bgton

Summary

I see a 24% upside to YETI Holdings (NYSE:YETI). The broad thesis is that YETI has a premium lifestyle brand, strong innovation, and successful omni-channel strategy. YETI has expanded its product offerings to meet the changing needs of consumers and has a strong DTC sales channel that allows for direct engagement with customers and higher profit margins. Additionally, the improvement in inventory management and higher margins expected in 2023 provide a positive outlook for the company.

Company overview

With roots in coolers and other insulated drinkware, YETI has expanded into the design, marketing, distribution, and retail of a wide range of branded, premium outdoor products.

A premium lifestyle brand

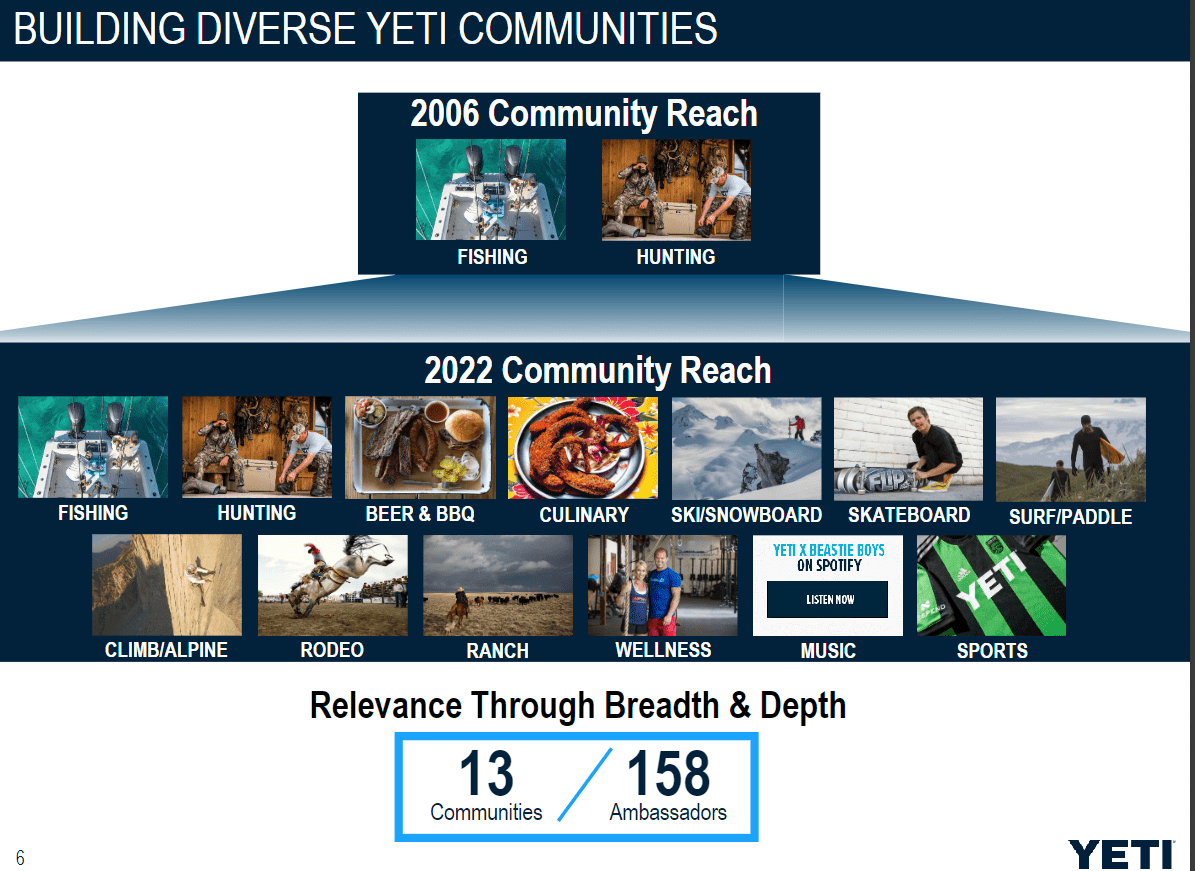

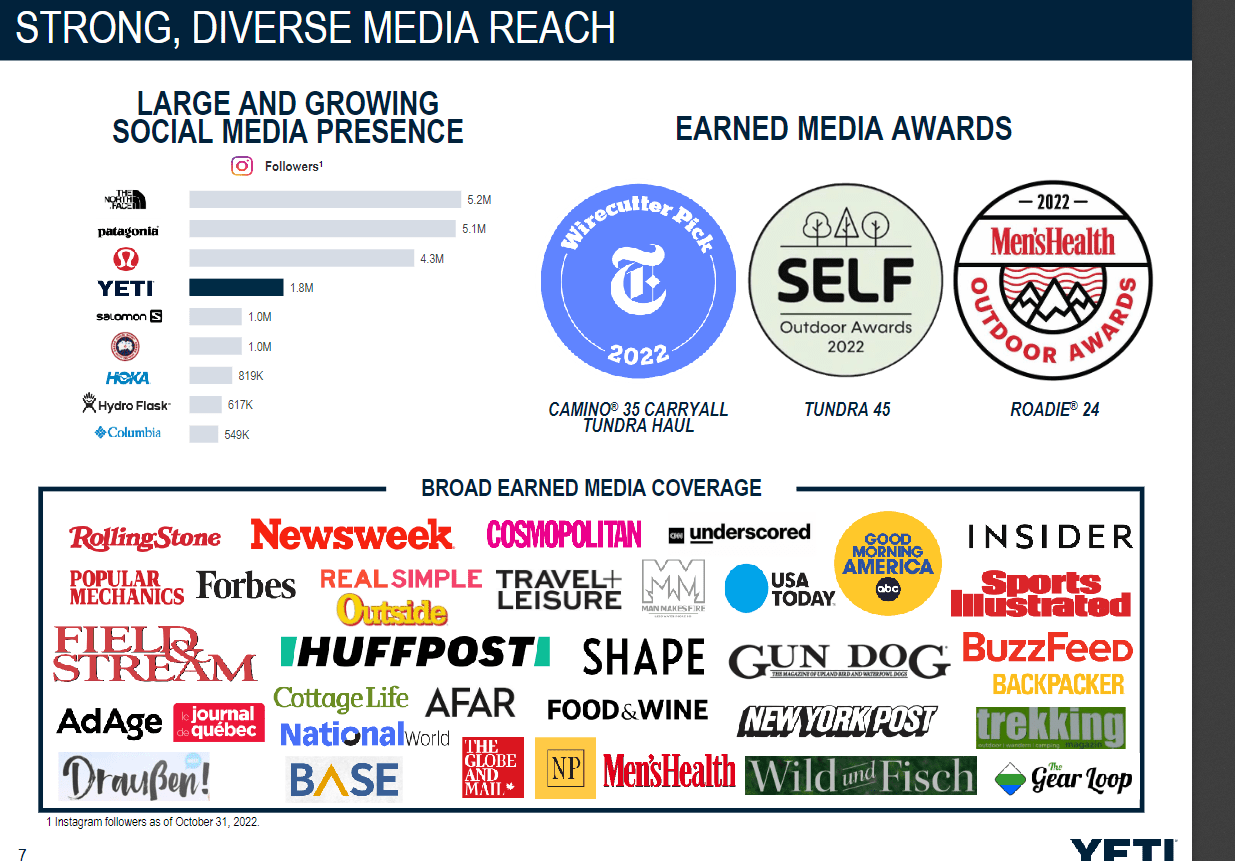

When I think of YETI, I think of the outdoors. Which stands out from the competition because of its superior performance in key areas. I think YETI sells a high-quality product because its customers believe it will last a long time and perform well. To complement this, YETI has put considerable resources behind its brand with a strategic marketing plan that encompasses a wide range of potential customers. A key part of YETI marketing strategy is carefully selecting a group of brand ambassadors who are highly influential in the active and outdoor communities to help spread the word about the company and its products.

Study results from 2022 show that YETI’s brand positioning has improved by a factor of two since 2016. For YETI, expanding its already massive online following via social media is a key part of the company’s larger plan to raise the profile of the YETI brand.

3Q22 earnings 3Q22 earnings

A strong innovator

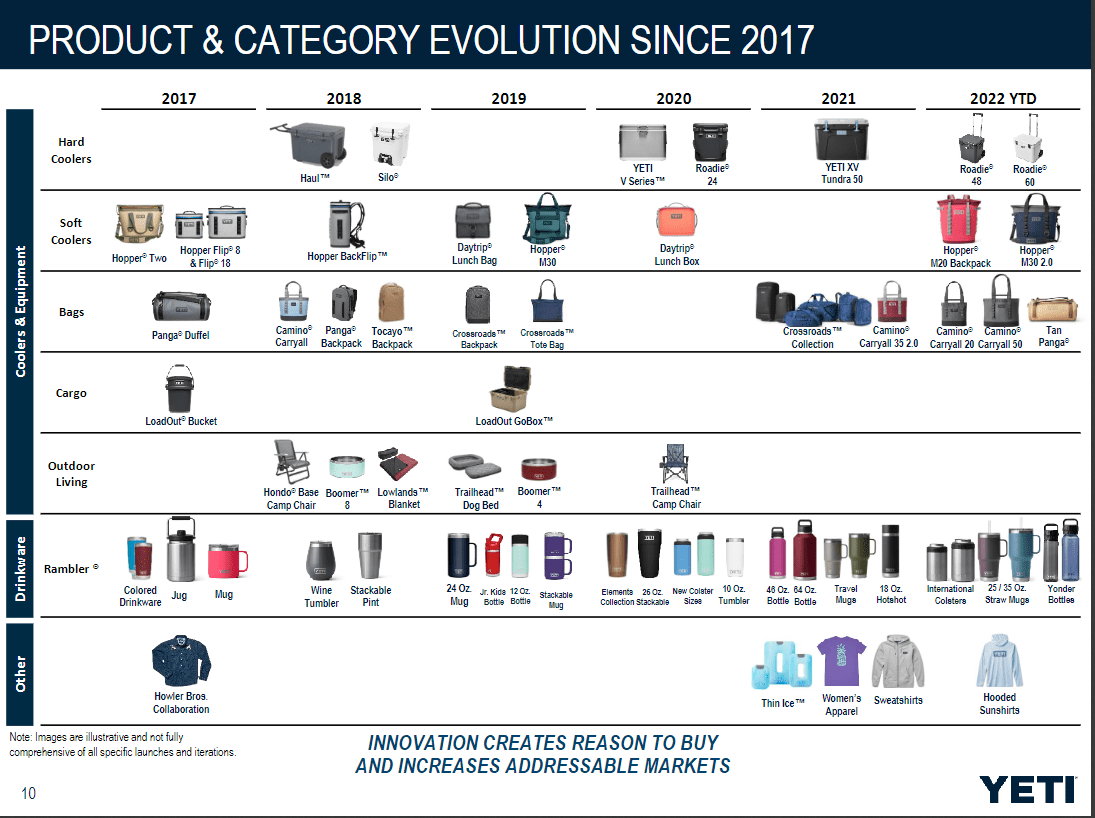

In my opinion, YETI is a forward-thinking company with the potential for global growth and the ability to carve out new niches in existing markets. When considering the company’s history, it is clear that YETI initially focused on selling tumblers and hard coolers, but it has since branched out into other drinkware and cooler products that are relevant to the core YETI consumer. Indeed, innovation has become increasingly rapid in recent years. YETI’s rapid expansion can be traced back to the introduction of its soft cooler line and drinkware in the middle of 2014, which were met with immediate success due to their low cost in comparison to hard coolers and wide range of potential applications. Since then, the company has released a wheeled hard cooler in addition to an improved line of soft coolers (refer to diagram below). The range of drinkware available is one area that has grown significantly as a result of this expansion.

