Anup Shah/DigitalVision via Getty Images

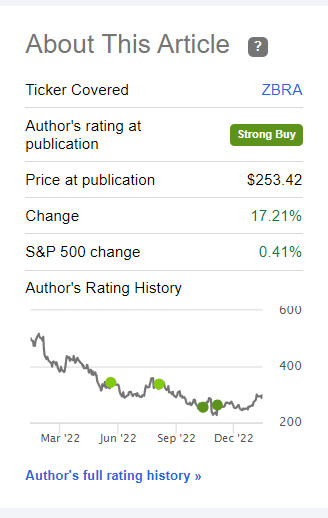

In this follow-up article, I will examine what has happened with Zebra Technologies (NASDAQ:ZBRA) since my last coverage. After the market was disappointed with Q3 earnings, the stock plummeted by around 20%. I was impressed with how the management handled the situation and addressed all issues transparently; you can read the details in my last article. Since then, the stock massively outperformed the S&P 500 and now stands at $297.

Performance since last Coverage (Seeking Alpha)

The new Stallion of the Zebra herd

Plains and mountain zebras live in stable, closed family groups or harems consisting of one stallion, several mares, and their offspring.

Wikipedia

On the 8th December 2022, Zebra Technologies announced that Anders Gustafsson would step down as the CEO on 1st March 2023, after 15 years as Zebra’s CEO. He will stay in the company as the Executive Chairman of the Board of Directors. A change in the CEO position is a rarity for Zebra. In its 54-year history as a company, Anders has just been the second CEO of the company. The leadership transition has been a multi-year effort of the board to play a smooth succession. The new CEO will be Bill Burns, currently Chief Product & Solutions Officer. Bill has 30 years of technology experience and was the CEO of two other companies before joining Zebra seven years ago. For the last five years, he has guided Zebra to its market share leadership and profitability across existing business segments while entering adjacent verticals via accretive M&A.

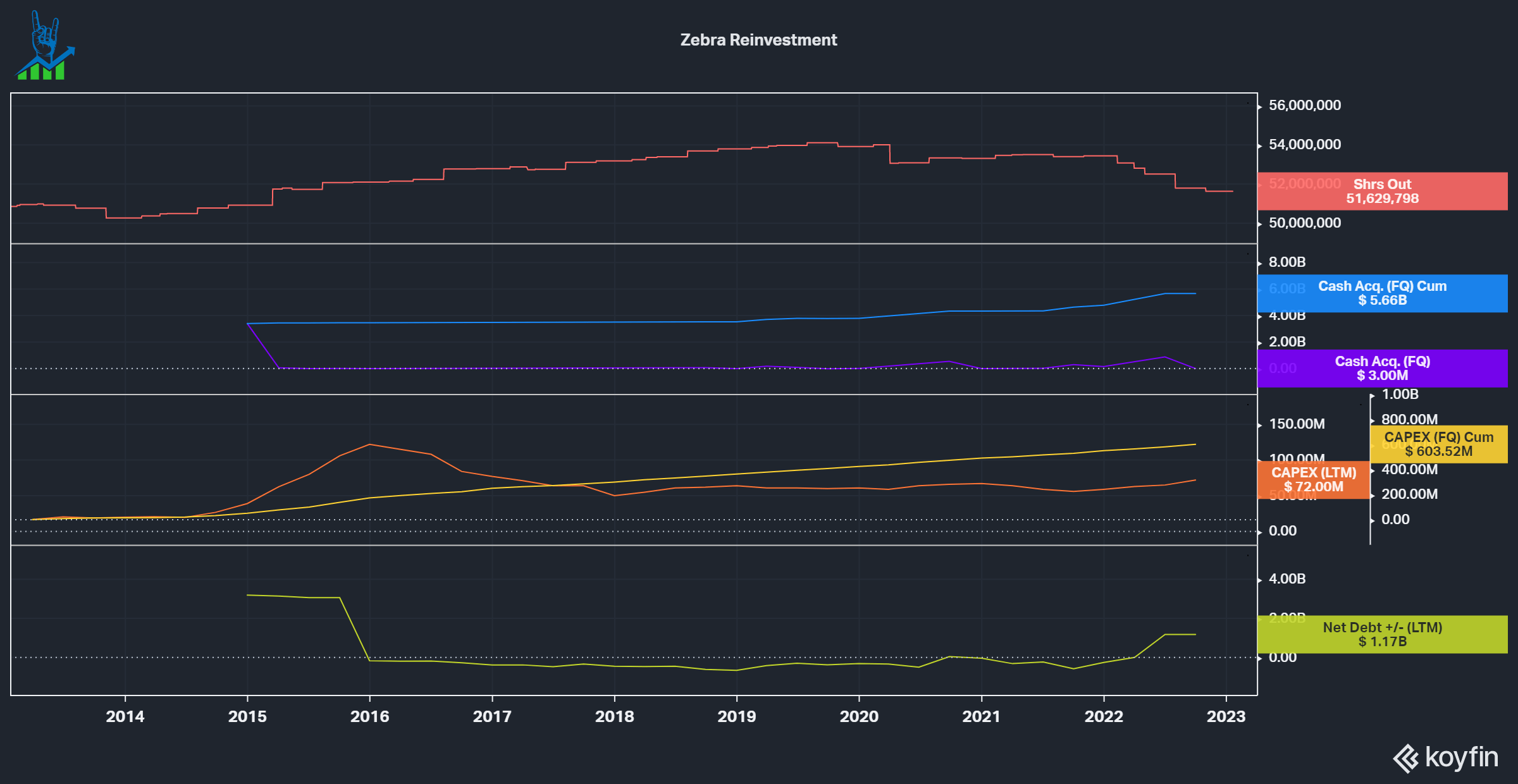

Over the last decade, the company spent over $5.6 billion on acquisitions, with the bulk of it in the transformative Motorola Solutions Enterprise Business acquisition in 2014 at $3.45 billion. This elevated the company to the #1 industry leader in:

- Enterprise Mobile Computing

- Barcode Scanning

- Specialty Printing

- RFID Reading and Printing

Additionally the company also invested an average of $60 million a year into CapEx, with a total of $600 million invested over the last decade. I am confident that Bill Burns will be able to continue leading Zebra on its growth path.

Zebra reinvestment spend (Koyfin)

What to expect from Q4 earnings

Let’s take a look at the upcoming Q4 earnings. Analysts expect $4.6 EPS, up 1.33% YoY and $1.46 billion in revenues, down 0.73%. Over the next two years analysts have a wide array of expectations for both EPS and revenues, with 11-14 analysts covering over that time period. Looking out until 2026 there is only one analyst, so I’ll disregard that.

| Year | EPS Low | EPS High | Revenue Low | Revenue high |

| FY 22 | $17.13 | $17.45 | $5.72 billion | $5.92 b |

| FY 23 | $15.6 | $19.77 | $5.24 billion | $6.12 b |

| FY 24 | $16.99 | $24.75 | $5.52 billion | $6.52 b |

I believe that results will come in more towards the optimistic estimates. Zebra has had a very challenging year with Supply Chain issues, elevated inventory levels due to the supply chain issues in select components, elevated freight costs and the general macro, see my prior article for more details. I am confident that we’ll see many companies looking to rationalize their employee levels and Zebra is in a prime position to offer these services, be it in optimizing employee efficiencies or with robots.

Revisiting buybacks

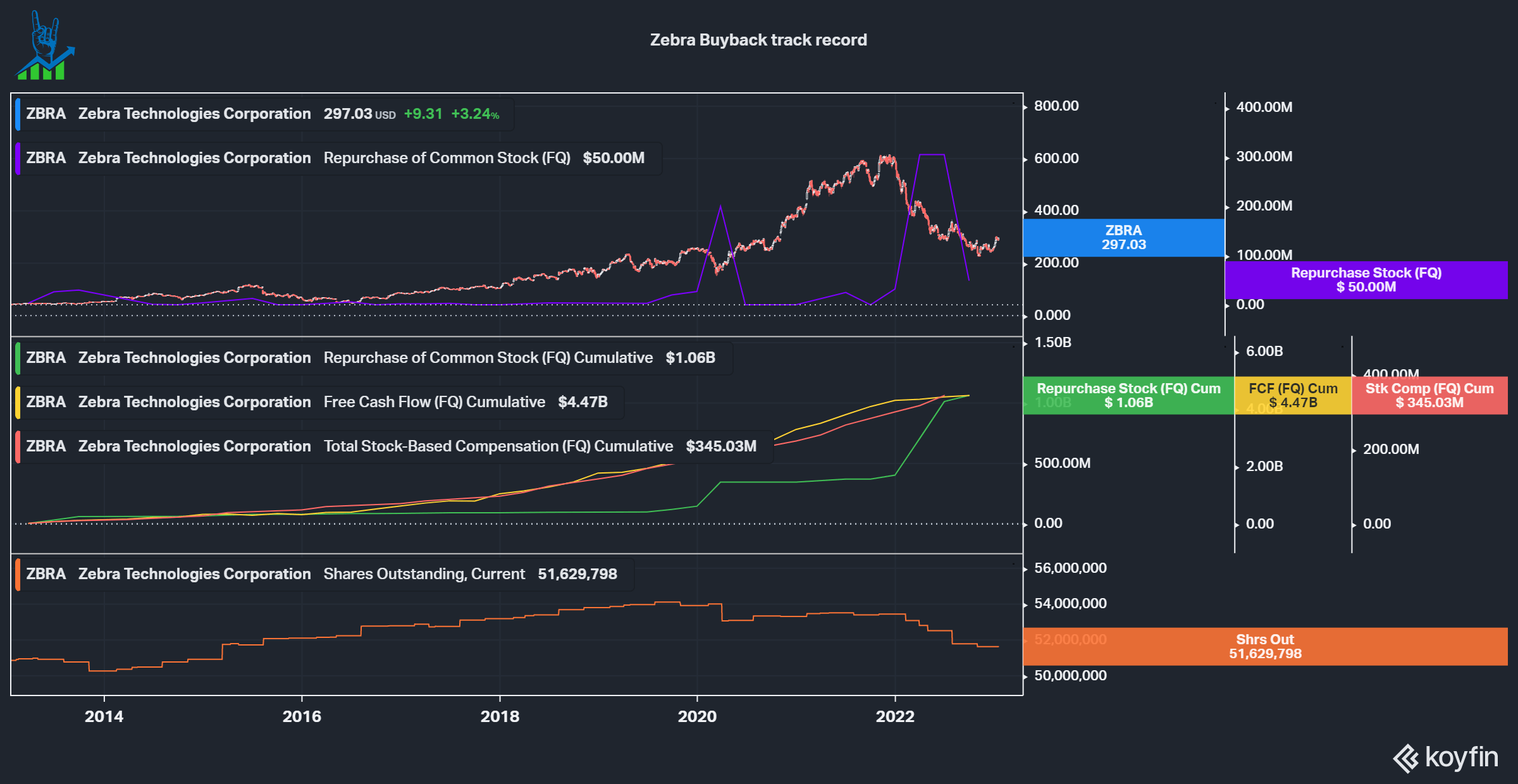

Zebra’s management has been a good capital allocator in the past, so let’s revisit their buyback track record. We can see that shares outstanding have been roughly equal over the last decade due to $345 million of stock-based compensation and acquisitions. The company primarily invests back into the business via M&A and internal investments. If they, however, buy back shares, it has always been accretive in the past. We can see the large spikes in repurchases during the March 2020 crash, followed by two years without repurchases, while the stock price bubbled up to a PE of 50 at the top. After the multiples compressed again, management started to buy back again. Since the start of the March 20 buybacks the company reduced shares outstanding by 4.6%. I believe that management will continue to be disciplined with shareholder capital.

Zebra buyback track record (Koyfin)

Zebra Technologies is still a buy

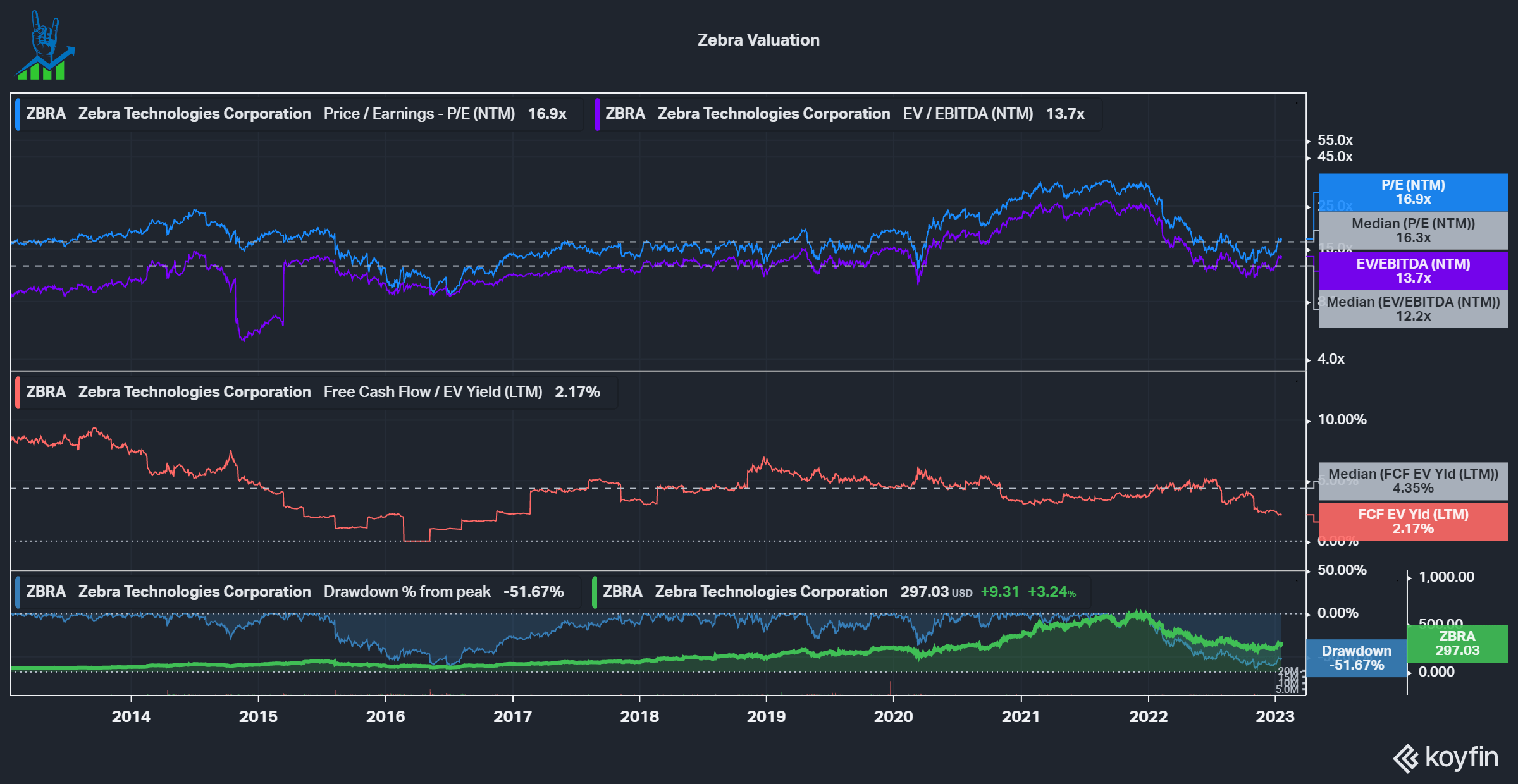

Zebra technologies rallied a good bit from the lows of my last article, but I still believe the company to be a good buy. FCF is currently depressed due to inventory headwinds ($350 million change in inventories over the last 12 months) and litigation settlements ($372 million), but on a PE and EV/EBITDA level, we are still trading in line with our 10-year median. I lowered my rating from a Strong buy to a buy, due to the run up in price. Zebra Technologies remains a core position in my portfolio at a 5.4% weighting at #7 in my concentrated portfolio.

Zebra valuation (Koyfin)

Be the first to comment