MicroStockHub/iStock via Getty Images

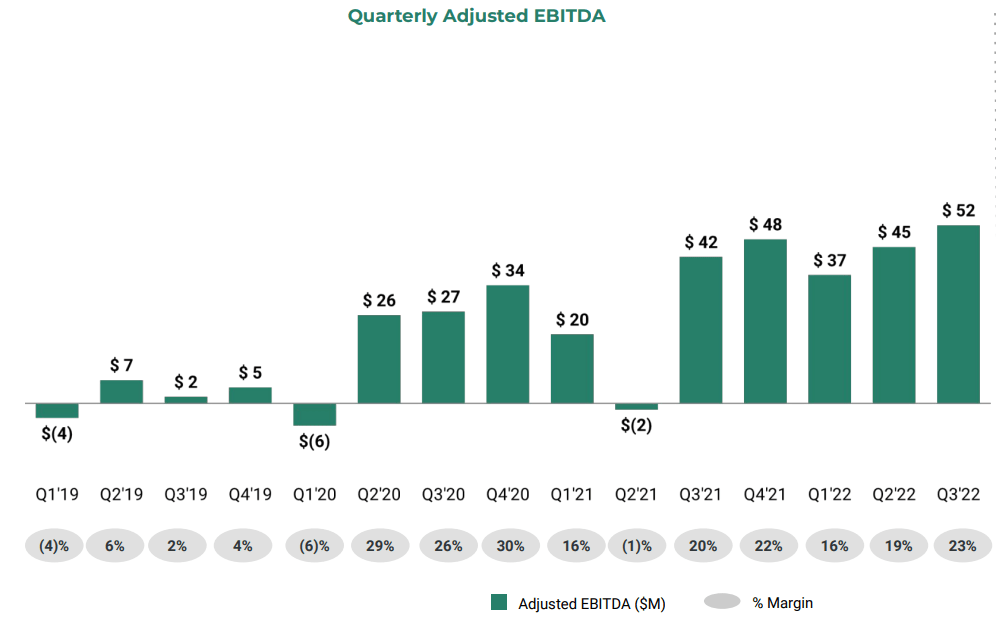

ZipRecruiter (NYSE:ZIP) exceeded the high end of its previous quarterly guidance, delivering $227 million in revenue, an increase of 7% when compared to Q3 of 2021. Adjusted EBITDA came in strong at $52 million and GAAP net income was $20.6 million.

The company reported that the cooling off of the job market continues, which is a trend that began in Q2 of 2022.During the last earnings call ZipRecruiter noted that they saw things start to cool down, specifically in June, and that same cooling generally continued throughout the quarter in Q3.

One thing we found particularly interesting discussed during the Q3 earnings call was that the company has made tremendous progress integrating its product with third party systems. As of Q3, it has now completed integrations with over 140 applicant tracking systems. This makes it easy for new enterprise customers to activate ZipRecruiter as a recruiting solution, it creates a better experience for jobseekers who never need to leave ZipRecruiter to apply to these employers jobs, and it represents an ever-increasing moat to competition given that implementing so many integrations has taken nearly a decade for the company and competitors would have a hard time replicating it.

Another interesting piece of news was that in Q3 the company updated their entire meta-learning model to include an algorithmically-driven prediction of a jobseeker’s likelihood of applying. This update delivered an 8% increase in invites sent by the average employer and a 15% increase in the number of responses received.

Q3 2022 Results

Third quarter revenue of $227 million exceeded the high end of the guidance provided by the company in August. It is reflective of a cooling hiring environment as well as facing particularly challenging comparisons against Q3 of 2021 when the company grew 107% y/y in the post-Covid reopening of the economy.

