Windstream (OTCPK:WINMQ) (“Win”) and Uniti (UNIT) recently settled their lawsuit that started in June 2019. As a result, Uniti transfers over a billion dollars of value to the Win creditors and the future shareholders. The settlement will cost Uniti five to ten dollars a share.

This article starts with an update on a previous article with the title “Windstream/Uniti Settlement: Better Than Expected”. Well, with some more details, we may have to change our mind: “Worse than expected”. Thereafter, we take a look at the value of the shares of Uniti. The last section discusses the problems arising from the settlement with respect to the 2030 lease renewal negotiations.

Win/Uniti settlement

The following list is almost a copy from this previous article, and the details can best be read there.

The settlement has five major aspects:

- Transfer of lease contracts generating a total of 30 million EBITDA.

- Issuance of 20%, or 38.6 million, of Uniti shares to certain investors.

- Transfer of dark fiber and the termination of exclusivity on certain of the lease assets.

- Equipment loan.

- Commitment to fund Growth Capital Improvements (GCIs).

The Big Stinker

One aspect that turned out to be very different from last analysis is around point 2, the stock issuance. It turns out that certain debtors, among which was the oligarch Paul Elliot Singer of Elliot Capital, negotiated for themselves a private transaction under which they will purchase Uniti shares at a price far below market. The Uniti shares are not even transferred to the bankrupt estate of Win to compensate all stakeholders, they go directly to these investors.

Regarding the strangely low stock price, Uniti has this to say:

at $6.33 per share, which represents the closing price of Uniti common stock on the date when an agreement in principle of the basic outline of the Settlement was first reached

So, these insiders are allowed to purchase 38 million Uniti shares at $6.33 per share while the price by the time of signing of the document was already $10.33, four dollars or $155 million higher.

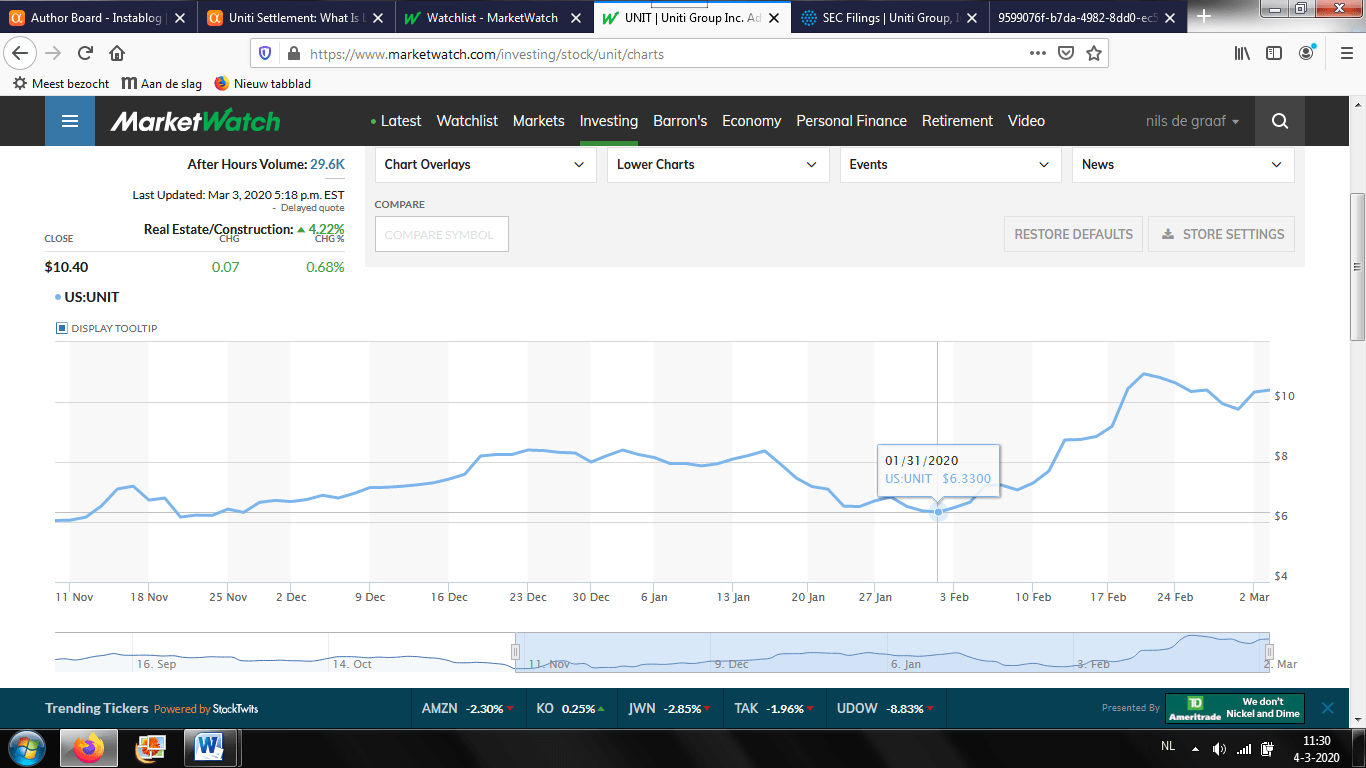

Let’s have a look at the price chart of Uniti stock during the period of the negotiations. The chart shows the period from when the first round of mediations broke off, 12 November last year, until now. We can assume the new round of negotiations started somewhere in December or January.

{kind=link}

This $6.33 share price turns out to be the lowest closing price over the last three months. So, that “date when an agreement in principle” was negotiated turns out to be, totally by coincidence of course, the lowest closing price in months. Who believes that? Or why was that “agreement in principle” day, 31st January, even relevant? They signed the contract over a month later, March 2nd.

The problem with this “Big Stinker” is not only that Uniti transfers hundreds of millions of value to “certain investors”. The bigger problem is that Uniti showed how weak it perceived its negotiation position was.

This expensive settlement forecasts problems for Uniti at renewal in 2030. Before we get there, we have to understand why the company signed this rather humiliating agreement.

Why the settlement?

A very important question is why Uniti settled at the cost it did. First the costs:

- Issuance of 38 million shares below fair value: at least $150 million.

- Cash settlement payment of $400 million.

- Tenant improvements (GCIs) at a net cost of $1 billion.

That sums up to $1.55 billion, or 32% of shareholder value (at $25 a share). In present value terms, Win has this to say in a recent court filing:

Based on the analysis of the Debtors’ financial advisors, consummation of the Uniti Transactions will result in transfer of more than $1.2 billion in value to the Debtors’ estates.

Regarding tenant improvements, note that in the original contract, it was Windstream that was supposed to pay for these investments. Uniti paid $7.45 billion for the lease assets under the contract, and part of that sum was paid to replace copper for fiber cables. With the new contract, Uniti is basically paying twice. If the current GCI approach was already in the original contract, then the investors would have been prepared to pay only hundreds of millions less.

Now, why did Uniti settle? Let’s briefly look at the possible explanations for the costly settlement:

- Win could have rejected the lease.

- Win could have run down the Uniti assets until obsolescence.

- Win could have won the trial.

- Uniti management is weak or corrupt.

1. Rejecting the lease

Especially the SA posters have discussed extensively whether or not Win was in the position to reject the lease contract. The jury is still out, and we may never know the answer. What we do know, however, is that Win had the chance for over a year to reject the lease and never did that. It continued paying the full monthly lease instalments.

In the last section, we will see that if lease rejection indeed was a plausible explanation, then this does not bode well for Uniti in the future. At renewal in 2030, Win will be in an even stronger position to reject whatever portion of the lease it doesn’t like.

2. Run down the assets

A more likely explanation is that Win threatened not to further invest in Uniti’s assets. It is likely that the Uniti assets then would have had far less value by the end of the lease in 2030 than originally expected. The GCIs in the settlement solve this problem and look, at first glance, reasonable from a business perspective from either side of the table.

However, the Big Stinker has nothing to do with this problem. Why was that in the settlement package? And why was there another $400 million settlement payment?

3. Win could have won

In the past, we looked closer at the lease contract – here, and here – and we could comfortably conclude that Uniti had a very strong lease contract in hand. There was no possible way that the judge would recharacterize the lease as a loan. Maybe the strongest argument was that you simply could not come up with a reasonable interest rate on the alleged loan. The lease as a loan simply did not work. In short, Win could not have won.

4. Uniti management is weak or corrupt

Uniti shareholders will transfer over a billion dollars of value to the Win creditors, the new shareholders of Win and directly into the pockets of certain oligarchs and bankers. So far, we haven’t seen a proper justification from Uniti.

During a recent conference at Morgan Stanley, Uniti completely ignored the issue and stated that the settlement was “mutually beneficial”. A settlement that costs shareholders 1.5 billion in value, or over 30% of the company, is not mutually beneficial, as reflected in the current stock price. Shareholders should be prepared to take action if no satisfying answers are forthcoming.

Why the settlement: Conclusion

Maybe management hasn’t yet told us the entire story. Uniti has to answer the questions of why it settled at such humiliating terms and where that perceived weakness came from. The $1.55 billion cost is very high, and would have been high even if Uniti entirely lost the court case. Remember, the company had a first lien security right over the lease assets.

But Uniti didn’t go to trial. It lost already before it went to trial. Without knowing why Uniti settled at such terms, we cannot know whether it is still a viable investment opportunity. In the last section, we will see why.

The value of Uniti after the settlement

In this section, we will look at what is left from Uniti after it gave away so much value. First, we summarize the various agreements, and then, we calculate the cash flows and expected dividends over the coming years.

To summarize the cash and stock impact of the various aspects of the settlement:

- Uniti pays $40 million upfront for contracts generating $8 million of annual EBITDA.

- Uniti offers 38.6 million shares for $21 million of EBITDA and some fiber.

- Uniti pays $432 million one year after closing of the settlement.

- Uniti will fund GCIs: $125 million in 2020, $225 for the next four years, then $175 million for two years and $125 million for the last three. With a one-year delay, Win will pay 8% interest until 2030.

With respect to point 3, the settlement amount is basically $400 million but can be paid in quarterly instalments over five years. The remaining balance will, however, carry an interest rate of 9%, which is expensive. In the below analysis, we assume that Uniti will redeem the outstanding amount as soon as allowed by the contract, which is one year from signing.

Uniti cash flows available for dividend

In this section, we are going to estimate the value of Uniti shares. To do so, we calculate the cash flows available for distribution to shareholders. We assume that all the above investments and settlement payments are going to be funded by retained earnings or the issuance of new shares.

The below table in the last column shows for each year the cash available for dividend after paying all costs and GCIs. The table ends with 2029, the last full year of the master lease contract. In the next section, we look at 2030 and beyond.

The second column shows the FFO, which stands for funds from operations, basically free cash flow before capital investments. The third column is the FFO minus the investment in that particular year, the GCIs, plus the rent on the GCIs. Also subtracted in the first year is the $40 million fiber investment and one instalment, $20 million, of the $400 million payment.

In the second year, we assume that the remainder of the $432 million settlement will be paid with the issuance of new shares. That is why you see the number of shares go up in 2021. The issuance price is assumed to be $13 per share.

|

We see that the cash available for dividend goes up over time as the GCIs start generating rental income. From this table, we can learn that Uniti is able to pay a dividend of one dollar per share in 2020. Thereafter, the dividend may go up.

Present value of Uniti

The above approach makes it possible to calculate the value of Uniti shares. Since we have the amounts that can be distributed to the shareholder for a very long period in the future, we can calculate the discounted value of that income stream.

In order to do that, we need to make some assumptions. First, we assume no further growth of the company. We assume Uniti will continue to earn what it currently earns until 2030. As per 2030, for the master lease we assume the value will be as calculated by E&Y in 2015, plus all tenant capital improvements and GCIs at cost. We expect these assets will then generate 9% for the next five years and zero thereafter. Note that this results in an assumed total value of the lease assets in 2030 of 4.15 billion versus 7.45 billion in 2015.

How does the income stream look?

|

Year |

FFO |

Free CF |

PV CF |

CF/share |

PV CF/share |

|

2020 |

420 |

235 |

235 |

1,01 |

1,01 |

|

2021 |

485 |

260 |

245 |

0,99 |

0,93 |

|

2022 |

506 |

281 |

250 |

1,07 |

0,95 |

|

2023 |

527 |

302 |

254 |

1,15 |

0,96 |

|

2024 |

549 |

324 |

257 |

1,23 |

0,97 |

|

2025 |

571 |

396 |

296 |

1,50 |

1,12 |

|

2026 |

588 |

413 |

291 |

1,57 |

1,10 |

|

2027 |

607 |

482 |

320 |

1,83 |

1,22 |

|

2028 |

620 |

495 |

311 |

1,88 |

1,18 |

|

2029 |

635 |

510 |

302 |

1,93 |

1,14 |

|

2030 |

432 |

432 |

241 |

1,64 |

0,92 |

|

2031 |

183 |

183 |

96 |

0,69 |

0,36 |

|

2032 |

184 |

184 |

92 |

0,70 |

0,35 |

|

2033 |

186 |

186 |

87 |

0,71 |

0,33 |

|

2034 |

188 |

188 |

83 |

0,71 |

0,32 |

|

2035 |

190 |

190 |

79 |

0,72 |

0,30 |

|

Sum |

6.872 |

5.062 |

19,32 |

13,17 |

The first three columns are the same as in the previous table. We added a present value of these cash flows based on a discount rate of 6%. This 6% seems rather low, but remember that we didn’t assume any growth, and we assume the debt funding costs remain elevated, which will not be the case. On the other hand, these cash flows are to a large extent already agreed upon under existing contracts, so the uncertainty is rather low.

In the last column, we see that the present value of all cash flows adds up to $13 a share. You can regard this as the value of the current shares. If you want to add value from the residual value of the company in 2035, you may add $0.30/6%, or $5 a share (the present value of the perpetual income stream of 72 cents, 30 cents current, as per 2035).

Negotiations master lease at renewal date

In this section, we look at the Win/Uniti relationship at lease renewal in 2030. How will the Growth Capital Improvements influence the lease renewal negotiations around 2030?

Uniti agreed to pay 1.75 billion of GCIs starting in 2020 and ending in 2030, right before the first term of the lease contract. At renewal, Win has the option to divide the lease into 36 contract areas and may continue with any of the areas that it likes, and consequently, may drop any area that it doesn’t like. That is what we call in finance a call and a put option.

The put option

Win already had this put option, but with the GCIs, the value of the put has become far more valuable. It is important to note that the original lease contract did not have these GCIs in the contract up until the end of the contract in 2030. In the original contract, there was, however, a Uniti funding commitment of Tenant Improvements (TIs), but that ultimately ended in the seventh year of the contract. There was even a condition that if Uniti funded these TIs, the contract would be automatically extended with five years. So, in the original contract, the Uniti-funded investments had a remaining life, and generated rental income, of at least thirteen years.

What we now have is Uniti investing in fiber, and doesn’t know whether these investments will be a success and will be rented out for a long period. Let’s assume Win builds new fiber in 2025 in a certain area and the income generated by these investments turns out to be far lower than expected. Will the company renew this contract area in 2030? At what rent level?

If you think this through, you will see that Win is in a strong position to lower the rent in unsuccessful areas. With this option, the investment risk entirely shifts towards Uniti. Uniti does not get sufficiently rewarded for this at eight percent rent for only a few years.

(You may argue that Win cannot drop these areas due to telecom legislation. Well, we have seen how strong that argument was in the recent settlement negotiations. And that was about the entire contract, not 1/36th at a time.)

The call option

Is the opposite also true? Will the rent rise dramatically for those areas where the income is higher than expected? We cannot be optimistic, as Win has a renewal option, which is basically a call option. In the current master lease, the rent is based on cost accounting. So, the rent is derived from the investment costs plus inflation minus depreciation. We can expect that same method will be applied to calculate the rent in 2030. That means the upside is for Win.

Negotiations renewal: Conclusion

It looks like Uniti did not carefully think through the settlement contract it just signed. Any landlord that is prepared to invest on behalf of its tenant requires and expects a sufficiently long period of rental income to earn back its investment. Uniti should at least have required a lease extension of five years, if not longer. This lease extension was in the original contract, and it is puzzling why the company gave this up. The current contract shifts the upside to Win and the downside to Uniti.

Conclusion

Even with a strong lease contract in hand, Uniti has proved to be a weak partner in the negotiations with Windstream. Many of the settlement terms are very costly for Uniti. The private stock issuance at $6.33 a share, the lowest closing price in 2020, is an outright humiliation. Uniti management transferred $1.5 billion of value to Windstream. Its shareholders lost many dollars a share, and Uniti stock may now be worth only $13-18 a share.

The current settlement is not the end of the trouble for Uniti. The draft proposal creates new issues that may cause serious uncertainties at contract renewal in 2030. This will affect both shareholders and bondholders.

One of the glaring omissions in the lease contract is that Uniti didn’t obtain an extension with at least five years. The current draft makes the company vulnerable for even tougher multi-billion dollar negotiations in 2030. Uniti’s current weak management and/or weak position do not bode well for the future.

Disclosure: I am/we are long UNIT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment