LuckyViks

Note: both companies have multiple listings – Yamana Gold is listed on TSX and LSE while Gold Fields trades on JSE and SWX. This write-up refers to their NYSE tickers and spread.

South African mining group Gold Fields Limited (GFI) is buying Canadian peer Yamana Gold Inc. (NYSE:AUY). The consideration is all-stock – 0.6 GFI shares for each AUY share. The merger requires regulatory and shareholder approvals from both the buyer and the target. While regulatory and AUY equity holder approvals seem very likely, the main uncertainty here appears to be buyer’s shareholder approval. Upon the merger announcement on May 31, GFI’s stock plunged 24% reflecting shareholder hostility. In mid-June, GFI’s two large shareholders, fund managers VanEck (5% stake) and Redwheel (3%), voiced their opposition towards the transaction, claiming that it is too expensive and untimely for the buyer.

Initially, the merger spread stood at 5% but has widened massively since the reports of shareholder opposition, reaching as much as 22%. On July 15, GFI’s CEO stated that some positive progress in shareholder discussions has been made. The spread somewhat narrowed but remains wide at 13%. Shareholder meetings will be held in October and the companies expect the merger to close in H2’22.

Yahoo Finance

GFI’s shareholder approval is far from guaranteed. However, I see several arguments suggesting that GFI’s management will eventually secure shareholder consent:

-

The merger seems to have a strong strategic rationale for the buyer given AUY’s low-cost mine portfolio and numerous long-term exploration/development assets that GFI currently lacks.

-

GFI’s management has put a lot of effort behind communicating with GFI equity holders and pointing them to the deal’s rationale. According to ICE’s CEO, progress has been made and “many shareholders are starting to say “we get it.” Moreover, the management has recently agreed to raise its dividend payout ratio after the acquisition closes in an effort to appease shareholders.

-

Key shareholder VanEck’s history with the Newmont-Goldcorp merger suggests that it could eventually support current acquisition.

-

Similar industry transactions reveal that, despite the significant premium over the trading price, AUY is valued at a fairly low EV/EBITDA multiple.

Strategic Rationale

Let’s start with the strategic rationale. In my view, the main benefit for GFI here is that the transaction will expand the company’s long-term asset pipeline. Despite being the sixth largest gold producer (as of 2020), GFI operates mostly near-term operating cash flow assets whose production is expected to decline in the upcoming decade. GFI’s standalone production is projected to peak at 2.8 Moz in 2027 before steeply falling to around 2m ounces per year. A quote from GFI CEO summarizes this nicely:

“We still have a runway over the next few years or so to continually grow both the cash flow and the volume [of gold we produce]. But if we look at the next 10 years, we don’t have the projects, we don’t have the pipeline of assets in our own portfolio.”

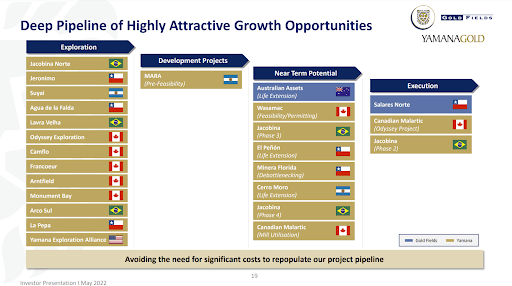

GFI’s only large development asset is Salares Norte mine in Chile, however, its measured and indicated (M&I) resources stand at only 4.5 Moz – insignificant compared to current GFI’s annual production.

AUY, on the other hand, has numerous exploration/ development/ feasibility-stage assets. Some examples:

-

MARA mine in Argentina. AUY has a 56% ownership stake. M&I resources are estimated at 48.1 Moz – by far the largest among AUY current assets and second only to GFI’s key South Deep mine. P&P reserves include 7.4 Moz of gold. Feasibility study is expected to be completed by the end of 2022. Expected mine life is 28 years.

-

Wasamac mine in Canada. P&P reserves estimated at 1.9 Moz. Production is expected to begin in 2026, reaching ~500k oz annually by 2028 and will keep these production levels until at least 2041.

-

Malartic Odyssey mine in Canada. This is an underground extension of AUY’s largest open pit mine. It is expected to extend mine’s life to at least 2039. GFI has a 50% ownership in the project. Expected peak production is 500k-600k oz annually.

There are numerous other projects in AUY’s exploration pipeline. In this light, the merger provides GFI with future growth optionalities that the current business somewhat lacks. Importantly, the acquisition will also expand GFI’s portfolio with a world-class asset – Canadian Malartic – which is a top 10 gold mine by production globally. The mine has an annual production of ~700k oz (by far the most among the two companies) and an expected mine life to at least 2040. AUY holds a 50% ownership stake.

Yamana Gold and Gold Fields Investor Presentation, May 31, 2022

Another benefit for the buyer – diversification of its asset portfolio. Whereas GFI has only one mine in the Americas in addition to Salares Norte (Cerro Corona in Peru), AUY operates mines exclusively in the Americas. However, Cerro’s M&I resources are only at 1.7 Moz. Besides providing diversification, gold assets in the Americas region generally have lower All-In Sustaining Costs (AISC). In 2021, AUY’s AISC stood at $1,030/oz. For reference, the industry average was $1,068/oz while GFI achieved $1,063/oz. For this reason, addition of AUY’s mines is expected to make the combined company the second lowest-cost producer among the gold majors.

The merger is expected to save $40m run-rate annual overhead and procurement savings. This is quite significant – for comparison, AUY has guided for $86m in 2022 G&A expenses. Synergies are projected to mostly come from South America as both companies operate mines in Chile.

Shareholders

Thresholds for shareholder approvals are at two-thirds of the votes cast for AUY and 50% of votes cast for GFI (with at least 75% of the total voting rights exercised). Given the proposal’s premium to the share price at the time (34% to AUY’s 10-day VWAP), I expect AUY shareholders to approve the merger. Reportedly, this premium is the second-highest in gold miner acquisitions the last 5 years. Another important aspect – the deal is all-stock, which gives target’s shareholders the opportunity to capitalize on the projects that the combined company will have in its pipeline.

Meanwhile, GFI’s shareholders – Redwheel and VanEck – have criticized the offer as overvaluing AUY. While Redwheel has openly pushed GFI to abandon the deal and pushed for share buybacks instead, VanEck described the deal as “poorly structured.” Here it is important to note that VanEck is also a large shareholder in AUY and owns 12%, showing the importance of this equity holder in the setup.

Having said that, see a few positives pointing to shareholder approval in addition to strong strategic rationale:

-

GFI’s management team has put its best efforts to convince shareholders. Apparently, GFI’s CEO expected the share price drop given that the rationale “wasn’t going to be an immediately obvious deal to shareholders.” GFI’s CEO as of July 26:

“Many of the Gold Fields shareholders don’t really know Yamana and the Yamana assets, and likewise with Yamana, many of them won’t know Gold Fields. We still see a really, really strong underlying strategic rationale for this deal.”

The management seems confident about the progress made since the proposal and reportedly has had “constructive” discussions with Redwheel. AUY’s Chairman has also expressed confidence when speaking about approvals from GFI shareholders:

“And our impression is that ultimately, those shareholders, I don’t mean to be presumptuous, but ultimately those shareholders would be supportive of the deal. They take comfort in what we are saying, because it underpins what Gold Fields has been saying, which is that we have conducted, I am speaking for them, but we have conducted seven months of diligence. And this is what we come up with.”

Moreover, the buyer has recently improved the offer. GFI will increase the company’s payout ratio to 30%-45% of normalized earnings from the previous 25%-30% range. This addresses one of the main concerns of shareholders who have said that capital returns/dividends would create more value.

-

GFI’s other large shareholders – institutional investors Blackrock (10% stake) and Africa’s largest asset manager Public Investment Corporations (PIC, 9%) – have not voiced any opposition. Importantly, GFI’s CEO noted that discussions with PIC have reportedly been positive. Overall, GFI has a greater concentration among large shareholders which has also been highlighted by AUY’s Chairman. This should make it easier to get the shareholders to vote in order to reach the 75% threshold.

-

VanEck’s involvement with the Newmont-Goldcorp merger in 2019 seems comparable. At the time, the fund manager expressed concerns over the merger consideration and the fact that it would provide the target’s shareholders excessive value from Newmont’s then-recent joint venture. Along with another large shareholder, VanEck asked the buyer Newmont to renegotiate the deal. The acquisition valued Goldcorp at a 17% share price premium to pre-announcement prices. Interestingly, similarly as in GFI-AUY, the buyer Newmont also sweetened the offer with higher dividends which eventually led to VanEck’s approval. At the time, VanEck was among the top 3 shareholders in both companies.

-

The offer values AUY at ~6x EV/LTM EBITDA. Admittedly, comparison with past transactions on an EV/EBITDA basis is complicated given movements in gold prices. However, current gold futures quotes trade close in the ~$1750/oz-~$1900/oz range through 2025. This is similar to AUY’s average realized gold price LTM range of $1789/oz-$1878/oz. In this context, AUY’s LTM EBITDA seems reasonable. That said, only Agnico-Kirkland merger valued the target company at a lower multiple (5.5x). Meanwhile, other large transactions fetched higher multiples, including Barrick-Randgold (~7x) and Newmont-Goldcorp (~9x). Given this and the fact that the transaction brings Gold Fields among the top four gold majors, the current multiple seems warranted.

Other Gold Mining Mergers

|

Month Announced |

Buyer |

Target |

EV ($bn) |

EV/LTM EBITDA |

Premium over share price |

|

Sep’18 |

Barrick Gold |

Randgold Resources |

7.2 |

7.1 |

0% |

|

Jan’19 |

Newmont Corporation |

Goldcorp |

11.9 |

9.0 |

17% |

|

Sep’21 |

Agnico Eagle Mines |

Kirkland Lake Gold |

9.7 |

5.5 |

1% |

|

Nov’21 |

Newcrest Mining |

Pretium Resources |

2.6 |

8.5 |

29% |

|

May’22 |

Gold Fields |

Yamana Gold |

5.4 |

5.6 |

34% |

Source: Company filings.

Regulatory Approvals

The merger is subject to approvals from three regulators: South African Reserve Bank and two approvals in Canada under Competition Act and Investment Canada Act. However, this seems rather a formality given numerous successful foreign acquisitions of Canadian gold miners shown above, including Goldcorp and Pretium Resources. In recent years, the only gold miner merger blocked in Canada involved a Chinese state-owned company where the transaction received pushback on national security grounds.

Downside

Spread stood at 42% before the merger announcement which implies a 29% potential downside. Gold miner ETFs are down 20%-25% since the pre-announcement date. However, exposure to gold prices should be minimal given that this is a hedged trade.

|

ETF |

iShares MSCI Global Gold Miners ETF (RING) |

VanEck Gold Miners UCITS ETF (GDX) |

U.S. Global GO GOLD and Precious Metal Miners ETF (GOAU) |

Sprott Gold Miners ETF (SGDM) |

|

Price Movement Since May 30 |

-25% |

-20% |

-20% |

-21% |

Conclusion

I see this as an interesting setup currently offering a 13% return. The main risk – buyer’s shareholder approval – remains, but in my view does not justify the current spread. Moreover, the short, expected timeline suggests an attractive annualized return of 34% if the merger closes by the end of ’22. Given this, I am willing to play merger arbitrage here.

Great News

Our new premium marketplace service is on its way to launch on September 15! The marketplace will feature only our highest-conviction special situation investment ideas backed by high-quality/original research. More details are coming shortly so stay tuned!

Be the first to comment