olm26250

Co-produced with Treading Softly

Do you have a timid friend? I think most of us do, if you don’t, you’re likely the timid friend.

My children all have various ranges of timidness or varying levels of risk tolerance.

My oldest is by far the most risk-averse, while her younger sister is the risk-taker.

However, they both like to do the same activities. No one likes to be left out. So my oldest will achieve the same result but often in a slower “less risky” method of achieving the goal. Her sister will dive in head first, filled with reckless abandon.

So when it comes to investing, investors come in every stripe. Some are rapid-fire traders, trying to leverage every penny of gain possible in a mind-numbing rapid pace of trading.

Others buy and hold for 50 years without ever giving a thought to selling a single share.

Some seek dividend growth and others seek high-yield immediate income. Some shockingly eschew dividends altogether!

Today, I want to offer up two excellent income investments for the lower-risk crowd. To do this, we are going to briefly look at two higher-yield investments with higher risk, but then climb up the capital stack. By doing so, we gain a closer place to the front of the payment line, while taking less risk. We can still enjoy an excellent income, albeit less, while seeing strong returns with lower overall risk.

We do this by moving into the preferred shares rather than the common shares issued by the companies. With preferreds we enjoy:

- Payment priority

- Less volatility due to call price and liquidation value having a fixed value

- Clear payment amount and timing

The downside with preferred securities is often:

- Less or capped potential upside

- Lower volume – which means it takes more time to fill out a large holding

So let’s look at two excellent preferred securities to lock in great income, with less risk to worry about.

Pick #1: TWO-C Preferred Shares – Yield 8.8%

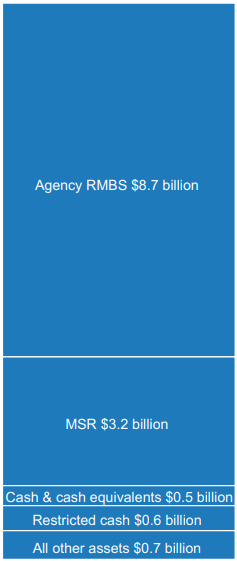

Two Harbors Investment Corp (TWO) is an mREIT (mortgage real estate investment trust) that sports a yield of 14.1%. Their primary focus is on agency MBS (mortgage-backed securities), which are low-risk investments as the principal value of the MBS is backed by a guarantee from the “agencies” Fannie Mae or Freddie Mac. If a borrower defaults, the agencies buy the loan back at face value.

Furthermore, TWO holds a large portfolio of MSR – mortgage servicing rights – where TWO collects the payments for mortgages and forwards those payments to the appropriate loan holders. For doing so, TWO gets a cut of the payment as their fee. MSR’s value shifts with the projected pre-payment rate of loan holders. If you pay your mortgage back faster than required, the MSRs have less value as they’ll generate less income for TWO or anyone else servicing your mortgage. With mortgage rates rising, MSRs are becoming more valuable as homeowners have less incentive to refinance their mortgages. (Source: TWO Earnings.)

TWO Earnings

In a rising rate environment, it’s less likely that mortgages will get refinanced or paid off early. So these MSRs are a valuable tool for mREITs to benefit from rising rates.

TWO is actually covering their common dividend. They generated $0.22 per share of earnings available to distribute while paying a dividend of $0.17 to common shareholders. All of this falls on the backdrop of TWO falling almost 20% year to date.

Two Harbors Investment Corp., 7.25% Series C Fixed-to-Float Cumulative Redeemable Preferred Stock (TWO.PC) is the preferred security issued by TWO. It is also down 18% year to date, but the key difference is that TWO-C is anchored by its $25 call value. TWO’s common share price will gyrate higher and lower; however, TWO-C has a set value for TWO to call it away.

Furthermore, the coverage of the common dividend is after the preferreds are paid. So TWO-C is extremely well covered while sporting a high almost 9% yield that income investors will enjoy without the risk of the common shares and their movements.

