bgton

Summary:

As we pivot away from the pandemic world of computers, gaming and indoor activities YETI intrigues me for its brand popularity and embodiment of the great outdoors, the complete antithesis of how we have spent the last three years. Perhaps it’s a company that will offer continuing growth while Tech undergoes a valuation recalibration.

YETI Holdings, Inc. is a lifestyle brand that designs, produces, and markets products for the outdoor and recreation market. The company offers a variety of products including coolers, drinkware, bags, and other outdoor gear. Its products are sold through specialty retailers, mass merchants, and e-commerce sites.

Like many growth stocks in 2022, YETI surrendered its pandemic gains and now trades back around $40 again. Many growth trends of the last 3 years were attributable to the digitalization of our lives through E-commerce, the Metaverse, Fintech technologies to name a few. However, in contrast, YETI is a brand that champions outdoor activities something that won’t be affected by pandemic tech trend normalization. Tech stocks look likely to remain subdued into 2023 with higher interest rates. Can the YETI growth story continue to provide above market returns?

YETI 5 Year Stock Performance (Google Search)

Where does YETI’s competitive advantage lie?

Quality design:

YETI’s products pride themselves on having high-performance and durability, catering to a range of outdoor enthusiasts.

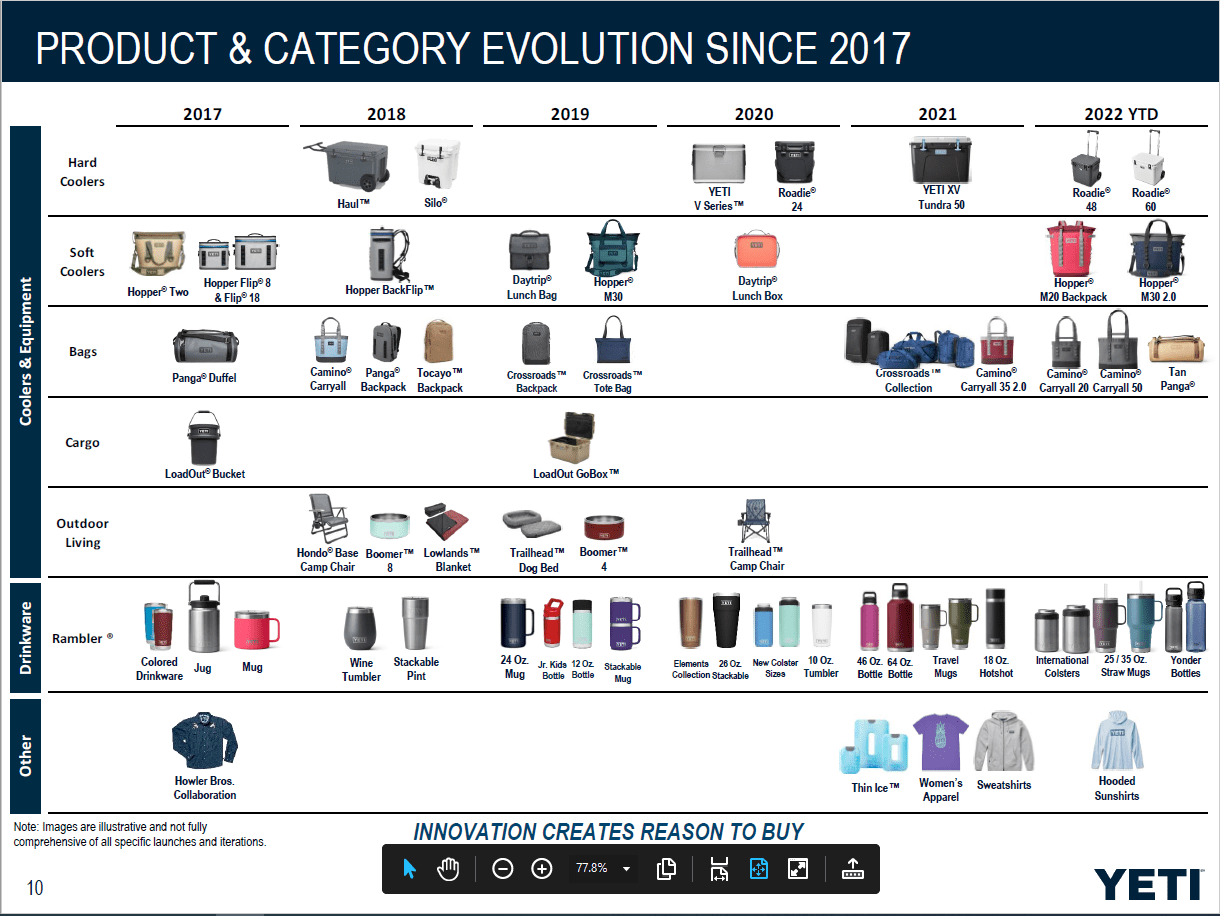

YETI Products (Q3 2022 Earnings YETI)

I have read many reviews online comparing YETI products to the competition in both of their two major markets, coolers, and drinkware. While its true YETI products usually rank in the top of the quality product metric tests, they don’t finish comprehensively above the competition and given they usually have the highest prices among competitors, this makes me question whether quality product is a sustainable competitive advantage. For example, there are coolers/drinks bottles on the market that perform just as well as YETI’s for a much lower price.

Please see here some of the latest detailed reviews I have seen on coolers and drinkware division:

Coolers:

Best Coolers for 2023: Cabela, Magellan Outdoors, YETI, RTIC and More

Drinkware:

Brand Development:

YETI has been very successful at marketing their brand. Their two main messages have been highlighting the quality of their product for outdoor use but also selling the experience of outdoor living.

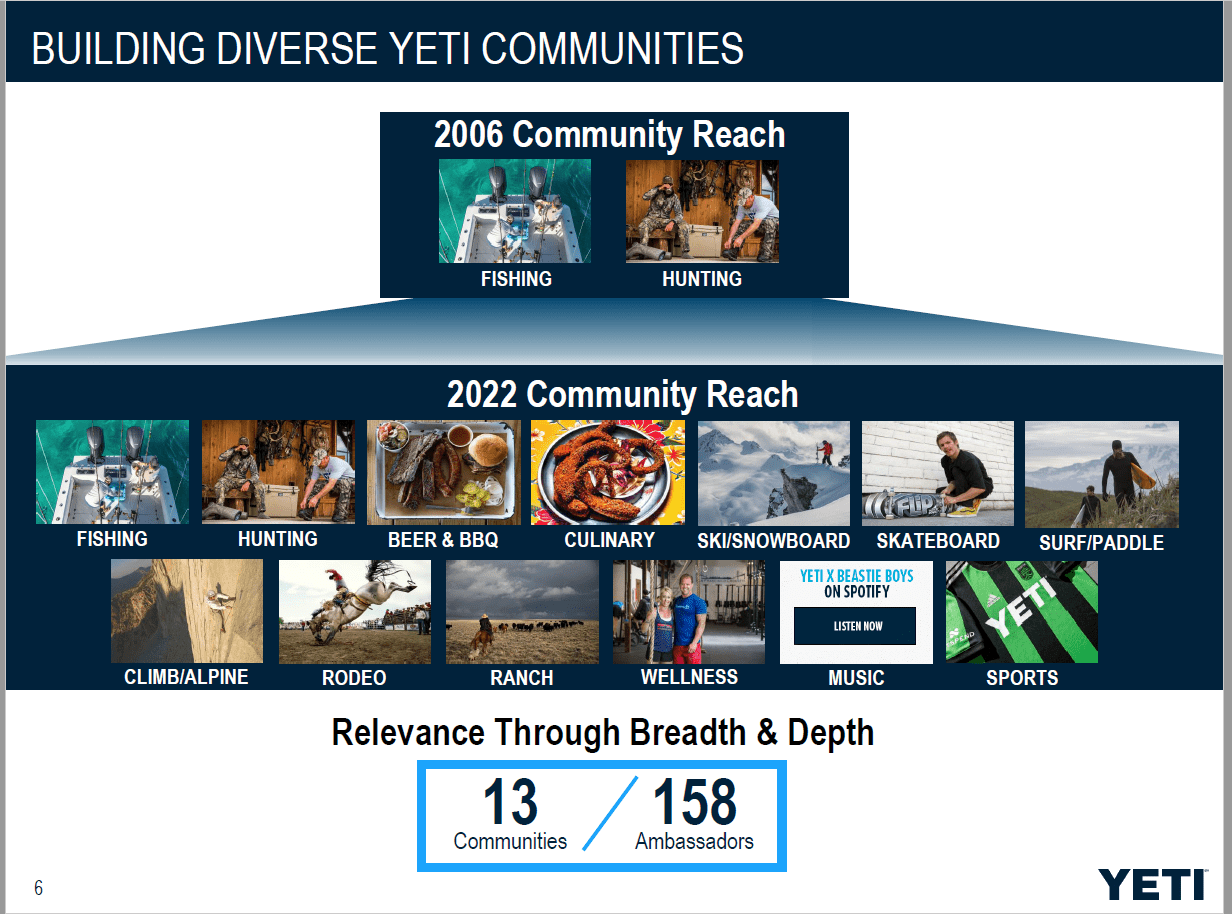

YETI Communities (Q3 2022 Earnings YETI)

Growing social media channels, partnering with high profile ambassadors, sponsorship of outdoor events and content creation are some of the tools they have used to convey their message.

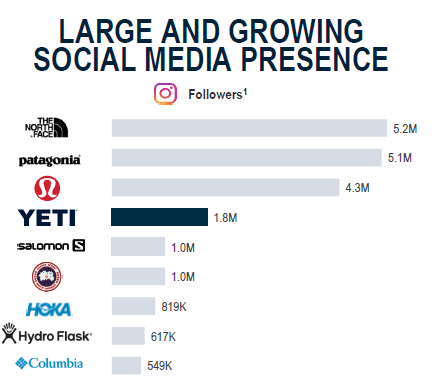

YETI Social Media (Q3 2022 Earnings YETI)

Similarly, their Tiktok Followers:

Lululemon: 505k

YETI:369k

The North Face:315k

Salomon: 198k

Columbia: 109k

Canada Goose: 68k

HydroFlask: 56k

Hoka: 16k

While I commend the marketing department on making coolers and drinks bottles popular products among affluent consumers, I wonder is it enough to carry the niche brand. As I will discuss below, addressable market, price point and narrow product offering are some of my concerns.

Marketplace and competition:

There are three competitive landscapes to analyze.

Firstly, the cooler and equipment market where YETI derives 40% of its annual revenue. The global retail cooler market size was valued at USD 1.50 billion in 2021 and is expected to expand at a compound annual growth rate CAGR of 8.6% from 2022 to 2030. YETI has about a 37% share of the cooler market. Otter Box, RTIC, Engel, Pelican, ORCA, Igloo, Coleman, Cabela’s, K2, Grizzly, and Icey-Tek are some of the other competitors in the cooler market. This feels saturated when you consider revenue forecasts market size of only 3.2bn in 2030. (8.6% compounded from 2021). Also, YETI’s market size is probably more niche than above considering they target the premium end of the market.

Similar statistics are noticeable in the drinkware market with high competition, a CAGR rate of 4.3% to 2030. The global reusable water bottle market size was valued at USD 8.64 billion in 2021 so a little more growth opportunities here.

GICS (Global Industry Classification Standard) classifies YETI in the consumer cyclical and leisure category. While no direct competitors, we may gain insight from how analysts are looking at the subsector as a whole to determine if cheap valuation exists.

YETI ultimately is an outdoor lifestyle brand and it is more likely to follow the future trajectory of the following companies although they have more of a presence in apparel. These being North Face, Columbia, Patagonia, Salomon, Arcteryx. These companies have premium branding and already a strong marketing message. If YETI is growing in this direction which product ranges or markets is it likely to compete in next? It feels like YETI is currently operating in a narrow range of niche enthusiasts and growing will require stealing market share from larger more established outdoor lifestyle brands.

Financials:

- Revenue growth % in the high teens, early 20s since going public in 2018. Solid growth from a consumer cyclical name.

- Gross margins are stable around 50% – not competing on price.

- Net Margins slightly into double digits – large margin highlights premium branding strategy

- Free cash flow positive

- Net Debt as % of total capital declining from 50% in 2018 to 13% in 2021.

A healthy income statement and balance sheet generally speaking.

Valuation:

YETI is notably the largest cooler brand in the USA with revenues over $1 billion. Igloo $500m, Pelican $460m RTIC $200m, OtterBox $100m are some of the competitors. The large amount of competitors and spread of market share does not warrant any dominant position premium to YETI’s valuation.

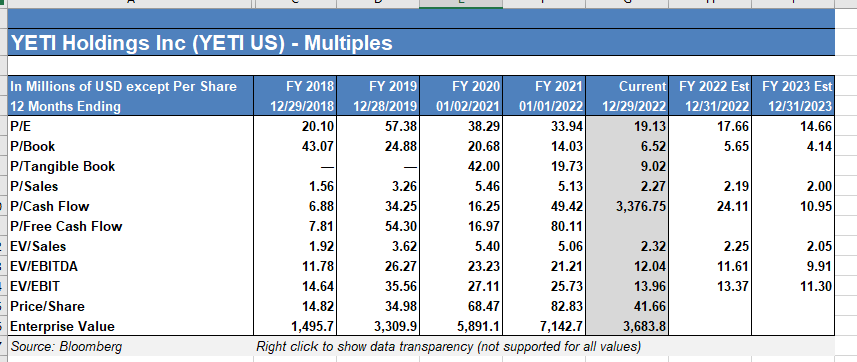

YETI’s valuation has become more reasonable, down from the pandemic highs of PE of 38 and P/S of 5.5, to 19 P/E and 2.3 P/S currently. However, we can’t conclude a cheaper valuation here as the macro dynamic has drastically changed. This new era of higher interest rates is unlikely to abate quickly with components of inflation likely to remain above long-term averages for the next few years. Combine that with the slower macro trends in growth forecasted for next year.

YETI Valuation Historic (Bloomberg)

If we analyze a GICS valuation comparison (below), we notice that YETI has solid gross and net margins and a forward PE lower than the industry average. I used a sector average of 19 of the largest companies to give a similar market cap to YETI for a fair comparison.Financial_Metrics_2.xlsx

I used Columbia Sportswear also as a comparable outdoor lifestyle brand company as Patagonia is private and North Face fundamentals are wrapped in VF Corporation valuation. We can see YETI again has lower forward PE but expensive on a sales and book basis. Margins are comparable between YETI and Columbia but YETI’s higher ROA, ROE and ROI indicate managements efficiency in asset utilization and carrying out their strategy namely successful marketing campaigns. The market may be slightly undervaluing YETI’s potential here, but I think the depressed share price (impacting multiples) is probably wrapped up in the macro growth sell off story. In any case the differences are not so meaningful to represent an arbitrage opportunity and therefore current valuation looks reasonable to me.

YETI Valuation Metrics (Finviz.com)

Risks to YETI’s performance:

Drinkware, Coolers and backpacks make up 98% of YETI’s product range which is narrow when compared to the likes of Patagonia, North Face and Columbia. There is a risk that YETI’s failure to innovate into other product ranges will lead to stagnant performance. The addressable markets of coolers and drinkware are not massive and failure to identify other successful growth markets could limit consumer interest and share price appreciation in the future.

Motley Fool also drew attention to the idea that YETI products are so durable that it may prevent consumers from needing to become recurring customers. All the more reason to increase product range.

The LEI (leading Economic Index) index, ISM new orders, consumer sentiment, reduced pandemic savings buffer, higher FED funds rate etc. There are many statistics arguing the economy is heading for a slower growth environment in 2023. Slowing revenue growth can derail share price gains especially for purported high growth companies. The high price point of $300-$500 for a cooler and between $30 and $50 for a drinks bottle may cause consumers to trade down to cheaper alternatives.

Management so far do not see this as an issue and one of the best questions on the Q3 Earnings call probed this very concern:

Sharon Zackfia – William Blair

“I guess I’m curious, there’s definitely a thesis on Wall Street that YETI is benefited from pull forward in demand. You’ve clearly been doing well all year on the top-line than that as you look into kind of ’23 what are your indicators on whether you can kind of hold the vast, long-term held goal for 10% to 15% revenue growth?”

“Good morning, Sharon. When it comes to the thesis that you mentioned, I would say it’s a little bit of a head scratcher to us, because we’ve been a consistent grower year-after-year for a number of years within — well within the ranges that you’re talking about and above. And we’ve talked through the pandemic moment in time where we grew through that disruption, we were growing at similar rates pre-pandemic on the other side of it. We’ve had a great year through the first three quarters this year.”

While Christmas is usually their strongest period as shown by Google Trends interest below, I would think price will become a more significant factor in the new year (despite CEO’s comments) which may hurt demand for YETI’s expensive product lines.

High pricing is obviously an issue but in push back, the likes of Apple and Lululemon provide premium products with not always the best quality in the industry but it’s their marketing strategy that catapults their performance. Given this can YETI’s future marketing campaigns continue to ignite interest in the brand?

The CEO mentioned on the call he expected shipping costs and inventory issues due to pandemic supply chain and inflation pressures to improve in 2023 improving margins. There’s a lot of commentary out there on inflation easing and I fully expect problems to be more driven from the demand side. But a risk to consider, nonetheless.

Christmas bounce in YETI interest:

YETI Search Trends (Google Trends)

I will be looking out for the following on Feb 16th2023 Earnings call as next means for assessing prospects:

- Is the company experiencing any slowdown in revenue growth?

- Progress on freight times, product cost, is inflation impacting margins?

- Leverage branding to expand product offering.

- International expansion metrics

- How is DTC impacting margin improvement.

Conclusion:

I think the key for YETI to grow exponentially, compete with the likes of other large lifestyle brands and provide real shareholder value is an expanded product offering. 98% of YETI products are in 2 markets. The price point further limits their target market and cheaper alternatives exist to question their “quality product” thesis. Despite this, the marketing department has done wonderfully in creating a brand image around the outdoor lifestyle experience and the “coolness factor” well and truly exists with their products.

YETI is currently fairly priced compared to competitors, its fundamentals and considering the macro backdrop. The product range is not phenomenal to warrant an investment just yet; coolers and water bottles, hardly rocket science with low barriers to entry.

I will keep on my radar for the time being as there’s big brand potential/growth opportunity if product innovation was to meaningfully increase. An early stage Lululemon comes to mind.

For now, I would hold off on any deployment of capital to YETI, I need more evidence that the company is a long-term winner.

Be the first to comment