Sucharas wongpeth

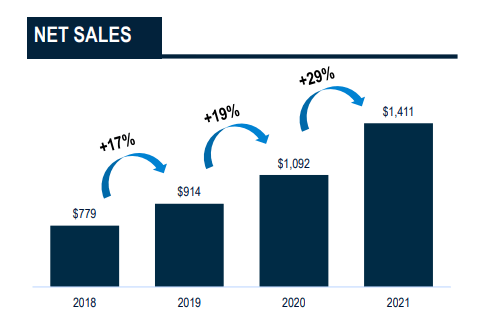

Given the challenging economic environment we believe YETI (NYSE:YETI) posted solid third quarter results, delivering a 20% sales increase. So far this year the company has delivered a year to date 19% top-line growth. Unfortunately inflationary pressures, including supply chain and shipping headwinds, have pressured the company’s profit margins and reduced earnings per share.

The company reported that corporate sales and YETI’s own stores have been sources of strength. In fact the company expects to have 13 stores by the end of this year, and to implement an accelerated pace of YETI store openings next year, as its stores are proving accretive to the business.

One of the biggest growth opportunities for the company remains international expansion. The company made good progress there with international sales growing ~60%, which increased the international sales mix to ~13%.

Overall we see good performance from the company, and we are surprised that shares are not trading higher given that the company is proving its growth is resilient. As we’ll see later in the article, the valuation remains attractive, although not what we would call an extreme bargain. We maintain our ‘Buy’ rating for the shares.

Q3 2022 Results

Third quarter sales increased 20% to $433.6 million compared to $362.6 million in the prior-year period. Direct-to-consumer sales grew 15% to $227.4 million, compared to $197.1 million in the same period last year. Direct-to-consumer performance included a healthy return to growth in the Amazon business.

Gross profit increased 7% to $222.4 million or 51.3% of sales, compared to $207 million or 57.1% of sales in the same period last year. The y/y contraction was primarily driven by a 490 basis point impact from higher inbound freight. Additional headwinds included 150 basis points from higher product costs, 70 basis points from unfavorable foreign currency exchange rates, 20 basis points from unfavorable channel and product mix, and 20 basis points from all other impacts. These headwinds were partially offset by 170 basis points from pricing actions.

Adjusted operating income decreased 1% to $73.3 million or 16.9% of sales, compared to $74.2 million or 20.5% of sales during the same period last year. Adjusted net income decreased 6% to $54.7 million or $0.63 per diluted share, compared to $58 million or $0.65 per diluted share in the previous year.

Growth

Some people believe that YETI benefited from pull forward in demand during the Covid crisis, and that is why it now deserves a lower valuation. While the company might have benefited from the increased focus on outdoor activities, we would like to point out that the company was growing at a good pace way before Covid, and has maintained a good growth rate after the worse of the Covid crisis has passed and up to the most recent quarter. We therefore believe the company deserves to be valued as a solid growth company, and not one that benefited from a one-time event.

YETI Investor Presentation

Balance Sheet

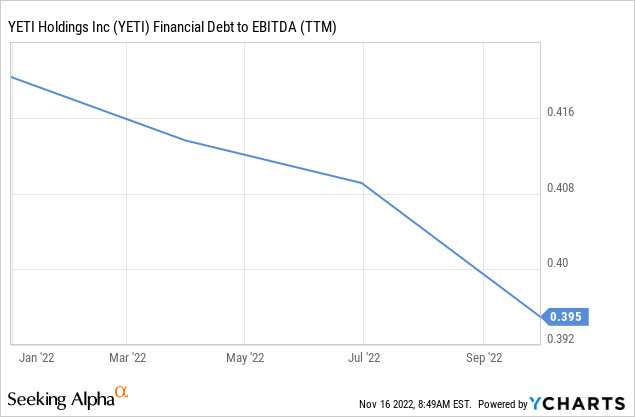

YETI ended the third quarter with $77.8 million in cash compared to $259.3 million the previous year. The lower cash position reflects share repurchases and working capital needs. For instance, inventory increased 65% to $439.4 million compared to $266 million during the same quarter last year. Total debt excluding unamortized deferred financing fees and finance leases was $95.6 million compared to $118.1 million at the end of last year’s third quarter.

Given the fact that the company has similar amounts of cash and total debt, and a very low financial debt to EBITDA ratio, we consider the balance sheet to be very healthy.

