shaunl

Buying, selling or renting a property remains a difficult and expensive process. Zillow (NASDAQ:Z) is trying to remove some of the friction from housing transactions by introducing a “super app”, which they hope will help them to capture a greater share of the number of transactions and realize more revenue per transaction. This makes strategic sense, but there is significant execution risk, and Zillow’s experience in iBuying likely won’t reassure investors. There is also the near-term housing market question. A drop in mortgage rates could cause the market to bounce back, but there is also reason to believe a more prolonged downturn could occur.

Strategy Shift

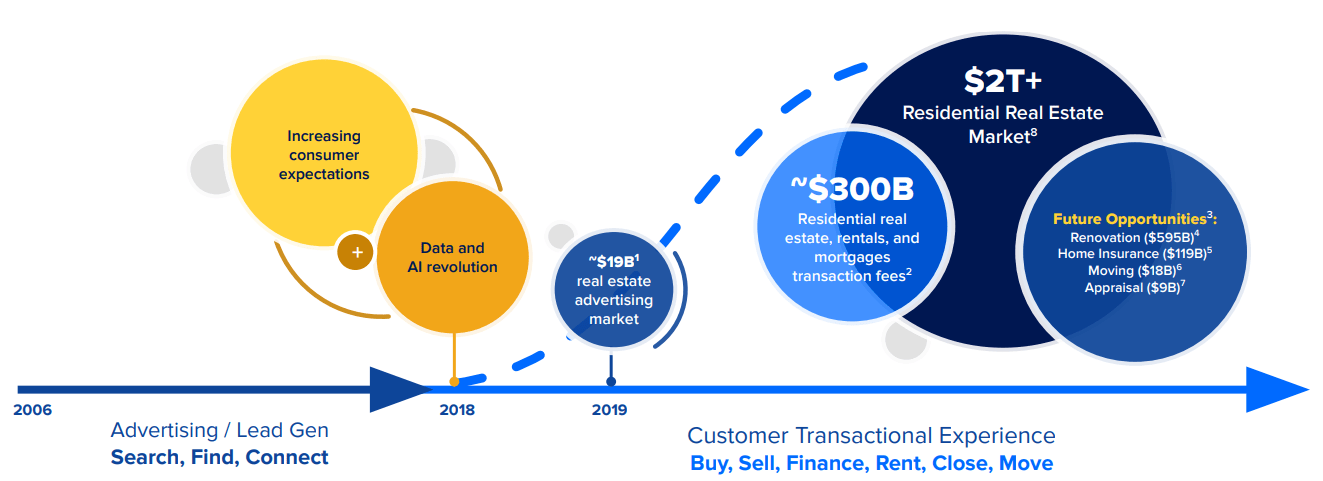

Zillow abandoned the iBuying business in 2021 after realizing the economics were difficult, even in a raging housing bull market. Rather than simply reverting to their previous business model, which while solid, was only able to capture a small share of housing transaction value, Zillow is attempting to build a housing “super app” – an ecosystem of connected solutions across buying, selling, financing and renting. It is hoped that this will lead to an increased market share and greater revenue per transaction.

Figure 1: Housing Super App (source: Zillow)

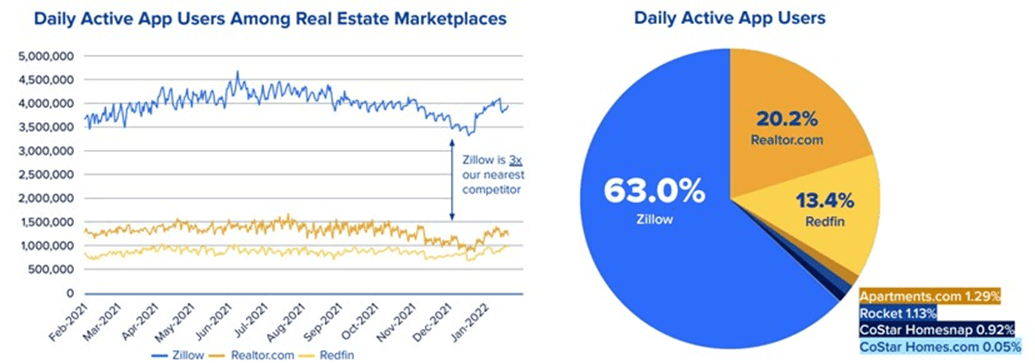

This move is designed to capitalize on the fact that Zillow controls a large share of discovery in the housing market. For example, Zillow has 3x more daily active app users than their nearest competitor.

Figure 2: Daily Active App Users (source: Zillow)

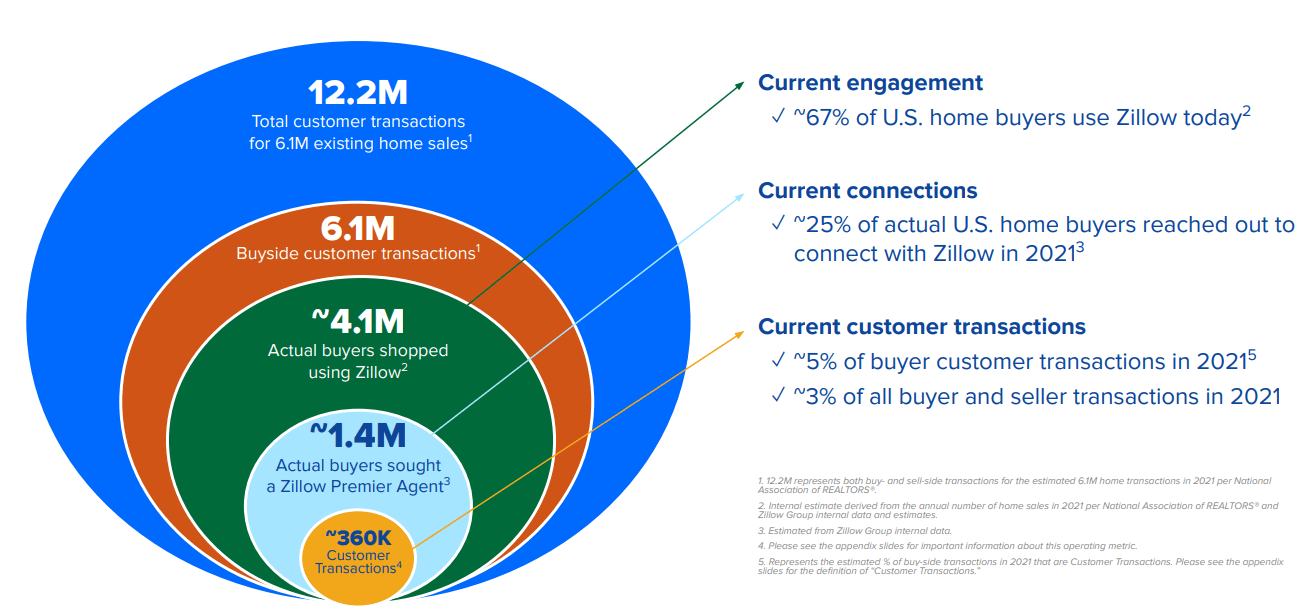

Zillow currently does a fairly poor job of monetizing this control though. It is hoped that the shift in strategy will increase their share of transactions, a reasonable objective given the large number of buyers that engage with Zillow at some point in the purchasing process.

Figure 3: Potential to Expand Transaction Share (source: Zillow)

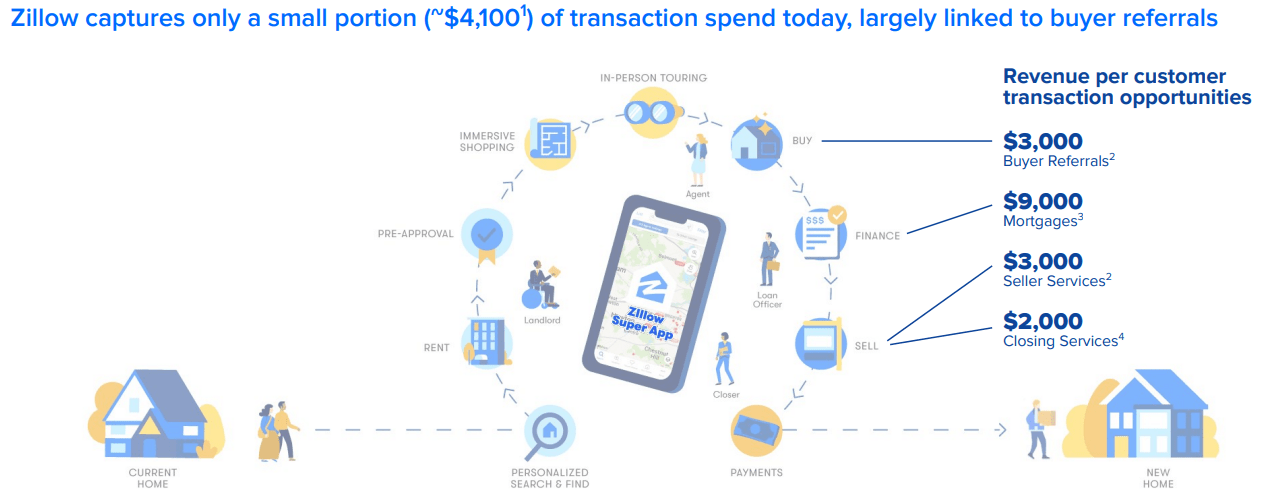

Zillow’s revenue per transaction is also modest, and could be increased significantly by capitalizing on areas like referrals, mortgage origination and seller services.

Figure 4: Potential to Increase Revenue per Transaction (source: Zillow)

As part of their new strategy, Zillow plans on offering the following:

- Touring – make it easier for high-intent movers to connect with homes and Zillow’s partners

- Financing – ensure customers are transaction-ready

- Expanded Seller Solutions

- Enhanced Partner Network

- Integrated Services

Tours are an extremely valuable source of leads, converting at 3x the rate of other leads. Zillow is currently fulfilling less than one third of the tours requested, meaning that most buyers do not get to see a house at the time they requested. By making it easier for buyers and agents to arrange viewings, Zillow can increase the number of tours and take advantage of this high-value source of leads.

Approximately 40% of customers want to start with financing, and Zillow believes this number is likely to increase over time. Zillow has been in the mortgage business for a while, but past efforts have focused on providing financing for iBuyers and using Zillow Home Loans for refinancing. Zillow is now attempting to build a large scale direct-to-consumer purchase mortgage operation.

The purchase mortgage market is large (50 billion USD annual revenue), fragmented (top 25 lenders only have around a one third market share), and customer acquisition costs are high (25% of origination revenue). Zillow believes that this fragmentation exists because of regulations, a lack of nationally-recognized brands, and the need for distribution (network of real estate agents).

Zillow’s control over discovery could help them overcome these issues. Approximately 67% of home buyers currently use Zillow, resulting in Zillow sending millions of prospective customers to third-party lenders over the past 12 months. Roughly 80% of those prospective mortgage customers did not have a real estate agent when they sought financing advice from Zillow.

Zillow still has work to do to capitalize on this opportunity though, primarily building a scalable lending business and redirecting prospective customers away from third-parties to Zillow Home Loans. Zillow is still transitioning from a small call center-focused mortgage business, to a large digital purchase originator serving millions of customers.

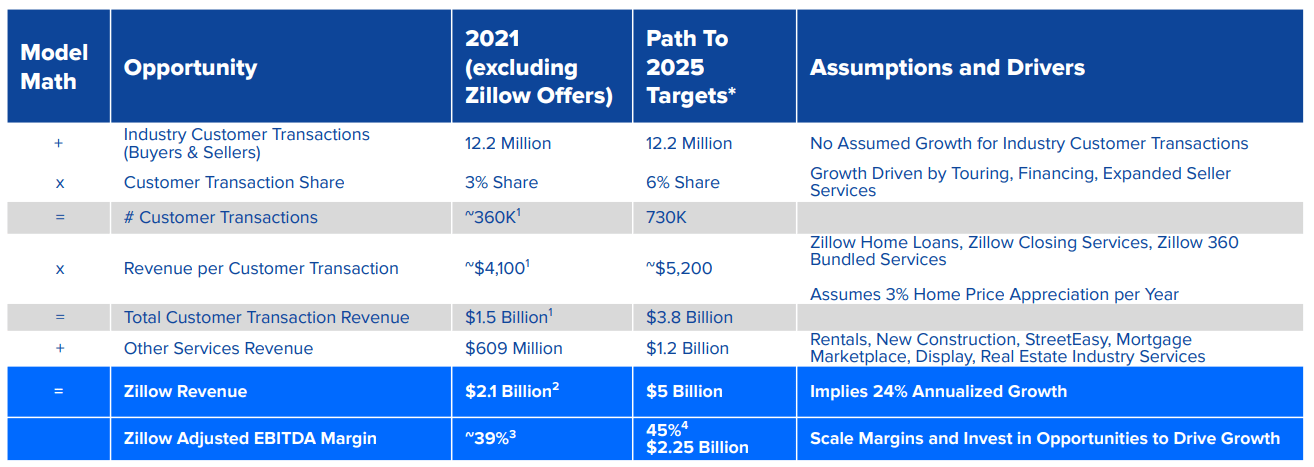

Zillow believes the combined impact of greater market share and more revenue per transaction could lead to 5 billion USD revenue in 2025, assuming there is a healthy housing market at the time.

Figure 5: Zillow 2025 Targets (source: Zillow)

Longer term, there could be further upside if Zillow can successfully expand into areas like insurance and appraisals.

Figure 6: Further Opportunities (source: Zillow)

Product Innovation

In support of their new strategy, Zillow has been rapidly introducing new products and features which aid discovery, improve the viewing experience and assist agents.

Zillow recently introduced a natural-language search tool to help buyers and renters discover properties in a more conversational style.

A feature was added that enables renters to book an apartment tour online based on integrations with Knock CRM and Funnel Leasing, leading platforms used by multifamily properties across the country. 71% of renters report taking up to four in-person tours and 58% of renters say they prefer to schedule in-person tours online.

Zillow acquired ShowingTime over a year ago to help improve the touring process. ShowingTime is a provider of software and phone-based real estate tour reservation services.

Zillow’s real estate software offerings were subsequently reorganized under the ShowingTime+ umbrella. ShowingTime+ is a suite of services (ShowingTime, dotloop, Bridge Interactive, and Rich Media technology) that is available to all agents, brokers and MLSs. This software is designed to help agents and brokers operate their businesses more efficiently, by offering an integrated suite of solutions. On average, agents currently use more than 12 unique software products in the home buying process, creating a disjointed experience.

Listing Media Services was recently launched in select markets as part of ShowingTime+. Listing Media Services is a photography service that provides agents with a comprehensive media package, including high-resolution listing photos, an interactive floor plan with embedded virtual tour and listing photos, downloadable floor plans and aerial photos. In support of this, Zillow acquired VRX Media to create a national photographer network. VRX Media is known for its aerial drone photography, virtual staging, 3D tours, high-definition photography and fast-media delivery to clients.

Housing Market

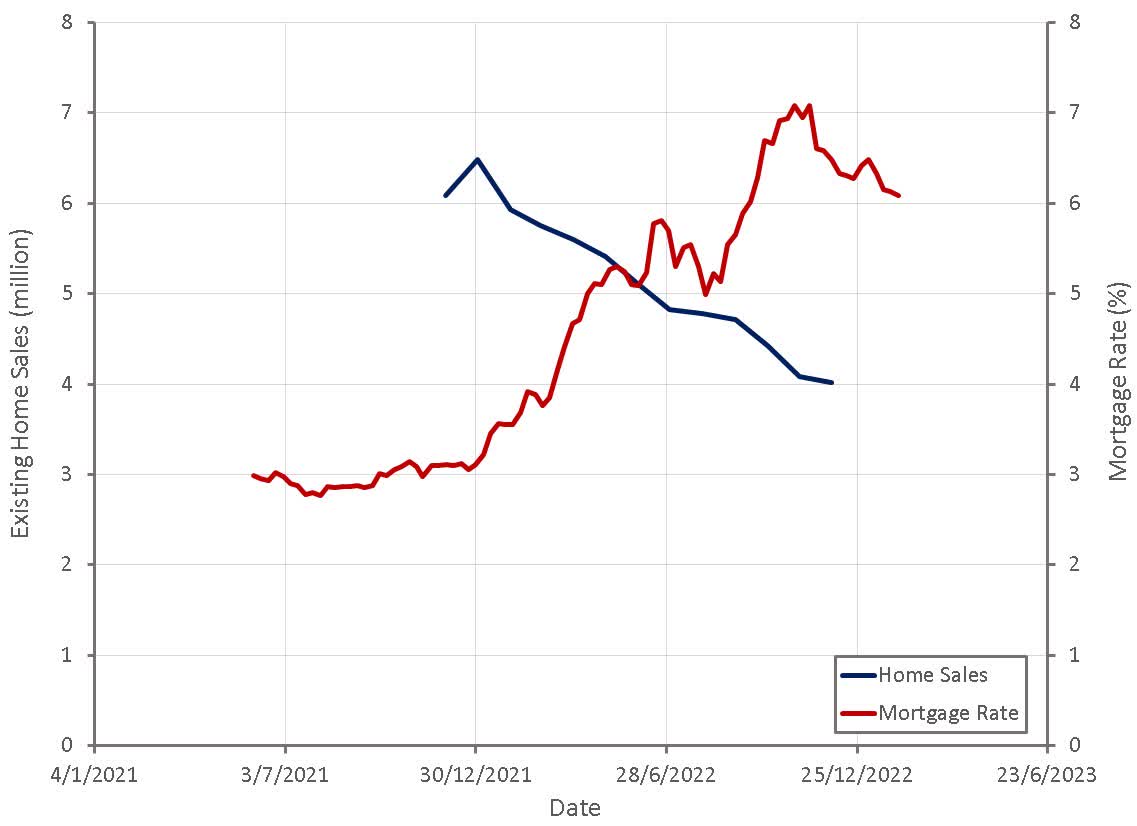

While Zillow’s new business model could create significant value in the long run if the implementation is successful, there is also the current state of the housing market to consider. The rapid rise in home prices over the last few years, coupled with a dramatic increase in interest rates in 2022, has dramatically slowed buying and selling activity.

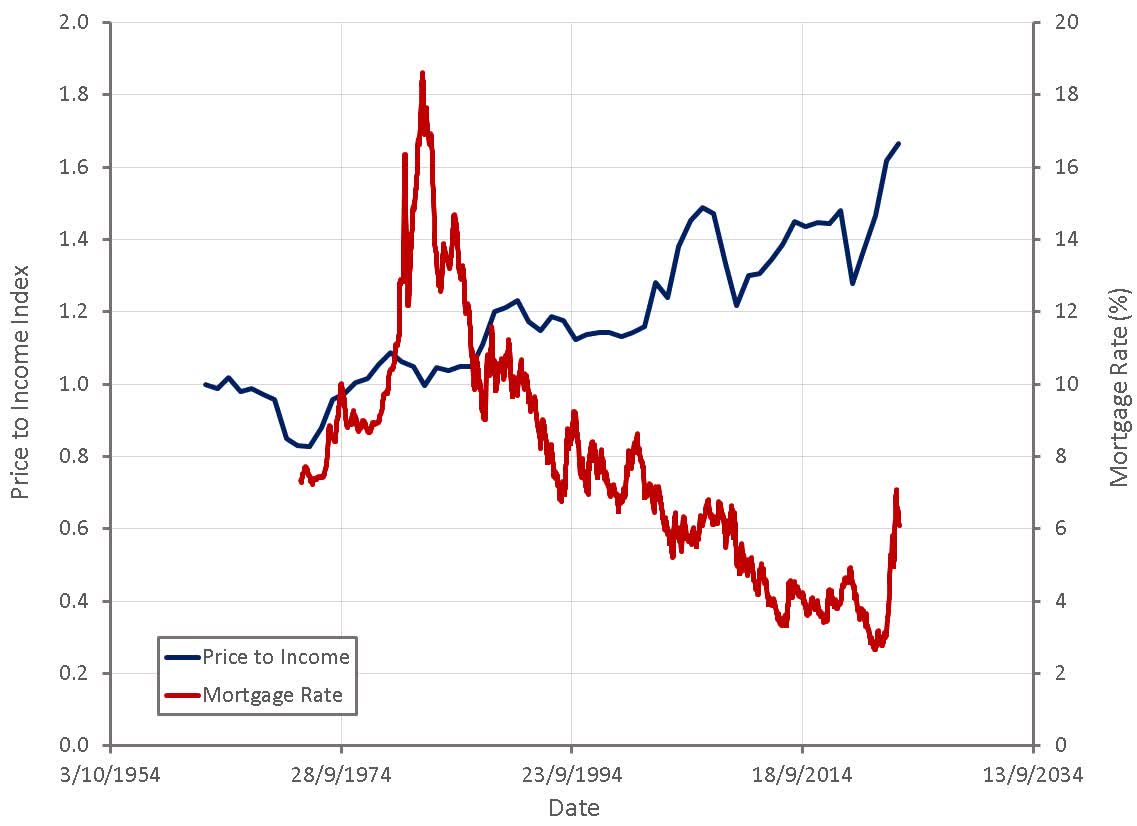

Historically housing inventory turnover has averaged roughly 4-4.5%, suggesting around six million transactions annually. Existing home sales are currently only around four million on an annual basis, and without a drop in interest rates or home prices, this situation is unlikely to change. Homes are not affordable for much of the population with the current combination of rates and prices.

Figure 7: Existing Home Sales and Mortgage Rates (source: Created by author using data from The Federal Reserve) Figure 8: Housing Affordability (source: Created by author using data from The Federal Reserve)

Home prices have eased somewhat, and rapidly declining inflation has helped to reduce mortgage rates as well. This appears to have created optimism that the housing market will soon return to more healthy levels of activity. It should be kept in mind that the Fed is unlikely to lower rates unless there are obvious signs of economic weakness, which likely places a floor under mortgage rates absent a recession.

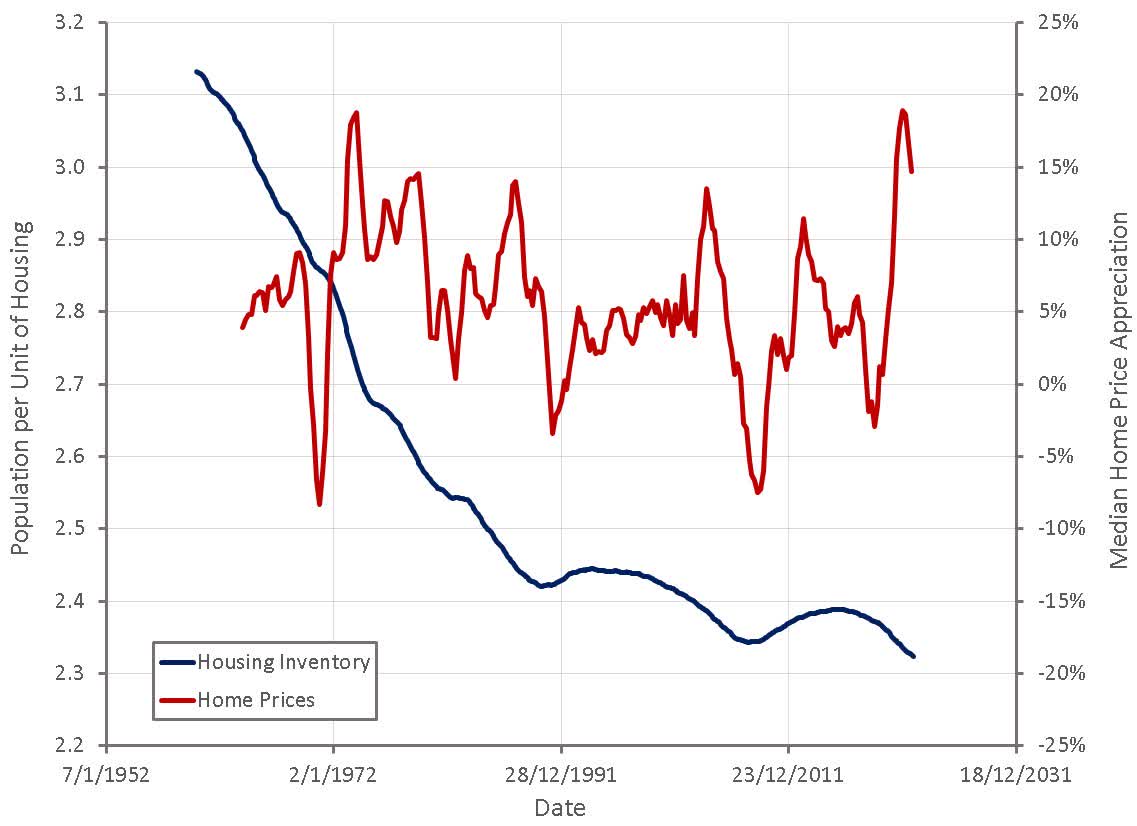

Even if mortgage rates do decline and the housing market normalizes, there is still a potential supply and demand issue. This is often glossed over as the supply of existing houses for sale is low and there are several reports which suggest there is a housing shortage in the millions. The number of homes for sales really says nothing about the supply of housing though, and the reported undersupply says more about home prices than it does about the housing stock.

Comparing the total population to the total estimated number of housing units shows that the housing supply has never been larger, and this level of supply is typically associated with large price declines. This approach is somewhat flawed, as preferences change (household structure, second homes, Airbnb (ABNB), etc.) and it does not consider the geographic supply of housing relative to demand. Despite this, it appears that there is a reasonable chance that the market is oversupplied and that prices will need to fall further before demand returns.

Figure 9: Housing Inventory and Median Home Price Appreciation (source: Created by author using data from The Federal Reserve)

Financial Analysis

Zillow is targeting 5 billion USD revenue in 2025 and a 45% adjusted EBITDA margin. These are achievable targets in a healthy housing market, if the company executes their strategy well, but these targets do imply strong growth, which may be difficult over the next 1-2 years.

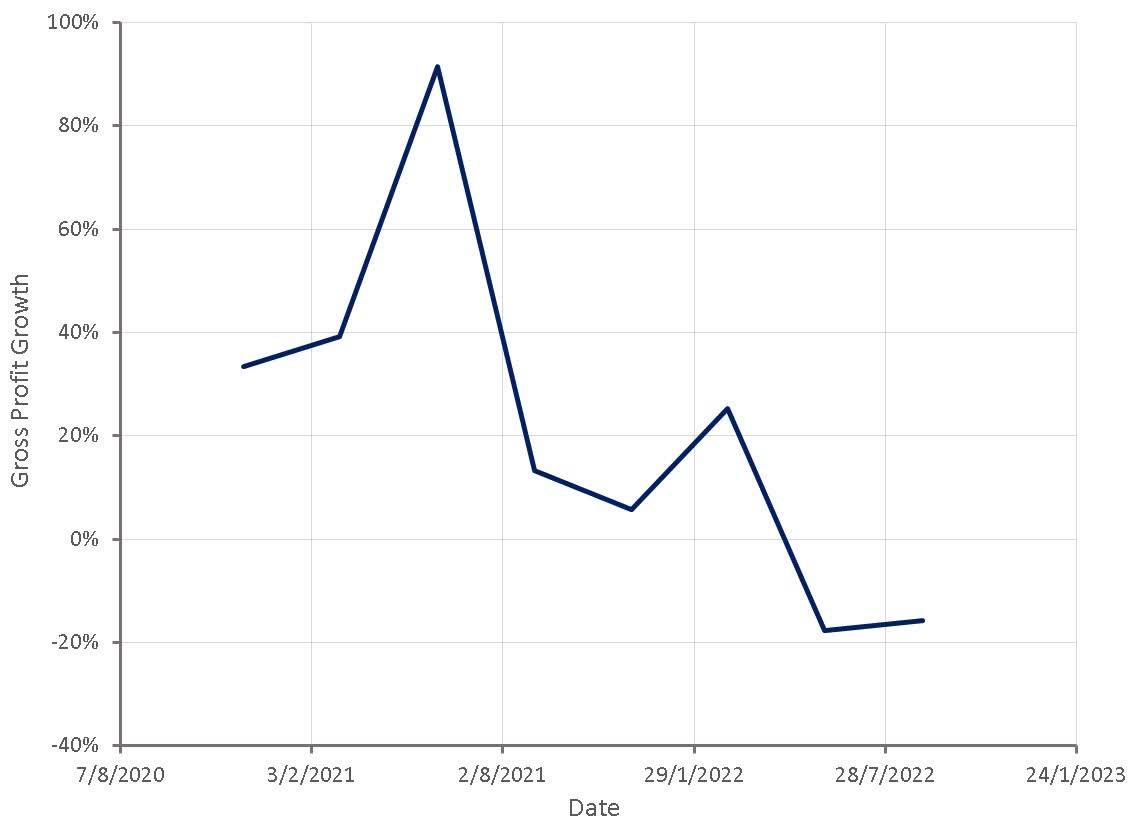

Figure 10: Zillow Gross Profit Growth (source: Created by author using data from Seeking Alpha)

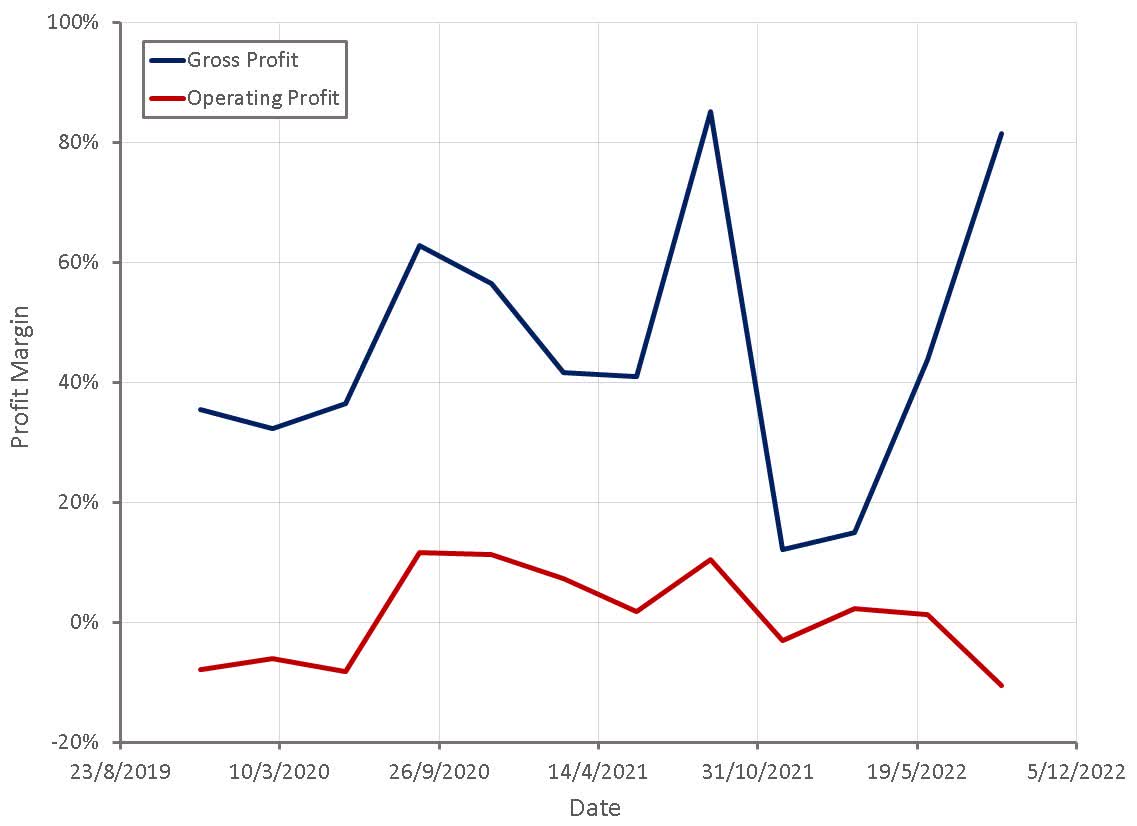

The soft housing market is likely to continue pressuring Zillow’s margins, but this does not matter too much as the company has a strong balance sheet and is currently cash flow positive. Management has also shown a willingness to cut costs when market conditions dictate it.

Figure 11: Zillow Profit Margins (source: Created by author using data from Seeking Alpha)

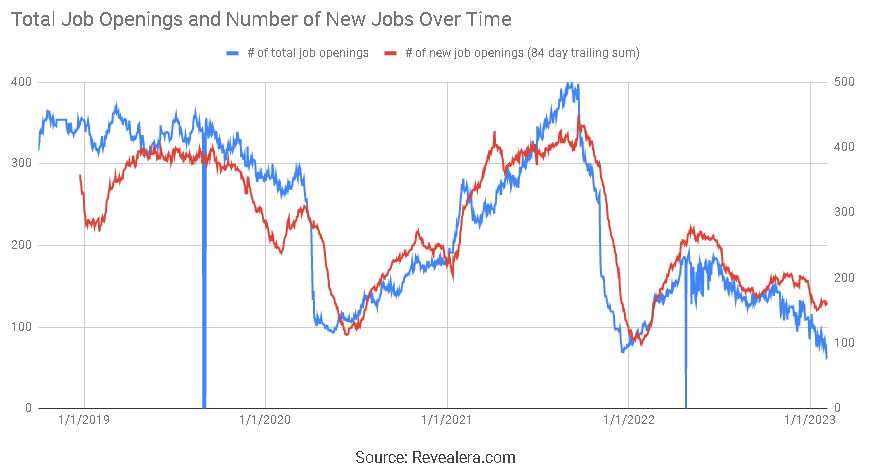

Zillow believes that the housing market will continue to be challenged in 2023, and as a result laid off approximately 25% of employees in 2022 during the wind-down of their iBuying operations. Job openings also continue to decline, which indicates an ongoing focus on cost control.

Figure 12: Zillow Job Openings (source: Revealera.com)

Zillow has authorization to conduct a fairly significant share buyback program and have already repurchased some stock. This could be viewed as a positive and indicates management’s confidence in the business, but it also needs to be viewed in light of stock-based compensation.

Zillow issued an off-cycle RSU grant and repriced some stock options to help with employee retention. This is expected to result in around a 2% additional dilution over the next few years. This highlights one of the hidden costs of SBC and the power of highly skilled employees in a tight job market. SBC is supposed to incentivize outperformance, but instead is often viewed more as part of baseline compensation. Rather than employee bearing the cost of the business performing poorly, along with shareholders, SBC is simply increased so that employees are made whole. This may be necessary to retain human capital, but it is not a shareholder friendly move. Particularly when the share price is depressed and has the potential to move significantly higher over the next few years.

Valuation

I owned Zillow stock for a while during their iBuying phase, because I felt that value-added services around iBuying could create significant value while iBuying was likely to be value neutral. Zillow’s current strategy avoids the execution risk of the iBuying model, and the existential risk of holding inventory during a severe downturn, while potentially allowing Zillow to still capture much of the upside.

I have not tried to develop a valuation model for Zillow, as their shift in strategy and the current real estate market present too many unknowns. It is easy to see that if Zillow can reach their 2025 target, the current share price is objectively cheap as they would only be trading on a PE ratio of something like 10 based on their current share price.

There are a number of risks though, some of which are in Zillow’s control and some of which are not. Zillow has a number of new products that they need to integrate into a cohesive solution. They are also pursuing vertical integration in some parts of the business, which introduces execution risk and potentially makes the business more cyclical.

The biggest unknown is how the housing market will evolve going forward. Markets appear to be pricing a fairly rapid return to normality in the housing market, but I believe there is an underappreciated risk of an extended downturn. If this occurs, Zillow’s returns over the next few years may be fairly poor.

Be the first to comment