Bet_Noire

Thesis

Turbulence in the broader market and steep declines in high-growth sectors has led more investor attention towards defensive exposure options. The Consumer Staples sector has performed relatively well in 2022 while offering favorable risk metrics over the long term. In this analysis, I explore the sector’s outlook and performance, as represented by the SPDR’s Consumer Staples Select Sector ETF (NYSEARCA:XLP).

Performance During A Turbulent Market

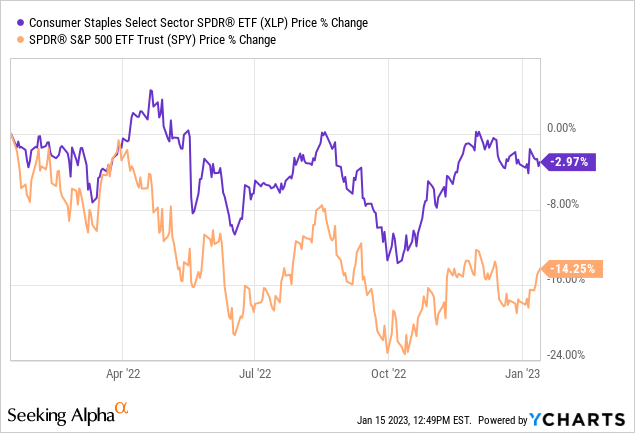

Without a doubt, 2022 has been a rough year for stocks, with all three major indexes recording significant losses. The technology sector has seen the largest drop, with other high-growth sectors following. The consumer staples sector has shown some overall resilience, despite elevated volatility. After an extended rally towards the end of the year, the sector looks to cover its losses. For the trailing one-year period, the sector has recorded a -2.97% decline compared to the broader market’s -14.25%.

A Defensive/Value Oriented Sector

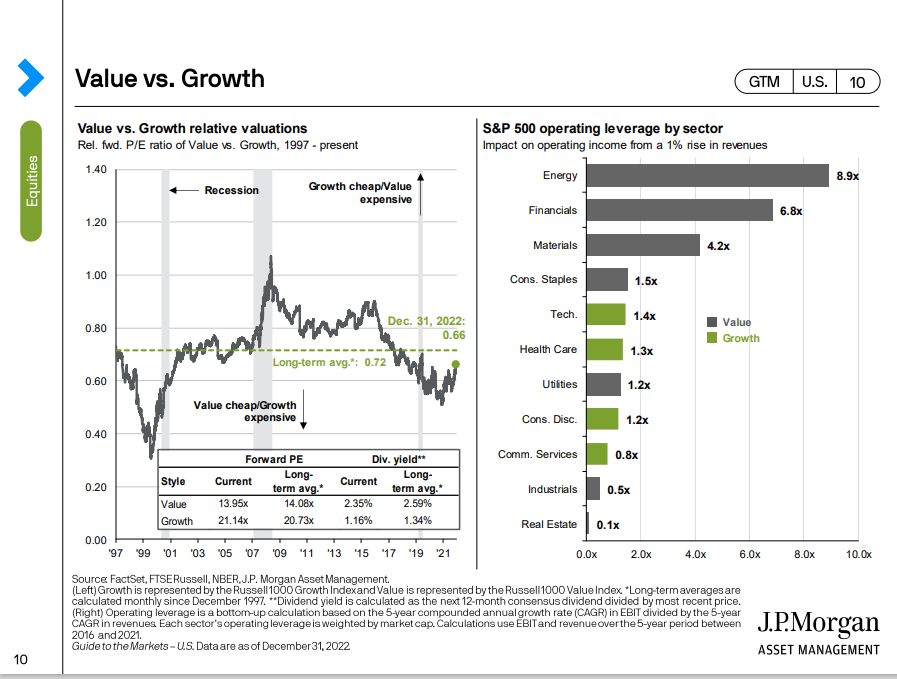

In an attempt to generalize a bit, we could argue that the U.S. stock market is going through a value phase for the past year or so. After a decade of growth overperformance, it seemed arguably inevitable that high valuation multiples would eventually subtract, reverting to historic means. After all, in the long-term, the value factor has been known to over-perform. Looking at the P/E ratio of Value vs Growth, provided in the chart below, it seems that still, despite the rerating in 2022, value stocks are, broadly speaking, more attractive.

The Consumer Staples sector is viewed by many analysts as a default value play, but that might not entirely be the case. Judging by operating leverage, the Consumer Staples sector appears to hung somewhere between Value and Growth factor loading. While its defensive nature usually earns better performance during downturns that does not guarantee a longer-term overperformance that would stem from undervalued stocks, trading at low P/E, EV/EBITDA or P/S multiples.

J.P. Morgan Asset Management

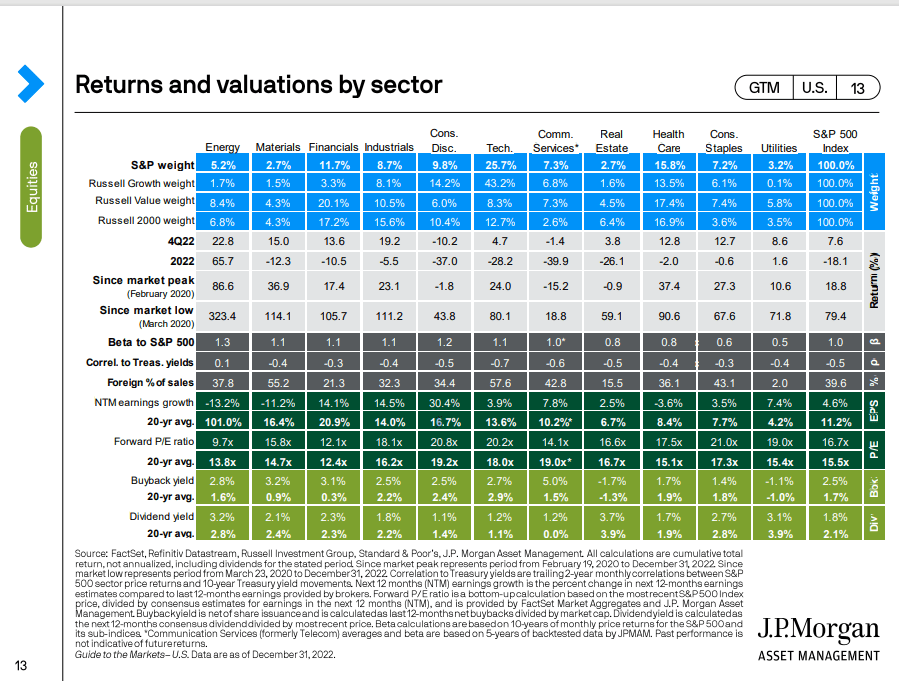

After the major revaluation of 2022 in high growth sectors, Consumer Staples holds the higher forward P/E valuation multiple in the market at 21.0x, slightly higher than the consumer discretionary sector (20.8x P/E). The Consumer Staples sector currently trades at a premium compared to its 20-year average P/E, while sectors like Financials, Energy and Communication trade at valuation discounts.

The dividend yield across the sector of 3.1% is also lower compared to its 20-year average of 3.9%, yet higher than almost all other sectors (excluding Real Estate, Utilities and Energy). The sector also has a positive, 1.4% buyback yield. The defensive nature of the sector is also confirmed by a low, 0.6 beta, indicating lower volatility swings, compared to the broader market. In fact, only Utilities appear to carry a lower beta.

J.P. Morgan Asset Management

Consumer Staples Vs. Discretionary Vs. S&P 500

Consumer goods and services have seen strong growth over the past 20 years. Consumer spending is the driving force of the economy and accounts for a large portion of the U.S. Gross Domestic Product. The consumer discretionary sector is more cyclical with stronger growth prospects, while the Consumer staples sector is more stable in performance.

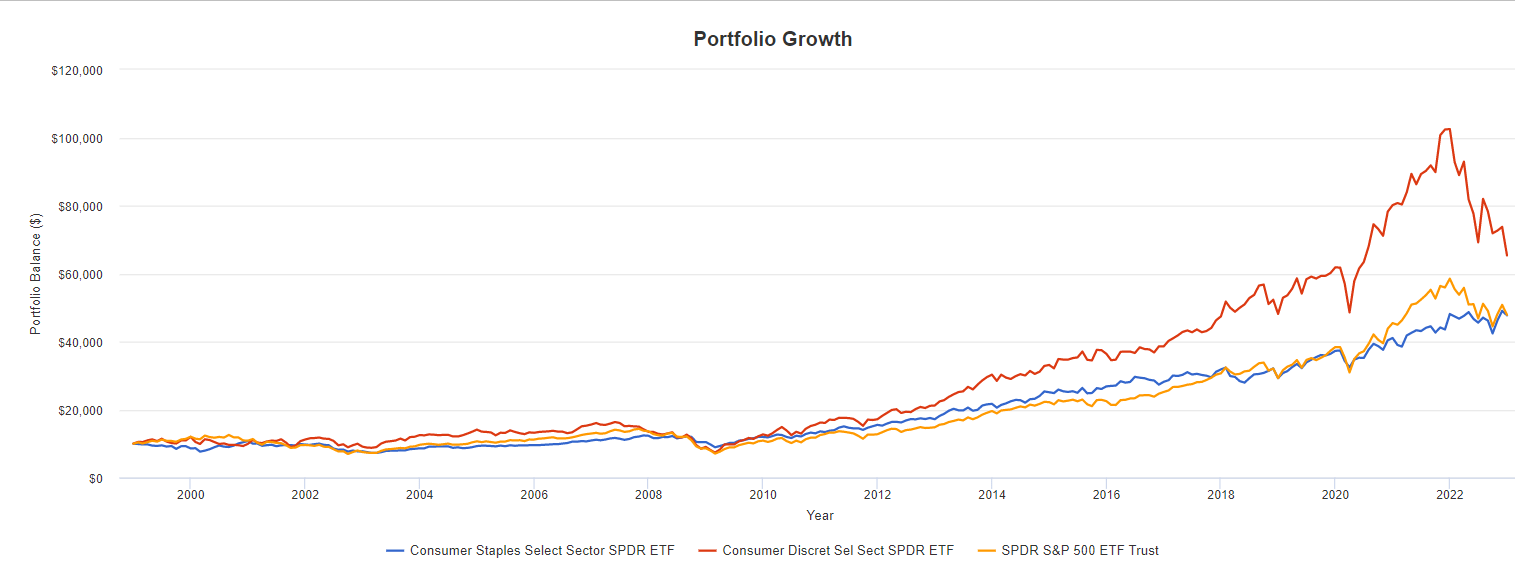

For a comparison analysis between the two sectors, I employed the tools offered by Portfolio Visualizer. The SPDR Consumer Staples Select Sector ETF was backtested alongside the SPDR Consumer Discretionary Select Sector ETF (XLY) and the S&P 500 ETF (SPY) to test return and risk performance. For the purpose of this analysis, a $10,000 starting balance and dividend reinvesting was assumed.

As easily visible in the chart below, XLY has significantly outperformed both the market and XLP over the past 20+ years. In fact, the performance gap becomes significantly larger after 2010 and only starts to close somewhat after 2021, when the Consumer Staples sector begins to perform better.

Portfolio visualizer

A $10,000 investment in XLP in 2000 would have returned $47,715 today (6.73% CAGR), while the same investment in XLY would have yielded $65,330 (8.13%). The consumer discretionary sector has outperformed the broader market, while the consumer staples sector has performed in par with the S&P 500.

In terms of risk metrics, however, XLP has recorded significantly lower volatility (standard deviation of 12.5%) in comparison to the S&P 500 (15.36%) and XLY (19.19%). It also recorded the smallest losses during its worst year, -20.10%. It might come as a surprise to many, but the Consumer Staples sector actually maintains the best risk-adjusted returns between the three investments, with a Sharpe ratio of 0.45 and Sortino ratio of 0.65. Naturally, XLP also has the lowest correlation to the market (0.60).

Portfolio Visualizer

In my view, after examining the results stemming from this analysis, it is prudent not to see this comparison as a binary choice between the two sectors and hence the two SPDR ETFs. They would arguably work better complimenting each other, with XLY capturing higher returns during periods of aggressive growth and XLP offering valuable downside protection against downturns in the market.

Final Thoughts

After all things are considered, I believe that the Consumer Staples sector is likely to remain a safe haven for investors in the mid-term. It offers significant diversification and risk-reduction benefits, despite trading at somewhat pricey valuation multiples compared to the broader market. XLP also offers a desirable option for dividend-oriented investors.

Be the first to comment