Guidance

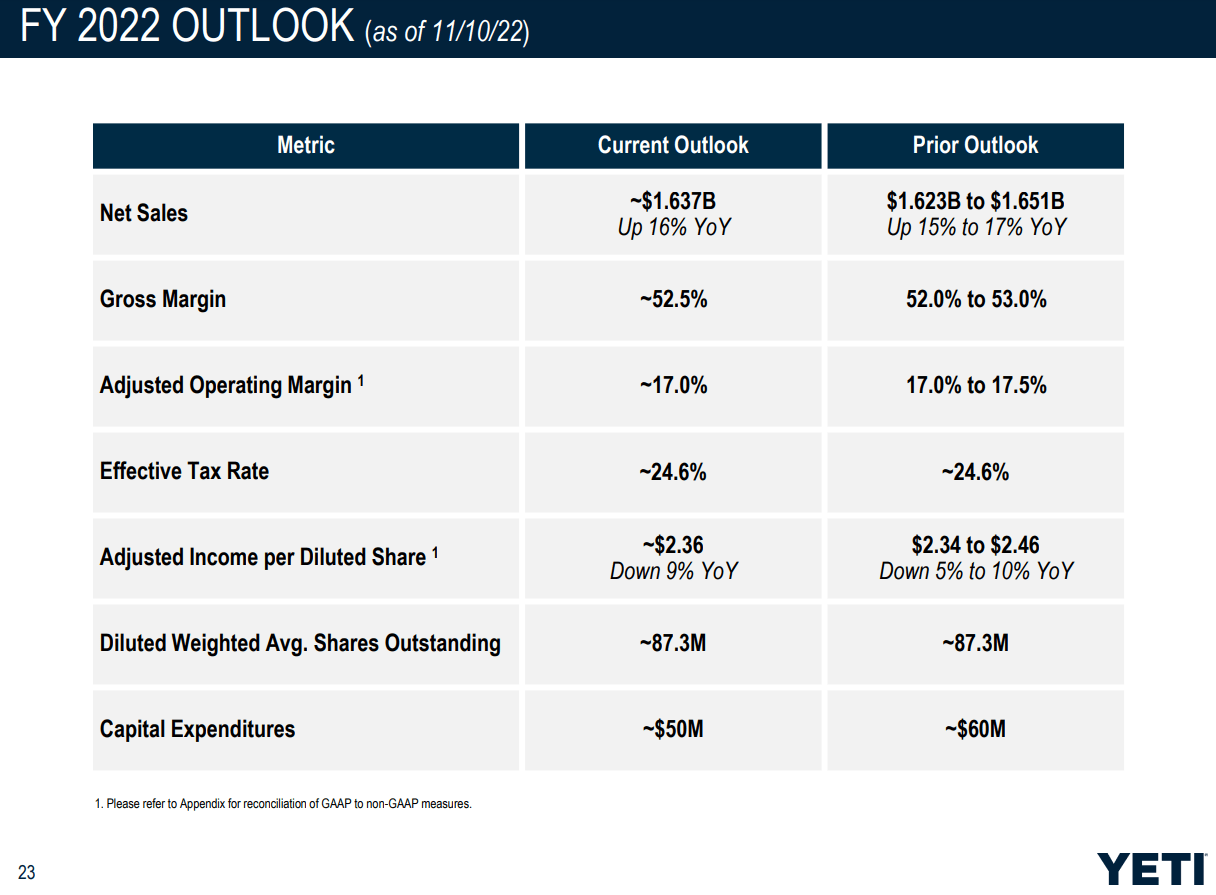

For the full year 2022 the company expects sales to increase approximately 16% compared to fiscal 2021. Higher inbound freight expenses are expected to impact gross margins by approximately 500 basis points, driving the majority of the overall y/y decline. On a positive note, ocean rates continue to decline sharply from peak levels, which is expected to be a source of margin recovery moving into 2023.

The company expects to achieve an adjusted operating margin of approximately 17% for the year, with adjusted earnings per diluted share of approximately $2.36 compared to $2.60 in fiscal 2021.

YETI Investor Presentation

Pricing

Given the inflationary pressures the company is experiencing, which are significantly affecting profitability, a natural question to ask is why the company has not been more aggressive with its pricing. Fortunately someone asked this question during the Q&A session of the most recent earnings call, and this is what CEO Matt Reintjes had to say:

We don’t use as you know, pricing as a lever. We very sparingly use that. We like where our products are priced. We like the consistency of our pricing. We think that’s a good consumer experience. And I think as you — to some of the questions around the promotional environment. We — it’s a highly promotional environment right now. YETI has retained being above that, as someone mentioned earlier and consistent with ways we’ve priced and we promoted before.

What we’re using this environment right now to do is to drive some transition of some products to bring in new innovation. It has the double benefit of some of the inventory we carry today is at a higher level, because of the supply chain costs and some of the innovation that we have coming. And so we’re using this sort of unique point in time to leverage our traditional approach to product transition, maybe accelerate a couple things and get some stuff into the market as we go into 2023.

Valuation

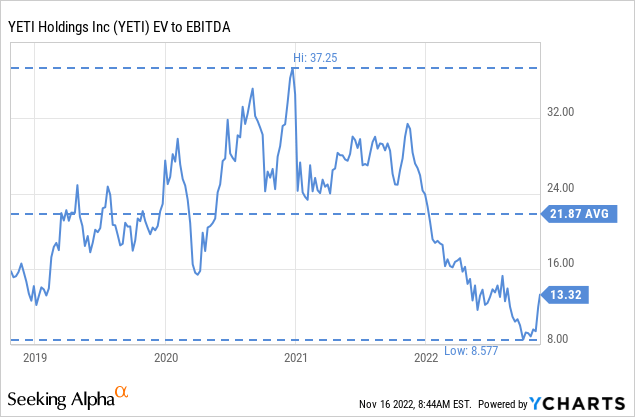

For a growth company, we find the EV/EBITDA ratio to be quite reasonable at ~13x. While we will not argue this is a bargain, but we believe it is a fair price to pay for a company that has proven it can consistently grow sales rapidly and that is already profitable.

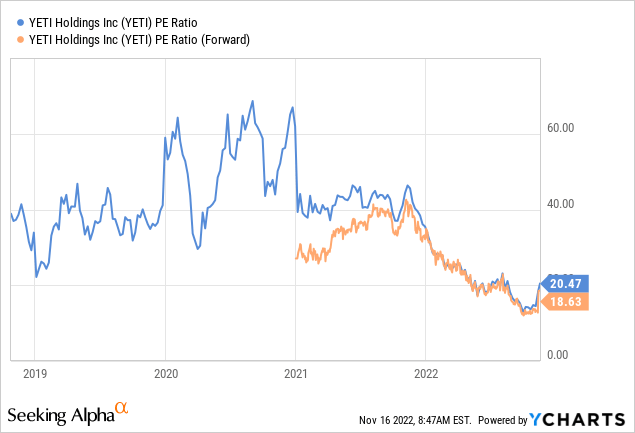

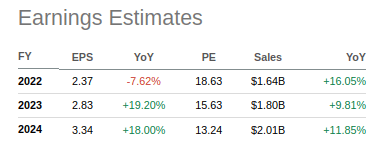

A ~20x price/earnings ratio for a company that can grow sales at ~20% seems quite fair to us, and looking at analyst’s earnings estimates we can see that the forward p/e’s come down quite quickly.

For example, based on earnings estimates for 2024, the forward price/earnings is an undemanding ~13x.

Seeking Alpha

Risks

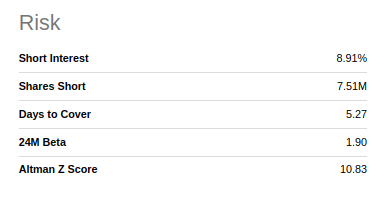

The biggest risk we see with an investment in YETI is growth decelerating. So far the company has proven its growth to be resilient, despite the challenging environment. To maintain a strong brand the company has to make sure the quality of its products remains excellent. In terms of financial strength, the company has a solid balance sheet and a very high Altman Z-score.

Seeking Alpha

Conclusion

We found YETI’s third quarter results to be quite solid given the macro-economic environment. It was not surprising that profit margins came under pressure given the inflationary conditions, including supply chain and transportation headwinds. The company still managed to deliver ~20% growth, which we believe proves that it was not a one-time beneficiary of the focus on outdoor activities during Covid. Overall we believe shares still offer value at current prices, with a p/e ratio of ~20x and growing sales at ~20%.

Be the first to comment