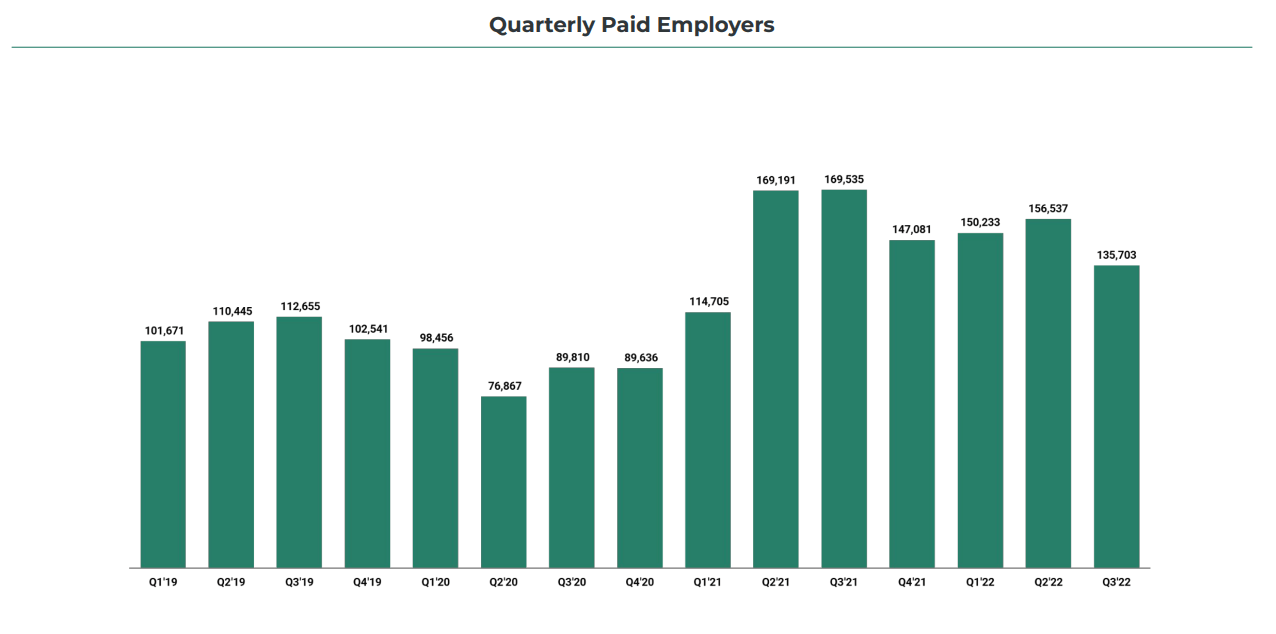

Paid employers were 136,000, representing a 20% decrease versus Q3 of 2021 and a 13% decrease versus Q2 of 2022. Importantly, Q3 revenue per paid employer went up 33% y/y, helping to compensate the loss of paid employers.

Financials

Adjusted EBITDA margin was 23%, 3 percentage points higher than Q3 in the prior year. As a reminder, the company has a 30% long-term EBITDA margin target, which it hopes to reach through operating leverage.

We believe that the fact that the company has a positive operating and EBITDA margin, despite being relatively young, is a reflection of the quality of the business as a platform with competitive advantages and good management.

ZipRecruiter Investor Presentation

Growth

Not surprisingly, as the job market has cooled off revenue growth has become more difficult for the company. This can be seen in the much lower growth rate of ~7% this quarter, compared to the much higher growth rates delivered in some of the previous quarters. Still, revenues are still coming in at more than 2x those of 2019.

ZipRecruiter Investor Presentation

One metric that shows particular weakness is the number of paid employers, which has been going down since it peaked in Q3 2021.

ZipRecruiter Investor Presentation

Fortunately for the company the average employer has been increasing their spend on the platform, which helped the company deliver an all-time high revenue per employer of $1,673 in Q3 of 2022, up 33% year-over-year.

ZipRecruiter Investor Presentation

Answering a question during the Q&Q session of the earnings call, CFO Tim Yarbrough explained what is driving this increase in revenue per paid employer:

Two big things driving revenue per employer, you are right, 33% up year-over-year, up sequentially as well. There is two big drivers. One would be our marketplace fundamentally works like an auction. So employers, especially as they age with us, they tend to spend up over time and that can show up in a bunch of different ways, but they can post more jobs or broaden their distribution or reach of their job adds over time, and that’s a trend that we’ve seen consistently over the many years that we’ve been doing this. The second big driver is our slow and steady push towards the enterprise side of our – side of the business. So assuming way out, we’re still getting started on enterprise we see it as roughly half of the overall market. We saw the percentage of performance-based revenue, which is a pretty good indication of our enterprise business we saw that increase to 23% of total revenue versus 19% last year. And then the total raw dollars increased by 29%. So we expect that trend to continue. But as that trend does continue, that will push up the revenue per employer over time, likely.

Balance Sheet

Cash and short-term investments were $669.7 million at the end of the quarter, compared to $699.9 million at the end of Q2. The decrease, despite the company being profitable, was primarily due to $53.5 million spent on the repurchases of 3 million shares during the third quarter. ZipRecruiter ended the quarter with $541 million in long-term borrowings.

The company announced that its Board of Directors has authorized a $200 million increase to the company’s share repurchase program, which is in addition to the previous authorization of $250 million in total earlier in 2022.

Guidance

The company guided Q4 revenue to be $206 million, which represents a 6% decline year over year. This reflects the continued softening in the labor market. Q4 adjusted EBITDA guidance of $42 million equates to 20% adjusted EBITDA margin.

Valuation

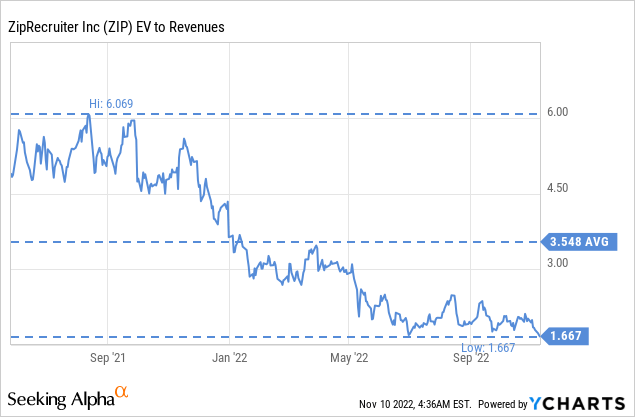

Despite the company guiding to a revenue decline y/y in Q4, and the job market continuing to cool off, we still view shares as attractively priced despite the headwinds. The company does not have an extensive history in the public market, but still, the valuation multiples are close to their lowest they have even been since its direct listing. The EV/Revenues multiple is currently at ~1.7x, which is about half the average since the company went public.

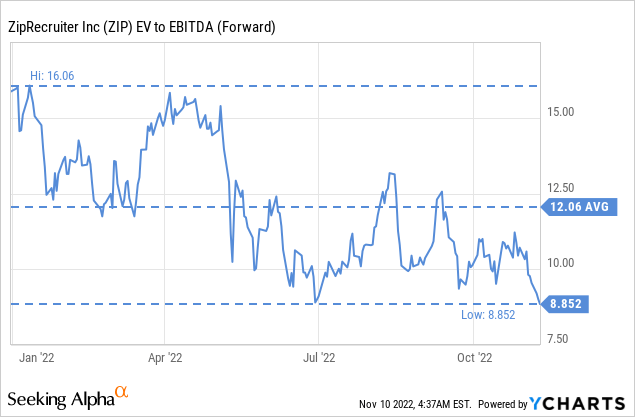

Forward EV/EBITDA is also close to an all-time low at ~8.8x, and we consider this an attractive multiple given that the company is a quality platform business, which long-term still has significant room to grow.

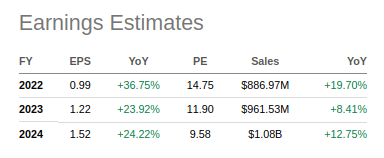

The forward price/earnings ratio is also relatively low at ~14x, with analysts expecting earnings to continue growing for the next few years. Based on 2024 earnings estimates, shares have a single digit p/e ratio.

Seeking Alpha

Risks

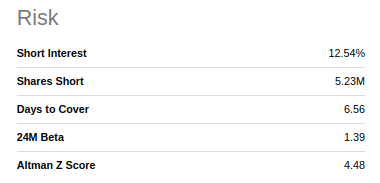

We continue to view Microsoft’s (MSFT) LinkedIn as the biggest risk to the company. If LinkedIn improves its platform it could take away customers from ZipRecruiter in a meaningful way. There is also the risk of a severe deterioration of the job market, although we consider this to be more of a cyclical trend that would eventually turn around. Risks are mitigated by the fact that the company has reached GAAP profitability, and that it has significantly more cash and short-term investments than long-term debt.

Seeking Alpha

Conclusion

ZipRecruiter delivered what we consider to be a relatively strong quarter given the headwinds. Guidance for next quarter is not great, but understandable given the cooling off of the job market. Still, we believe shares already reflect the headwinds and are attractively priced. The forward price/earnings and EV/EBITDA are relatively low for a quality platform business. The company seems to agree given the increase in the authorization to repurchase more shares.

Be the first to comment