduction in our net share count over a multiyear time frame” with share buybacks, which should be supportive of future EPS growth.

Is GIS Stock A Buy, Sell, or Hold?

I rate GIS stock as a Hold. On one hand, I like General Mills as the company has levers to offset the negative impact relating to inflation in the near term, and its long-term growth outlook is good as well. On the other hand, General Mills’ valuations are fair implying limited upside potential.

Be the first to comment