peshkov/iStock via Getty Images

There was a fair amount of misleading talk about Cenovus Energy (NYSE:CVE) cash flow for the current quarter. Seasoned investors know that a large acquisition takes a year (or even several years) to fully integrate into optimal company operations. Some benefits are immediate. In fact, a market with improved commodity prices, like the current market, makes management look like geniuses. Nonetheless, expectations following an acquisition can be very unrealistic because few of the many analysts following a company have any idea about the actual operations of the company and what is needed to make an acquisition work.

Additionally, Cenovus Energy management announced about a billion dollars (Canadian) in hedging program losses because oil prices unexpectedly went through the roof. Management can afford to discontinue the program because the debt levels are down, and the additional refining capacity provides badly needed vertical diversification. Forward profitability and cash flow is likely to be less volatile in the newly combined company configuration.

Therefore, the market can “pout” or put the company in the doghouse from time to time as unrealistic expectations make it nearly impossible for management to satisfy the market in a quarter. But good management will show excellent long-term results even if a quarter is “not up to par” in the eyes of the market.

(Canadian Dollars Unless Otherwise Stated)

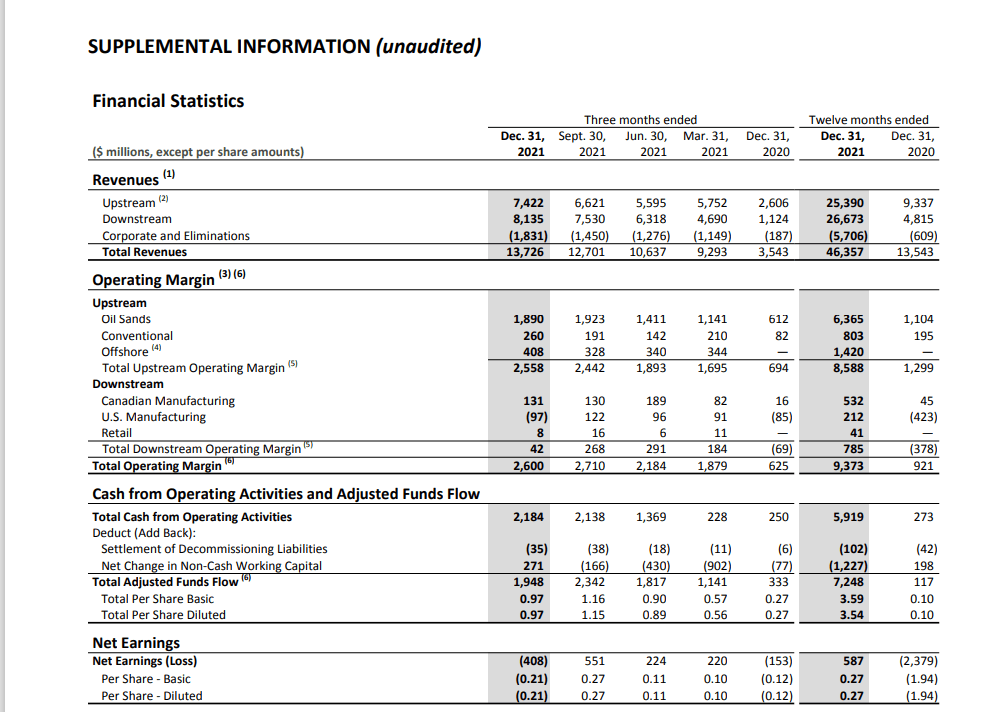

Cenovus Energy Supplemental Fourth Quarter 2021, Financial Information Summary (Cenovus Energy Fourth Quarter 2021, Supplemental Information)

Fortunately for investors, Canadian companies often report much more detailed information than their United States counterparts. This often makes it much easier for investors to determine the cause of some variations from market expectations. Now the hedging program may mean that the first couple of quarters have some lower-than-expected cash flow. But sooner or later, the benefits of the upgrader and the refineries will result in generous profits (on average) throughout the industry cycle.

In the case of cash flow, the cash flow from operating activities before the changes in noncash working capital had a roughly C$400 million quarter to quarter swing. This is in addition to continuing optimization costs that are probably not “smooth” or reasonably level from quarter to quarter. The net result is that cash flow shown above varied from market expectations for some events that likely will not repeat (or at least not repeat the same way).

As the consolidation of the acquisition proceeds, cash flow will likely increase. Management has sold some noncore properties to reduce debt and lower the cost of remaining operations. Management did mention that it is unlikely there would be more material sales in the future.

With all the good news shown in the results above, Mr. Market wanted still more. Management talked about potentially acquiring 100% interest in some of the refineries where the company has a joint venture. There is still the rebuild of a refinery that burnt to the ground before the acquisition closed. Management has some approximate answers to this. But Mr. Market wants a certainty that sometimes is not attainable. Management basically stated as much.

Mr. Market also wanted more money returned to shareholders. This management doubled the dividend to a level that was not acceptable to the market. The market acts like the current conditions will last “forever”. Indeed, there are companies I follow that cater to Mr. Market constantly only to disappoint (most likely) during the next cyclical downturn. Mr. Market can be very mercurial in the short run.

