Casanowe/iStock via Getty Images

Xerox Holdings Corp. (NASDAQ:XRX) had a disappointing 2022, but because of its dividend yield of 5.9% I still consider it a buy for investors seeking current income. Investors should not, however, expect some major turnaround that will drive the stock price significantly higher. Instead, I actually consider Xerox almost like a preferred stock that pays $0.25 quarterly. At one time I thought HP Inc. (HPQ) might buy Xerox, but I now consider that much less likely to happen.

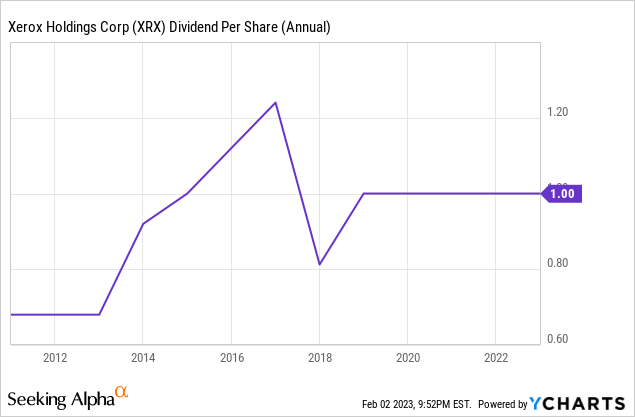

Xerox had a disappointing total return since I recommended the stock on March 14, 2022. Cost pressures from rising price and supply chain issues had a very negative impact on results, but 4Q results seemed to show a slight improvement in operations. I bought additional Xerox stock at significantly lower prices during 2022 as I averaged down my purchase price, which has resulted in a modest total return over the last twelve months. Carl Icahn also bought additional Xerox shares in April 2022 at $16.96-$17.17 per share bringing the total to 34,245,314 shares or a little over 22%. These shares are held at Icahn Enterprises (IEP) that yields a very high 14.8% distribution, which I recently wrote about.

Xerox and S&P Total Returns Since March 14, 2022

Buy Xerox for the 5.9% Dividend Yield

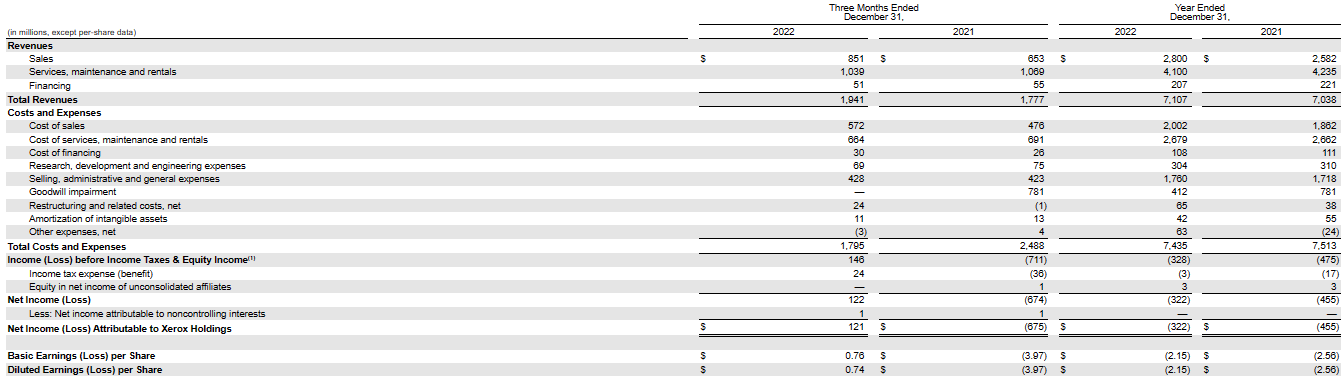

The primary reason why income seeking investors should consider buying Xerox is for the high dividend yield of 5.9%. This high yield helps support the stock price, but I think income investors should focus mostly on the dividend itself and not short-term stock price movements. As I noted in the introduction, I view Xerox as something akin to a preferred stock that pays a quarterly dividend of $0.25 and has the potential to eventually have the dividend increase in the distant future unlike a preferred stock that has a fixed dividend. Like a preferred stock, however, there is also no guarantee that the dividend will be declared in the future.

Often investors look at the annual dividend paid as a percentage of annual net income, which is the typical dividend payout metric, but I am going to use a different metric with Xerox. I am going to look at annual dividends compared to annual cash generated from operations since dividends are paid from cash and not from some GAAP accounting standard income statement. Starting back in 2018 it was 23.6%, then 18.2% in 2019, 42% in pandemic year 2020, 32.8% in 2021 as the economy began to recover. In 2022 it was 109.4% – a major yellow flag.

Part of the problem was caused by a $143 million increase in inventories and $141 million increase in finance receivables in 2022, but these two items were almost completely offset by a $278 million increase in accounts payable. So, the yellow flag remains. According to management’s latest guidance numbers for 2023, there should be $550 million cash from operations for 2023, but that includes about $200 million from the new FITTLE financing deal. (See below.) This guidance would imply a 28.4% payout in 2023 assuming quarterly dividends stay at $0.25 per share. The guidance for free cash flow was $500 million after deducting $50 million for CAPEX. Management also guided for revenue to be “flat to down low-single-digits in constant currency” to $7.1 billion with a $200 million profit, after adjustments.

The reality is that Carl Icahn may have significant influence on dividend payments. The $1.00 annual Xerox dividend kicks over $34.2 million into IEP’s cash position. IEP pays a $2.00 quarterly distribution, which currently results in close to a $2.7 billion annual distribution, but only about $158 million cash is paid. Most of the IEP distribution is paid in addition to IEP units. It would be inappropriate of me to even try to guess Icahn’s actions regarding Xerox and the dividend in an article, but I do think investors need to be aware of these numbers.

New Financial Deal Will Improve Their Financial Position

Xerox has a very high level of long-term debt of $2.866 billion at the end of 2022. According to the latest management conference call most of their debt is allocated to their FITTLE lease portfolio and the remaining $800 million of their debt is related to their other business areas. In early January the company announced a new financing deal with HPS Investment Partners. Under the financing agreement an affiliate of HPS buys “pools of receivables relating to non-consumer standalone equipment leases on a monthly basis”. Xerox will continue to “service the lease receivables for a specified fee and will also be paid a commission on lease receivables sold”.

This should have a significant positive cash flow impact for Xerox. Already Xerox is getting enough cash to pay off the $300 million 4.625% (interest rate was increased from 4.375% after credit rating was downgraded in early 2022) notes maturing in March instead of having to do some note refinancing transaction. It will be interesting to see if they can get enough cash from this new financing deal and cash from operations to pay the $300 million notes that mature May 15, 2024, without having to do a note refinancing transaction. If this new financing continues going forward it could greatly reduce Xerox’s financial leverage.

At the same time this new financing deal was announced, the company announced that their credit agreement was amended that reduced the bank’s revolving credit commitment by 50%. I don’t think this is a major issue because Xerox has not drawn on the revolver and may not even need this line of credit given that they also have this new financing deal.

The massive stock repurchases, in my opinion, have caused most of the financial problems Xerox has been facing. I am absolutely against stock repurchases. I think companies should paydown debt, increase CAPEX, and/or increase dividends instead of using cash to repurchase stock. Xerox used about $888 million cash in 2021 to repurchase stock and additional $113 million in early 2022. During 4Q they did not repurchase any stock and it does not seem that there is any current authorization to purchase stock. I think Xerox needs to get its finances in order and not repurchase any shares going forward. (Note: if there is a future announcement of the board authorizing stock repurchases, I will sell my Xerox shares.)

Recent Reported Results

The 4Q results continued to show increasing cost and supply chain problems along with weak demand because many workers still have not returned to offices. I saw a report on CNBC last week that in 10 major cities 50% of the office workers are now back in their offices. The reality is that Xerox needs more workers back in their offices because that is the company’s primary target market.

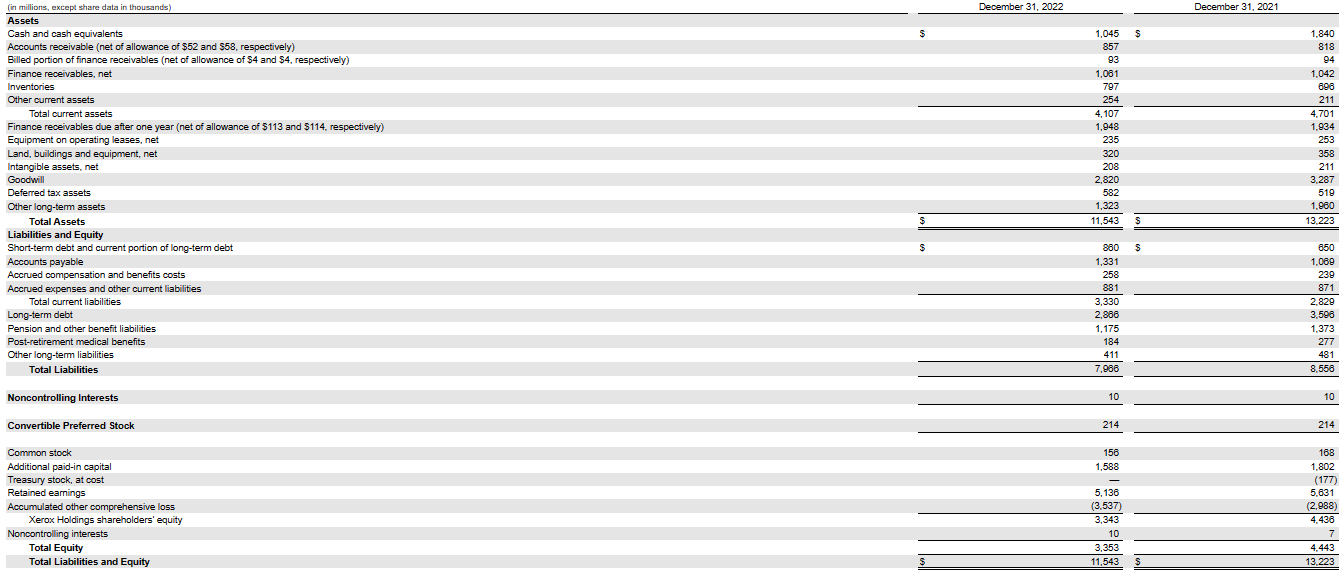

4Q and Annual Income Statement for 2022 and 2021

sec.gov

At least Xerox did not report any real surprises, which I guess is a positive given the current market. The reported GAAP EPS numbers for fiscal 2022 include $2.54 goodwill impairment charge that was taken in 3Q. The adjusted 2022 EPS was $1.12, which was down $0.39 from the prior year. Using the $1.12 adjusted number and the current stock price of almost $17, Xerox trades at a 15x P/E.

Year-End Balance Sheets 2022 and 2021

sec.gov

FUJIFILM Issue

These issues have been covered by others in prior articles, but I think they are important to remember in valuing Xerox. FUJIFILM Business Innovation Corp. is both a major Xerox supplier, but now is also a competitor. It is a division of FUJIFILM Holdings Corp. (OTCPK:FUJIY). According to numbers in the February 2022 10-K filing Xerox estimated it would make purchases of $1.18 billion from FUJIFILM in 2022, which is a high percentage of Xerox’s total costs for the year.

After their prior deal was terminated, FUJIFILM was able to compete in the entire global economy. According to a November 2022 press release for their 2Q, FUJIFILM Business Innovation Corp. had a 6.7% revenue increase and 17.5% increase in operating income for the quarter. A statement that caught my eye was “leading to growth in exports of multi-function devices, printers and consumables mainly to the U.S. and Europe”.

The problem that has been asserted by some is that FUJIFILM will most likely be very competitive in the U.S. taking market share from Xerox, but Xerox may not be able to be very competitive against FUJIFILM in the faster growing Asian market. Some have responded that people often say “xerox this”, but nobody states, “FUJIFILM this”. This is an issue that needs to be followed by investors.

Conclusion

Fifty years ago, Xerox was one of the top growth stocks Wall St., but now it is perceived by many investors as a dying company and is ignored by many. Those seeking high income, however, love their dividends. I consider Xerox a buy mostly because of the relatively high dividend yield of 5.9%. With the new FITTLE financing deal with HPS Investment Management, the $0.25 quarterly dividend has become safer, in my opinion.

Increased competition from FUJIFILM and potential for a relatively low return to the office becoming the new status quo are the two major headwinds facing Xerox. While people need less paper/printing/copying because they write/report/store items on computers, there will always be a need for paper materials. Xerox is not dead.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment