Pekic

Upstart Holdings (NASDAQ:UPST) showed promising prospects in the personal lending market, but the extent its business has collapsed in the past few quarters is quite worrisome. If the economy enters into a recession, it may not survive in the coming months, with upside coming mainly from a potential buyer that may be interested in its technological capabilities.

As I’ve analyzed in a previous article, I saw Upstart as an interesting long-term play in the Fintech industry, even though its business model still had some question marks, as the company’s operations haven’t faced an economic downturn throughout its history.

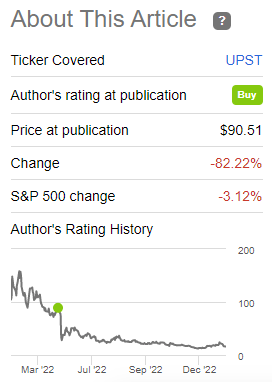

Unexpected at the time, the company’s operating backdrop has deteriorated rapidly since my last article, and Upstart’s share price has been on a severe downtrend over the past few months. Its current market value is just about $1.3 billion, compared to more than $6 billion at the time of my previous article.

Share price performance (Seeking Alpha)

This terrible performance is justified mainly by Upstart’s woes, with its operating performance being hit rapidly by rising interest rates and tighter funding conditions from its banking partners, which led to much lower revenue in the past few quarters and operating losses since Q2 2022.

The company has released today its Q4 and full year 2022 results, thus I think it is now a good time to revisit its investment case to see if Upstart is now undervalued after a strong share price decline in recent months, or if its business model has structural issues that aren’t easy to fix and therefore its current valuation is justified.

Earnings Analysis – Q4 2022

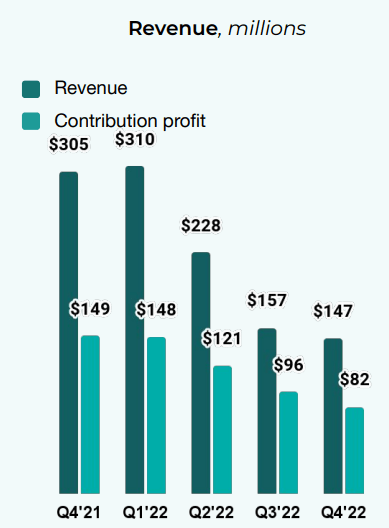

Upstart reported its Q4 2022 financial figures, with revenue coming at $147 million, which was slightly above its guidance of revenue between $125-145 million, but a decline of 52% YoY. This was above consensus estimates of $134 million, while its net loss of 25 cents per share also beat the loss of 47 cents per share expected. Its adjusted EBITDA was ($16.6) million, also better than its guidance of ($35) million, and its net loss in the quarter amounted to $55 million (vs. guidance for a net loss of $87 million.

While these revenues and earnings were better than expected, expectations were quite low and the company continued to report a weak operating trend, as revenue and earnings declined sequentially compared to the last quarter.

Revenue (Upstart)

Upstart’s business model is based on its cloud-based artificial intelligence (AI) lending platform, to improve access to credit while reducing the risk and cost of lending for banking partners. Its goal is to be a ‘technology company’ rather than a financial institution, which means that it aims to originate loans through its platform, but its goal is not to maintain those loans on its balance sheet.

This business model works during periods of low interest rates and easy access to funding, with the loans issued through Upstart’s platform being financed mainly in three ways: retained by the originating banking partners, distributed to investors, or retained in Upstart’s balance sheet. During 2021, some 80% of the loans issued through its platform were bought by institutional investors, while 16% were retained by the originating bank, and only a small part of loans were funded by Upstart itself.

However, this backdrop has changed in recent quarters, with banking partners and investors being more risk-averse and less willing to finance personal loans.

Not surprisingly, Upstart’s loan origination volumes have decreased considerably compared to the same period of the previous year, leading to a significant drop in revenue and earnings. This happens because Upstart’s major revenue stream is fees paid by banks, which can be referral fees for each loan referred through its website and originated by a bank partner, platform fees for each loan originated, and loan servicing fees as consumers repay their loans.

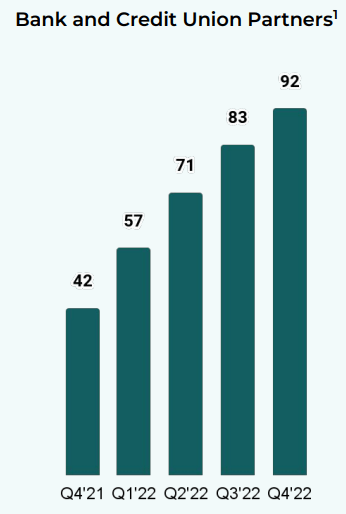

This trend is quite worrisome given that its total number of bank and credit union partners has consistently increased over the past few quarters, which means existing partners are less willing to fund loans, putting the company in a difficult position. Indeed, the total number of bank and credit union partners amounted to 92 at the end of 2022, being a new record.