All in all, I think this is an important attribute to have because it allows YETI to do 2 things:

- Meet the needs of the ever-changing consumer preferences (either style, type, or activities)

- Expand its TAM to continuously extend its growth runway

3Q22 earnings

Omni-channels strategy

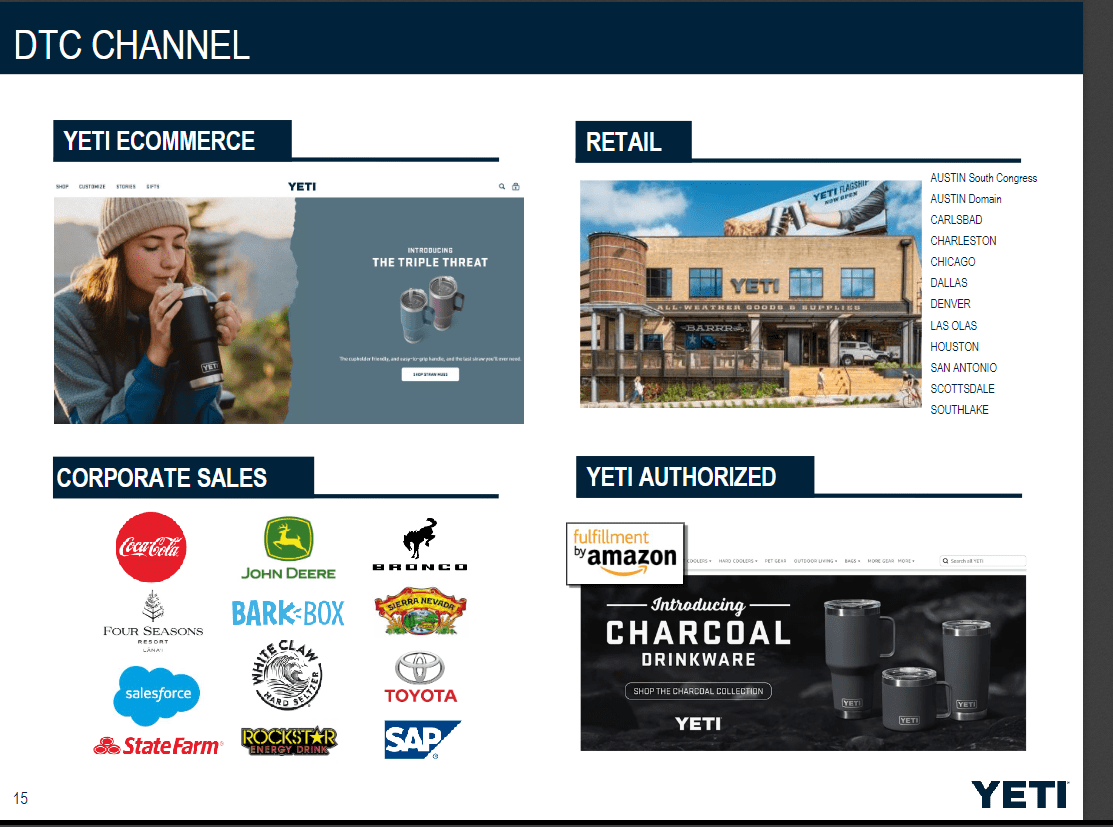

YETI’s product distribution network encompasses both wholesale and direct-to-consumer avenues [DTC]. YETI’s wholesale business operates through a network of carefully chosen accounts and independent retail partners. On the other hand, the DTC channel is made up mainly of online and inside sales. The DTC channel is the higher performance which has expanded at a rapid pace. In my opinion, DTC sales now account for roughly 50% of all sales. I think this DTC channel is crucial because it allows YETI to have a engage directly with its customers, have greater control over the brand experience, gain insight into end-users preferences, and provide unique products. I also think that YETI’s command of the DTC market helps to foster the deepest possible level of customer involvement with the brand, which in turn strengthens customer loyalty and yields healthy profit margins.

As the company increases its brand presence on its own direct-to-consumer website and custom shop, I expect DTC sales to continue to grow at a double-digit rate. Additionally, I believe YETI will increase its focus on corporate sales clients through a dedicated sales program, leading to higher sales through third-party marketplaces.

3Q22 earnings

With the introduction of new products and the expansion of the YETI brand into underpenetrated regions, I expect the wholesale channel to continue growing modestly. In addition, I anticipate concentrated growth in international wholesale to be a primary factor driving this channel, with expansion occurring primarily in mature international markets. YETI generally concentrates on a few carefully chosen premium distribution channels, focusing on independent accounts with brand position aligned with YETI. To maintain this premium position, YETI has recently undertaken a drastic rationalization of its independent dealer network. I do not anticipate significant long-term growth in new accounts for YETI due to the size of its Wholesale partner footprint. Instead, I anticipate this channel’s expansion to result primarily from increased sales to existing accounts, demand for new offerings, and enhanced consumer recognition of existing products.

3Q22 earnings

Recent performance was stellar

The results for 3Q22 for YETI were outstanding. During the period under review, YETI’s demand showed remarkable resilience, expanding strongly in both its DTC and wholesale channels, expanding healthily on a global scale, and expanding robustly across all product lines. A strong growth result for YETI is, in my opinion, evidence of the brand’s strength and the company’s ability to consistently introduce new and exciting products to the market. While I anticipate that the risk of a choppy macro and heightened competition will persist as top-line growth normalizes following a restocking year, I also anticipate that the risk will be mitigated by improved inventory management and higher margins into 2023 as a result of the normalization of freight cost pressure.

- Inventory management (positive): At the end of the third quarter, inventory dropped to $439 million, a decrease of about 10% from the previous quarter. I found it encouraging that the gap between inventory growth and sales growth narrowed significantly from the previous quarter to the current one. The management also saw an improvement in inventory levels compared to the previous year.

- Wholesale performance (positive): Sales through the wholesale channel increased by 25%, an increase from the 21% seen in 2Q, thanks to the continued demand for coolers and an improved inventory position. In addition to YETI core products, Bags were also singled out as a key factor in the expansion.

In terms of guidance, Management now expects full-year sales growth of 16%, up from the previous guide of 15 to 17%, and adjusted earnings per share of $2.36, which is in the lower range of the previous guide. Similarly, management has guided to an adjusted operating margin of 17%, which is at the low end of previous guidance.

Valuation

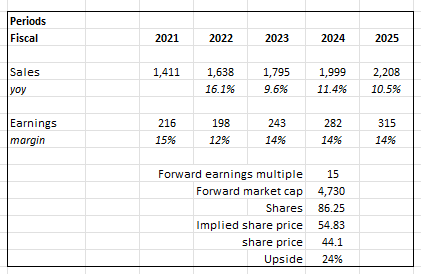

I believe YETI there is 24% upside. Using consensus estimates, it is expected that YETI will achieve $2.2 billion in revenue and ~$315 million in earnings in FY25.

I believe the stock is headed in the right direction to continue rising because cost pressures will likely ease in the near future, and expectations have been reset. In light of the lowered expectations and the fact that the company is maintaining its FY outlook within the previous range, I believe the stock is on the right path to realizing further upsides. Furthermore, freight and product cost pressures are expected to moderate this year, which will improve YETI’s margin profile going forward. Moreover, the current valuation of 15x forward earnings is lower than the historical average of 25x over the past decade. In sum, I believe the stock’s potential for growth exceeds my current expectations.

Own calculations

Risk

Brand dilution

Traditionally, the company has excelled at producing high-quality coolers and drinkware that can last for years without being replaced. While the company’s foray into new product categories has increased its reach and revenue potential, I worry that consumers will become less loyal to the brand and less receptive to new offerings.

Conclusion

YETI is a premium lifestyle brand that stands out from its competitors due to its exceptional performance in key areas. The company is highly innovative, with the potential for global expansion and the ability to create new opportunities in existing markets. YETI has a strong omni-channel strategy, including a growing DTC channel, which allows for deeper customer connections and higher profits. Recently, the company has seen exceptional growth, expanding both its DTC and wholesale channels. Additionally, YETI is expected to see increased profits through 2023 due to the stabilization of shipping costs. Overall, YETI is a strong business with a strong brand and a strong growth strategy.

Be the first to comment