Key Talking Points:

- USD/MXN reverses bearish momentum as yields stabilize

- Banxico is likely to continue its hiking cycle in November

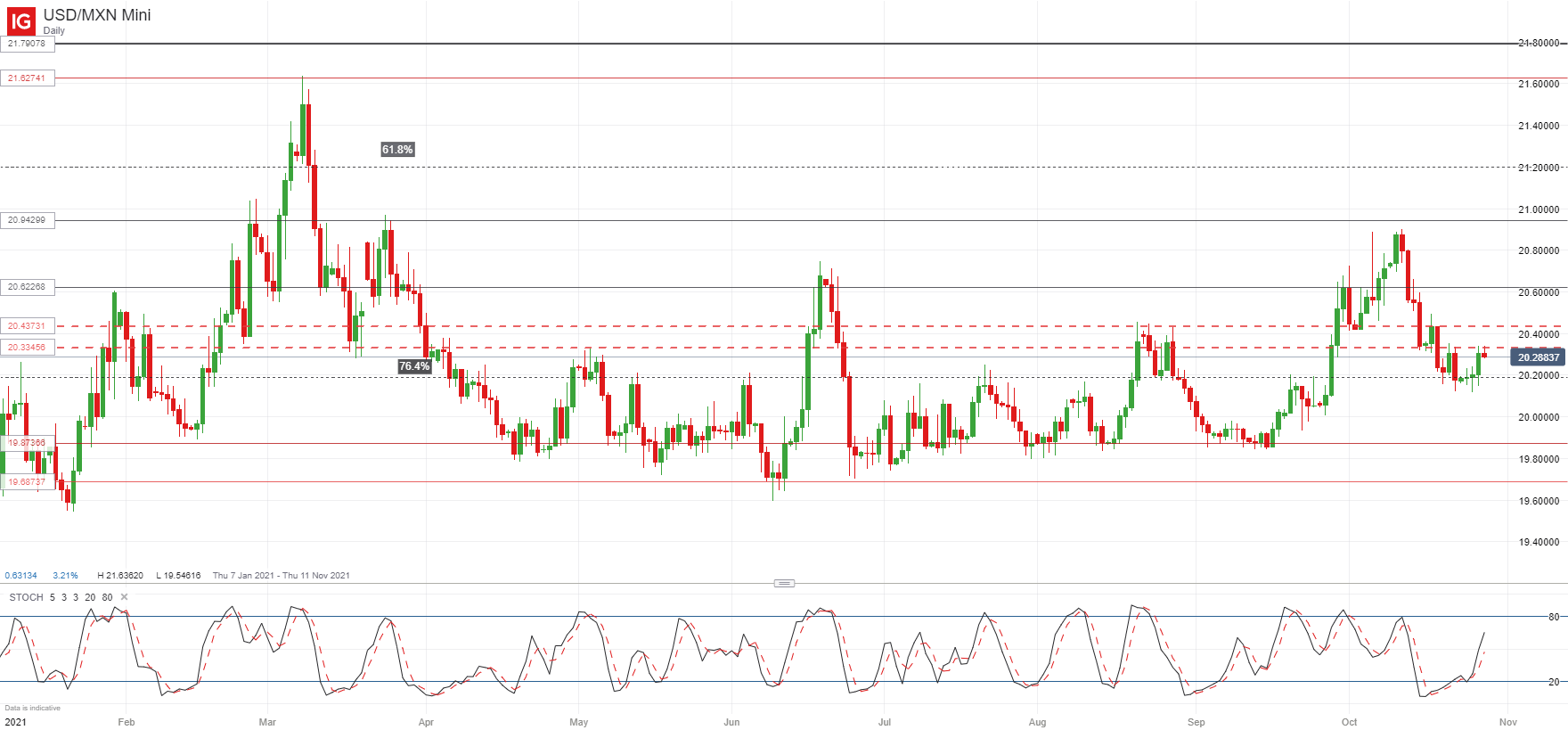

USD/MXN is back at 20.30 pesos per dollar despite attempting to break below the 76.4% Fibonacci (20.18) at the end of last week. The move lower was a consolidation of the bearish momentum that took over two weeks prior, when the USD had exhausted its rally after seeing USD/MXN reach a 7-month high (20.90).

USD/MXN Daily chart

{kind=link}

The pair has been – for the most part – trading in a pretty stable range since April, but a few false breakouts along the way had kept momentum building. There is an area of confluence up ahead (20.33 – 20.43) which has seen some strong resistance in the past so I would expect this time to be no different. But, if this area is cleared, 20.60 or even 20.80 could be back on the table. Alternatively, persistent rejection around this area may see speculators grow confident that additional moves lower can be achieved, bringing a move below 20.12 back into focus.

A lot of this move will be determined by the Dollar side of the trade, with the Fed meeting in focus for next week. Yield curves have started to flatten – brought down further after the hawkish BOC meeting on Wednesday – as investors expect Central Banks to become more hawkish, pushing up short-term rates, and moving out from longer-term bonds, pushing down rates, as there is less need to hedge inflation in the future. This will weigh on the Dollar, which has been shadowing longer-term yields, at the same time that risk-on sentiment reduces the need for safe-haven demand. The reaction in markets from the current central bank meetings is going to be slightly hard to judge, especially given how hawkish market expectations are on rate hikes. The inability to deliver a hawkish enough message will be a detriment to the local currency, but what would a rate hike in November actually mean? The initial reaction would likely be bullish but the risk of a policy mistake given stagnating growth may eventually weigh the currency down.

Can this be applied to the Fed next week? Markets aren’t really pricing in a rate hike by the Fed until the end of the first half of 2022 which means investors are likely to be more focused on the messaging around inflation and its “transitory” nature. They’ll also be expecting the Fed to announce it will start tapering its asset purchases, one of the tools it has available before resorting to rate hikes. But the Fed can’t alter the supply-side dynamics that are causing prices to surge, which means it may need to start hiking rates sooner than expected in order to alter demand-side pressures.

On the Peso side, Banxico will be holding its November interest rate decision meeting in two weeks. Market expectations have been growing for the bank to raise the key rate by 50 basis points to 5.25%, which would be an acceleration from consecutive 25 bps hikes it has been delivering since June. If so, this would likely lift the Peso a little bit and would make the Mexican currency more attractive for those investors seeking carry trade advantages. Even if the rate hike is limited to 25 bps – given how inflation in Mexico has been less aggressive than in other emerging markets – it would still fall in line with the general market consensus, offering the Peso a little bid along the way, especially now that currencies are really driven by interest rate differentials.

Fibonacci Confluence on FX Pairs

— Written by Daniela Sabin Hathorn, Market Analyst

Follow Daniela on Twitter @HathornSabin

Be the first to comment