Partners (Upstart)

Despite a higher number of partners, Upstart has reported much lower loan volume in recent quarters. This happens due to a combination of several factors, including higher interest rates that led to lower demand for personal loans, tighter funding conditions for banking partners that make the loan economics less interesting, plus higher loan defaults than its models were expected.

In 2022, Upstart’s revenue was $842 million, a decrease of 1% from the previous year, while its initial guidance for the year was to generate revenue of about $1.4 billion, representing annual growth of 65% YoY. This clearly shows how fast Upstart’s fundamentals and operating performance deteriorated in recent quarters, and how it was completely unexpected by its management.

This weaker top-line performance has, not surprisingly, led to operating losses, while in the previous year it has reported a net profit of $135 million. This happened due to lower revenue, but also by higher operating expenses (+35% YoY to $956 million).

This shows that Upstart has not adjusted its cost base to lower loan volumes, putting itself in a tough situation to return to profitability. Moreover, in a strong signal that operating momentum has not improved in the beginning of 2023, Upstart has recently announced deeper cost cutting measures.

To reduce operating expenses in a meaningful way, Upstart has recently announced a layoff of about 365 people, or 20% of its workforce, and also suspended the development of its small-business loan product, until macroeconomic conditions improve. While this will help the company to save about $100 million in annual expenses, both from staff costs and share-based compensation trough 2025, it is a sign that a rapid recovery in volumes is not expected and further losses are likely ahead.

Another negative factor was the company’s rapid cash burn, given that it had a strong balance sheet twelve months ago, but its weaker operating performance led to a cash balance of $532 million at the end of 2022, while it had more than $1 billion in liabilities. At the end of 2021, Upstart had a net cash position that enabled it to announce a share buyback program, a financial profile that has changed dramatically during 2022.

More worrisome than its weak operating performance in the past few quarters, was it very weak guidance for Q1 2023. Upstart expects to generate about $100 million in revenue in Q1, while the market was expecting some $158 million, and its adjusted EBITDA is expected to be a loss of $70 million (vs. loss of $12 million estimate by sell-side analysts). This clearly shows that Upstart’s performance is not expected to reverse soon, increasing investors’ doubts about the sustainability of its business model.

Medium-Term Estimates & Valuation

Regarding the company’s medium-term prospects, investors should note that current estimates have a high degree of error as uncertainty is quite high right now. Indeed, when I last analyzed Upstart the market was expecting the company to achieve some $3.5 billion in revenue by 2025, this estimate is now at just only $1.4 billion.

This shows how estimates can change quite rapidly, as the business performance also deteriorated quite rapidly, and should be taken with a grain of salt. Nevertheless, according to analysts’ estimates, Upstart is only expected to generate $712 million in revenue during 2023, and recover to $945 million by 2024, and $1.4 billion by 2025. Based on GAAP figures, the company is only expected to return to profit by 2025, to a net profit of about $95 million.

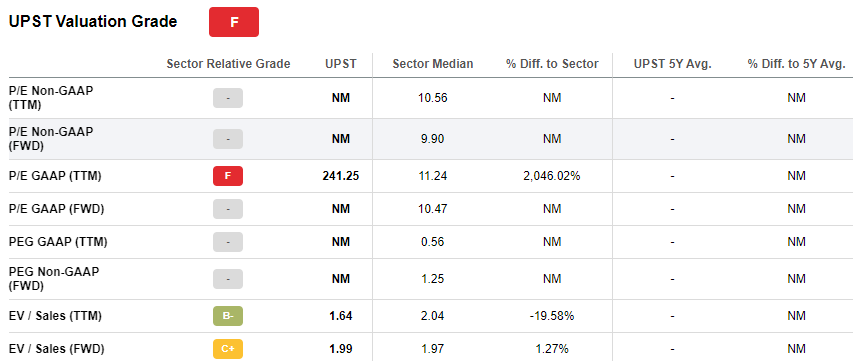

Regarding its valuation, as the company is now reporting losses the only metric that has some meaning is EV/revenue. Upstart is now trading at some 2x forward revenue, which may seem low, but the company has fundamental issues that investors should not overlook and therefore, I think at this point its valuation is highly speculative.

Valuation (Seeking Alpha)

Conclusion

Upstart’s AI-powered approach to lending seemed to be quite disruptive in the financial industry, but recent performance has shown that its business model has serious problems. If the company maintains its business approach, I have doubts that it will survive the current downturn. It is burning cash quite fast and a quick reversal doesn’t seem likely.

For its business model to work, it needs to take deposits to finance loans to retain in its balance sheet, as during market downturns its approach simply doesn’t work. Therefore, I think its business prospects are quite uncertain right now, and upside comes mainly from a potential takeover approach from a banking institution that may want to integrate Upstart’s technological capabilities within a ‘traditional’ banking model.

Be the first to comment