SDI Productions/E+ via Getty Images

Zoom Video Communications, Inc (NASDAQ:ZM) became a social sensation during the COVID-19 pandemic, when consumers used video conversations to stay in touch with family and friends. Demand for Zoom’s cloud-based services increased as demand for remote learning and telemedicine expanded, and Zoom raised its investment in computer servers as demand climbed.

Zoom’s business grew during the pandemic’s early days and sales for fiscal 2021 surged 326% over fiscal 2020, powered by the work-from-home trend, and by October, ZM stock had surged.

However, as vaccinations were distributed, in-person meetings resumed, and workers returned to their offices during the pandemic, Zoom’s revenue growth slowed, leading some investors to believe Zoom Video Communications was just a pandemic stock and its relevance had passed.

Zoom Share Price (Finviz)

Q1-23 Earnings Release

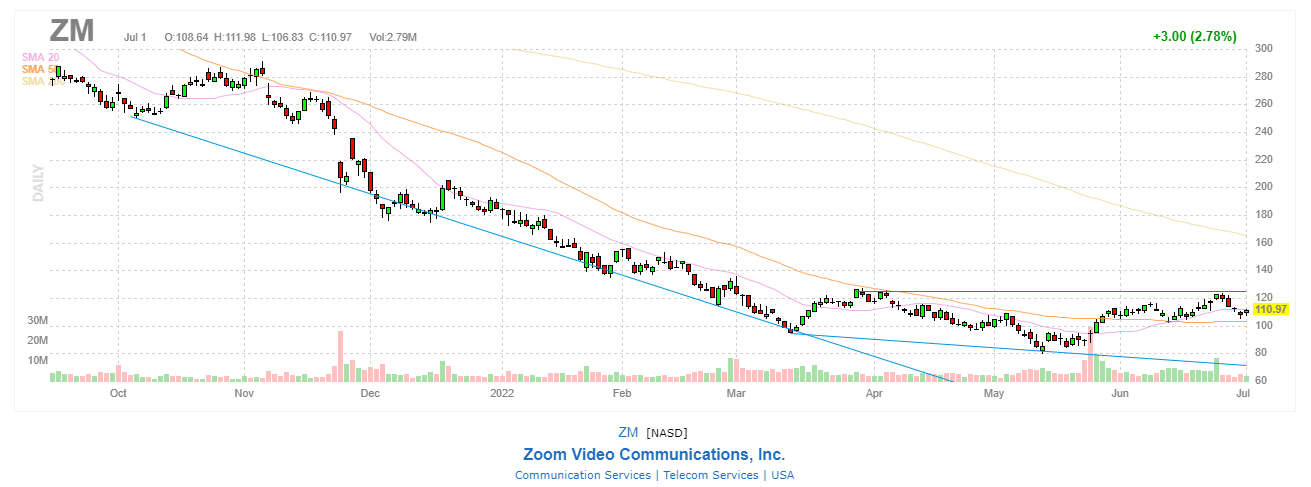

ZM stock has been declining all this year, but it is on the verge of a rally. On May 23, 2022, Zoom Video Communications released its Q1-23 results for the quarter ending April 30, 2022.

Zoom Video Communications reported revenue of $1.07 billion in Q1-23, a 12% increase YoY, driven by continued success in its platform offerings such as Enterprise, Zoom Rooms, and Zoom Phone. The company also maintained strong profitability and cash flow, with a GAAP operating margin of 17%, a non-GAAP operating margin of approximately 37%, an operating cash flow margin of approximately 49%, and an adjusted free cash flow margin of more than 46%.

Zoom Video Communications is also financially sound, with $5.7 billion in cash, equivalents, and marketable securities on its balance sheet. While growth is expected to slow, Zoom has already proven to be highly profitable.

Revenues for the Q2-23 are expected to range between $1.115 billion and $1.120 billion, with revenues for the full year 2023 expected to range between $4.53 billion and $4.55 billion.

Growing Rivals

Video calling, according to ZM stock bulls, is here to stay and will play a far larger part in enterprises, schools, and everyday life. The problem is that Zoom’s competitors also believe there is a large market opportunity and do not want Zoom to dominate this space alone.

With its Teams collaboration capabilities, Microsoft (MSFT) poses a significant challenge. In December of last year, Microsoft released Teams Essentials, a low-cost standalone product aimed towards small enterprises.

Other expanding competitors in the business market include Google parent Alphabet (GOOGL), RingCentral (RNG), Cisco Systems (CSCO), LogMeln, and Fuze.

Zoom still controls nearly half of the global video-conferencing industry with a 48.7% share, while Google Meet trails far behind with 21.8%. To maintain its dominance in this market, Zoom is going all-in on workplace communication and appears eager to embrace the capabilities of AI technology.

AI To Play Significant Role In Zoom’s Growth

As firms across the industrial spectrum have been compelled to embrace new tools in a world that has swiftly rushed toward remote labor and digital commerce, the cloud contact center market is expected to grow to $45.5 billion within four years, up from $11.5 billion in 2020.

Zoom intends to be a big participant in the contact center market with its own products and services, and AI software will almost certainly play a significant role.

Zoom Contact Center

Zoom initially announced plans to purchase cloud contact center startup Five9 (FIVN), but the $14.7 billion deal fell through when Five9 failed to garner sufficient shareholder backing. Zoom’s stock dropped dramatically after the announcement, but five months later, Zoom officially introduced Zoom Contact Center, their own contact center product.

In May, Zoom also completed its acquisition of Solvvy, a developer of conversational AI technology that would help to expand its Zoom Contact Center product offering. This is only one part of its push to offer and extend additional corporate workflows on its platform.

Zoom has also made a financial investment in Observe. AI, a firm that uses artificial intelligence for contact center apps, as well as purchasing German startup Karlsruhe Information Technology Solutions, which provides artificial intelligence-powered real-time language translation solutions.

Zoom’s Evolving Product Categorization

To further increase its market possibility for future growth and expansion with its customers, Zoom has recently unveiled the latest evolution of its communication platform with the rollout of offerings such as Zoom Whiteboard and Zoom IQ for sales teams, not to mention the launch of Zoom One services, whose announcement resulted in the company’s shares increasing by nearly 1.2% on June 24, 2022.

Zoom Phone

Zoom Phone, a cloud-phone business communication solution with enterprise-grade functionality, has had remarkable success since its inception in January 2019, growing from zero to two million licenses in just over two and a half years, and doubling from one million to two million paid seats in less than nine months.

Recent significant enterprise wins include health insurer Humana, which purchased 24,000 Zoom Phones, and Avis Budget Group, which purchased over 10,000 Zoom Phones.

Zoom Phone reached an incredible three million seats during Q1-23.

Acquiring New Customers And Expanding Across Existing Customers Is Key

Retaining small businesses as well as large accounts will be critical to Zoom’s future as the coronavirus crisis subsides. While paying consumer subscribers are crucial, Zoom’s origins are in the enterprise sector, and the company’s goal is to convert monthly business subscribers to attractive annual contracts.

Renewals for customers with 1-10 employees are projected to drop as the economy recovers, and it remains to be seen how well Zoom can sell its premium packages to the enterprise sector – although recent client metrics appear to be robust:

Zoom has about 200,000 enterprise clients at the end of Q1-23, a 24% increase over the same quarter previous fiscal year.

Furthermore, the amount of larger organizations using Zoom’s platform and providing more than $100,000 in 12-month trailing (TTM) revenue is the main measure to monitor. This particular customer base increased 45.9% to 2,916 in Q1-23, demonstrating Zoom’s ability to grow its clientele despite the world economy’s downturn. These customers will give more consistent, long-term revenue than smaller customers.

My Conclusion

Zoom Video Communications faces short-term obstacles from the macroeconomic background and the reopening of the economy, but the company’s long-term business prospects remain good. Its growth rate has slowed significantly, yet the company continues to attract new consumers on a regular basis.

With shares down 38% YTD and 70% in the past year, combined with continued commercial opportunities and the incorporation of AI technologies, I believe Zoom Video Communications is as viable as ever and that now is a fantastic moment to buy shares of the video-conferencing behemoth.

Be the first to comment