But a reliable and conservative reputation should serve the company stock price positively in the long run. In some ways the market behaves like a child that does not get what it wants only to find out the wisdom of the parents in the future. While the reaction of the stock price to the conference call may not have been what investors hoped for, that reaction will likely pass quickly because this management produces results that appear to please the market in the long run. It would be reasonable to expect those pleasing results in the future.

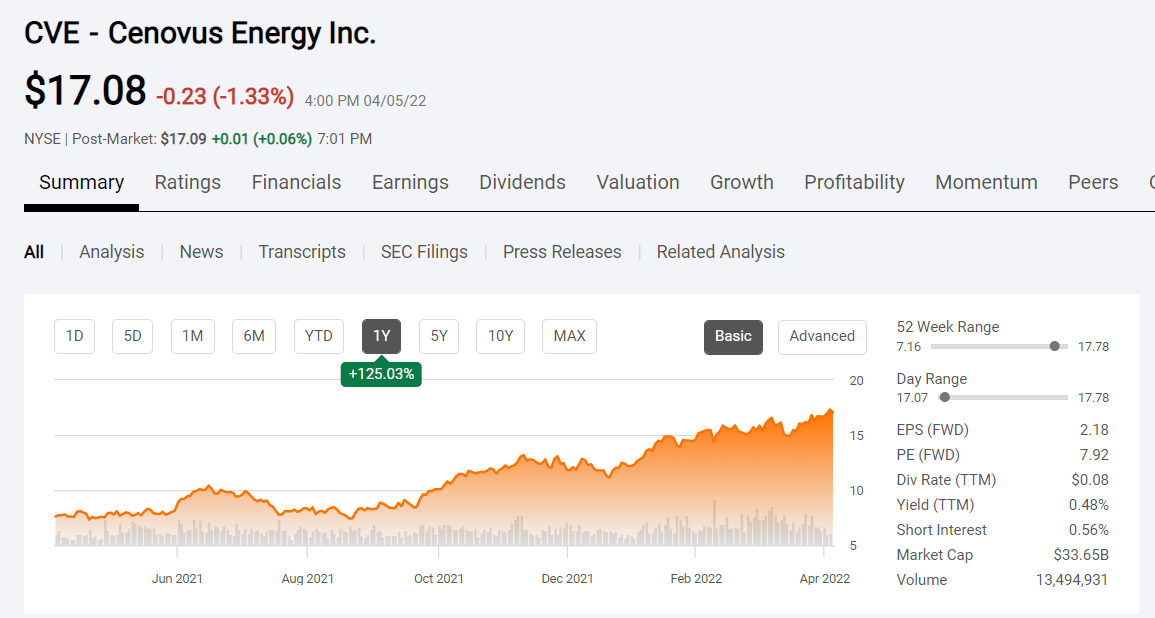

Cenovus Energy Stock Price History And Key Valuation Metrics (Seeking Alpha Website April 5, 2022)

The fact of the matter is that the stock has performed rather well for a “large company stock”. Few companies the size of Cenovus have stock prices that have increased as much over the last year (or two for that matter).

Cash flow has increased tremendously since the buyout from partner ConocoPhillips (COP) and so has production. Of the two companies, Cenovus Energy has grown much faster since that acquisition even accounting for the sale of some noncore interests. In contrast ConocoPhillips production has decreased considerably as it paid down debt and sold assets (at least cheap prices at first) because it had to repay debt. I estimate that ConocoPhillips production dropped by at least one-third before the latest acquisition. I covered this in several past articles of both companies.

Even so the market cap shown above is dirt cheap for a company that produced roughly C$2 billion in cash flow from operating activities before changes in noncash working capital accounts for the fourth quarter.

Well run thermal companies tend to cash flow rather well because thermal projects require a large cash investment in the beginning. Since much of the cash flow is the recovery of that initial large investment, management has a lot of discretion in spending the cash flow (or saving it).

Low debt must be the top priority because thermal margins have often disappeared (or worse) during cyclical industry downturns. Therefore, a bank line during the worst part of the industry cycle is likely essential. Lenders can be very conservative in lending to industries during a cyclical bottom. So, management indicated some planning is in order before deciding how much to return to shareholders in the current environment. The last two industry bottoms have been absolutely brutal. In my mind, it would be really hard to be too conservative. Mr. Market, on the other hand appears to have completely forgotten the experience.

The most likely program would be a flexible stock repurchase program combined with an annual special dividend. Both of these could be discontinued in the event of a sudden downturn. But the real priority is to make sure that the company is ready for the worst because the “beyond worst scenario” happened in fiscal year 2020 (and that was one very scary event).

The company management is also open to acquiring more refining operations to protect more of the production from the volatility of the WCS pricing market. That would probably be by far a very wise move. The asphalt market, for example has to be far less volatile than the WCS market pricing (and more value added). The planning needed is to keep enough cash to be able to take advantage of the opportunity to acquire more refining capacity while maintaining a very conservative financial position in case the unexpected happens. The result was management naming a lot of “moving parts” and possibilities that Mr. Market had not patience for.

There were some questions about the hedging program. But the hedging program will shrink as more product is upgraded or refined. So, the prior importance of hedging before the merger no longer exists.

It is going to take some time for Mr. Market to get used to the new Cenovus Energy. Patient investors are likely to be rewarded some more as the improvements in reported results continue. Unlike Mr. Market, I will wait for this management to do things there way because I believe that is the wisest course. I can live with more uncertainty than the market can at the current time.

Be the first to comment