Given the rapid change in economic conditions, enterprises and people have adapted to living and working from home, something we would have thought as nearly impossible only a few months ago. The clear beneficiaries of this work-from-home trend are technology and cloud-based companies that have made this migration as seamless as possible.

Zscaler (ZS) is one of these companies who have benefitted from significantly increased demand related to internet security. As companies move their employees to a work-from-home model, internet security has become increasingly more important. The increased demand will surely accelerate the company’s revenue growth and expand their market share, however, investors should still be cautious around investing in high-valuation names.

While the company continues to have a significant opportunity to disrupt the cloud-based security market, valuation has risen over the past few months as the stock has gone up over 40% year-to-date. While investors are riding the bullish train on companies benefitting from the work-from-home transition, valuation should still be a concern for long-term holders.

Historically speaking, ZS has consistently beat their quarterly expectations and investors have become accustomed to big revenue beat and raises. Even if ZS does not continue to provide guidance metrics given the significant uncertainty around the global pandemic, investors are likely to expect heightened growth patterns for at least the next several quarters.

One of the biggest questions is whether or not ZS will be able to execute on this heightened demand patterns and at what point do things normalize, thus potentially deflating the company’s valuation multiple. Competitors are also experiencing increased demand and there could eventually been a shake-out among leaders of the group. I believe ZS could become a clear leader of internet security, though as these price levels, I am a little more cautious around putting money into the name.

Brief Q2 Earnings Recap

Revenue during the quarter grew 36% to $101.3 million, which was only ~$2 million ahead of expectations for ~$99 million. Revenue growth did however decelerate from the 48% seen in Q1, which could partially be a factor of the law of large numbers. Even more challenging is the company’s billings, which grew only 18% during the quarter, down from the 37% growth seen last quarter.

Source: Company Presentation

Source: Company Presentation

Billings are known for being a good indicator of future revenue growth as they represent deals the company has won but has not yet converted into revenue. With billings growth decelerating to only 18% growth, the underlying trends in the business may have started to slow down. These figures are somewhat irrelevant today because of the large demand spike caused by the work-from-home trend. However, once demand starts to normalize, investors will have a heightened awareness of billings growth trends.

Operating margins were a little weak, coming in at 11% during the quarter, down from 13% in the year ago period. Over time, investors are expecting margins to expand as the company gains scale and is better able to leverage their operating expense base. However, in the near-term, it seems like the company is sacrificing some of their margins for continued strong growth. With the company planning on expanding their sales headcount during this year, operating margins are likely to remain under pressure during the near-term.

Source: Company Presentation

Source: Company Presentation

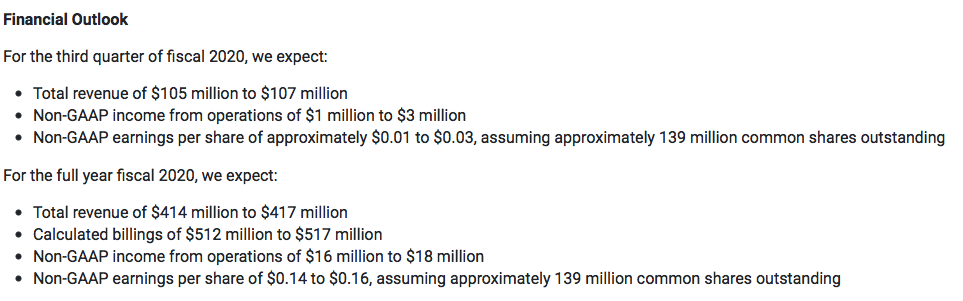

The company also provided updated guidance which includes full-year revenue of $414-417 million, up from their previous guidance range of $405-413 million. Billings were also raised to $512-517 million, up from $500-510 million. However, given the significant change in demand over the past few weeks, investors should not place a lot of weighting on their current guidance.

Valuation

Given the 40%+ year-to-date performance, valuation has increased as well. I believe ZS remains a great position to have in a long-term portfolio, however, investors should be aware of a few items before making an investment.

First, the company’s billings growth seems to be slowly decelerating prior to the global pandemic caused enterprises to transition to work-from-home models. The increased demand could last for several quarters, and potentially longer if working-from-home becomes a long-term trend. Second, margins have remained under pressure, though the company is investing heavily into their workforce. Finally, valuation, the stock’s valuation has increased significantly and is now a bit of a risk to the name

Using TTM revenue for ZS of ~$360 million, we can start to generate different potential outcomes related to growth and valuation. With a current market cap of ~$8.7 billion and net cash of ~$400 million, the company has a current enterprise value of ~$8.3 billion.

First, let’s assume growth trends accelerate from the current ~30% rate and grow ~40% over the next year. This could result in revenue of ~$500 million, which implies a current valuation of ~16.6x forward revenue. While this multiple doesn’t seem too expensive, we are also assume revenue growth accelerates quite significantly over the next year.

Next, let’s assume the growth rate remains pretty stable at ~30%, which would imply revenue of ~$470 million and imply a revenue multiple of ~17.7x, a somewhat expensive premium to pay for a company who has seen margin pressure and cash flow challenges.

Finally, let’s assume revenue growth slows down as competition increases and the work-from-home trend is short-lived. While I believe this is unlikely, if revenue were to grow only ~20%, similar to their recent billings growth, we could see revenue of ~$430 million, which would imply a loft forward revenue valuation of ~19.3x. Investors who are skeptical of the next 12 months of revenue growth are surely to be scared away from a near 20x forward revenue multiple.

Even though ZS is likely to be a beneficiary from the global pandemic, I am hesitant to put new money to work given the current valuation is already baking in strong revenue growth over the next year. My concerns over underlying billings growth and margin trajectory outweigh my optimism that revenue growth will meaningfully accelerate, thus implying a more reasonable forward revenue valuation.

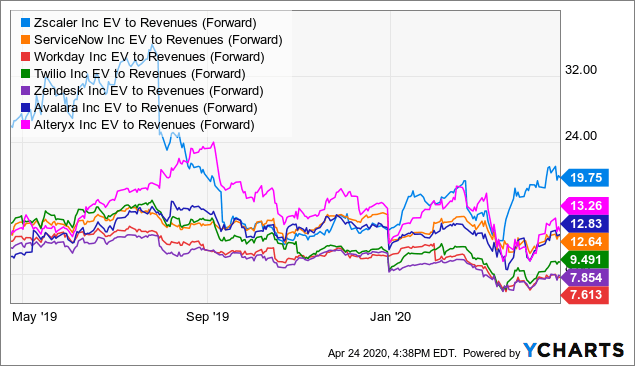

The valuation chart above does a good job demonstrating several other software and cloud-based technology names that have 20%+ revenue growth and trade at a much more reasonable forward revenue valuation. While I remain a long-term bull of ZS given their leadership position in internet security, I remain on the sidelines for now until we are better able to understand medium-term revenue growth and margin trajectory.

Risks to the name include a continued slowdown in billings growth as new sales may be more challenged given the stay at home order many states and countries are currently under. This may make future revenue growth lumpier as larger contracts may become more common. Other risks include increased competition from legacy vendors who are also likely experience increase in demand given the shift to work-from-home. The high forward revenue valuation also poses a risk as investors are typically harsher on growth names when the market goes through a correction phase.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment