kali9/E+ via Getty Images

Hell is truth seen too late.”― Thomas Hobbes, Leviathan

Today, we take our first look at a small cap concern called Wrap Technologies, Inc. (NASDAQ:WRAP). The company and its stock has had its share of challenges over the past few years. Wrap Technologies installed new management last year who laid out a strategic roadmap that seems to have some promised. Do brighter days lie on the horizon? An analysis follows below.

Seeking Alpha

Company Overview

Wrap Technologies, Inc. is based just outside of Phoenix in Tempe, AZ. The company develops policing solutions for law enforcement and security personnel.

August Company Presentation

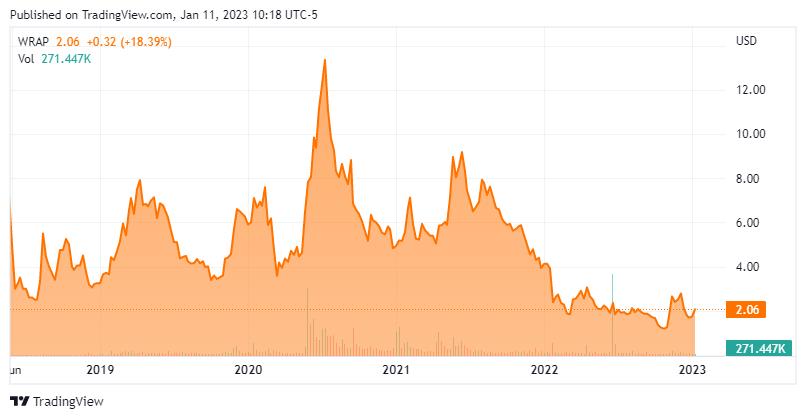

Wrap Technologies’ primary asset/product is called BolaWrap 150. This is a hand-held remote restraint device that discharges a Kevlar cord to restrain noncompliant individuals from a range of 10-25 feet. The stock currently trades just around two bucks a share and sports an approximate market capitalization of $80 million.

August Company Presentation

The company also offers Wrap Reality which it describes as:

A virtual reality training system, is a fully immersive training simulator and comprehensive public safety training platform providing first responders with the discipline and practice in methods of de-escalation, conflict resolution, and use-of-force to better perform in the field.”

August Company Presentation

However, the BolaWrap 150 is its primary product offering.

Third Quarter Results

On November 9th, the company posted third quarter numbers. Wrap Technologies had a GAAP loss of nine cents a share as revenues fell just under six percent on a year-over-year basis to $1.7 million.

The company did note that:

- Trained law enforcement agencies grew to more than 1,300, up 39% from the same period a year ago

- Certified officer instructors grew to nearly 4,400, a 36% increase from 3Q2021

The company ended the quarter with a non-existent backlog but signed an initial $1.5 million agreement in October with a very large police agency in the EMEA region. The company also announced a deal with a law enforcement agency in South America during the fourth quarter that consisted of 120 BolaWrap 150 remote restraint devices including provisions for cassettes, holsters, and training services.

Wrap Technologies announced both a new CEO and a new president for the company in April of last year. The was followed by the appointment of a new CFO in July. New management has laid out a new strategic roadmap that will focus on reducing expenses and expanding international sales with the goal of achieving profitability by 2024. Wrap Technologies did reduce quarterly operating expenses by $2 million in the third quarter compared to the same period a year ago, it should be noted.

Analyst Commentary & Balance Sheet

All three analyst firms (Northland Securities, Maxim Group, Ladenburg Thalmann) currently have hold ratings on the stock. Price targets proffered range from $2.10 to $2.50 a share. Approximately 10% of the outstanding float is currently held short. The company ended the third quarter with just under $24 million worth of cash and marketable securities on its balance sheet. The company posted a $3.9 million net loss in the quarter. Wrap Technologies has no long term debt.

There has been a noticeable uptick in insider buying in recent months. Several insiders bought nearly $350,000 worth of stock in November and December of last year. Prior to this, there was no insider activity in the stock at all in the preceding six months.

Verdict

The current analyst firm consensus has the company losing 41 cents a share in FY2022 on nearly $8 million in revenues. Sales are projected to more than double in FY2023 to $18 million while losses drop to approximately a quarter a share.

August Company Presentation

In theory, the company should be operating in a favorable environment. The George Floyd incidents of May of 2020 as well as the riots that followed, put a renewed focus on developing non-lethal tools and processes for law enforcement.

August Company Presentation

Unfortunately, despite some 800 police agencies in the United States having BolaWraps as well as over 50 countries, sales have been lacking and the product can have a long sales cycle. New management seems to be making some progress on the expense side and expanding international sales. However, at the current burn rate, the company only has six quarters of funding in place.

August Company Presentation

Obviously, if sales pick up in 2023 as analysts project, the burn rate should be reduced, especially if new management continues to make progress on the cost front. It is also encouraging to see some insider buying in the shares. That said, I would wait to see if management’s strategic roadmap gains further traction in the quarters ahead before I would make any investment in WRAP at these levels.

The truth is like salt. Men want to taste a little, but too much makes everyone sick.”― Joe Abercrombie, The Heroes

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment