alvarez

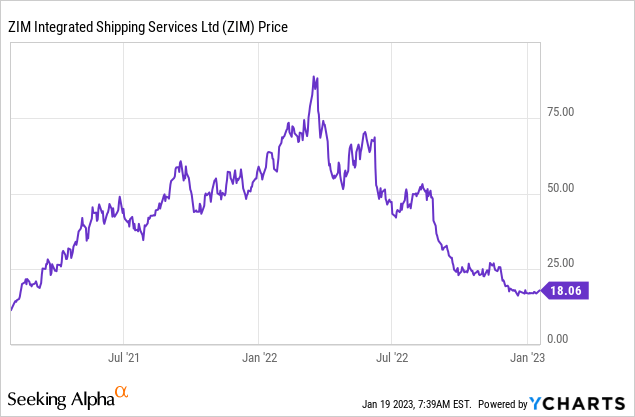

ZIM Integrated Shipping (NYSE:ZIM) is an international shipping company which operates a range of container ships. The company was founded way back in 1945, but has continually improved and reinvented itself over the decades. ZIM perfectly timed its IPO in 2021, and benefited from the huge increase in shipping costs, as a sleeping economy woke up. Investors benefited from a tremendous voyage as its stock increased by nearly 600%, which was outstanding. However, since that point we have seen a rising interest rate environment choke the economy and shipping demand (and prices) slow as a result. Despite this Founders Capital has increased its stake in ZIM by over 525%, which could be an indication of value. In this post, I’m going to break down this recent trade before diving into the technical charts and revisiting its financials. Let’s dive in.

The Trades

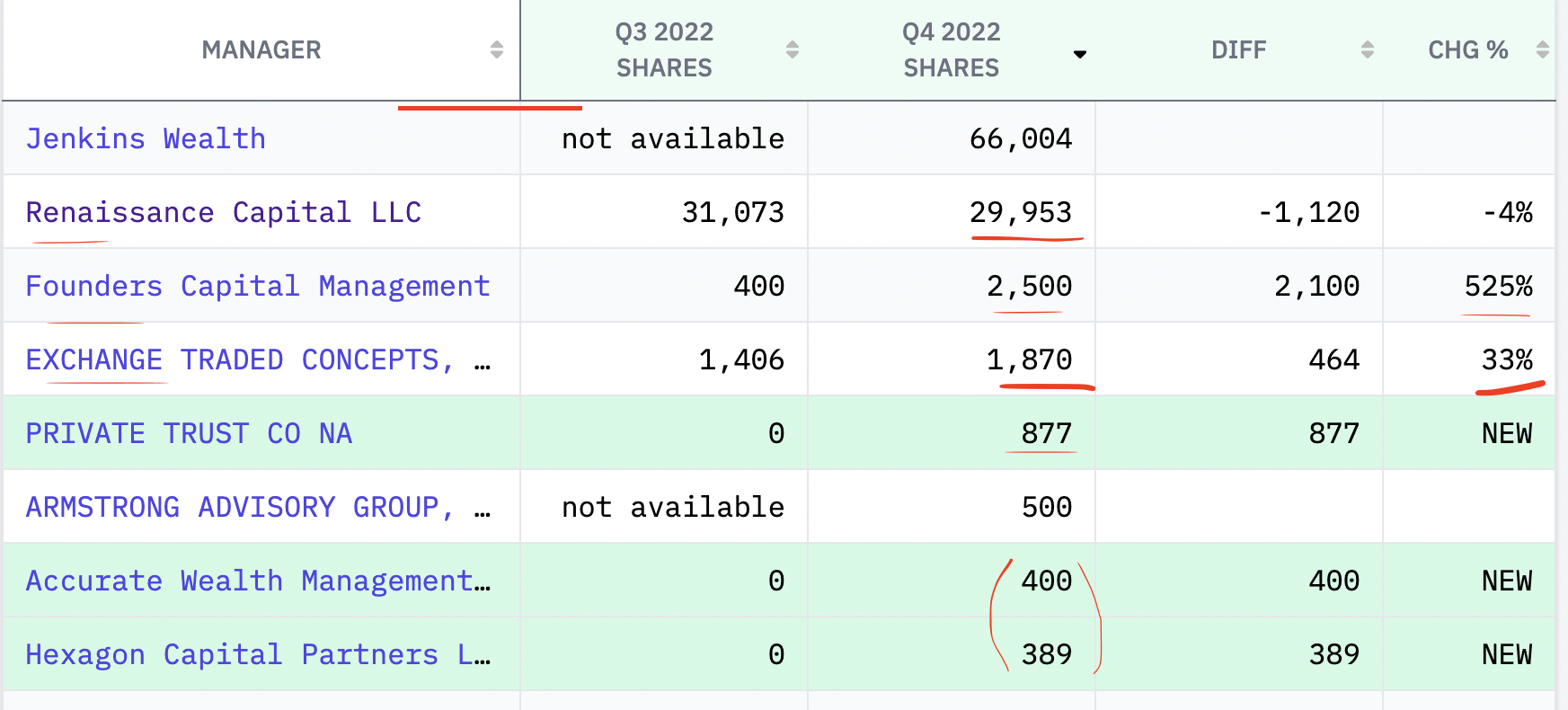

Every investment firm with over $100 million in assets under management must file a 13F filing with the SEC to indicate the holdings they have. From this data we can identify which funds have been buying or selling. In this case a recent 13F filing from the fourth quarter of 2022, shows an investment firm called “Founders Capital”, increased its position in ZIM by a staggering 525%. This represented an increase in the number of shares purchased from just 400 shares to 2,500 shares, with an approximate value of $43 million. Now although this isn’t a huge amount of capital, the proportional increase is substantial.

SEC Filings ZIM (SEC)

Exchange Traded Concepts also increased its stake in ZIM, by 33% from 1,406 shares to 1,870 shares. Its stake was valued at ~$32 million. There were many other funds that purchased ZIM stock in the fourth quarter of 2022. These included; Private Trust CO, which purchased 500 shares, Accurate Wealth Management (400 shares) and Hexagon Capital Partners (389 shares).

A notable fund that owns shares in ZIM is Renaissance Capital, which is owned by the Russian Billionaire Mikhail Prokhorov. Renaissance Capital owns 29,953 shares and despite trimming its position by 4% in Q4,22 its stake is still valued at ~$515 million (over half a billion dollars), which is substantial.

Renaissance Capital (SEC)

Technical Chart

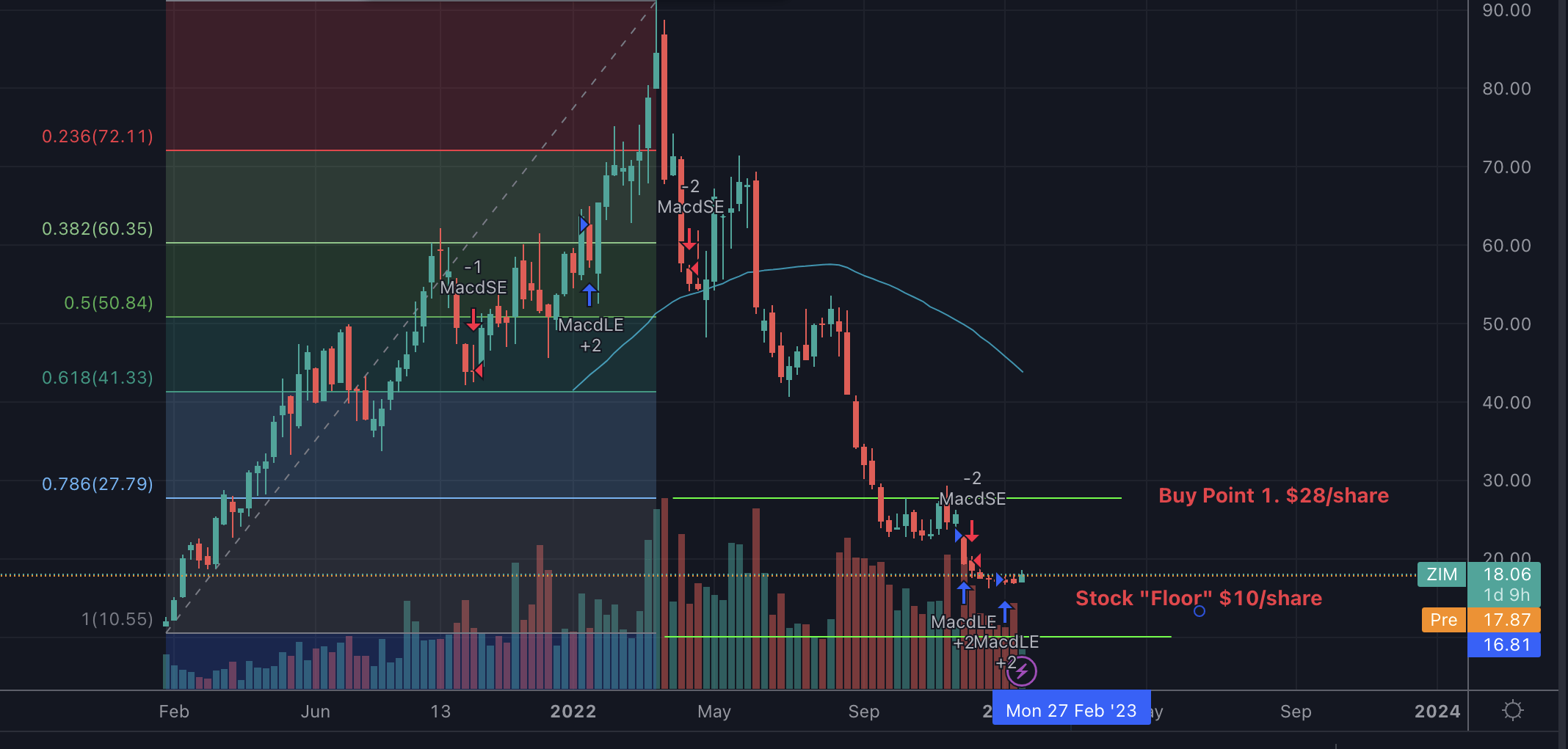

Generally when analysing a stock I tend to purely look at the fundamentals such as revenue and earnings. However, I believe it also makes sense to check the technical charts to look for areas of support/resistance or even a stock “price floor”. As ZIM has only been public since 2021 its stock price action is limited. Nevertheless I have added a “Fibonacci retracement” indicator to the left side which indicates areas of support and resistance. In this case, we can see ZIM’s share price has sliced through almost every support line and has even crossed through my “Buy Point 1” zone at $28/share. Its stock price “floor” is approximately $10/share and is based upon its original IPO. In investing, it’s about analysing the risk/reward ratio and in this case, ZIM’s stock could fall by another 44% from $18 to $10/share. This is under what I deem to be as a “worst” case scenario, which includes freight rates further declining.

ZIM technical chart (Created by author Deep Tech Insights)

The good news for ZIM is it is trading below its 200 day moving average line (in blue). Therefore if a “reversion to the mean” scenario occurs the stock could lift higher. The MACD indicator is also showing some positive upwards signs (little blue arrows), despite heavy selling volume. Overall, due to the conflicting patterns on the chart, I deem it to be a “hold”. In the next section, I will review its financials.

ZIM Business and Financials

In my previous post on ZIM I covered its business model and financials in great detail. Here is a quick recap with a financial update for the most recent quarter. ZIM’s strategy is to effectively act as a “Global Niche” carrier which operates globally.

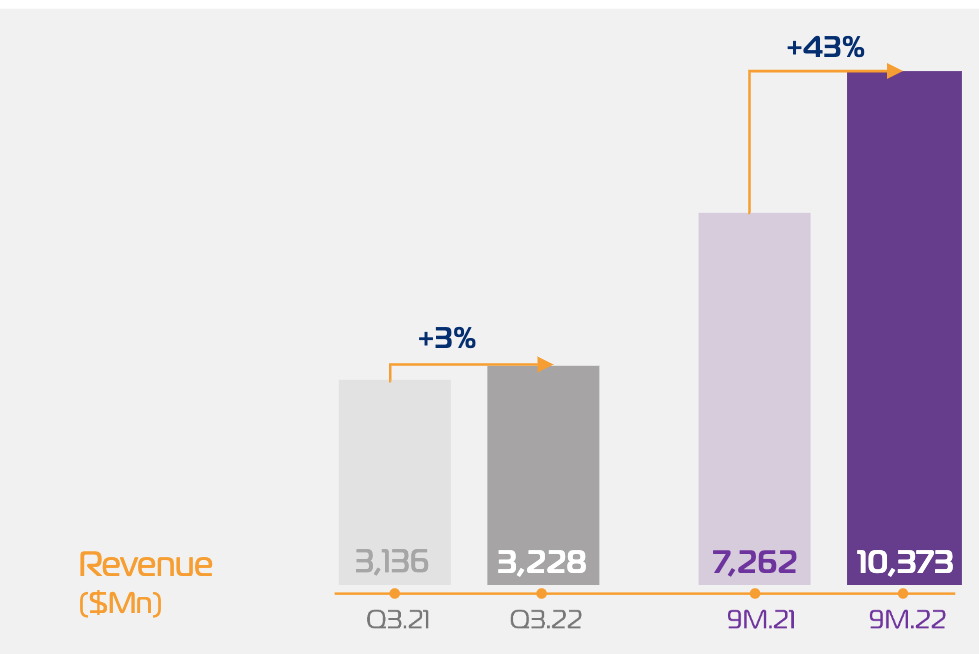

In the third quarter of 2022, the company reported sales of $3.23 billion which only increased by 3% year over year but still beat analyst estimates by $21.86 million. However, if we zoom out ZIM’s revenue is still up a staggering 43% year over year.

ZIM revenue (Q3,22 report)

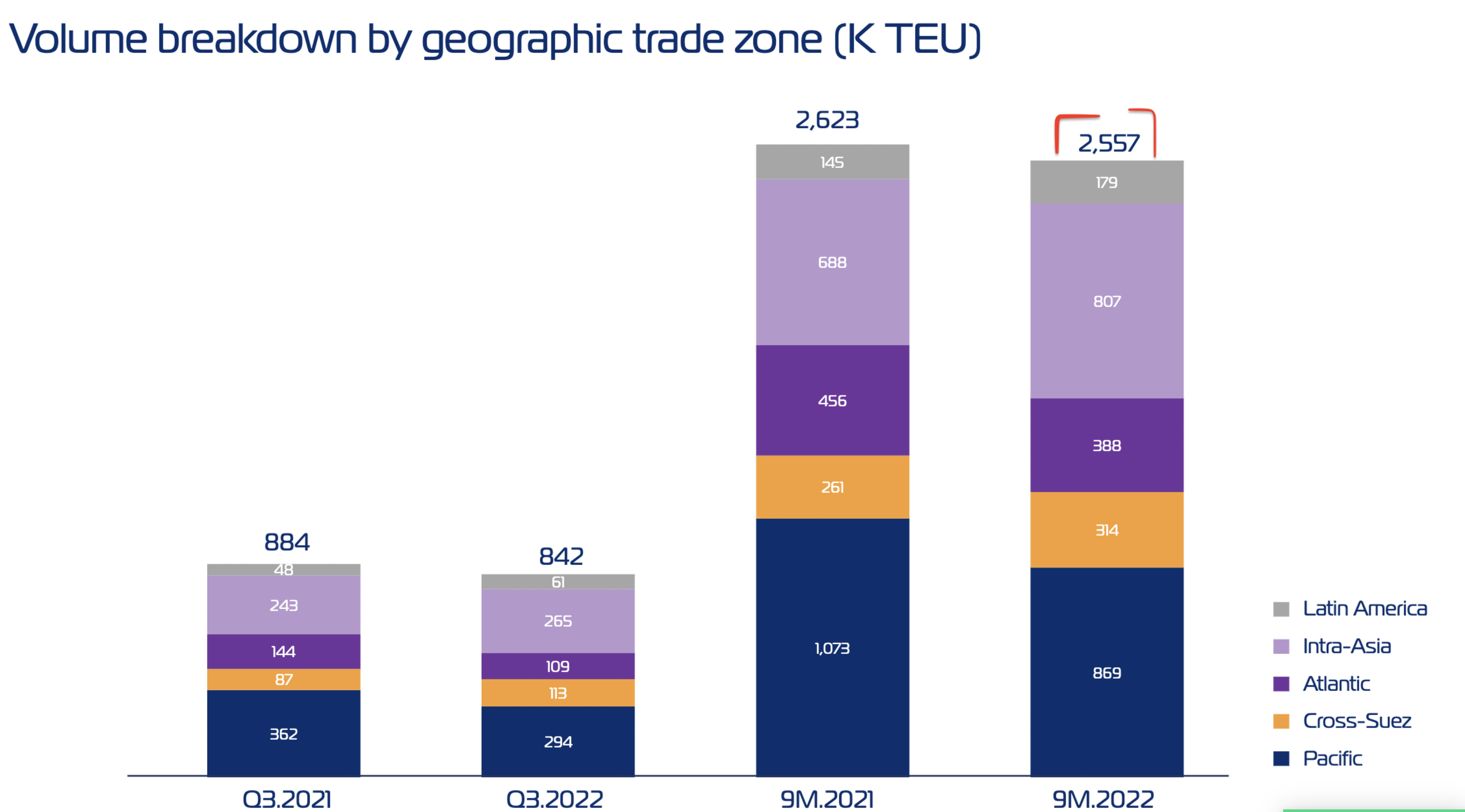

As ZIM makes its revenue from both shipping volume and the cost to ship goods, I will review each in turn. Its revenue growth was impacted by freight volume, which declined by 2.5% from 2623 KTEU in 2021 (trailing 9 months) to just 2,557 KTEU. I expect this volume to fall further in 2023, as we enter a recession environment which will likely cause a slowdown in the number of goods and units being manufactured and thus shipped.

ZIM volume (Q3,22 report)

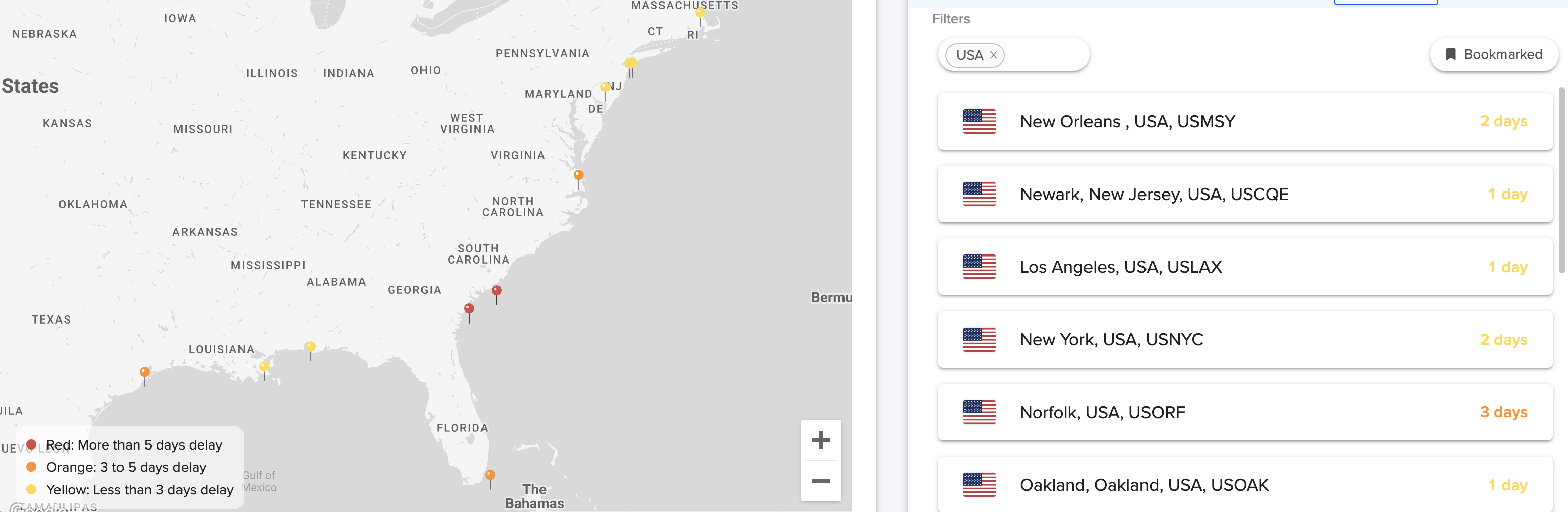

Moving onto earnings ZIM reported $1.166 billion in net income which plummeted by an eye-watering 20% year over year. This was driven mainly by a sharp decline in shipping rates, as economic demand slows and the shipping industry experiences a cyclical downturn. I think it is worth taking a step back to understand how we got here. The cost to ship goods is governed by supply and demand. Thus during the economic reopening of 2021, there was a huge demand for goods, but also a constrained “supply” of ships. A study by McKinsey indicated that there were actually enough ships around the world, but because the ports were clogged up, there was actually a lack of “effective shipping”. Either way, ZIM benefited massively from the sharp increase in shipping costs, which caused them to have a major boost in profits. In order to understand the port congestion issue I have reviewed a variety of “live port” congestion maps over the past year. Back in the third quarter of 2022, Ports such as New Orleans and Houston had substantial delays of 25 days and 39 days respectively. Reviewing todays data (2023), New Orleans has just a 2-day delay on its ports (down from 25 in Q3,22). Whereas Houston has a 3-day delay down from 39 days.

US Port Congestion (GoComet)

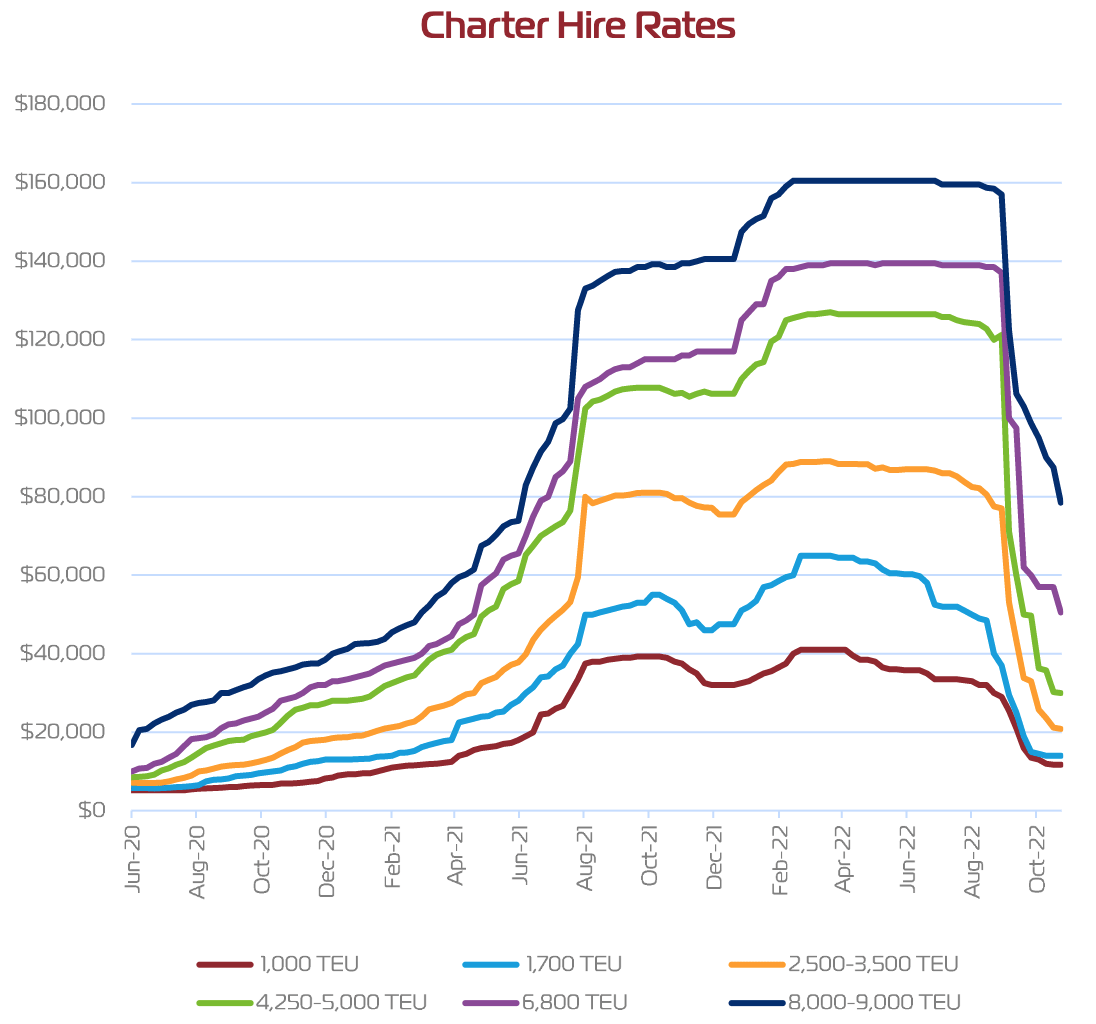

The graphic below perfectly shows the decline in freight costs. For example, a huge 8,000 to 9,000 TEU shipping load would cost ~$160,000. This has plummeted by at least half to $80,000 by Q3,22.

Charter Rates (Clarkson data)

The question now is how low will shipping rates fall and will they bounce back? This is a challenging question, I personally believe rates will fall more if we enter a recession, but I also believe they will bounce back as the shipping industry tends to be cyclical. In addition, I expect rates to be higher than pre pandemic levels long term, due to the complex nature of supply chains and increase in global e-commerce.

ZIM is in a solid position to weather the storm as the company previously secured huge partnerships with the two largest shipping companies in the world (Maersk Line and MSC,). This will enable ZIM to adjust its capacity with greater flexibility, which should give them a competitive advantage against other niche carriers.

The company also has a new batch of 28 LNG powered ships coming online, as part of 48 new ships in production. This such make a huge difference to the company’s margins as LNG is more fuel efficient than traditional fossil fuel based shipping fuels. ZIM even entered into an agreement with UK-founded energy giant Shell to secure its LNG supply for at least the next decade. This was beautiful timing from ZIM’s management, as Europe is now experiencing an “energy crisis” due to the uncertainty around supply from Russia. LNG or Liquified Natural gas is seen as a way to help solve this issue. The chart below shows the price of LNG has shot up substantially.

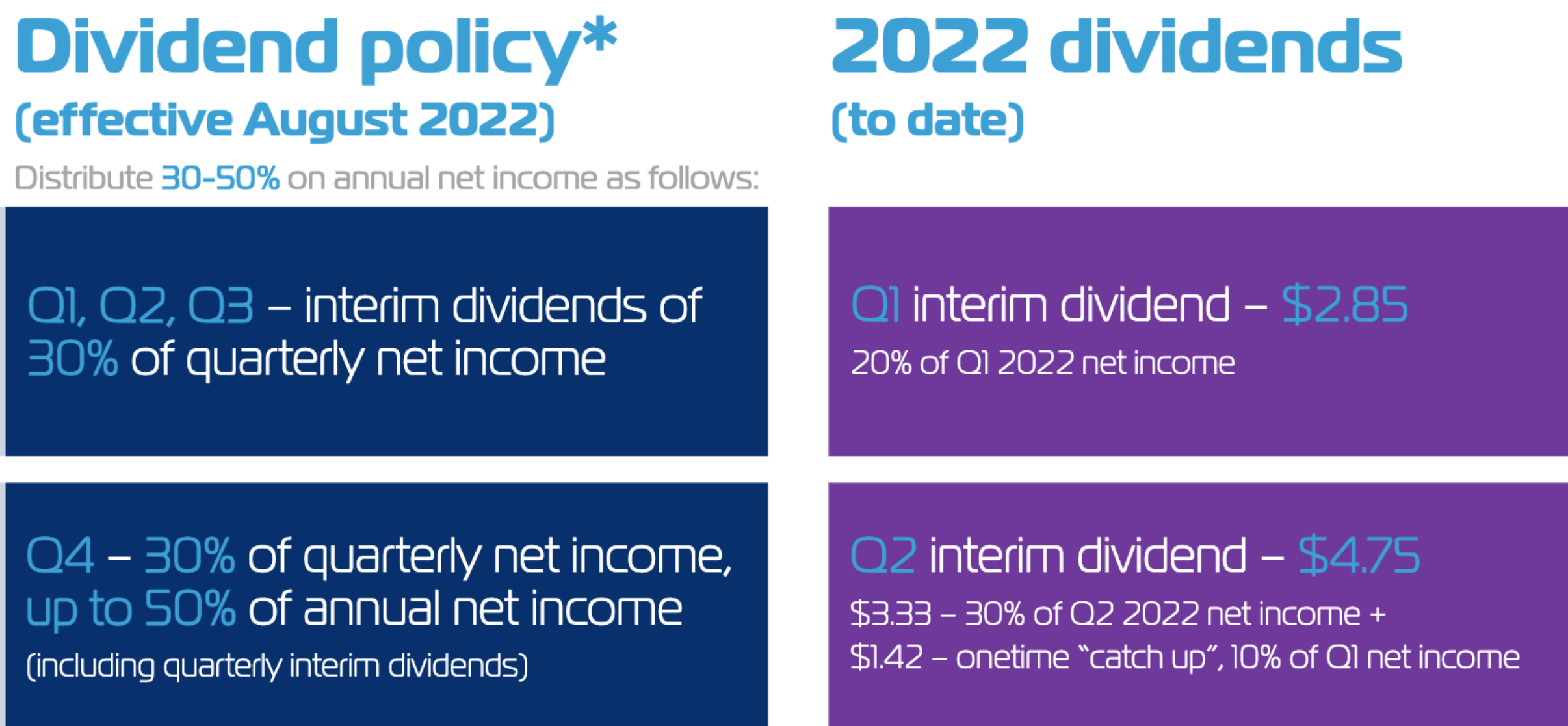

ZIM’s management has also used its excess cash generated to pay down its debt, which has reduced its net leverage ratio from 3.4x to 0x. The business also has a solid balance sheet with $4.44 billion in cash, cash equivalents, and short-term investments. Let us also not forget that ZIM pays a monster dividend of between 30% and 50% of net income. I forecast this to be ~30% in Q4,22, due to the macroeconomic environment.

Dividend (ZIM IR)

Unlike most traditional shipping companies ZIM has an interesting venture capital arm that invests into startups with huge potential. In January 2023, the company reported it had invested into 40Seas, a fintech company which specializes in cross-border trade finance. ZIM invested into a seed round which raised ~$11 million. 40Seas is a small company having only raised $111 million to date, but this potentially offers ZIM some optionality in the stock. For example, Microsoft invested in an early-stage AI company called OpenAI many years back. Today, the business has been valued at ~$20 billion after its AI platform ChatGPT went viral online. Microsoft is now pledging another $10 billion into this investment. Venture Capital investments work based upon a power law, in which the majority will fail but a few will be hugely successful.

Valuation?

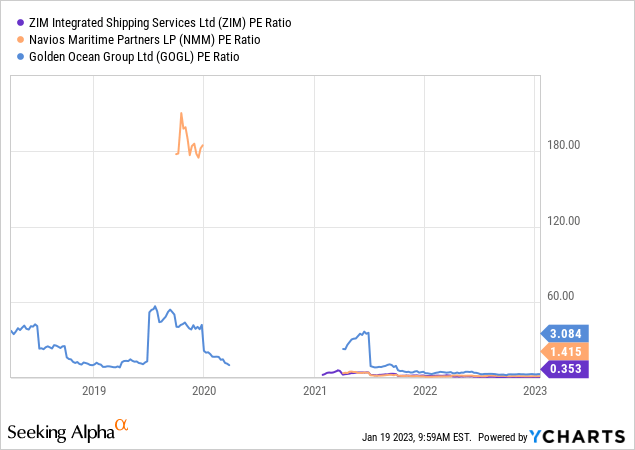

Valuing ZIM is fairly challenging as its future profitability is based upon the uncertain shipping rates moving forward. However, we do know ZIM trades at a Price to Earnings ratio = 0.48. This is substantially cheaper than historic levels. In addition, this is cheaper than industry peers, Golden Ocean Group (GOGL) trades at a P/E Ratio = 3.13 and Navios Maritime Partners L.P. (NMM) which trades at a P/E Ratio = 1.37.

Risks

Recession/declining shipping rates

Many analysts have forecast a recession, which will likely result in lower consumer demand. This will have a knock-on effect of lower shipping volume and likely result in a further decline in shipping costs.

Final Thoughts

ZIM Integrated Shipping is one of the most forward-thinking shipping companies in the world. Its management has conservatively paid down its debt and executed a strategy which focuses on agile and efficient operations. In addition, its huge dividend cannot be understated. The issue for the company is macroeconomic environment will likely cause a further decline in shipping rates. In addition, the technical chart looks woeful as the stock price has broken most major supports. Therefore, I will deem this stock to be a “hold” for the time being.

Be the first to comment