Pgiam/iStock via Getty Images

Today, Yara International ASA (OTCPK:YARIY; OTCPK:YRAIF) just released its three months accounts. Here at the Lab, we have been negative about the company lately – despite our optimistic view on the long-term opportunity, we were more skeptical about the short-term horizon. Today’s performances were outstanding, and it is not coming as a surprise that Yara’s stock price is up by more than 6%.

We have analyzed the Norwegian company twice already in 2022, and we recommend that our readers check up on our previous publications to get acquainted with the story up to now:

- Yara: Too Much Short Term Turbulence, A Pass At This Price

- Yara International Still With Mixed Feelings

Q3 Results

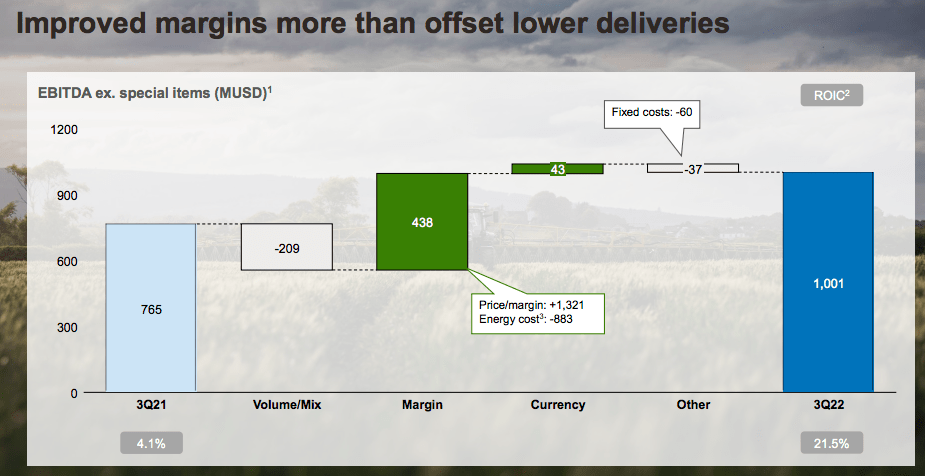

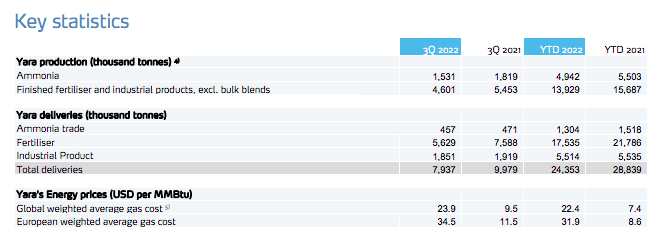

Yara delivered a strong set of numbers compared to Q3 2021. However, on a quarterly basis, the company achieved lower profitability at the EBITDA level. Numbers in hand, the Norwegian company increased top-line sales by 38% reaching $6.2 billion compared to last year’s quarterly results. EBITDA margin stood at almost 17% versus Q3 2021 and Q2 2022 at 2.6% and 23.4% respectively. Cross-checking the Wall Street estimates, the company was 23% above consensus expectations. Indeed, Yara manages to achieve a positive pricing delta outpacing higher energy prices (fig 2) and raw material inflationary cost pressure. On the volume side (still presented in figure 2), Yara’s production was lower both in the ammonia as well as in the finished fertilizer & industrial outputs. Production was also negatively impacted by the EU gas shortage. Important to note, as already discussed in our last analysis, the company has only two production facilities located in Germany so, in the case of gas curtailments, this would not be disruptive to the company’s production capability.

Yara EBITDA Evolution (Yara International ASA Q3 Results)

Yara Productions and Energy Price (Yara International ASA Q3 Press Release (Fig 2))

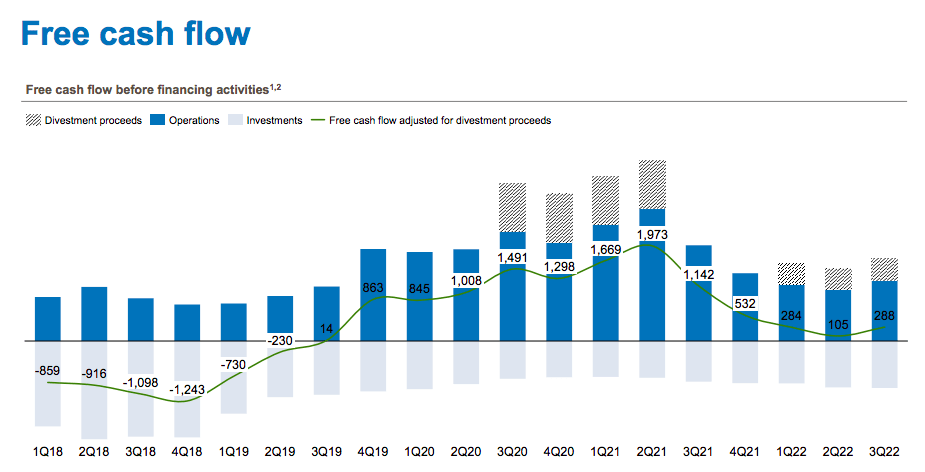

On the upside, Yara was positively impacted by the currency effects, totaling a plus $43 million in the quarter. Costumers inventories are still at a historic low and the company disclosed that there are no new projects on additional Urea capacity expansion. From a free cash flow perspective, it seems that we reached a bottom, and we are heading toward the upper end of the U-turn (Fig 3). It seems that raw material costs and energy price developments are easing, and working capital requirements should soon revert (positively impacting Yara’s cash position). For the above reason, the company also announced a NOK10 dividend per share that was positively welcome by Wall Street.

Yara FCF Evolution (Yara International ASA Q3 Results (Fig 3))

Conclusion and Valuation

Thanks to the strong results achieved by the company (even in this uncertain time), we decided to move our rating from underperforming to neutral, rolling our average 12-month forward EBITDA estimate. Then, we derive a price of NOK450 per share, based on a 4.5x multiple.

Mare Evidence Lab’s previous coverage within the sector:

- Corteva: Comment On The Investor Day

- Corteva: Additional Upside

- LSB Industries: Still A Good Investment Against Inflation?

Be the first to comment