greenbutterfly

Investment Thesis

Zscaler (NASDAQ:ZS) has seen its multiple compress as investors shun high-growth cyber names in 2022. This led me to turn ”neutral” on ZS. However, I am now upgrading this stock to a tepid buy rating.

As we dig in, beyond the headline story, we have to come to terms with the fact that Zscaler’s growth outlook could now be slowing down.

On the other hand, I believe we can conclude that despite its slowing growth rates, its multiple has already derisked a lot in the past year.

Hence, I’m inclined to become tepidly bullish on ZS.

Cybersecurity, More Than Just a Story

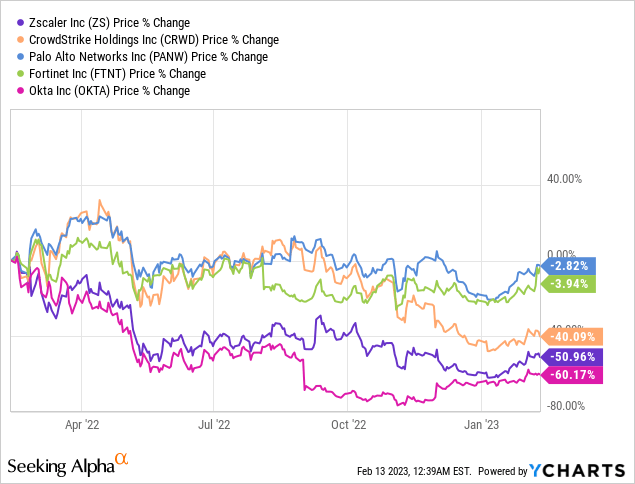

The cybersecurity sector had some gripping disruption in 2022. Geopolitical tensions revitalized the need for cybersecurity. At least that’s the narrative many cybersecurity players have attempted to pass on. But investors haven’t been all that convinced and believe that it’s probably just a story.

Indeed, the performance of cyber stocks in the past twelve months, since the events of last February took place appears to echo that insight.

Indeed, I believe what the graphic above shows is investors’ appetite for profitable cyber names. Not so much the fastest-growing cyber player that may or may not end up with the most market share.

The Key Question Facing Investors

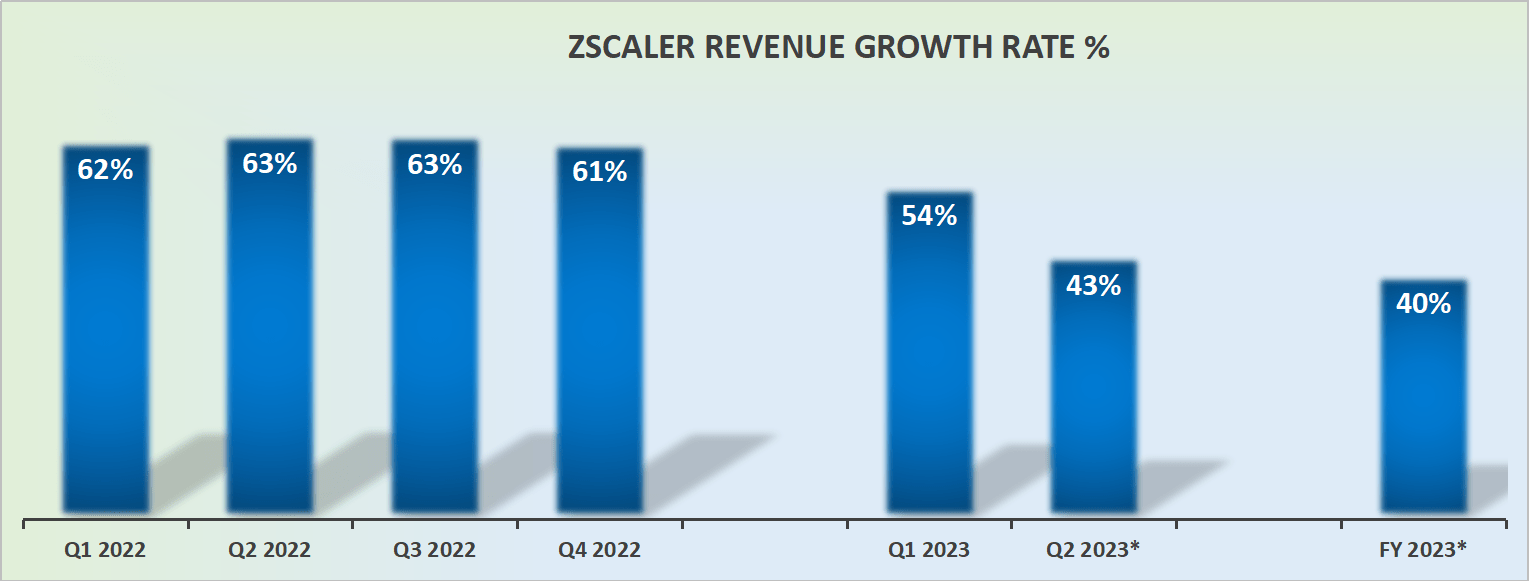

ZS revenue growth rates

As touched on already, the fact that Zscaler is growing at a rapid clip is certainly one of the most compelling aspects of this investment thesis.

The problem, though, is that investors no longer simply want just ”growth”. Because investors are fearful that these strong growth rates could fizzle out materially if the economic cycle was to slow down.

Case in point, commentary coming out of Microsoft (MSFT) and Amazon’s AWS (AMZN) both appear to echo this stance. The end customer is more discerning. Requesting more proof of the underlying value of the offering. Ultimately, leading to a longer sales cycle for Zscaler.

So, even though Zscaler is pointing to strong revenue growth rates right now, the unavoidable question that weighs on investor enthusiasm is what sort of growth rates will Zscaler exit in fiscal 2023 (ends July 2023)?

Indeed, recall that Zscaler’s billings last quarter were up 37% y/y. Remember, billings are a leading indicator of revenue growth rates. If billings fall substantially below a company’s growth rates, that could pose a lull in future growth rates. Could this imply that when Zscaler exits fiscal 2023, Zscaler will be growing at a sub-40% CAGR?

I’m not going to argue that sub-40% isn’t still a very fast growth rate. It clearly is. But it’s not the same as the +50% CAGR that Zscaler reported just a few months ago.

And yet, to be clear, it isn’t all bad when it comes to Zscaler.

Highly Free Cash Flow Producing

There’s some good news and bad news when it comes to Zscaler’s free cash flows.

Zscaler

The good news is that Zscaler is clearly reporting robust free cash flows. Indeed, as Zscaler points out, for fiscal Q1 2023, Zscaler reached a Rule of 80, making it a truly impressive output.

While on the other hand, the problem, is that Zscaler’s free cash flows don’t appear to be scaling alongside its revenue growth rates. In fact, it appears to be the case that the stronger its revenue grows, the less impressive its free cash flow margins become.

And then, to further compound matters, if the economic environment becomes even more challenging in the coming few months, one has to wonder how much further might this free cash flow compress.

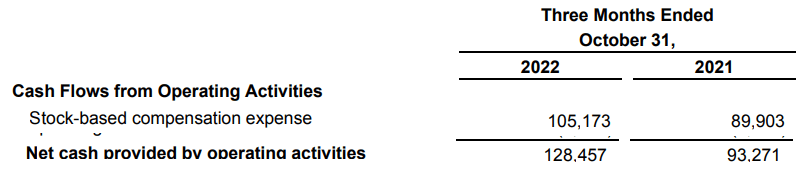

What’s more, as it stands right now, it appears that the bulk of Zscaler’s cash flows ends up as stock-based compensation.

Zscaler

In fact, for fiscal Q1 2023, Zscaler’s free cash flows of $96 million were less than management’s stock-based compensation of $105 million.

With that in mind, what sort of multiple makes sense for Zscaler?

ZS Stock Valuation – How to Think About its Valuation?

As alluded to, there are two key considerations at play here. In the first instance, in the present environment, it appears to be more challenging than in the past to forecast what a suitable and sustainable growth rate could be for Zscaler.

Accordingly, even if we assume that management is lowballing its revenue guidance, and ultimately beats the top end of its fiscal Q2 2023 guidance by 500 basis points and reaches 48% y/y growth rates, that would still be a 600 basis point deceleration from the previous quarter.

And the whole thing with investing for growth is that nobody wants to invest in a company that’s seeing its growth rate decelerate.

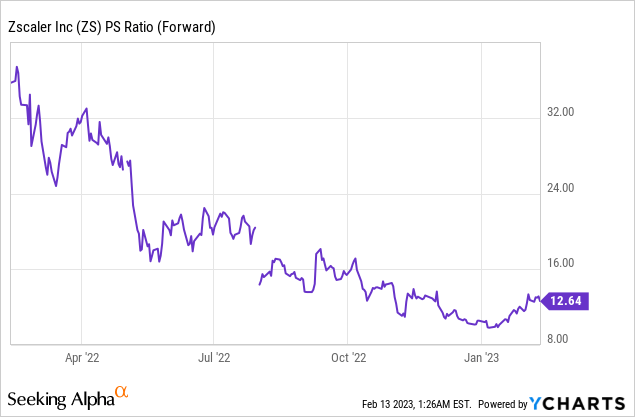

On the other hand, consider this multiple compression.

As you can see here, Zscaler’s multiple to sales has already been cut down by more than 50%. Indeed, closer to a 65% reduction compared with this time last year.

The Bottom Line

There’s no doubt in anyone’s mind that Zscaler has seen the multiple that investors are willing to pay for its stock come down. There’s some element of this multiple compression that is justified. After all, in hindsight, the stock was just too expensive, particularly in 2020-2021.

But a part of me wonders whether this multiple has now compressed as much as it makes sense. Hence, I believe that the risk-reward now is the best it has been for a while.

Be the first to comment