TWO-C also has an attractive yield-to-call of 17% assuming it is called immediately when it becomes callable in January of 2025. If TWO decides not to call it, TWO-C will start floating and pay a dividend equal to 3-month LIBOR + 5.011% on its $25 par value. At current LIBOR rates, that means TWO-C’s dividend would go up by almost 15%. If interest rates drop back down by 2025, then we can expect TWO-C’s price to rise back up to par as lower rates are generally favorable for the price of preferred.

So while the market may give common TWO shareholders a stomachache from the swing in value, TWO-C is a prime opportunity to climb up the capital stack and enjoy the excellent lower-risk income and protection from rising rates.

Pick #2: ARR-C – Yield 8.2%

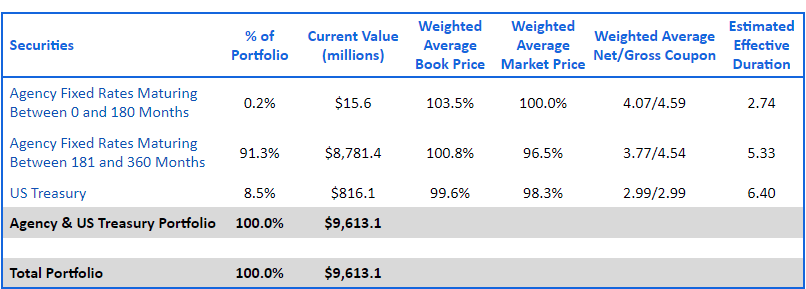

ARMOUR Residential REIT, Inc. (ARR) is another mREIT focused on Agency MBS investments. Their common shares yield 18.5% at this time. When we look at ARR’s portfolio, we can see they are laser-focused on Agency MBS, providing them a very low-risk portfolio of holdings. (Source: ARR Update – Sept 12th.)

ARR Company Update – Sept 12th

They also have a portfolio weighted towards a longer duration, meaning their portfolio is not set up to immediately benefit from interest rate hikes. The longer the duration, the less benefit is seen from rate hikes.

Looking at their earning power, ARR earned Q2 distributable earnings of $0.29 per share while paying a dividend of $0.10 a month. This means they are overpaying their dividend to common shareholders ever so slightly.

- Raised $79.7 million of capital by issuing 10,424,858 shares of common stock at $7.65 net proceeds per share, after fees and expenses, through at the market offering program.

- Repurchased 248,000 shares of common stock , at an average cost of $6.23 per share, pursuant to existing authorization.

ARR is also active in buying back shares on dips, and turning around and issuing new shares when the price moves above their book value. This buy and sell approach on their own shares has helped to increase book value, but it also means investors shouldn’t get overly excited when management talks up their share repurchases, they are just as ready to issue new ones again.

So instead of getting caught up in the common, we look higher up and see their preferreds – ARMOUR Residential REIT, 7.00% Series C Cumulative Redeemable Preferred Stock (ARR.PC). ARR-C sports an attractive high yield of 8.2%. Currently paying preferred dividends only costs ARR $3 million a quarter vs. their distributable earnings of $34 million, making their preferreds easily serviceable.

Furthermore, ARR-C has an attractive 14.5% yield to call – it is callable in January of 2025 – and pays its dividend monthly to preferred holders. So, while the common may one day face a dividend cut from an overpayment, the preferreds are easily covered and have little risk to their payment.

Taking a little less yield for a lower-risk high yield is the best action here in our mind as well.

Dreamstime

Conclusion

By buying mREIT preferreds, we can reduce the risk associated with lost share value or dividend cut risks, and instead lock in excellent income with high yields and high YTCs. TWO-C and ARR-C offer two lower-risk, high-yield preferreds to buy and enjoy until at least 2025.

I love to hold preferred securities and enjoy income. I view them as long-term buy-and-hold investments that require spot checking but not frequent trading. Others may enjoy trading in and out of preferreds, but for me and my income portfolio. I lock in an excellent yield or yield to call, and I let it do what I bought it for – paying me income!

This way I reduce the stress and amplify the enjoyment in my day-to-day life. You can do this too by applying this principle to your portfolio from our Income Method.

Be the first to comment