Jorge Villalba

ZIM Integrated Shipping (NYSE:ZIM) is expected to submit its earnings card for the fourth-quarter in the first week of March. With shipping rates stabilizing at the end of FY 2022, I believe ZIM Integrated Shipping’s Q4’22 earnings could be slightly better than expected. The shipping company benefited from high contract rates throughout FY 2022 which protected ZIM Integrated Shipping from the collapse in market rates, but the outlook for the firm’s FY 2023 EBITDA is likely going to be depressing. Although risks have decreased lately, shares continue to have an unattractive risk profile!

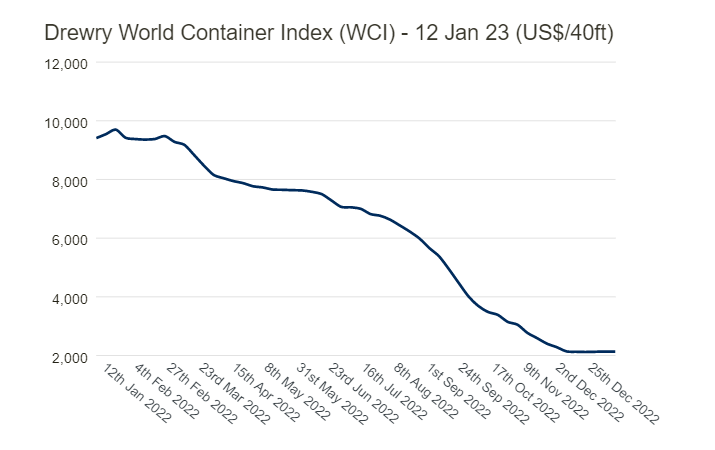

Drewry composite index and pricing environment

According to the Drewry World Container Index, freight rates for shipping a 40 foot container stabilized in December and have not fallen for four straight weeks. Shipping a 40 foot container cost companies $2,132 per container in the week ending January 12, 2022. Since the first week of December freight rates appear to have stabilized in a range of $2,120 and $2,140 per 40 foot container. Still, freight rates have fallen precipitously in the last twelve months: they are down 78% year over year and about 80% from their peak in September 2021. While it is too early to say that freight rates have definitely bottomed this cycle, the pricing environment did improve compared to November when freight rates were still in freefall.

Source: Drewry

3 key metrics to watch

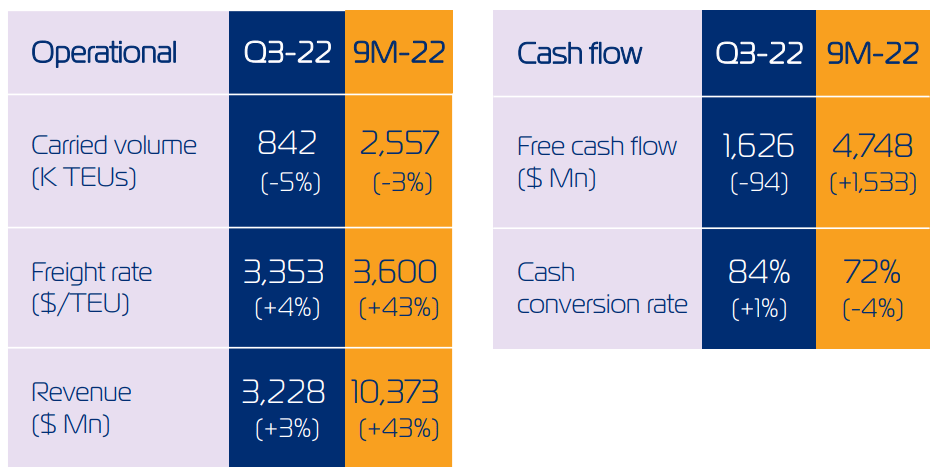

Freight rates are always a function of demand and transportation volumes. With volumes dropping, shippers have less pricing power and contract rates are primed to fall. ZIM Integrated Shipping’s average freight rate was $3,600 in the first nine months of FY 2022, showing an increase of 43%. Pricing pressure is likely to drive contract freight rates lower in FY 2023 and the average freight rate for FY 2022 is likely to be one of the most important key metrics for ZIM Integrated Shipping’s Q4’22 earnings sheet.

Free cash flow is another key metric I will be paying close attention to in ZIM Integrated Shipping’s Q4’22 earnings report. In the first nine months of FY 2022, the company collected $4.75B in free cash flow, showing an increase of 47.6%. ZIM’s free cash flow can be expected to drop off in Q4’22 due to falling container volumes and weaker shipping rates: I expect the shipping company to report fourth-quarter free cash flow between $1.3B and $1.4B, everything above would be a positive surprise.

Source: ZIM

The third key metric I will be watching is the EBITDA outlook for FY 2023 which may very well be the most important metric in ZIM’s Q4’22 earnings release.

Given the precipitous drop in freight rates in FY 2022 and the accompanying drop in forward rates, ZIM Integrated Shipping is looking at dramatically lower EBITDA possibilities in FY 2023. For FY 2022, the shipping company expected $7.4-7.7B in adjusted EBITDA — which I believe ZIM will achieve — but with freight rates resetting lower and the world bank seeing a sharp deceleration of global economic growth in 2023, I believe ZIM Integrated Shipping could count itself lucky if it achieves $4.0B to $4.5B in EBITDA this year, showing a potential decline of more than 40% year over year.

Growing risk of a global recession, risks to trade flows are on the rise

The world bank lowered its projection for global economic growth from 3.0% to just 1.7% in January, citing historically high inflation. A global economic down-turn is the worst case scenario for globally operating shipping companies like ZIM Integrated Shipping. A global economic down-swing will most likely result in contracting trade volumes which then again could lead to lower contract rates for cargo companies. I expect ZIM Integrated Shipping to address the deteriorating macro outlook for the shipping industry and it will most certainly find a reflection in the company’s EBITDA forecast for FY 2023.

What are analysts saying about ZIM Integrated Shipping, valuation implications

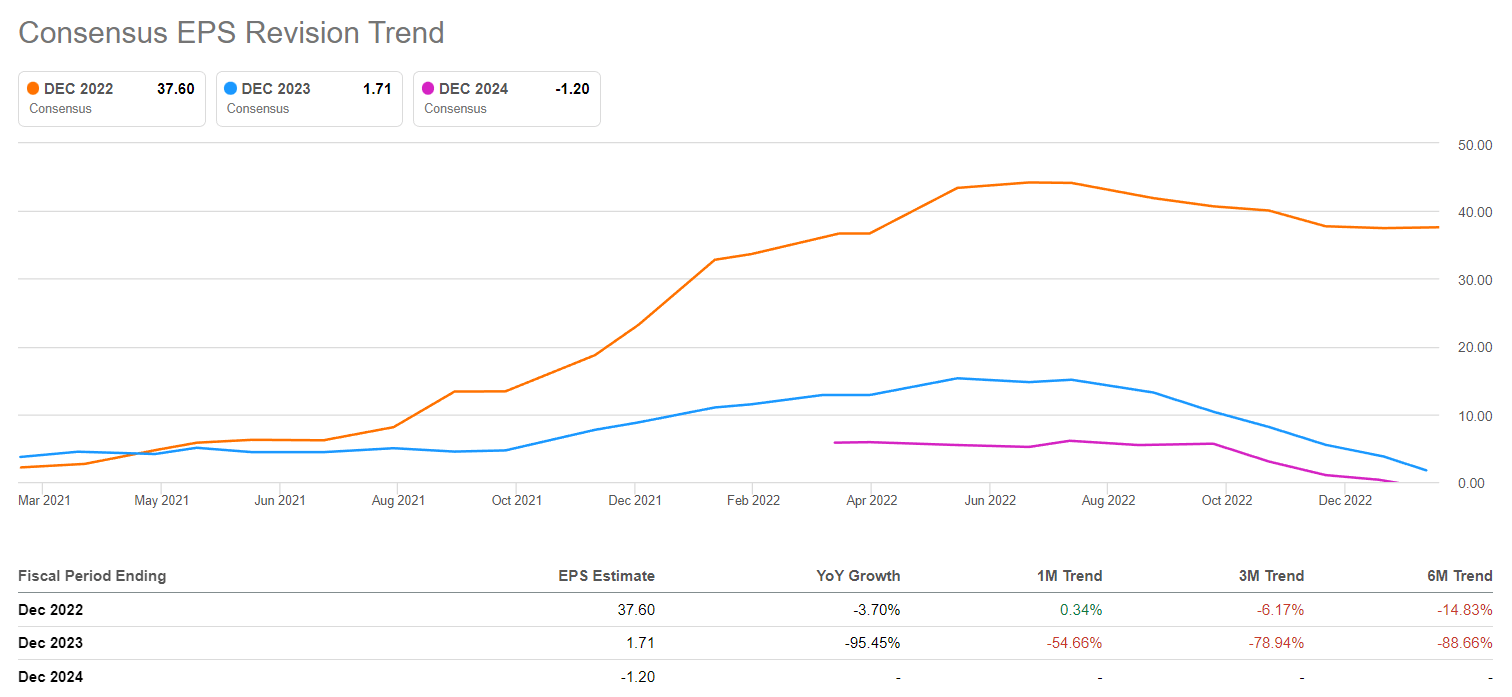

The earnings revision trend is not positive for ZIM Integrated Shipping which isn’t really much of a surprise with freight rates dropping the way they did last year. While freight rates have stabilized as of late, the stabilization happened too late in FY 2022 in order to make a difference for ZIM Integrated Shipping and its earnings estimates.

In the last 90 days, the number of downward revisions for ZIM Integrated Shipping’s FY 2022 EPS exceeded the number of up-ward EPS revisions by a ratio of 6:0, meaning analysts overwhelmingly expect a steep drop in earnings relative to FY 2021. The estimate trend for FY 2023 is also getting worse as analysts now expect ZIM Integrated Shipping to see a massive 95.5% drop-off in earnings, which is largely a reflection of recession expectations being now fully reflected in EPS estimates.

Source: Seeking Alpha

ZIM Integrated Shipping’s 2023 P/E ratio is 10.6 X and turns negative for the year afterwards as analysts expect $(1.20) in EPS in FY 2024. I expect ZIM Integrated Shipping’s P/E ratio to reset higher as the company issues its FY 2023 EBITDA forecast in March and the EPS trend is likely to remain profoundly negative in the near future.

Risks with ZIM Integrated Shipping

The rapid decline in shipping rates has been stopped in December, but a global recession could weigh on transportation volumes, and thereby renew pressure on the pricing environment and on ZIM Integrated Shipping’s contract and average freight rates in FY 2023. ZIM Integrated Shipping’s earnings release for Q4’22 itself could be catalyst for a new round of EPS down-ward revisions.

Final thoughts

ZIM Integrated Shipping is set to report robust EBITDA results for the full-year in the first week of March, but the company is set to see a major deterioration in key metrics, including free cash flow and realized average freight rates. The EBITDA outlook for FY 2023 is likely going to be depressing given the broad deterioration in the shipping industry. Investors must therefore expect continual EPS downward revisions leading up to earnings as well as continual valuation pressure for shares of ZIM Integrated Shipping despite stabilizing shipping rates!

Be the first to comment