nathaphat/iStock via Getty Images

Thesis highlight

ZoomInfo Technologies (NASDAQ:ZI) has 28% upside. ZI offers a comprehensive solution for marketing and sales teams, providing precise and thorough data and insights on businesses and individuals they are trying to reach. ZI’s strength in artificial intelligence and machine learning sets it apart from competition, allowing for high-volume intelligence delivery through an AI- and ML-enabled engine that sifts through massive amounts of data from millions of sources. This helps businesses to identify the best target customers, zero in on the right decision makers, obtain updated predictive lead and company scoring, and improve overall sales and marketing strategies.

Company overview

ZI offers marketing solutions. The business’s services include marketing and advertising, customer relationship management, lead generation, data warehousing, and development of individualized strategies.

Marketing is crucial to every business

It’s impossible to overstate the importance of sales and marketing to any business’s bottom line. Therefore, companies often allocate sizable resources toward advertising and promotion. A wide variety of departments are involved in sales and marketing. As such, it’s crucial for these teams to be in sync and have access to the right tools, platforms, and content in order to put their strategies into action.

Previously, B2B businesses had to rely on field sales representatives and paper-based sales processes before the development of modern sales and marketing tools. Salespeople conducted one-on-one meetings to gather data, which was then stored in physical forms. This method relied on manual labor, was time-consuming and costly. Data collected was shallow, sparse, and inaccurate, and it quickly lost its value after being recorded. Without efficient strategies for finding new accounts to target on a large scale and with consistent success, many sales representatives instead concentrated on keeping their current clientele happy. In addition, sales representatives frequently kept their own knowledge to themselves and did not disseminate it to the rest of the company. Salespeople took their contact lists and any relevant data about their clients with them when they left one company for another. There was a lack of scalable methods for businesses to collect, share, and use data across their operations.

To solve these issues, companies have made investments in cutting-edge technological tools for a complete digital overhaul of their marketing and sales operations. The primary motivation for implementing CRM systems was the improvement of sales management. These customer relationship management systems also enabled the digitalization of salespeople’s contact lists and the centralization of data for widespread dissemination. Despite the investments, most businesses rely on manual processes to collect the data that powers these systems. As a result, CRM and sales and marketing automation [SAM] data is often out of date, inaccurate, incomplete, and lacks sufficient breadth and depth.

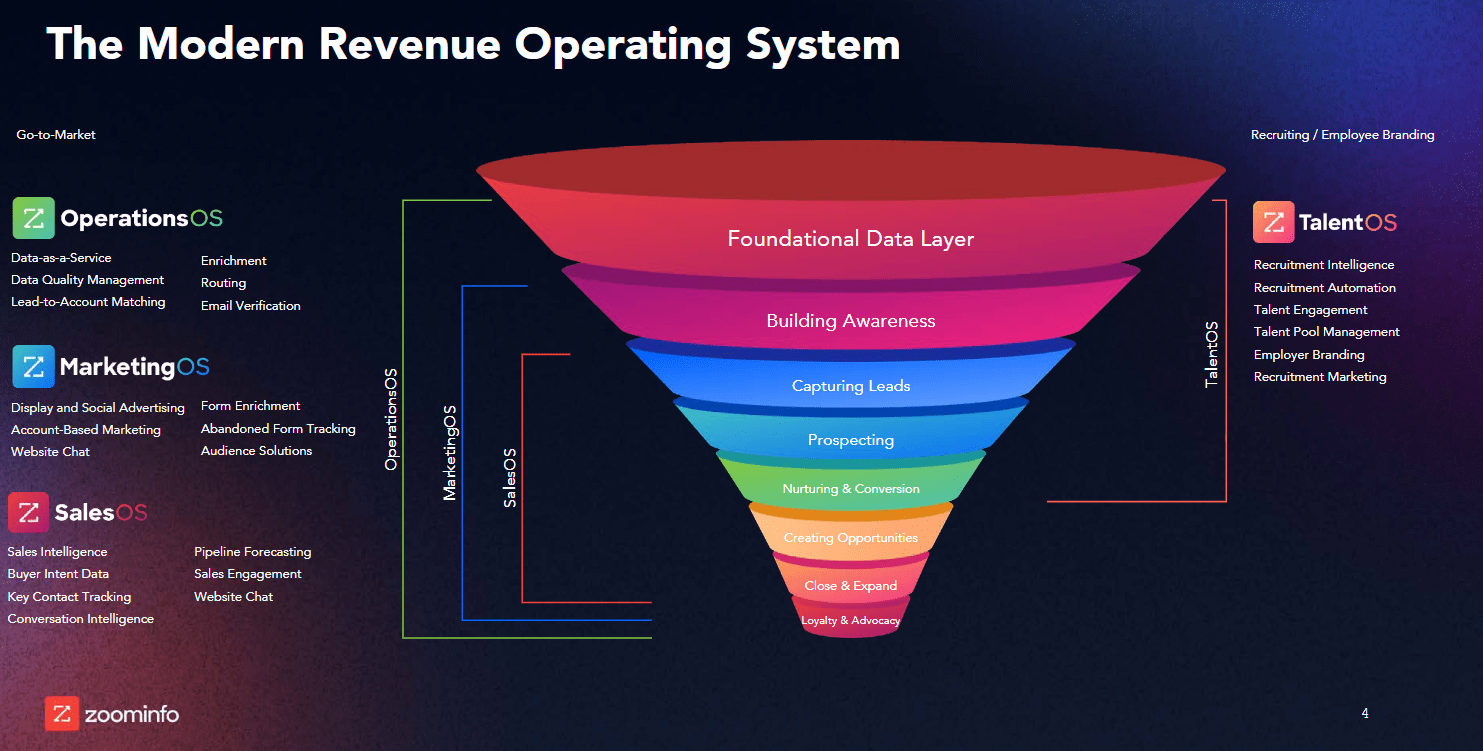

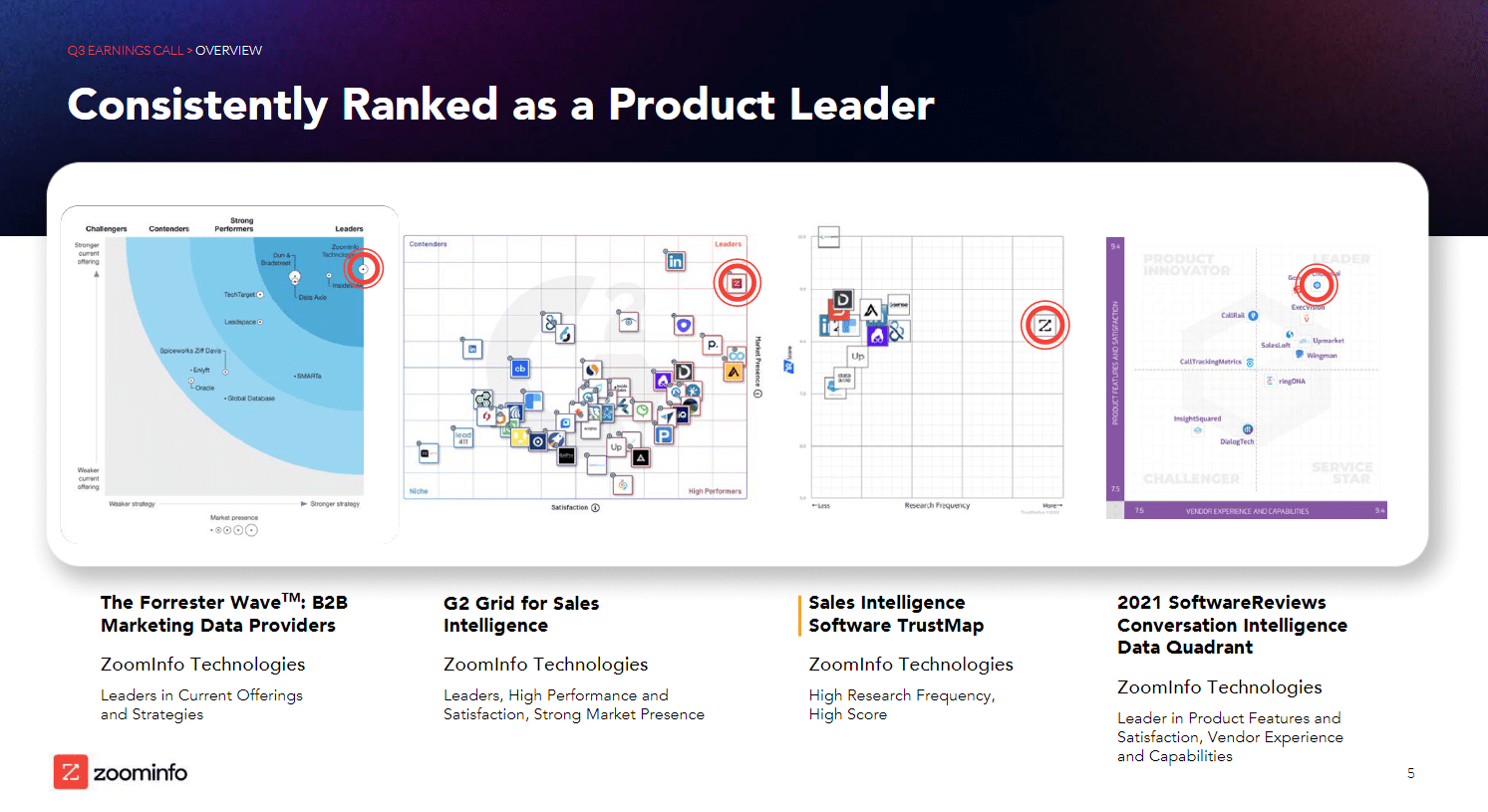

ZoomInfo offers a leading comprehensive solution

As of 3Q22, ZI is the premier go-to-market intelligence platform for over 30,000 business teams around the world. Its cloud-based platform provides sales and marketing professionals with precise and thorough data and insights on the businesses and individuals they are trying to reach. In combination with ZI analytics, the comprehensiveness of this view helps to reduce sales cycles and improve win rates by ensuring that the right marketing pitch is made to each prospective buyer.

In short, ZI helps its users to efficiently identify potential customers, target the correct individuals within those companies, access frequently updated predictions for leads and company performance, track purchasing signals and other relevant information about potential clients, create effective messaging, utilize automated sales tools, and manage the progress of deals.

3Q22 earnings 3Q22 earnings

Strong AI/ML capabilities

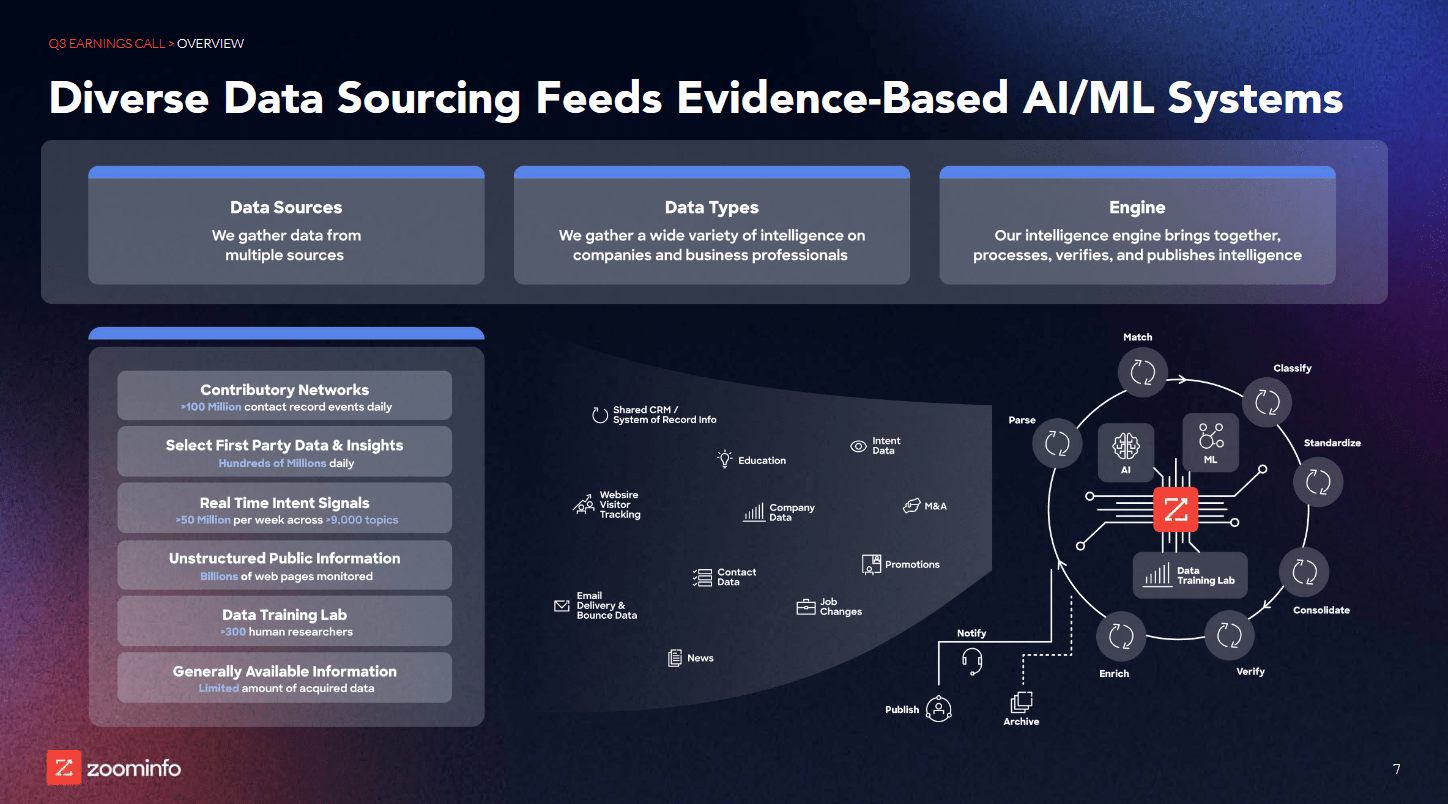

ZI’s strength in artificial intelligence and machine learning sets it apart from the competition. ZI’s high-volume intelligence delivery is made possible by an AI/ML enabled engine that sifts through massive amounts of data from millions of sources. To achieve this goal, they collect and categorize information from a vast array of public and private databases. ZI algorithm then ranks, scores, and makes decisions daily based on these data points. ZI’s AI/ML team have extensive experience in cleaning B2B data, which they use to help train ZI’s AI and ML technologies and expand its contributory network. In my opinion, this human touch has a crucial function because they ensure high quality and fill in gaps that machines cannot.

3Q22 earnings

Effective GTM model with target set on enterprise market

ZI’s go-to-market strategy is highly effective, as evidenced by the fact that its S&M percentage of sales is in the mid-to-high 20% range. One reason for this is the efficient go-to-market mechanism built into ZI, which allows for rapid responses and rapid closing times. Many of the leads the business receives are inbound, as customers increasingly look to automate their sales processes.

In addition, the company has been putting more effort into upselling customers to the new platform, which has a higher price point and could lead to the sale of more seats. Upmarket sale penetration is an area where ZI has made successful investments. The number of customers whose ACV is over $100,000 has increased to 1,848 in 3Q22, a huge increase from 1Q21 thanks to this strategy.

A powerful network effect is also fueled by this growth in customers. The increasing size of ZI’s contributory network has resulted in a daily increase in the number of records it receives from our system. The depth and breadth of ZI’s intel improves in tandem with the size of its contributory network. Customer value increases as a result of more data and better market intelligence thanks to an increase in the number of users.

Stock down but unit economics looking good

Due to a significant slowdown in leading indicators like billings and RPO, ZI stock has dropped by over 40% since it reported earnings. ZI’s RPO increased by 38% compared to 52% in the previous quarter, and billings grew by 28%. The deal delays that began in early July and are expected to last through early CY23 are reflected in this cautious FY22 revenue guidance of 46% growth, in my opinion. I think it’s great that, despite growth slowing, management is still dedicated to keeping operating margins at 40%.

That aside, ZI focus on capturing the upmarket opportunity is highlighted by the momentum in enterprise customer growth. The enterprise market’s larger deal sizes and higher retention rates are likely to contribute to revenue growth. Another positive thing to highlight is that, even with the ongoing investment in international go-to-market strategy and new product development, the company is able to maintain efficiency in the model by keeping S&M costs below 30% and R&D spending below 13% of revenues. As such, operating margins for ZI should remain around 40% even with rapid expansion and a growing top line. Strong customer momentum, a move to the enterprise market, an expansion of the TAM to include use cases like human resources candidate sourcing, and consistent profitability and strong FCF generation all point to ZI having unit economics that are above average.

Valuation

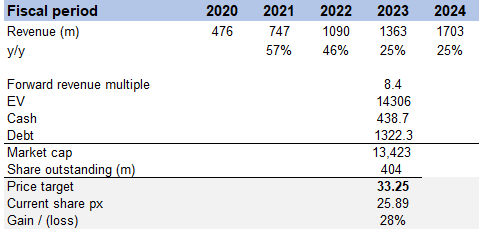

My model suggests that ZI is worth $33.25 in FY23. The core part of my thesis is that ZI is able to continue consolidating market share by offering a critical solution that businesses need. On top of that, it should be able to continue penetrating the enterprise market, thereby diversifying its revenue base away from SMBs and also improving unit economics.

I believe the slowdown in growth is inevitable given the weak macro environment, as such I modelled ZI to grow 50% slower than the past, which is still a healthy growth rate, in my opinion. This is considering that ZI management reaffirmed their outlook for 40% long-term operating profit margin.

Suppose ZI grows as planned, ZI should be able to generate ~$1.7 billion in revenue in FY24. Attaching the current forward revenue multiple here would suggest a 28% upside.

Own valuation

Risks

Increase in competition is a worry

ZI’s value proposition could be threatened by larger software companies as they try to cash in on the broad secular trend of Customer 360. Despite the fact that ZI has developed a unique platform, I believe that as CRM vendors and legacy data providers seek new avenues for expansion, they will eventually pose a threat to ZI’s market dominance.

Exposure to SMBs

The small and medium business sector still accounts for a sizable share of total revenues despite having a significantly lower net retention rate than the enterprise sector. Net new ACV may suffer again if the economy experiences a downturn. While a rise in the enterprise mix will help reduce some of the SMB risk, it won’t eliminate it entirely. ZI has apparently been able to successfully adapt its SMB go-to-market engine for the enterprise, but there is a chance that the company will run into short-term execution issues as it expands its enterprise sales force.

Conclusion

ZI provides an end-to-end answer for businesses in need of accurate and detailed information about the companies and people they are trying to reach for marketing and sales purposes. ZI’s superiority in these areas gives it a leg up on the competition, allowing for rapid dissemination of intelligence via an AI- and ML-enabled engine that sifts through data from millions of sources. This allows businesses to better focus their sales and marketing efforts on the most profitable customers, learn more about their ideal decision-makers, obtain more accurate predictive lead and company scoring, and increase their overall customer base.

Be the first to comment